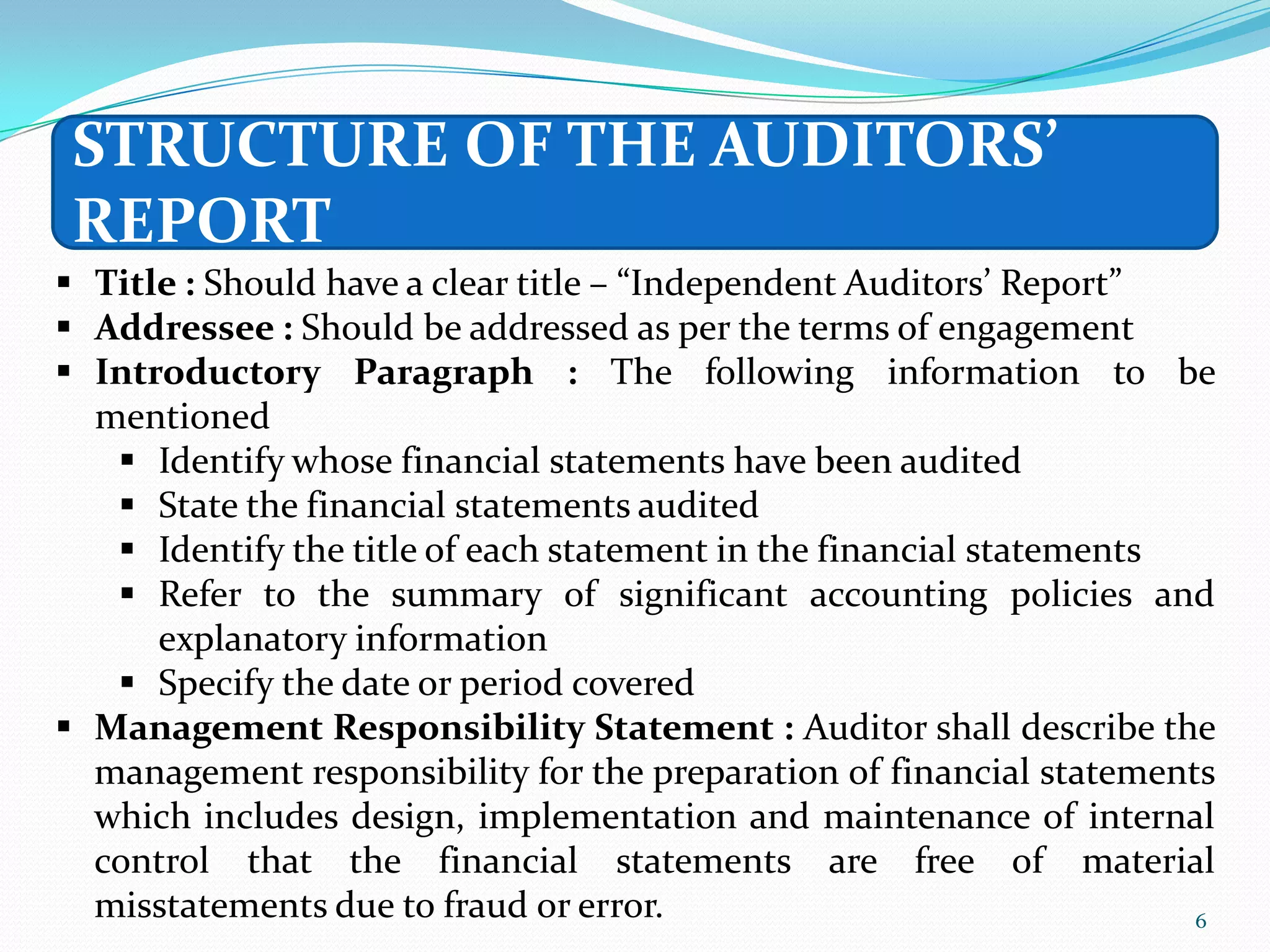

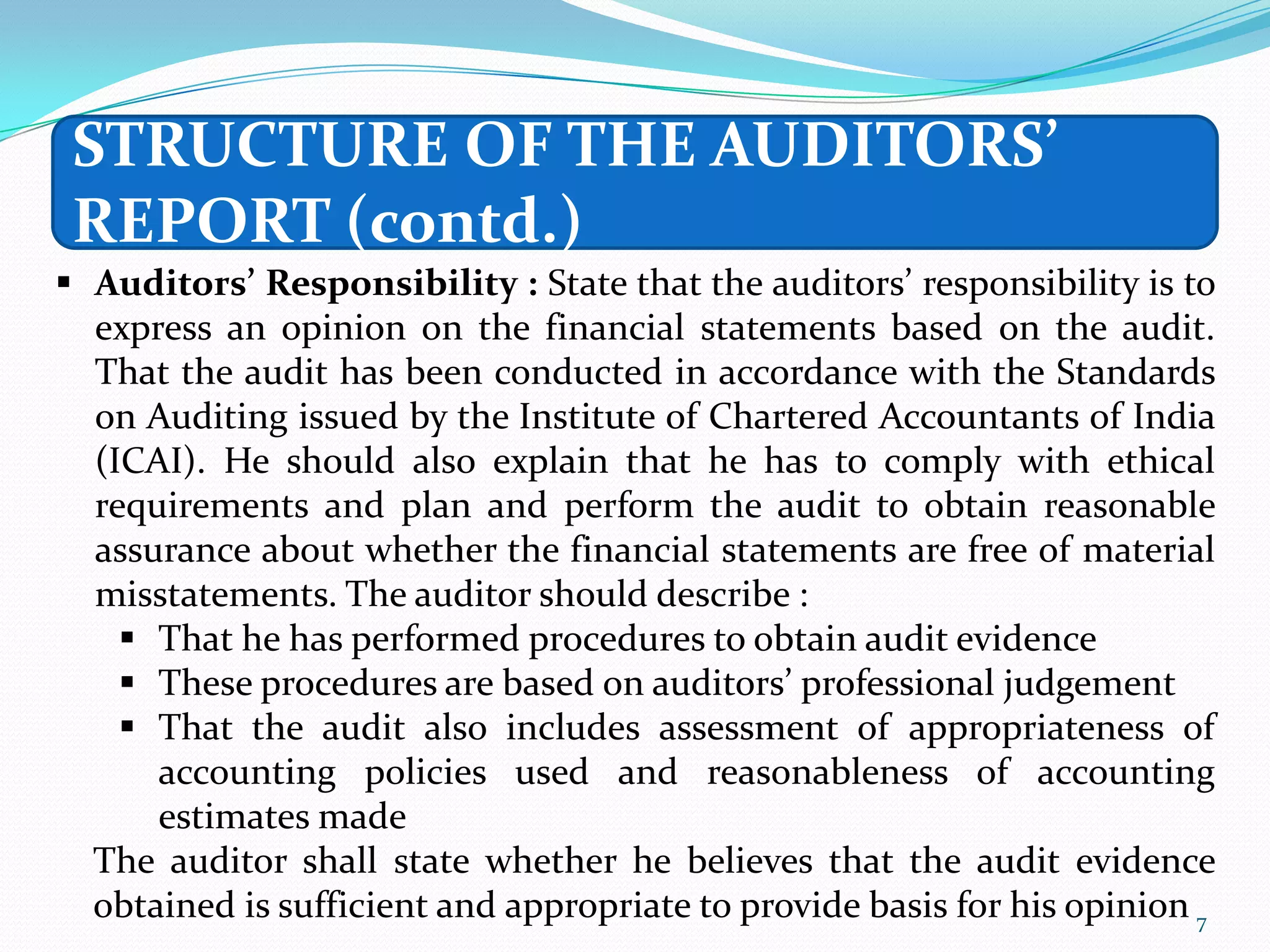

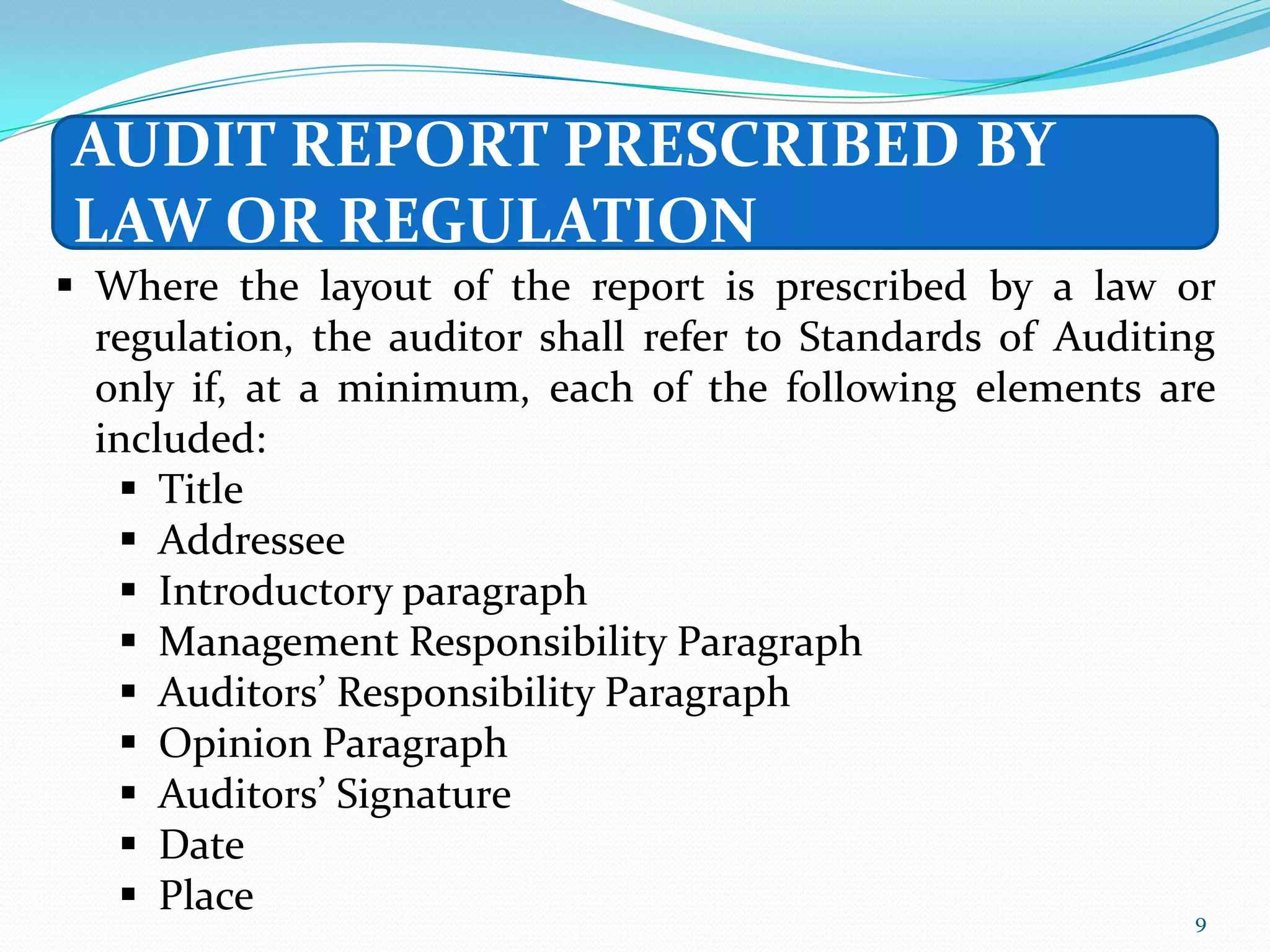

The document summarizes standards on auditing (SA) 700 and SA 705 regarding forming an opinion on financial statements and reporting.

SA 700 deals with the auditor's responsibility to form an opinion on financial statements and the structure of the audit report. It requires the auditor to evaluate accounting policies, estimates, disclosures, and determine if statements are free of material misstatement.

