Downloaded 75 times

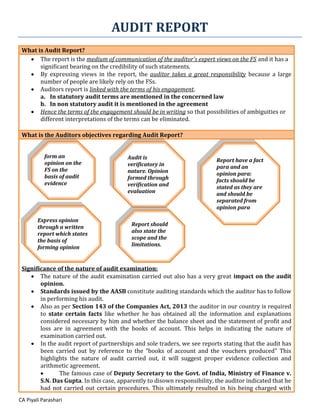

The document provides an overview of audit reports, including: - The objectives of an audit report are to form an opinion on the financial statements based on audit evidence and to express this opinion through a written report. - The report must state the scope and limitations of the audit and separate facts from opinions. - The nature of the audit examination, management responsibilities, and standards of auditing like SA 700 all impact the structure and wording of the audit report.