Downloaded 322 times

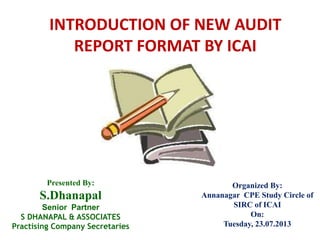

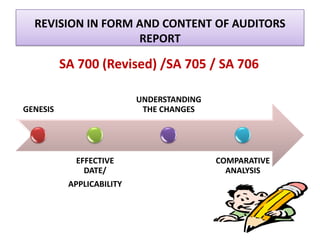

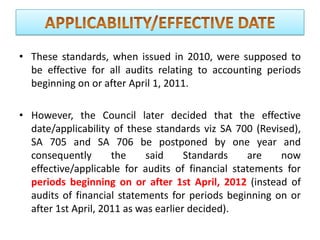

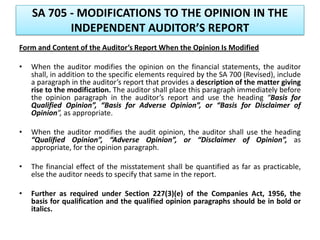

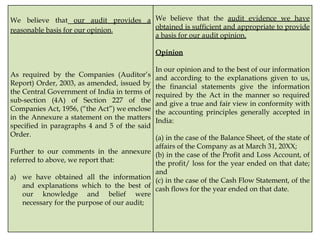

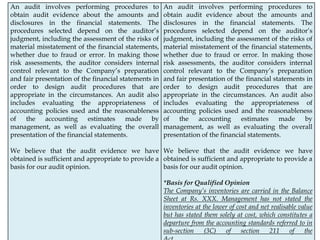

![SA 700 (REVISED) - FORMING AN OPINION AND

REPORTING ON FINANCIAL STATEMENTS

The main highlights of SA 700 (Revised) are:

• The Auditors report shall be in writing – hard Copy or report using electronic format.

• It shall have a title that clearly indicates that it is the report of an independent

auditor.

• The introductory paragraph of the report shall contain the name of the entity, name

and period of each statement that comprises the financial statements, refer to the

summary of significant accounting policies and other explanatory information and

state that the financial statements have been audited.

• The auditor’s report shall include sections and headings as under

Report on the Financial Statements (if other reporting responsibilities have been

addressed)

Management’s [or other appropriate term] Responsibility for the Financial

Statements

Auditor’s Responsibility

Opinion

Report on Other Legal and Regulatory Requirements [or otherwise as

appropriate] (wherever applicable)

• The auditor’s report shall be signed and dated and shall also contain the place of

signature along with membership number of the auditor signing the report and the

FRN of the firm, as applicable.](https://image.slidesharecdn.com/auditreport-130809013413-phpapp02/85/Audit-report-11-320.jpg)

