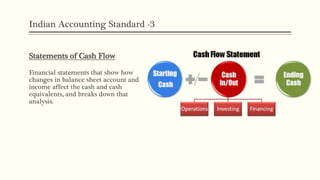

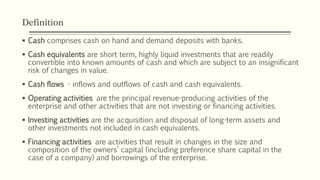

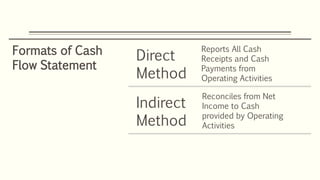

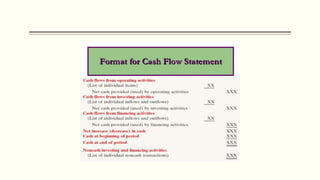

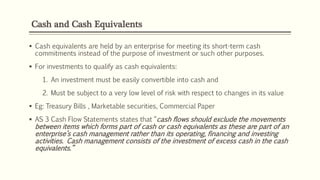

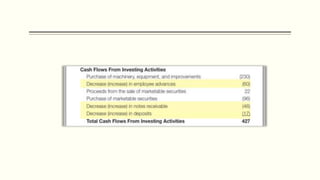

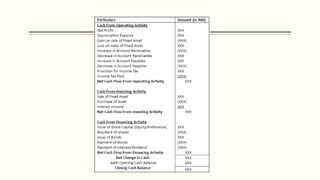

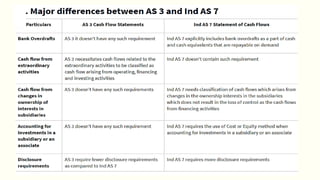

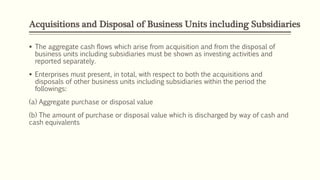

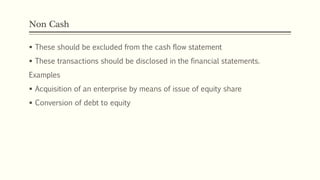

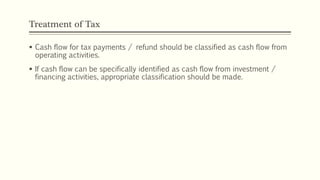

This document discusses Indian Accounting Standard 3 on cash flow statements. It defines key terms like cash, cash equivalents, operating activities, investing activities and financing activities. It explains the direct and indirect methods of preparing cash flow statements and requirements around classification of cash flows from various transactions like tax, foreign exchange, dividends and interest. The standard aims to provide useful information on changes in cash balances to investors and other stakeholders.