Downloaded 41 times

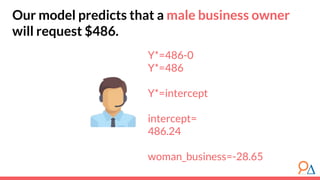

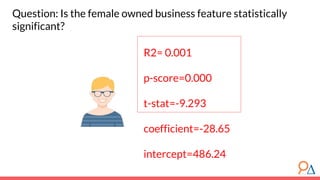

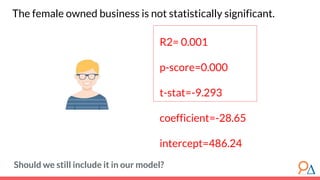

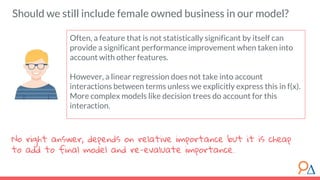

![Performance

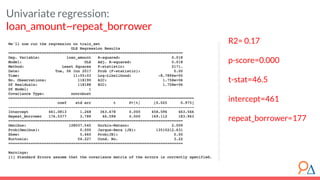

Measure

2) Are there holistic objectives that model

choice based upon accuracy might hurt?

Choosing a model to deploy based purely on predictive

power may pose ethical problems. Some examples:

● A risk score algorithm that predicts whether someone

will commit a future crime, used by US courts,

discriminated based upon race. It was clear the model

relied heavily on race as a feature. [Link]

● Carnegie Mellon found that women were less likely

than men to be shown ads by Google for high paying

jobs. [Link]

● Orbitz, a travel site, was showing Mac users higher

priced travel services than PC users. [Link]

We have values

as a society

that are not

captured by

optimizing for

accuracy.](https://image.slidesharecdn.com/module4modelselectionandevaluation2-190707194704/85/Module-4-Model-Selection-and-Evaluation-12-320.jpg)

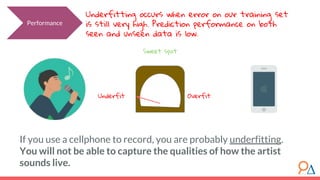

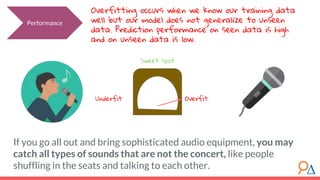

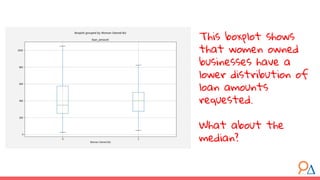

This document outlines a course module on model selection and evaluation, focusing on how to appropriately choose, assess, and validate models in research. It emphasizes the importance of performance measures such as accuracy and mean squared error, as well as considerations regarding ethical implications and generalization to unseen data. Furthermore, the document addresses issues of underfitting and overfitting in model training and suggests methods for improving model performance through feature selection and utilizing more complex algorithms.