Download as PDF, PPTX

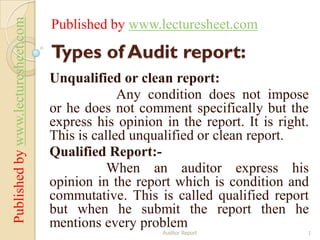

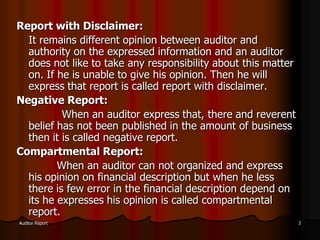

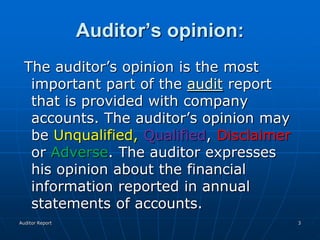

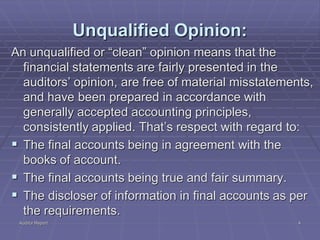

The document discusses different types of audit reports that can be issued by an auditor: - Unqualified or clean report is issued when no issues are found during the audit. - A qualified report is issued when the auditor has reservations but the financial statements are still fairly presented subject to the auditor's qualifications. - A disclaimer is issued when the auditor is unable to express an opinion due to limitations or uncertainties. - An adverse opinion is issued when the financial statements are materially misstated. - A compartmental report is issued when the auditor can express an opinion on some but not all aspects of the financial statements.

![AUDIT REPORT [ AUDITING ]](https://cdn.slidesharecdn.com/ss_thumbnails/auditingtypesofauditreport-210303052610-thumbnail.jpg?width=640&height=640&fit=bounds)