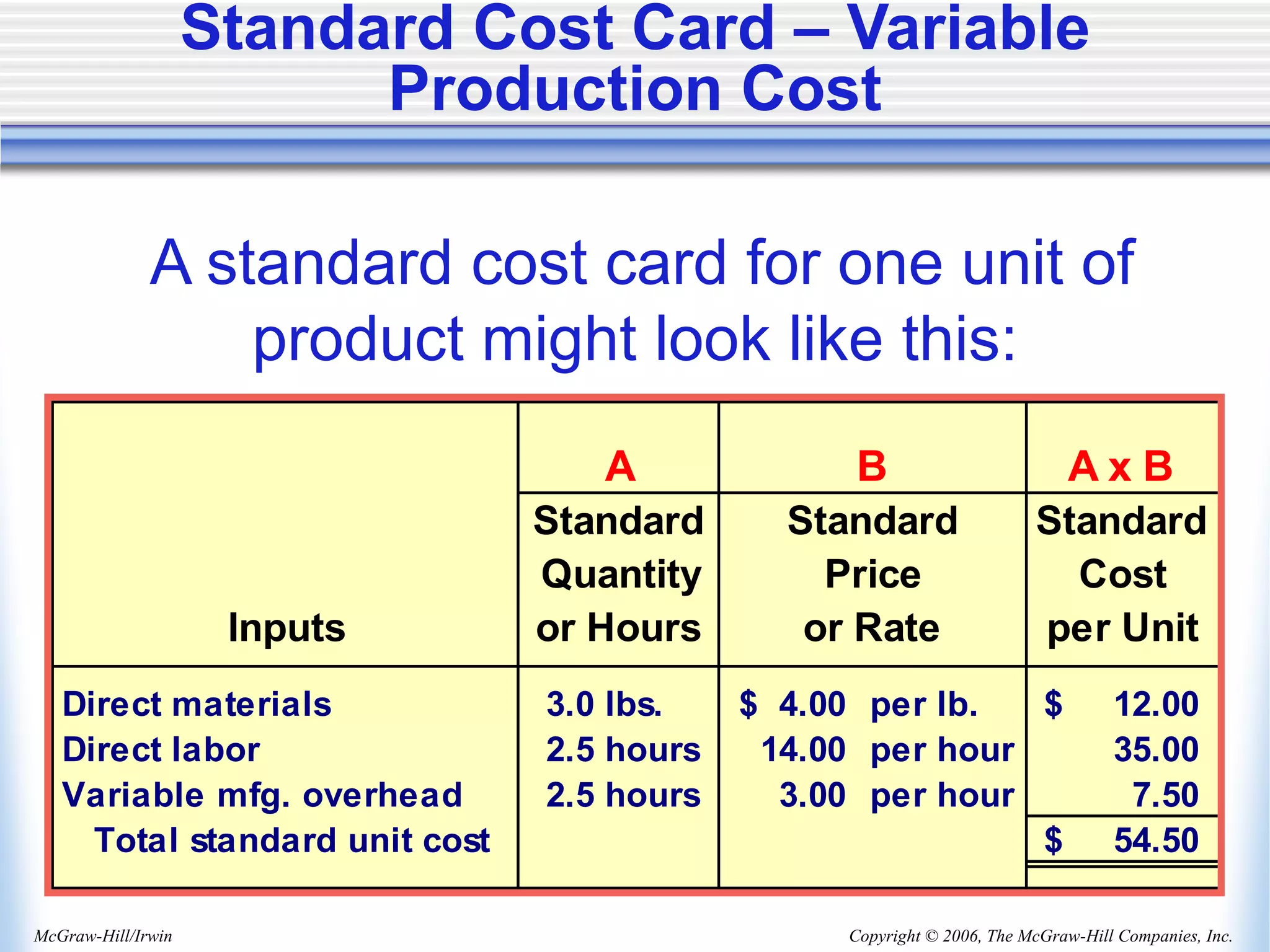

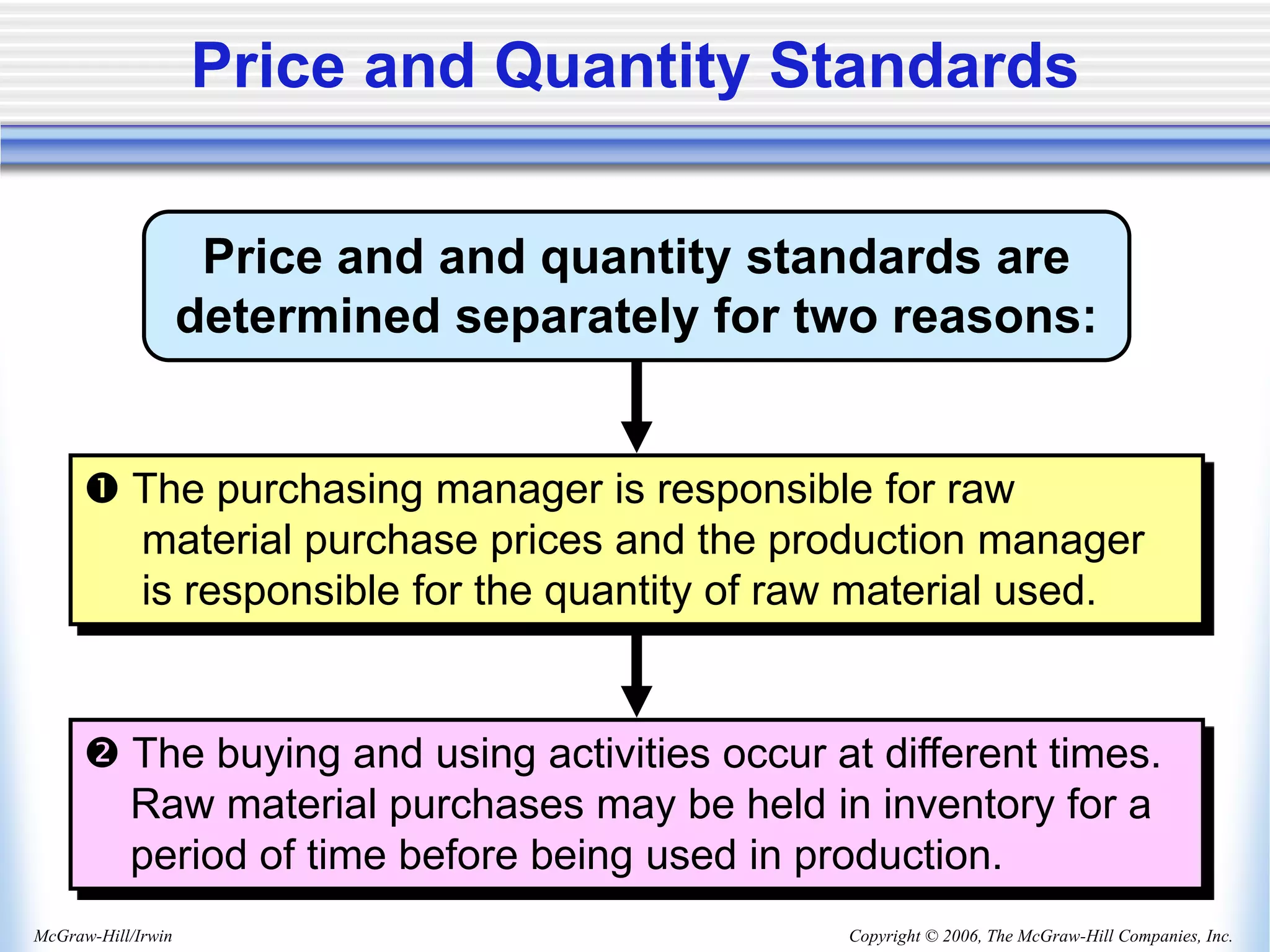

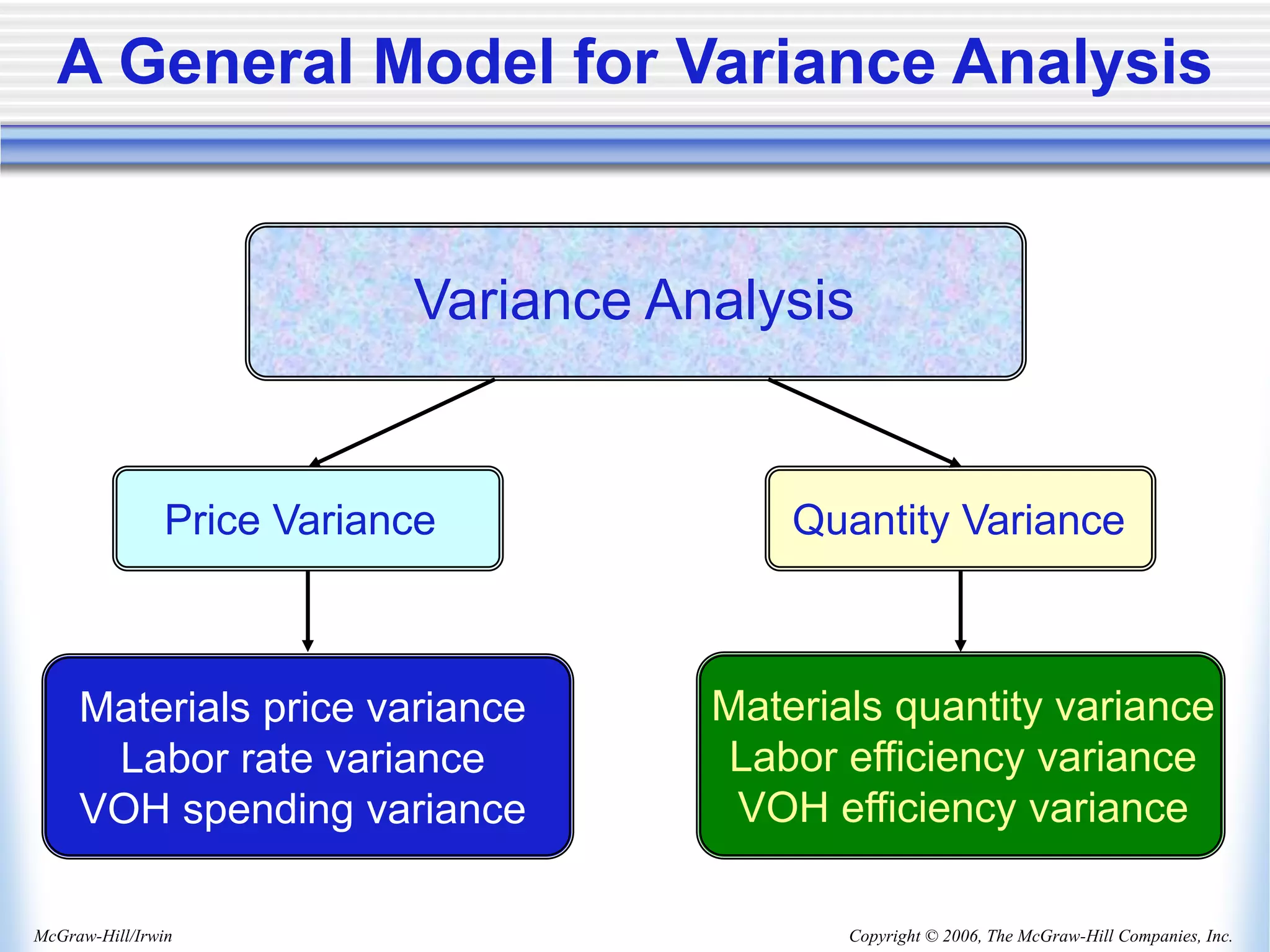

