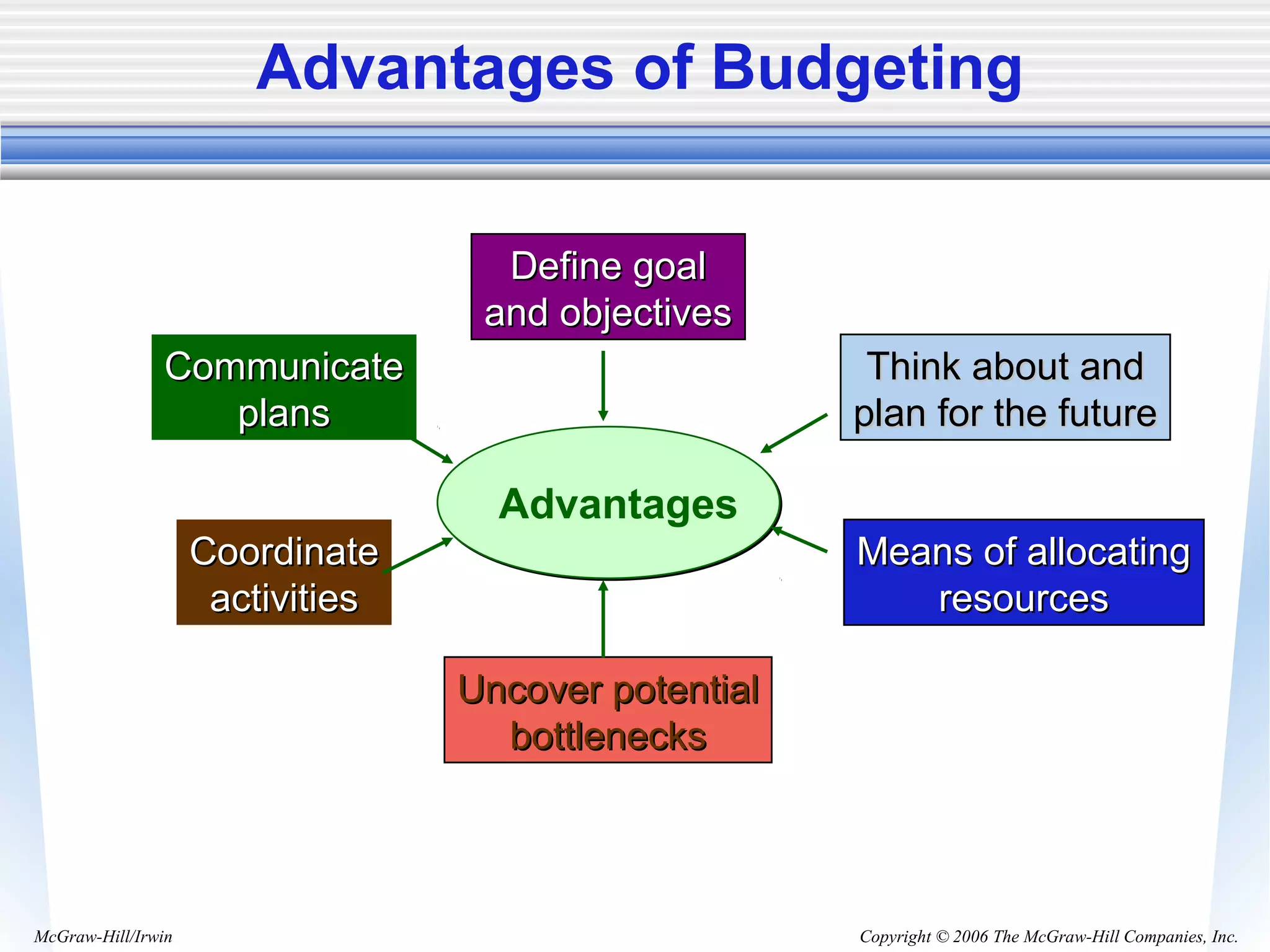