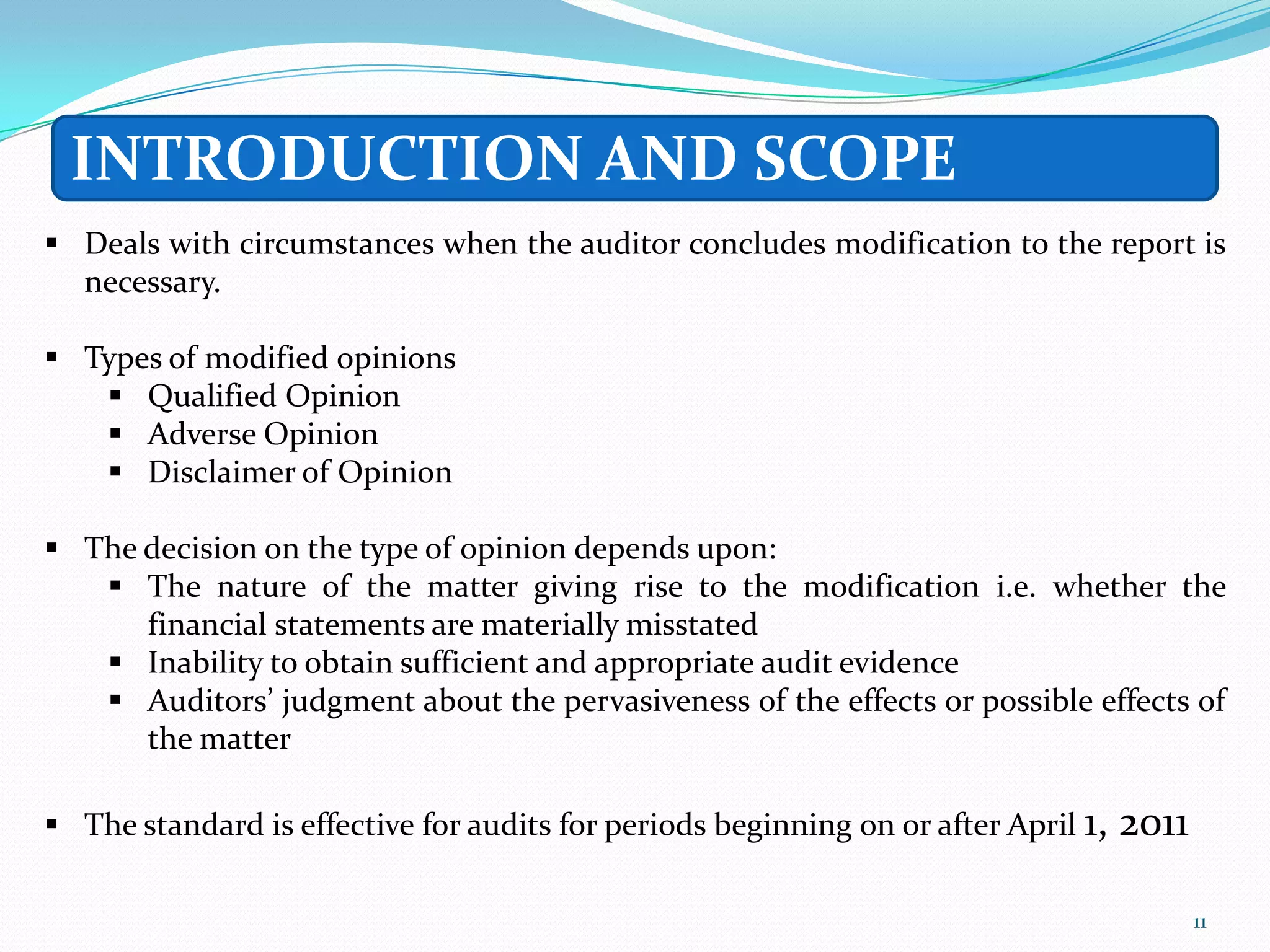

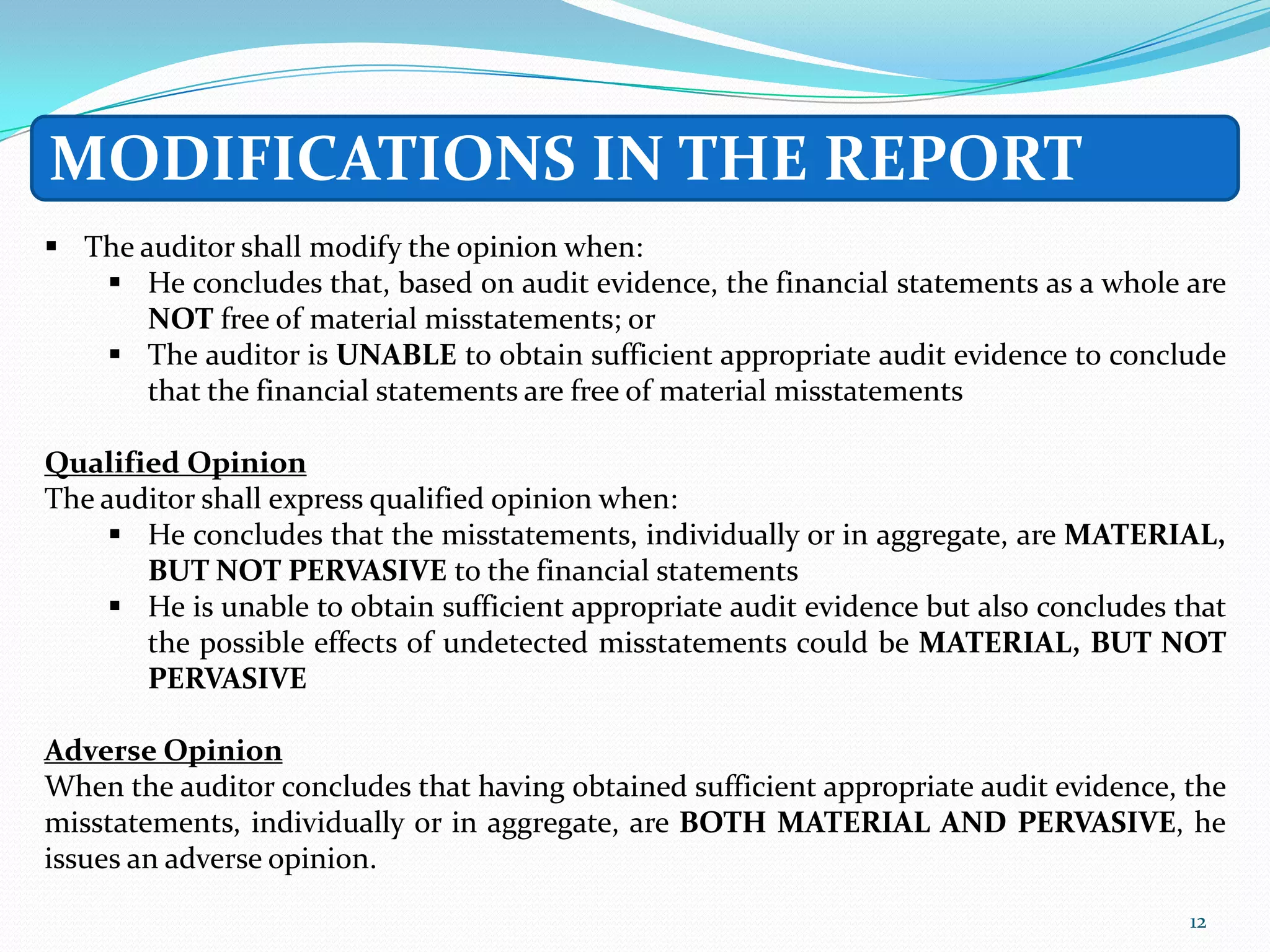

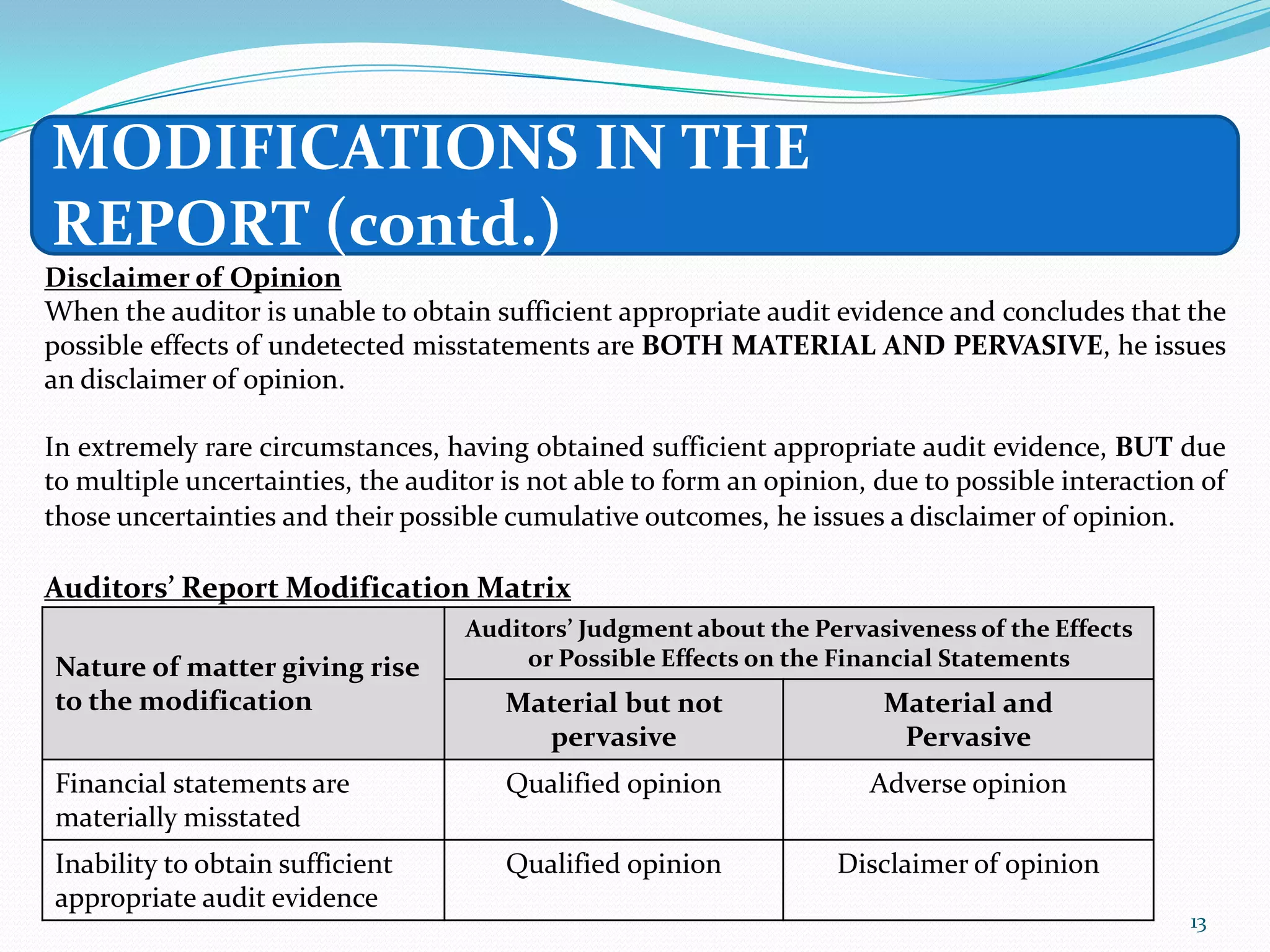

