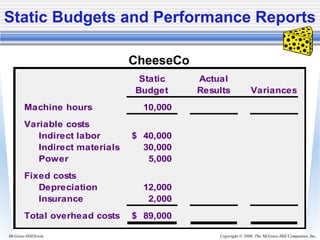

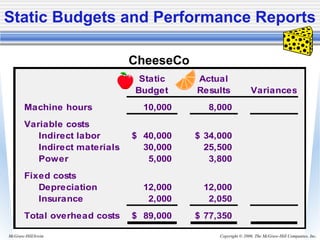

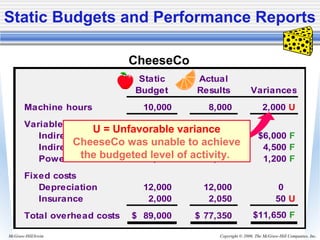

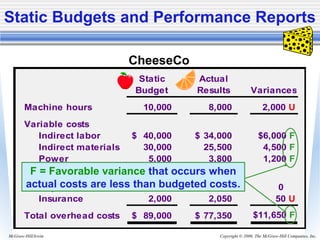

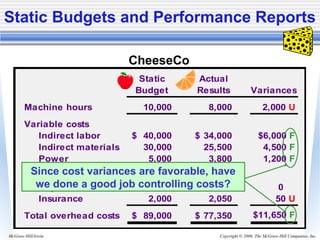

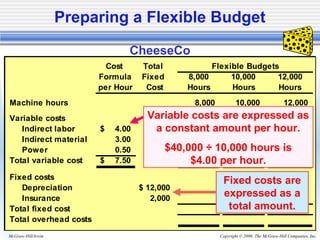

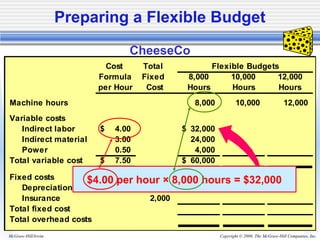

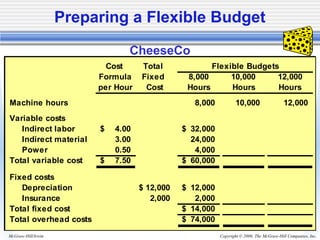

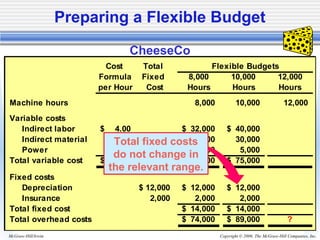

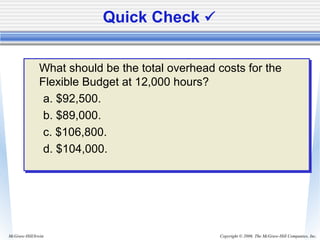

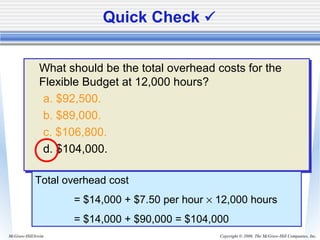

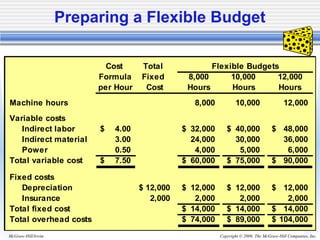

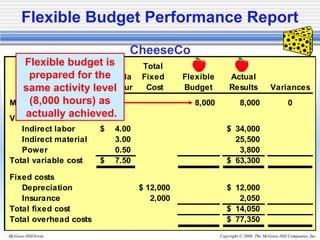

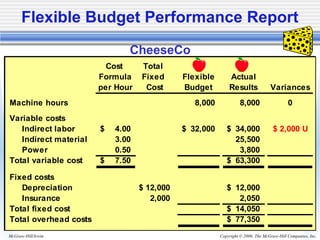

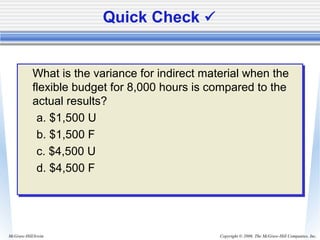

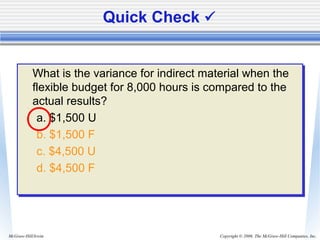

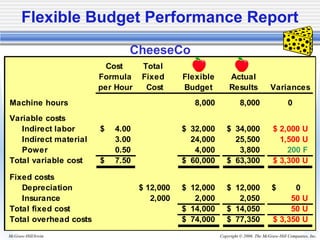

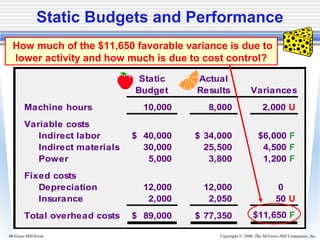

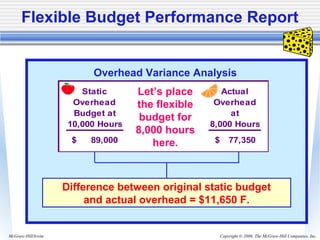

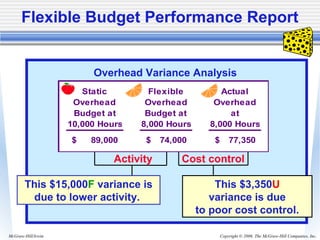

The document discusses static budgets and flexible budgets. A static budget is prepared for a single planned activity level and is difficult to use for performance evaluation when actual activity differs. A flexible budget can be prepared for multiple activity levels and allows for "apples-to-apples" cost comparisons at the actual activity level. The document provides an example of CheeseCo preparing both a static budget and flexible budget to evaluate performance when actual activity was lower than planned. Variances are identified to determine whether favorable cost variances were due to lower activity or good cost control.