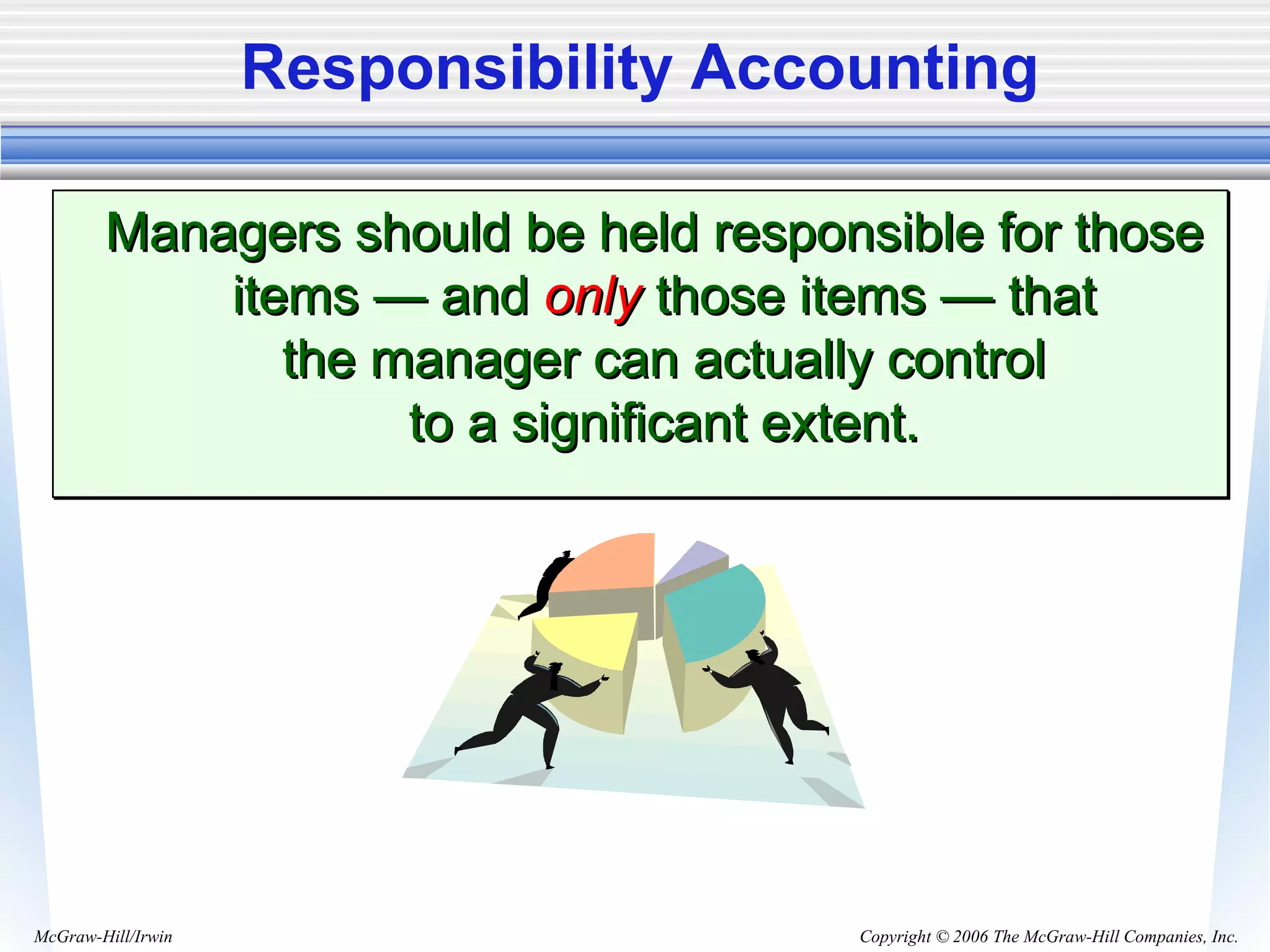