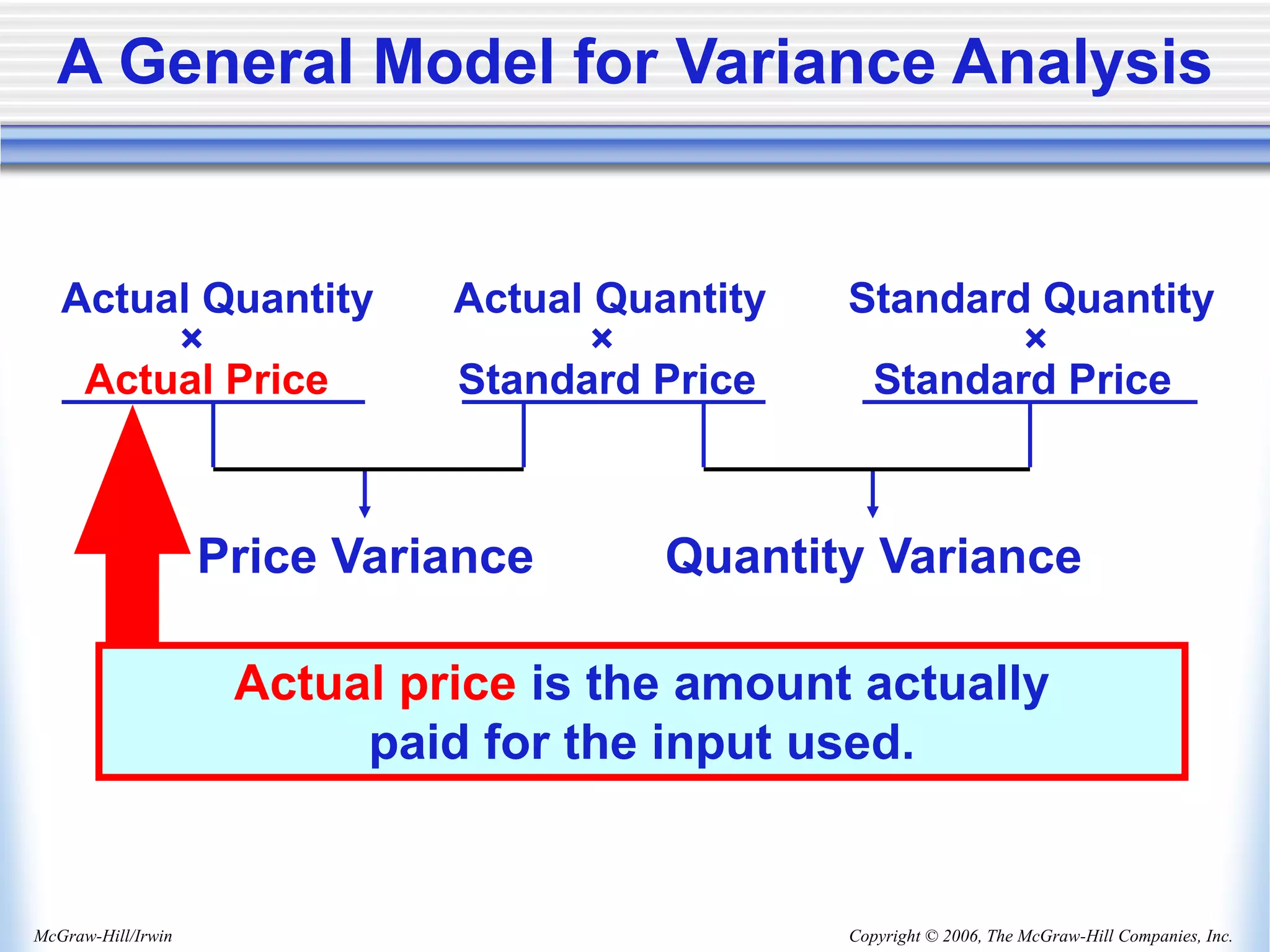

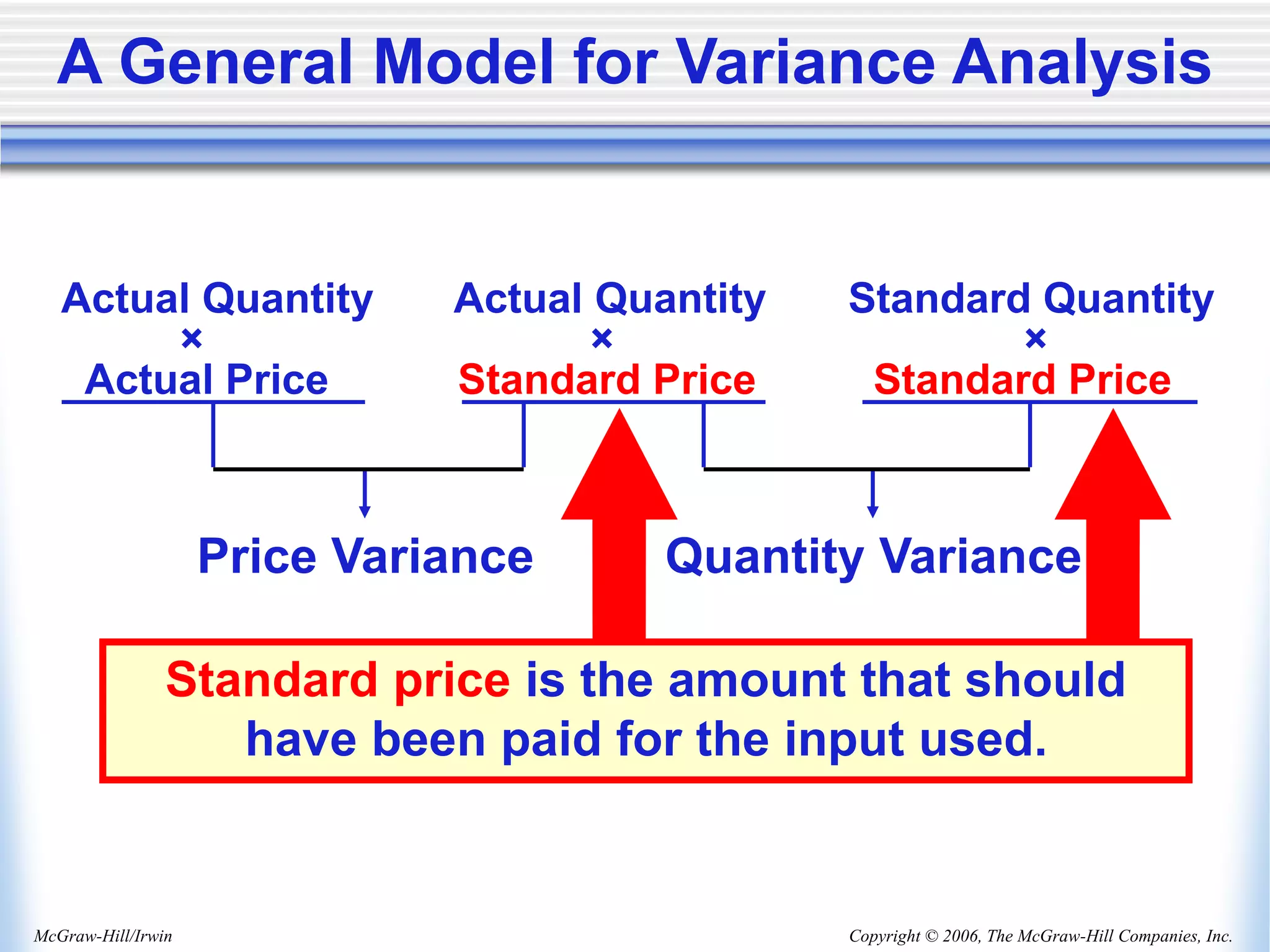

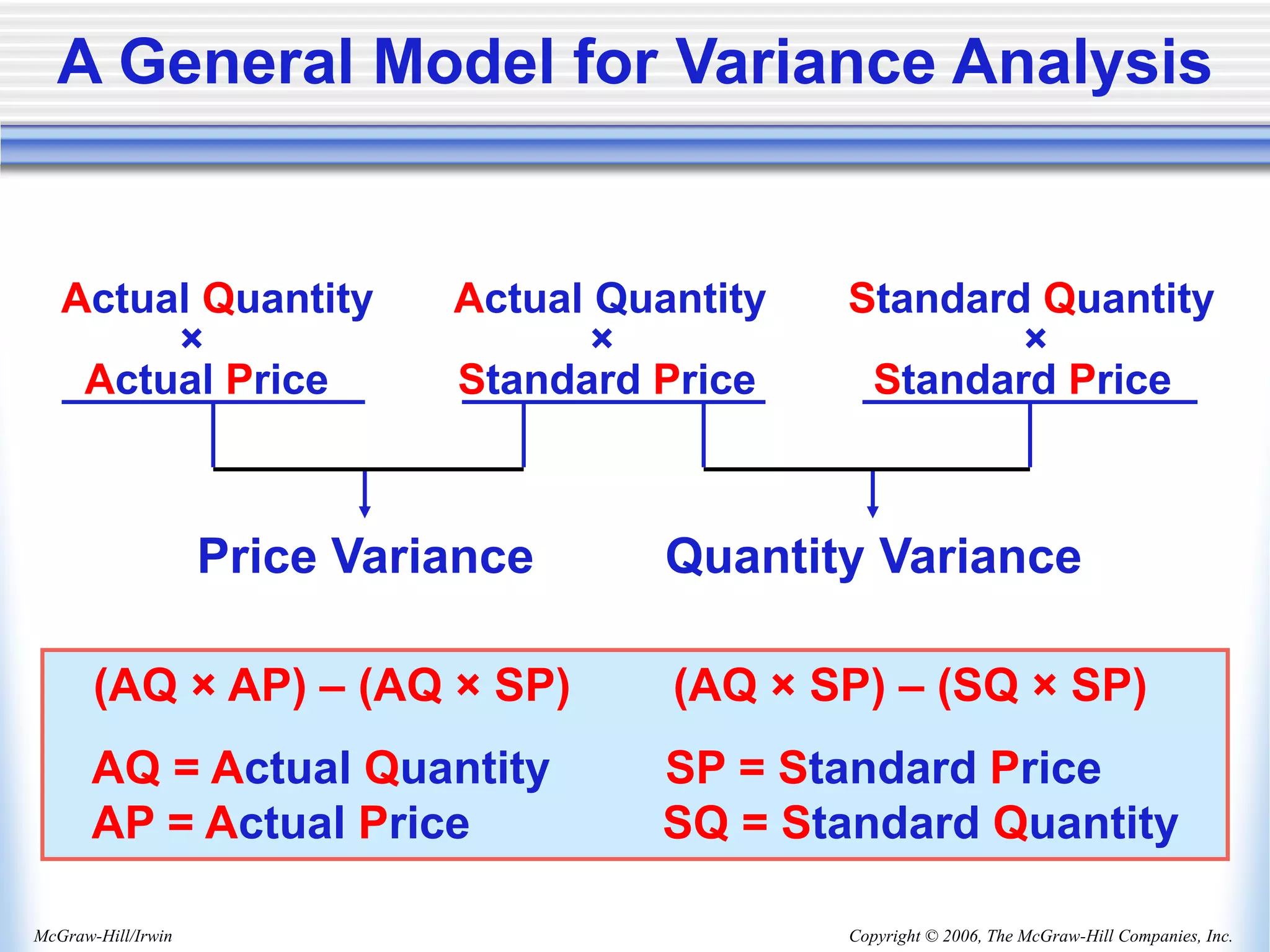

