Downloaded 26 times

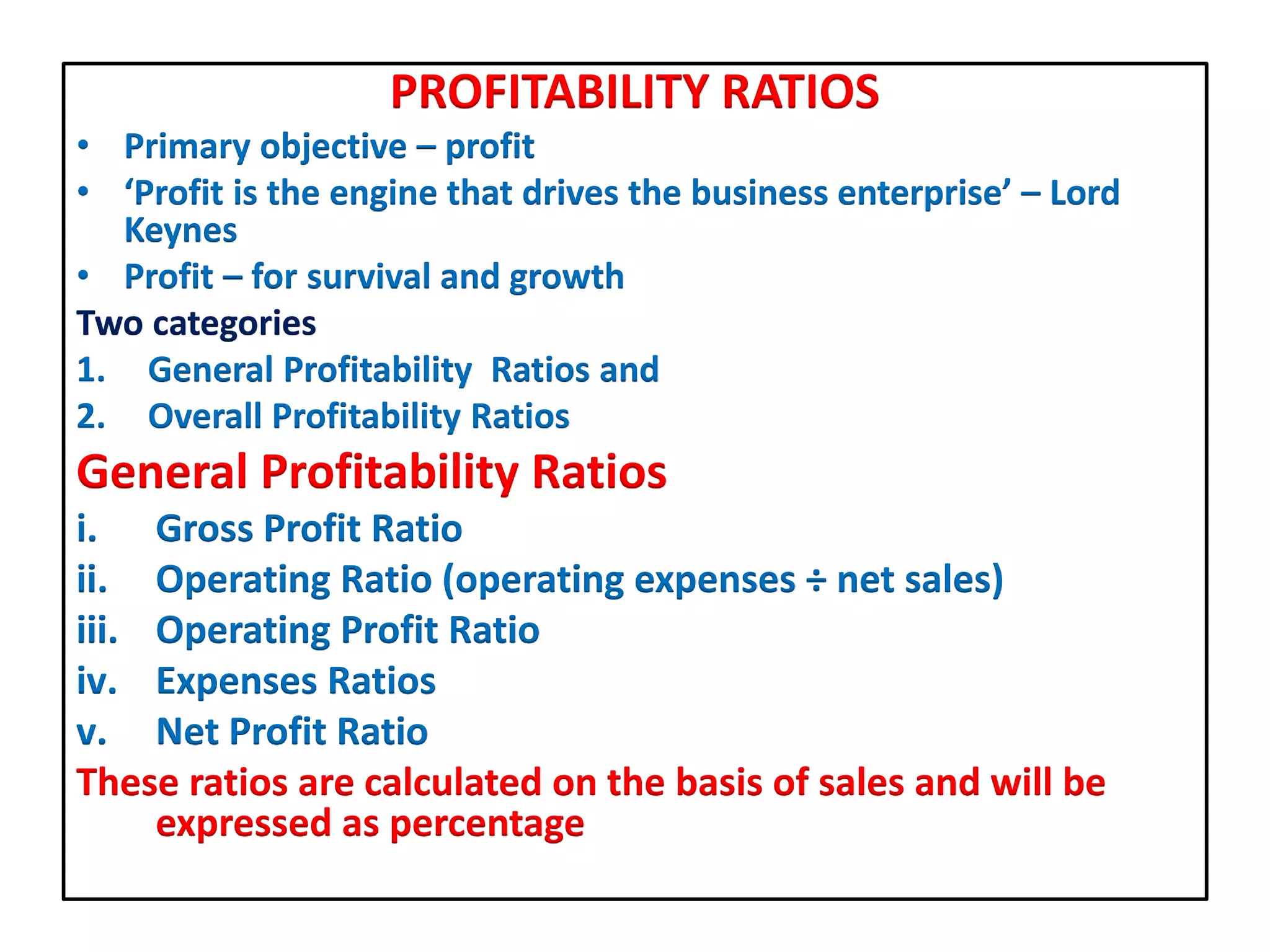

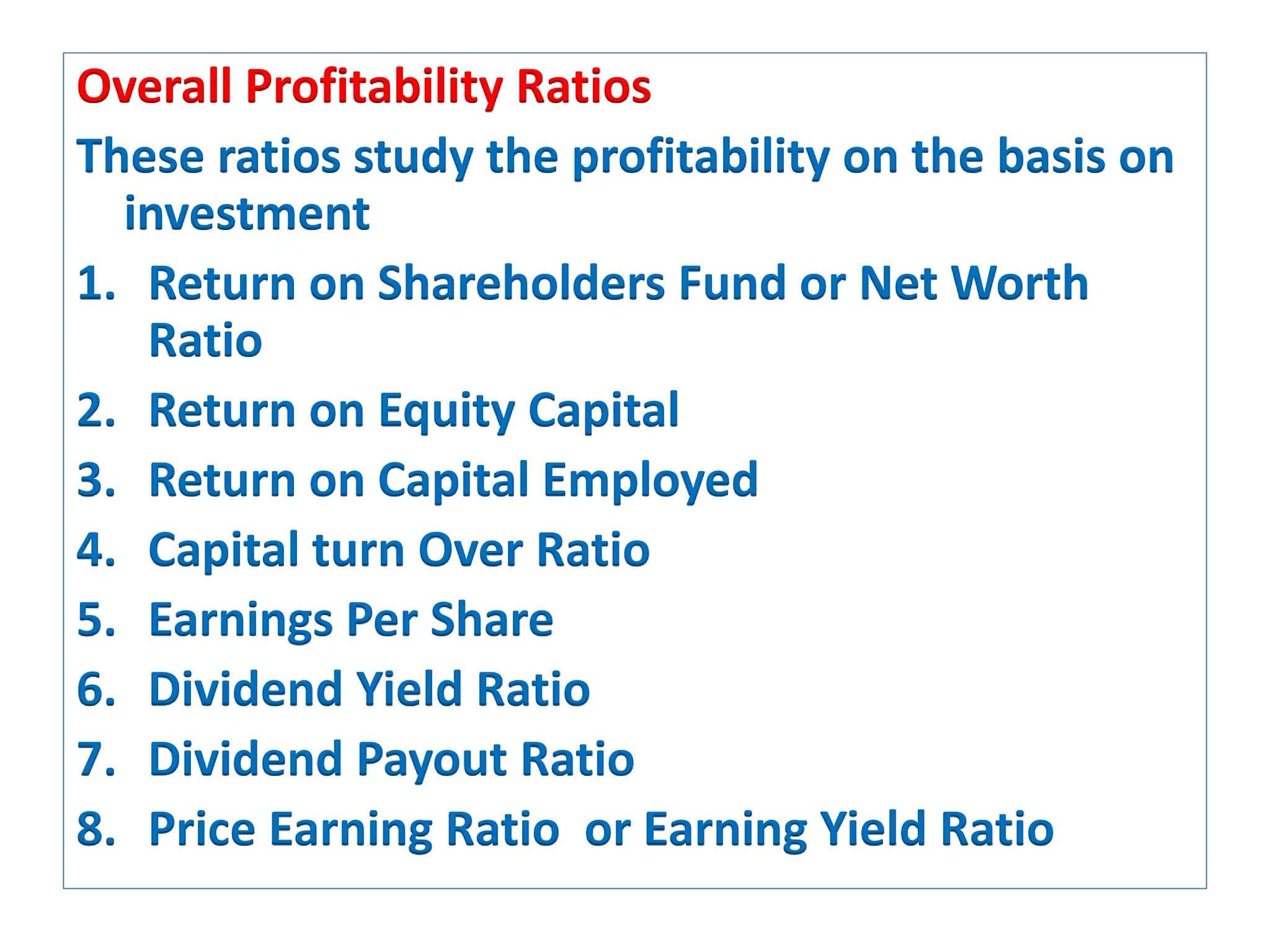

The document by Dr. Mohamed Kutty Kakkakunnan discusses profitability ratios, emphasizing their importance for business survival and growth. It categorizes these ratios into general and overall profitability ratios, detailing various formulas and definitions for calculating them based on sales and investments. Key ratios include gross profit ratio, return on equity, and capital turnover ratio, which measure efficiency in capital usage.