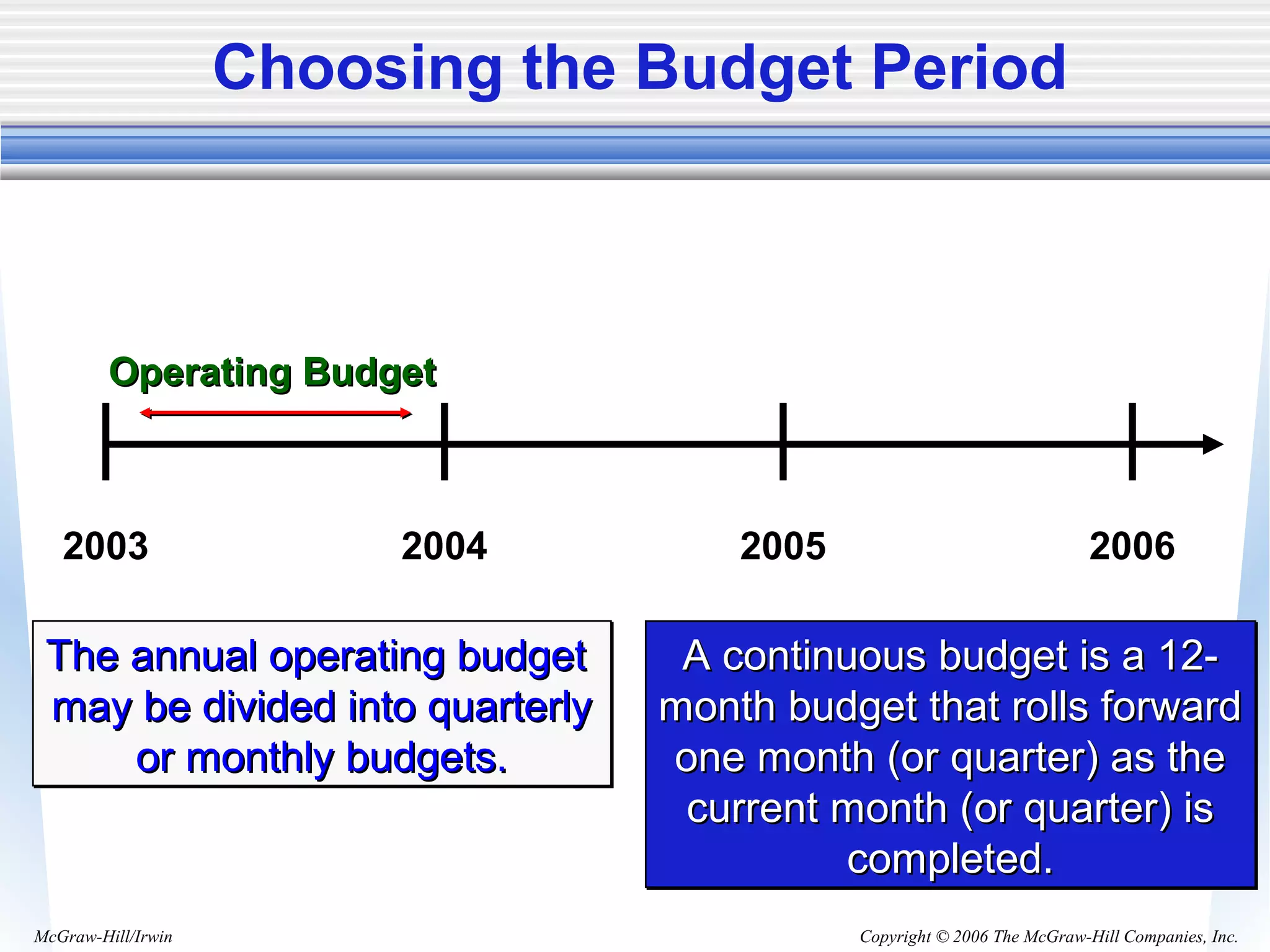