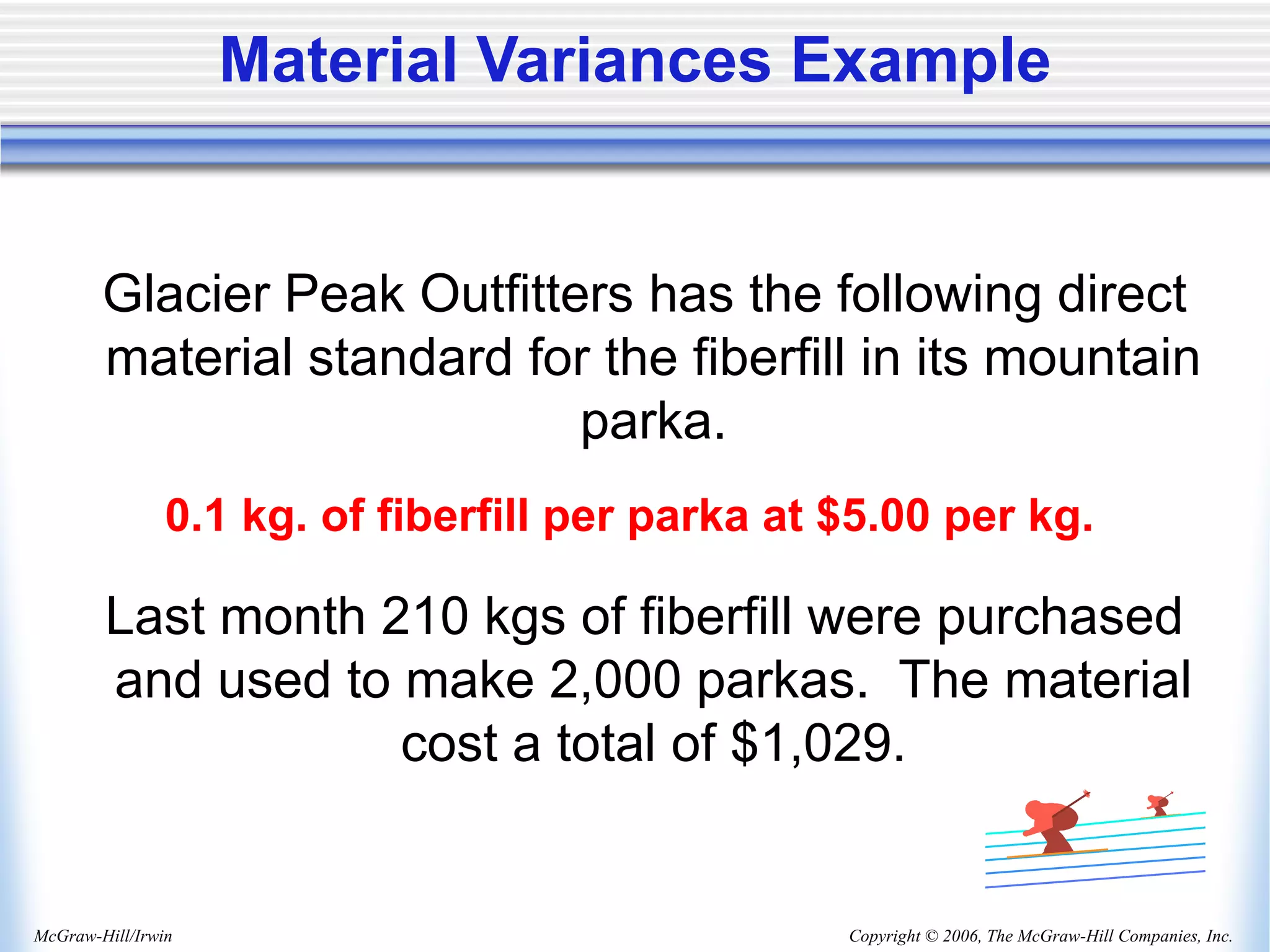

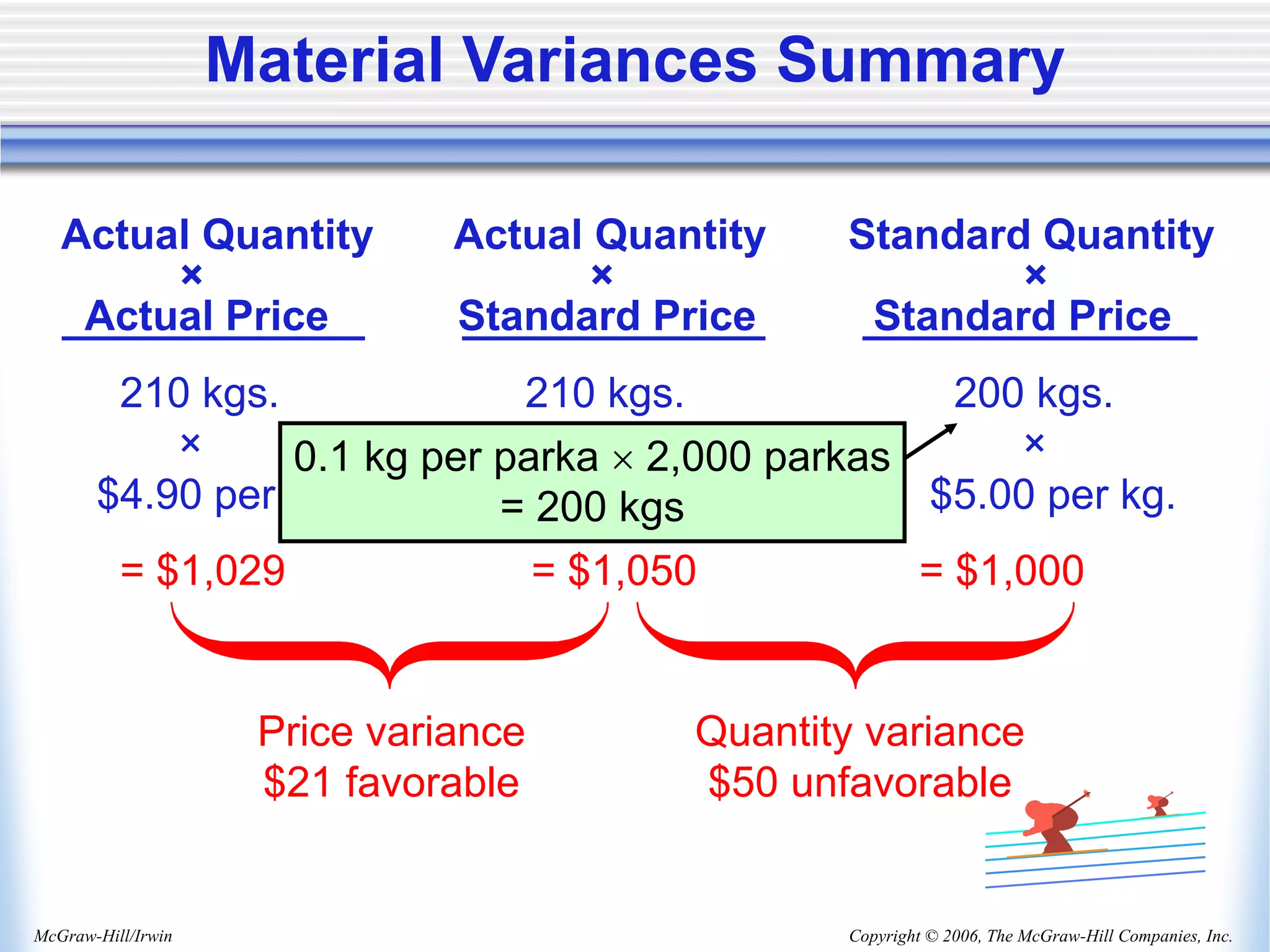

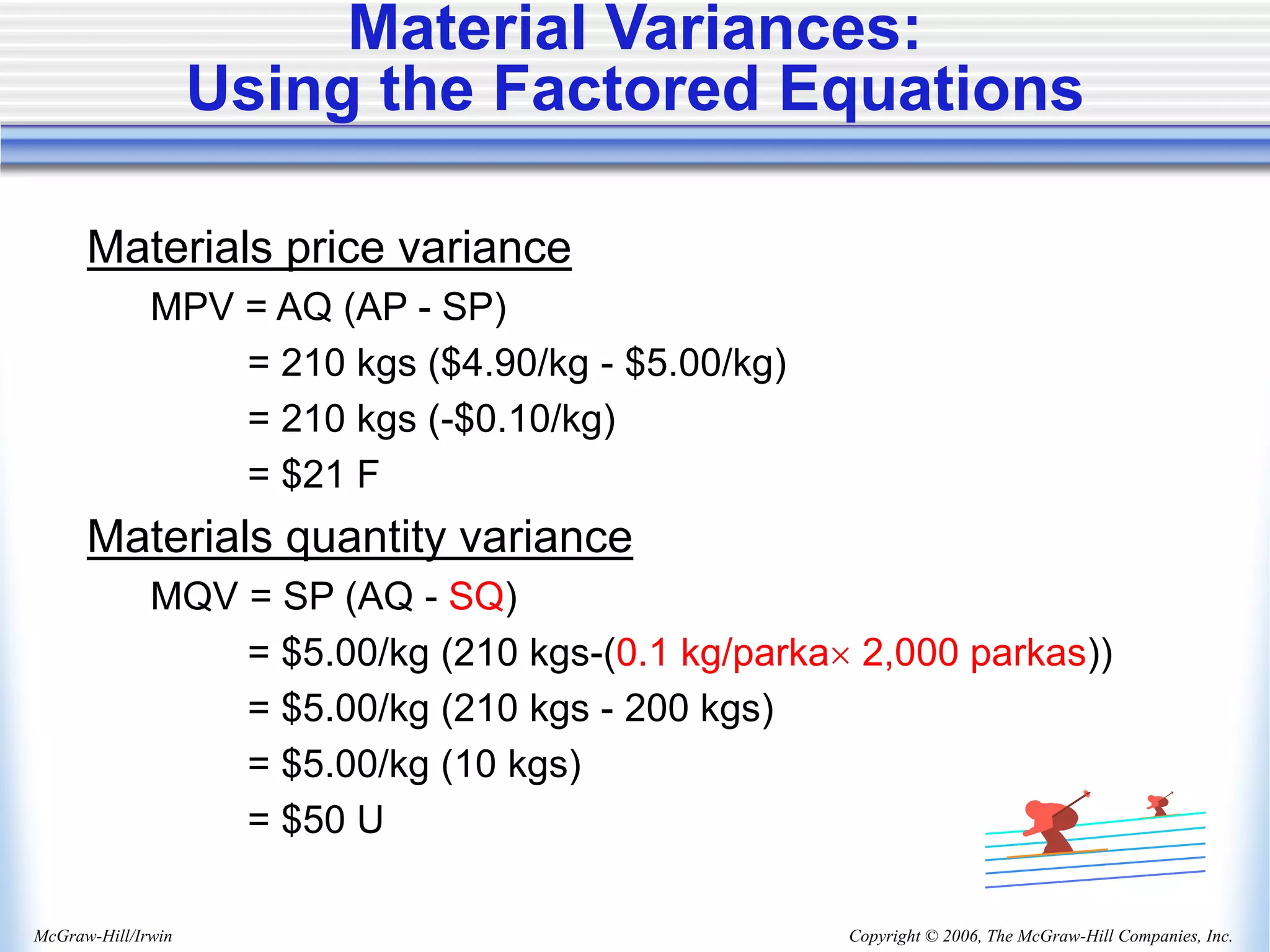

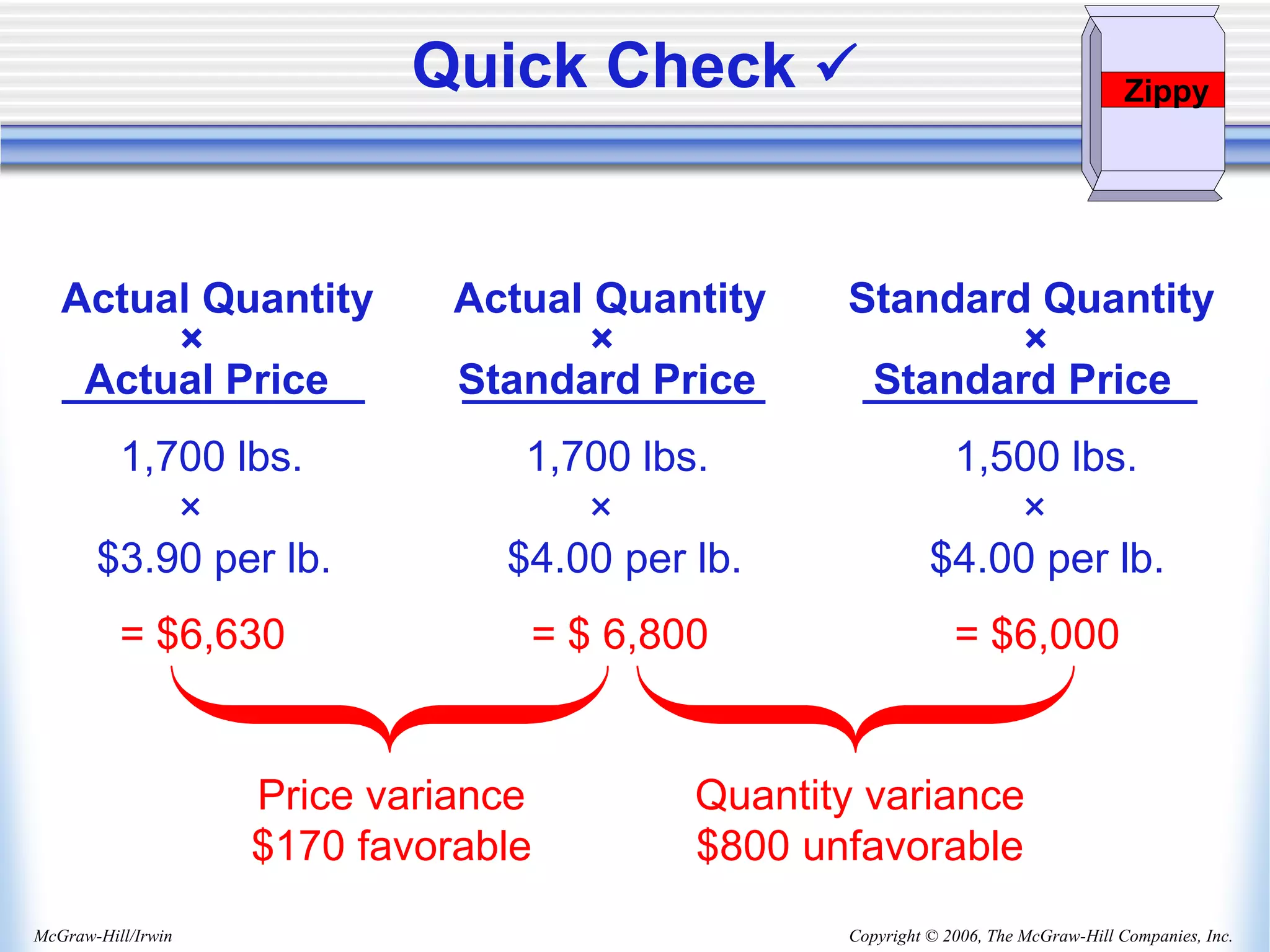

