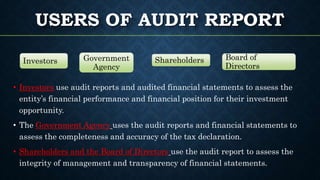

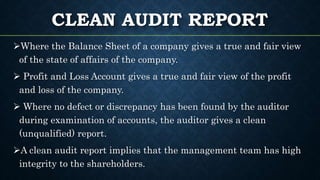

An audit report is prepared by auditors post-examination of a company's financial statements, conveying their opinion on accuracy and completeness. There are four main types of audit reports: clean, qualified, adverse, and disclaimer, each indicating different levels of confidence regarding the financial statements. Users of these reports include investors, governmental agencies, shareholders, and boards of directors, who rely on them for assessing financial performance and integrity.

![AUDIT REPORT [ AUDITING ]](https://image.slidesharecdn.com/auditingtypesofauditreport-210303052610/85/AUDIT-REPORT-AUDITING-12-320.jpg)