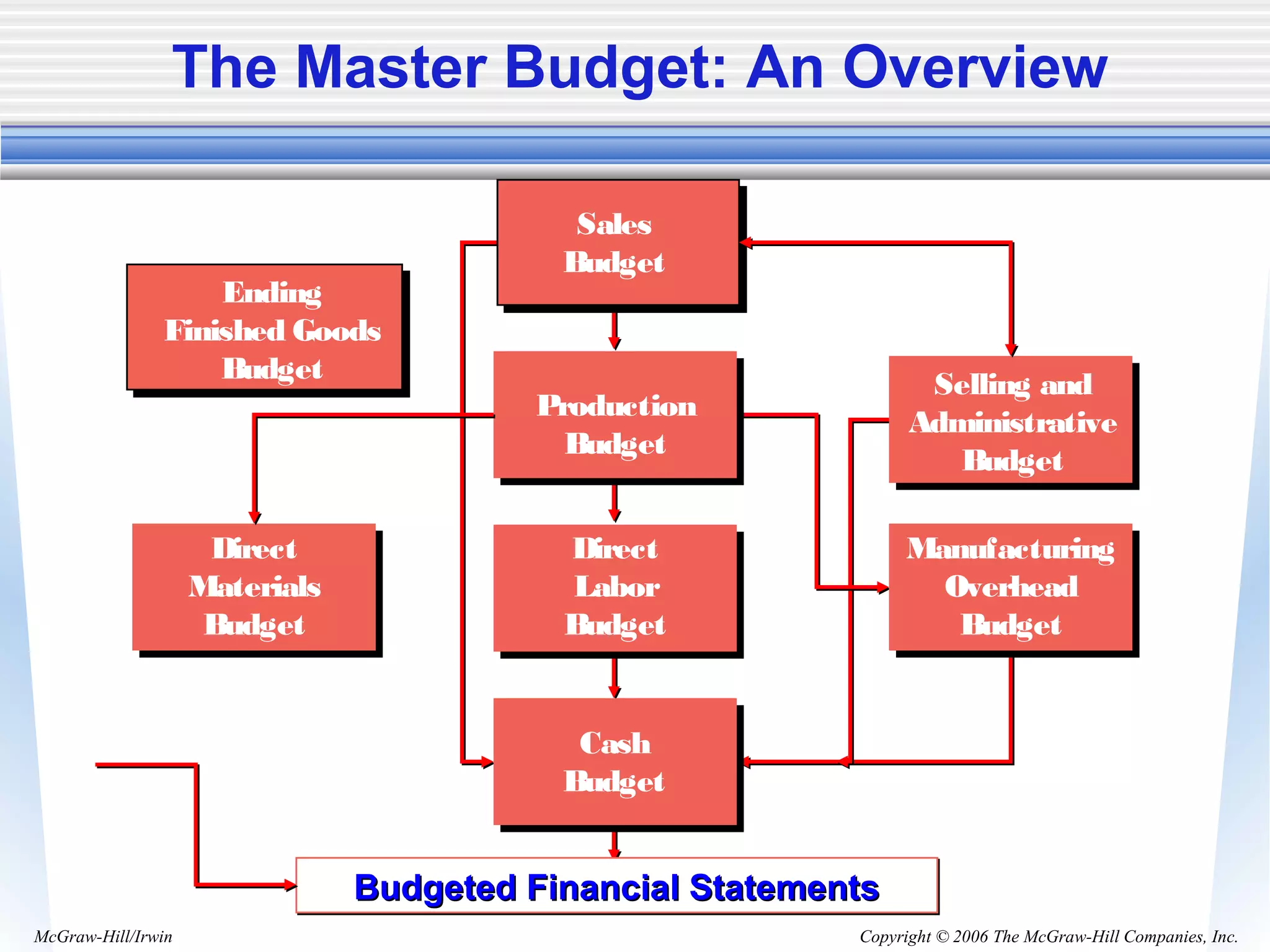

