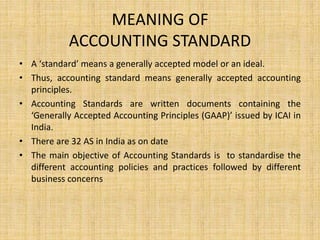

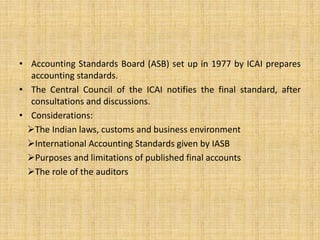

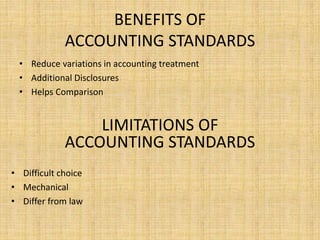

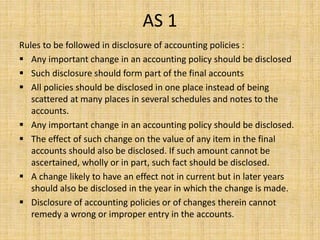

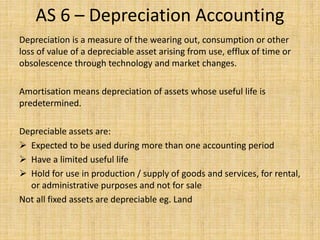

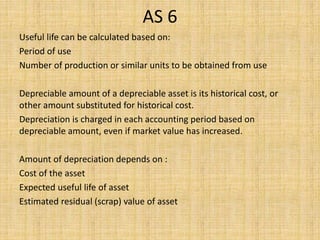

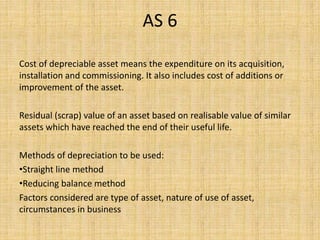

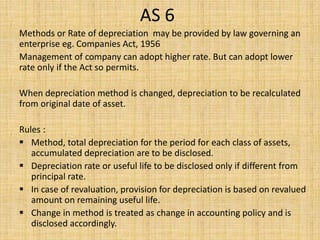

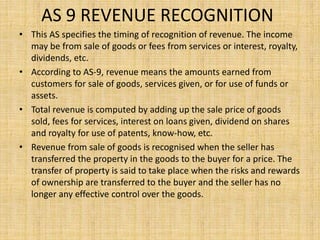

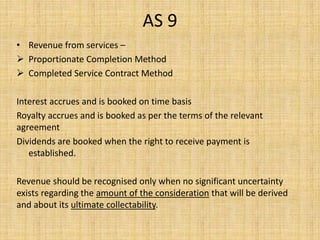

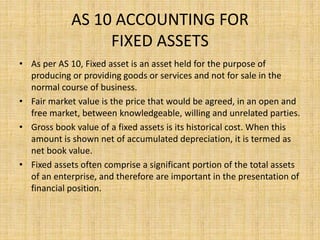

The document discusses Indian accounting standards, including the meaning and benefits of accounting standards. It provides details on several specific accounting standards such as AS1 on disclosure of accounting policies, AS6 on depreciation accounting, AS9 on revenue recognition, and AS10 on accounting for fixed assets. The standards cover topics such as selection and disclosure of accounting policies, methods of depreciation, timing of revenue recognition, calculation of costs of fixed assets, and revaluation of fixed assets. The overall objective of the accounting standards is to standardize different accounting policies and practices in India.