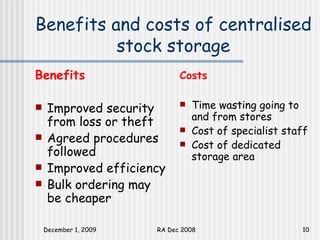

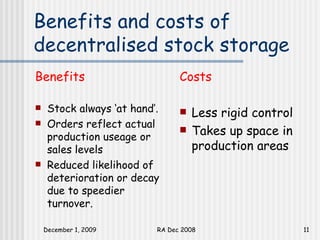

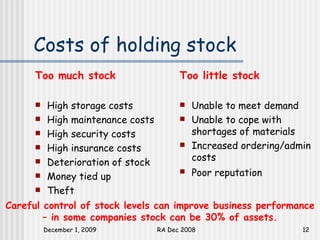

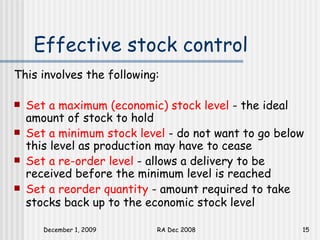

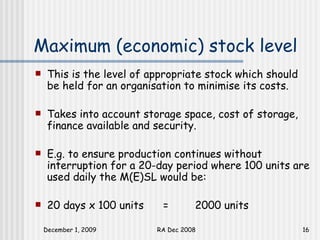

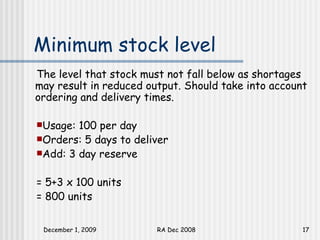

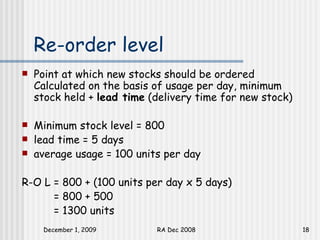

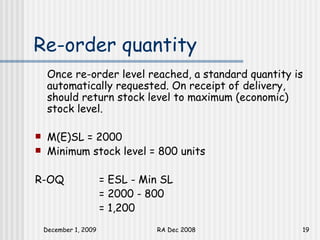

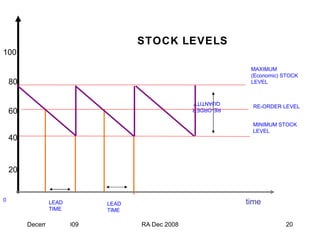

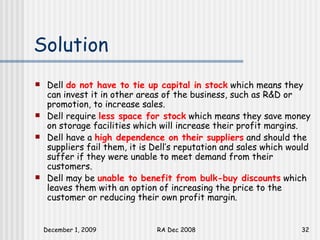

The document discusses stock control and purchasing in manufacturing organizations. It describes factors that purchasing managers should consider when choosing suppliers, such as quality, quantity, time, dependability and price. It also discusses the benefits and costs of different stock control methods, such as setting maximum, minimum and reorder stock levels to efficiently control stock. Computerized stock control allows automatic reordering and identification of best sellers. Just-in-time (JIT) production aims to minimize stock levels by receiving goods just before production.