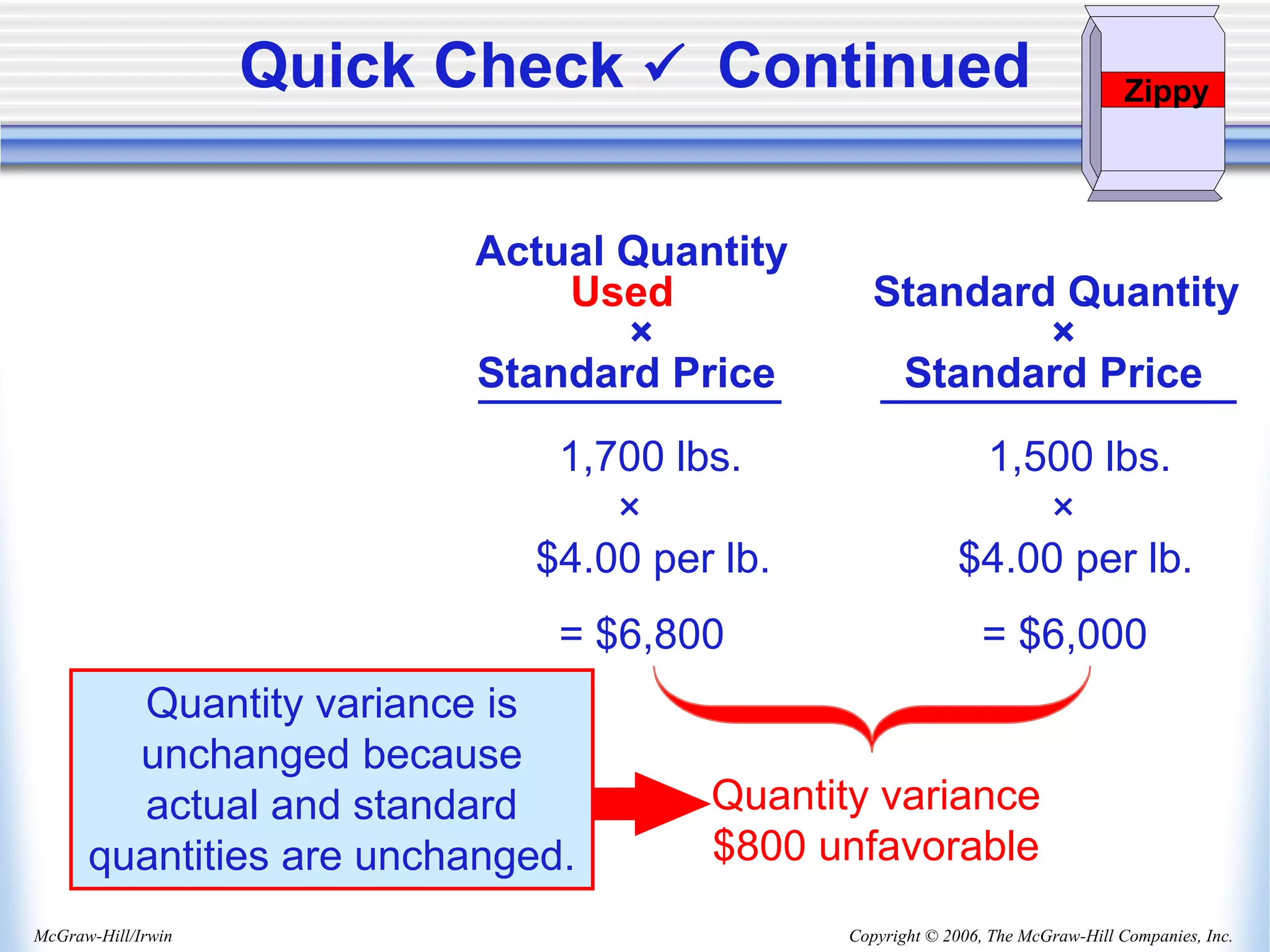

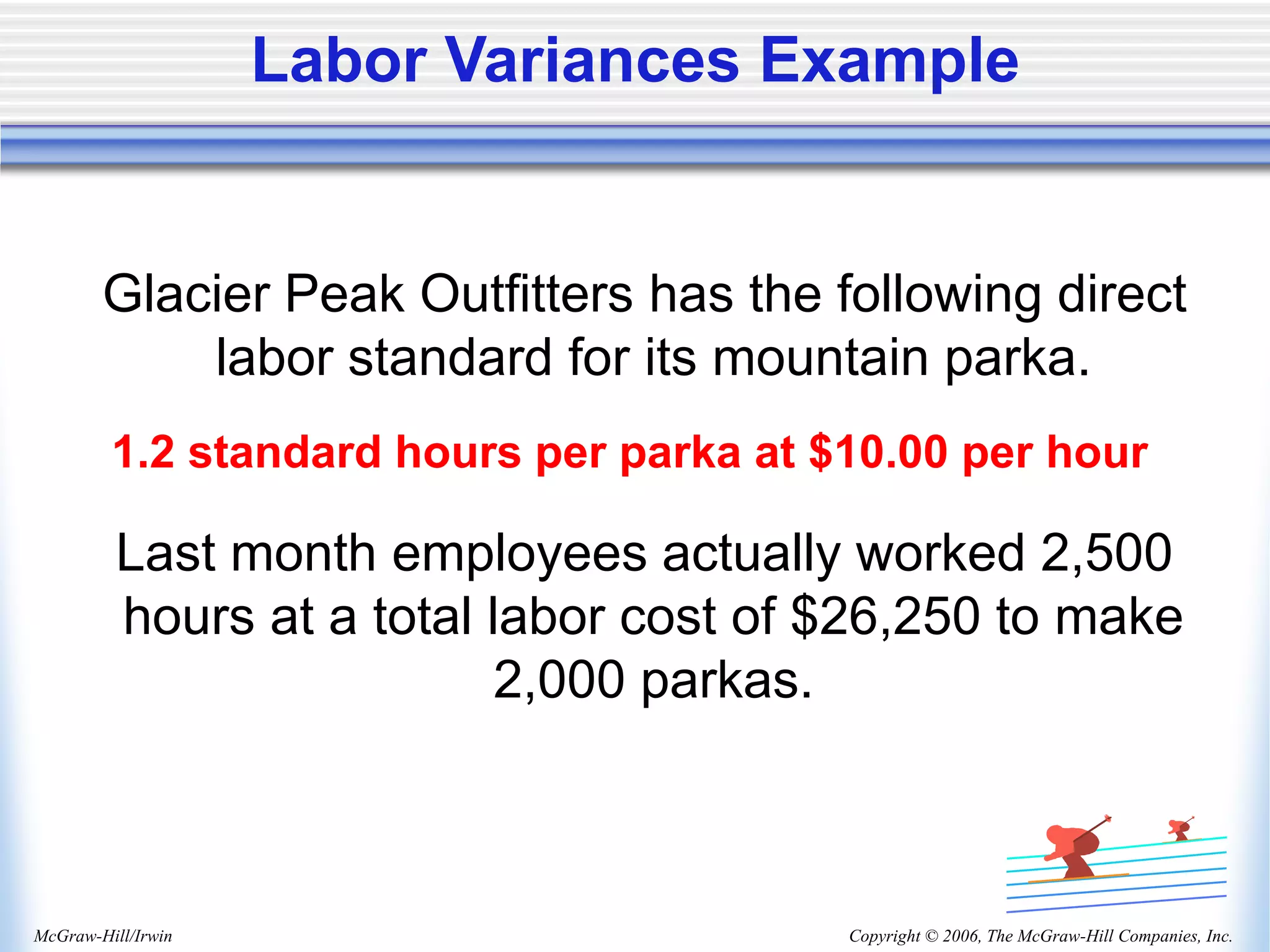

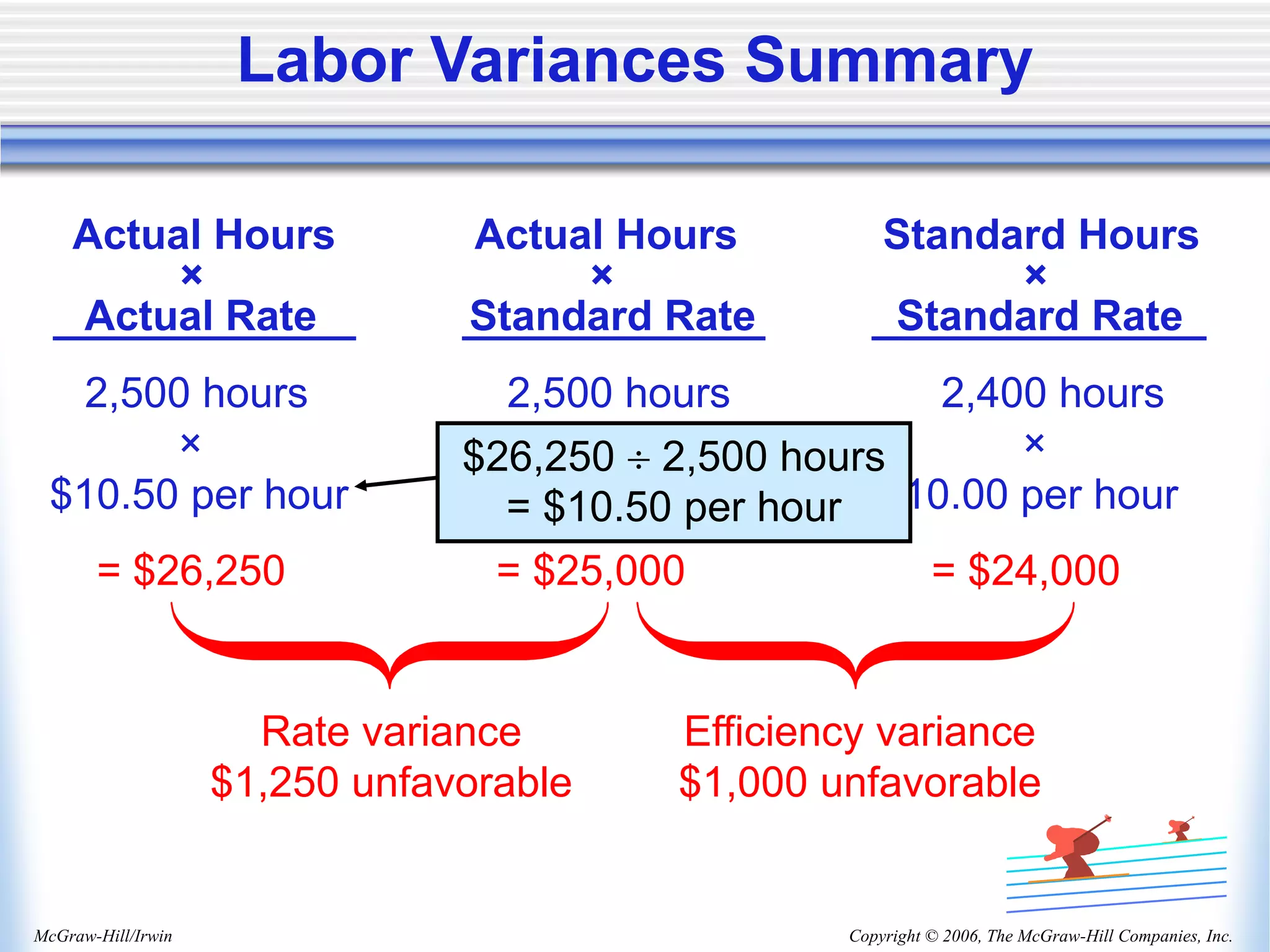

The document discusses standard costs and variances. It explains that standards specify the quantity and price of inputs expected to produce a product. Variances measure differences between actual and standard quantities and prices of direct materials, direct labor, and manufacturing overhead. Variances are used to identify areas for improvement and assign responsibility to managers. The document provides an example where a company calculated a $21 favorable price variance and $50 unfavorable quantity variance for direct materials.