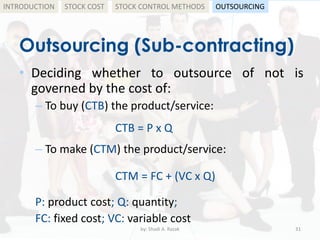

The document outlines the objectives and concepts of production planning in business, focusing on stock management, control methods, and cost implications. It differentiates between just-in-case (JIC) and just-in-time (JIT) stock control methods, discussing their advantages and disadvantages. Additionally, it covers outsourcing strategies and calculations needed to make informed make-or-buy decisions.

![Outsoucing- General approach [Bharti Airtel]](https://cdn.slidesharecdn.com/ss_thumbnails/outsoucing-finalppt-131016143457-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)