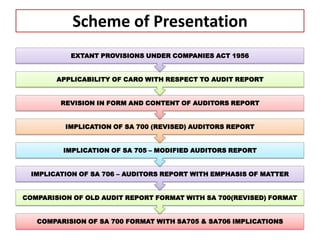

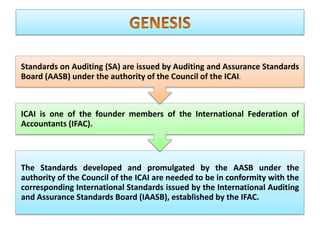

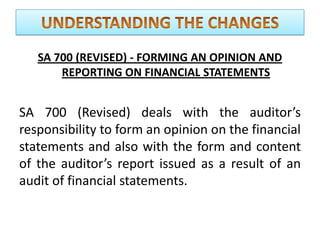

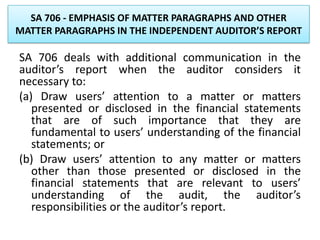

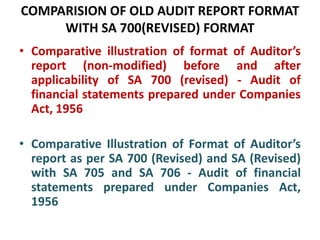

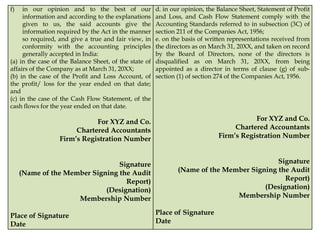

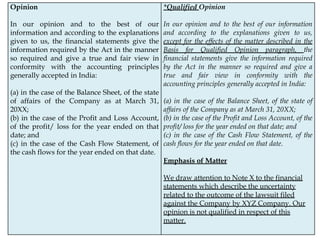

![Format of Audit Report before and After SA 700

Illustrative format of Audit Report

applicable till 31.03.2012

[Before application of SA 700 (revised)]

AUDITORS’ REPORT

To the Members of ABC Company

Limited

We have audited the attached balance

sheet of ABC Company Limited (“the

Company”) as at 31 March 20XX and the

statement of profit and loss for the period

….. annexed thereto.

Illustrative format of Audit Report

applicable from 01.04.2012

[After application of SA 700 (Revised)]

INDEPENDENT AUDITOR’S REPORT

To the Members of ABC Company Limited

Report on the Financial Statements

We have audited the accompanying financial

statements of ABC Company Limited (“the

Company”), which comprise the Balance

Sheet as at March 31, 20XX, and the Statement

of Profit and Loss and Cash Flow Statement

for the year then ended, and a summary of

significant accounting policies and other

explanatory information.](https://image.slidesharecdn.com/auditreport-130809013413-phpapp02/85/Audit-report-21-320.jpg)

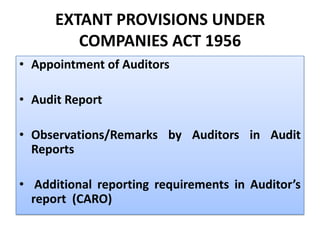

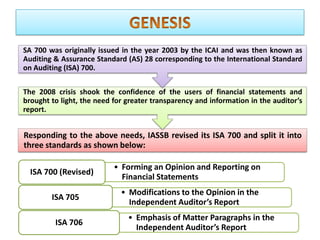

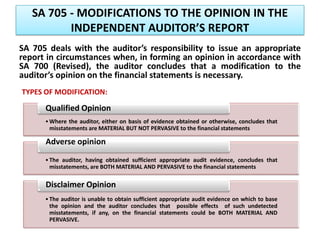

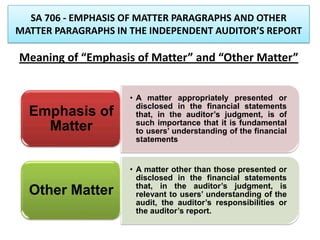

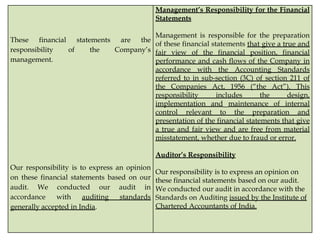

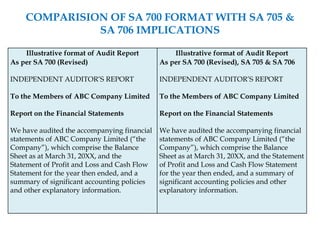

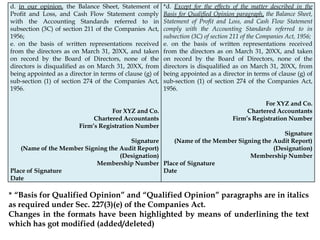

![b) in our opinion proper books of account

as required by law have been kept by

the Company so far as appears from our

examination of those books [and proper

returns adequate for the purposes of our

audit have been received from branches

not visited by us];

c) the Balance Sheet, Statement of Profit

and Loss, and Cash Flow Statement

dealt with by this Report are in

agreement with the books of account

[and with the returns received from

branches not visited by us;

d) in our opinion, the Balance Sheet,

Statement of Profit and Loss, and Cash

Flow Statement comply with the

Accounting Standards referred to in

subsection (3C) of section 211 of the

Companies Act, 1956;

e) on the basis of written representations

received from the directors as on March

31, 20XX, and taken on record by the

Board of Directors, none of the directors

is disqualified as on March 31, 20XX,

from being appointed as a director in

terms of clause (g) of sub-section (1) of

section 274 of the Companies Act, 1956.