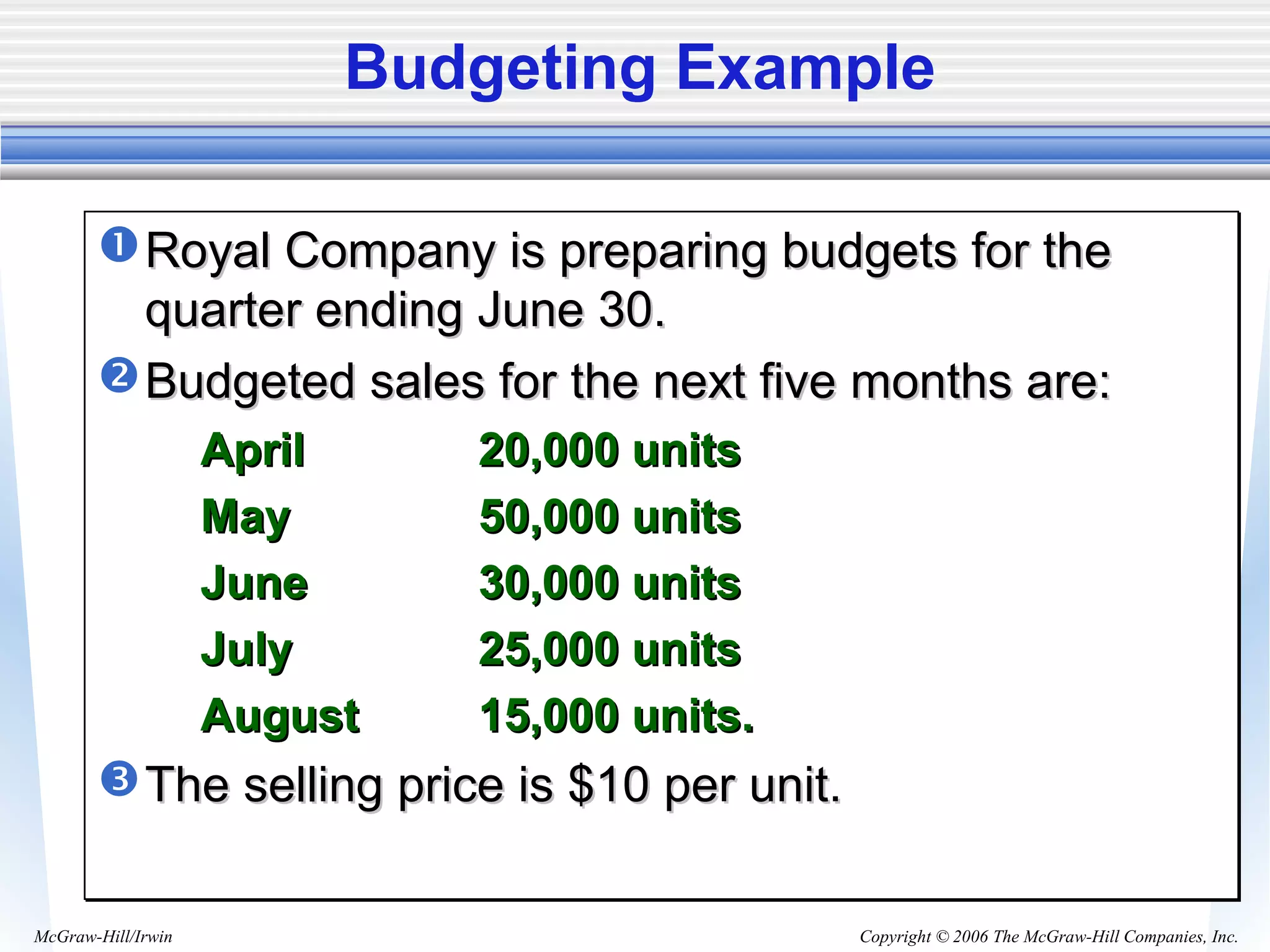