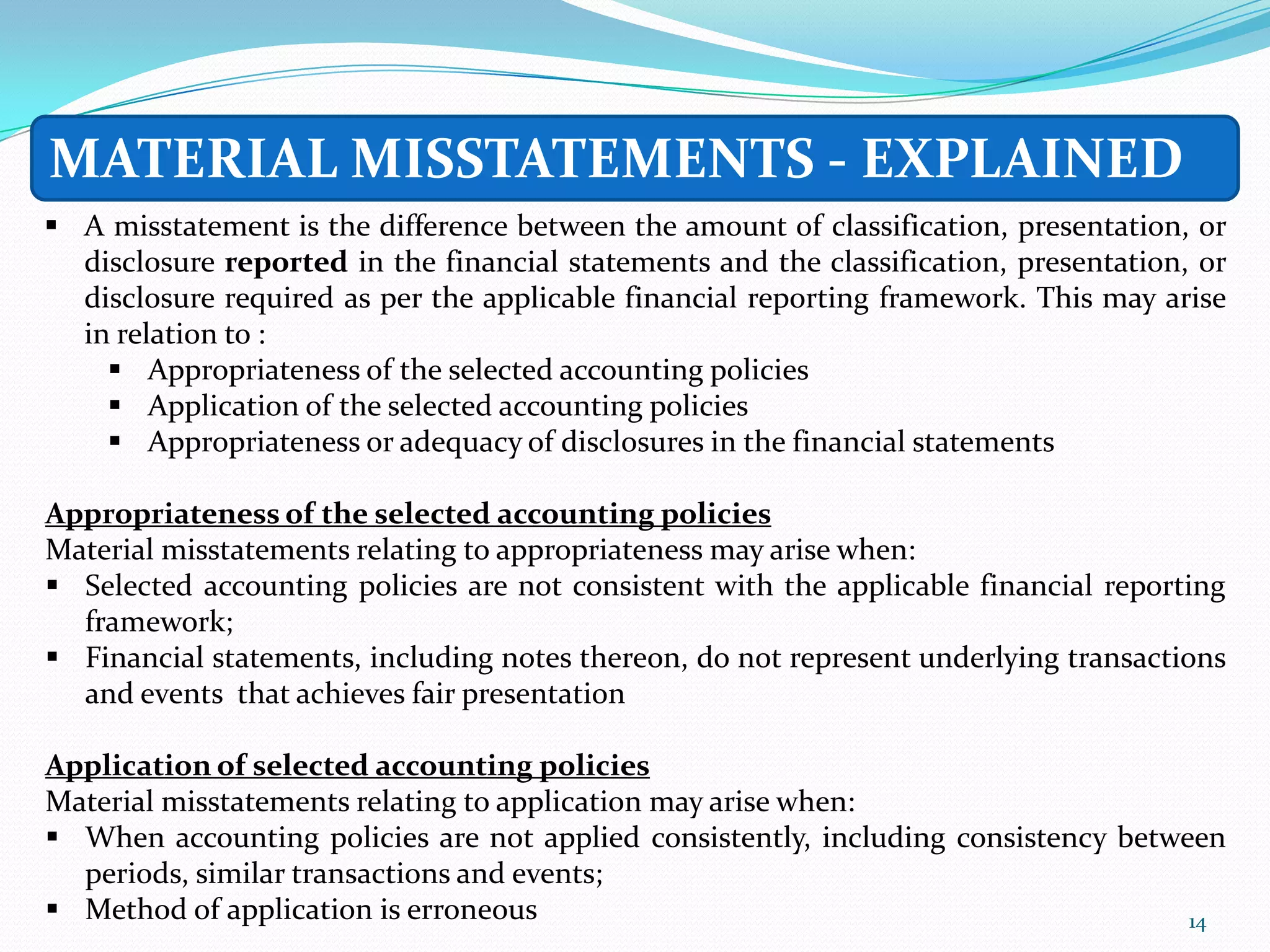

SA 705 covers circumstances requiring a modified audit opinion, including qualified, adverse, and disclaimer opinions depending on the pervasiveness of misstatements or inability to obtain evidence. It defines material misstatements and explains how they can arise from inappropriate accounting policies or application.