Report on Other Legal and Regulatory

Requirements

1. As required by the Companies (Auditor’s

Report) Order, 2003 (“the Order”) issued by the

Central Government of India in terms of sub-

section (4A) of section 227 of the Act, we give in

the Annexure a statement on the matters

specified in paragraphs 4 and 5 of the Order.

2. As required by section 227(3) of the Act, we

report that:

a. we have obtained all the information and

explanations which to the best of our knowledge

and belief were necessary for the purpose of our

audit;

b. in our opinion proper books of account as

required by law have been kept by the Company

so far as appears from our examination of those

books [and proper returns adequate for the

purposes of our audit have been received from

bran

c. the Balance Sheet, Statement of Profit and

Loss, and Cash Flow Statement dealt with by

this Report are in agreement with the books of

account [and with the returns received from

branches not visited by us;](https://image.slidesharecdn.com/auditreport-130809013413-phpapp02/85/Audit-report-25-320.jpg)

![Report on Other Legal and Regulatory

Requirements

1. As required by the Companies (Auditor’s

Report) Order, 2003 (“the Order”) issued by

the Central Government of India in terms of

sub-section (4A) of section 227 of the Act, we

give in the Annexure a statement on the

matters specified in paragraphs 4 and 5 of the

Order.

2. As required by section 227(3) of the Act, we

report that:

a. we have obtained all the information and

explanations which to the best of our

knowledge and belief were necessary for the

purpose of our audit;

b. in our opinion proper books of account as

required by law have been kept by the

Company so far as appears from our

examination of those books [and proper

returns adequate for the purposes of our audit

have been received from branches not visited

by us];

c. the Balance Sheet, Statement of Profit and

Loss, and Cash Flow Statement dealt with by

this Report are in agreement with the books of

account [and with the returns received from

Report on Other Legal and Regulatory

Requirements

1. As required by the Companies (Auditor’s

Report) Order, 2003 (“the Order”) issued by

the Central Government of India in terms of

sub-section (4A) of section 227 of the Act, we

give in the Annexure a statement on the

matters specified in paragraphs 4 and 5 of the

Order.

2. As required by section 227(3) of the Act, we

report that:

a. we have obtained all the information and

explanations which to the best of our

knowledge and belief were necessary for the

purpose of our audit;

b. in our opinion proper books of account as

required by law have been kept by the

Company so far as appears from our

examination of those books [and proper

returns adequate for the purposes of our audit

have been received from branches not visited

by us];

c. the Balance Sheet, Statement of Profit and

Loss, and Cash Flow Statement dealt with by

this Report are in agreement with the books of

account [and with the returns received from](https://image.slidesharecdn.com/auditreport-130809013413-phpapp02/85/Audit-report-31-320.jpg)

The document summarizes the key changes introduced by the Standards on Auditing (SA) 700 (Revised), SA 705, and SA 706 issued by the Auditing and Assurance Standards Board of the Institute of Chartered Accountants of India regarding the format and content of audit reports. Specifically, it provides a comparative analysis of the old versus new audit report formats, explains the types of modified audit opinions under SA 705, and the use of emphasis of matter and other matter paragraphs in audit reports as per SA 706. The document aims to explain the implications of the revised standards for auditors in India.

![AUDIT REPORT [ AUDITING ]](https://cdn.slidesharecdn.com/ss_thumbnails/auditingtypesofauditreport-210303052610-thumbnail.jpg?width=640&height=640&fit=bounds)