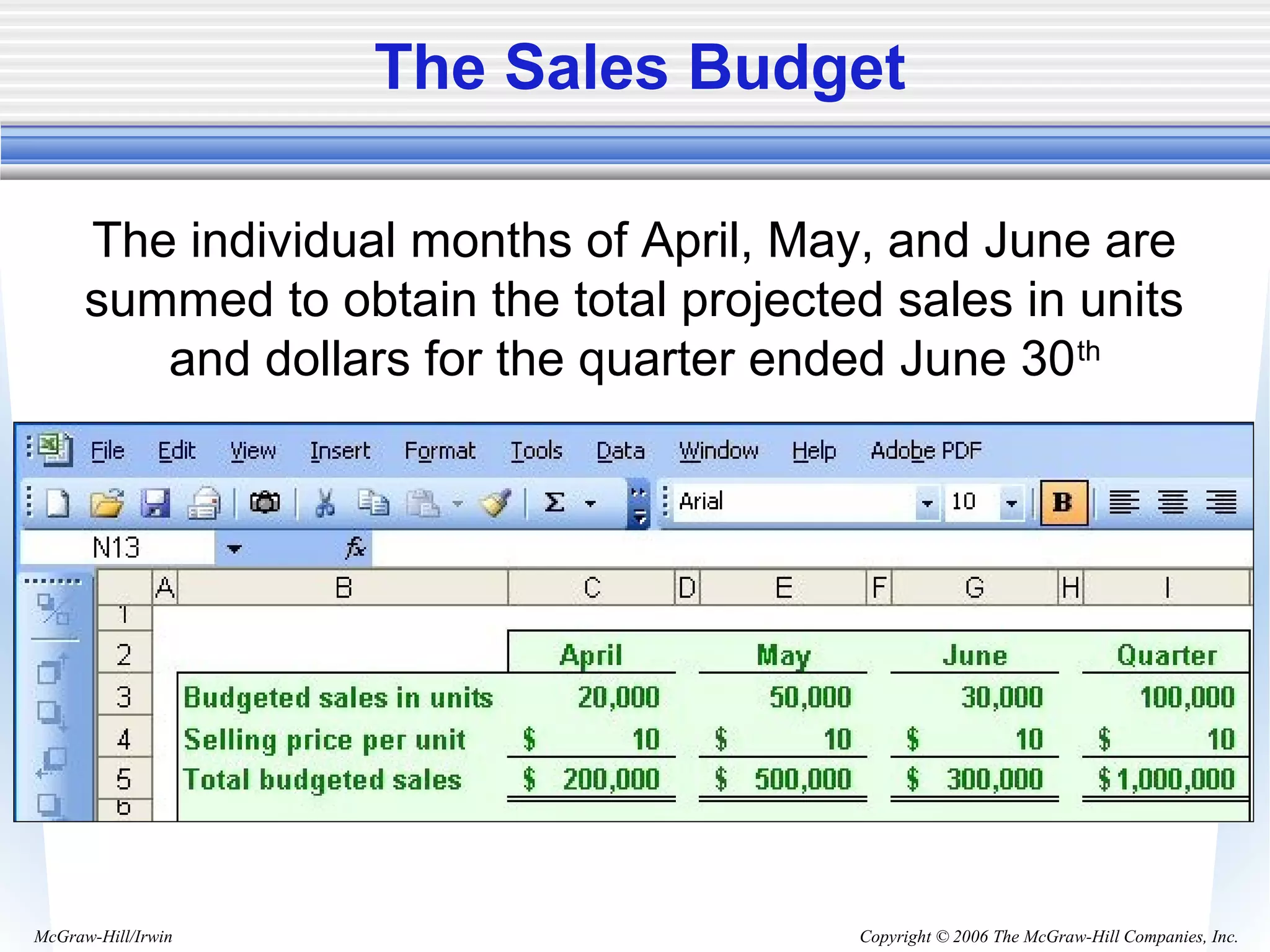

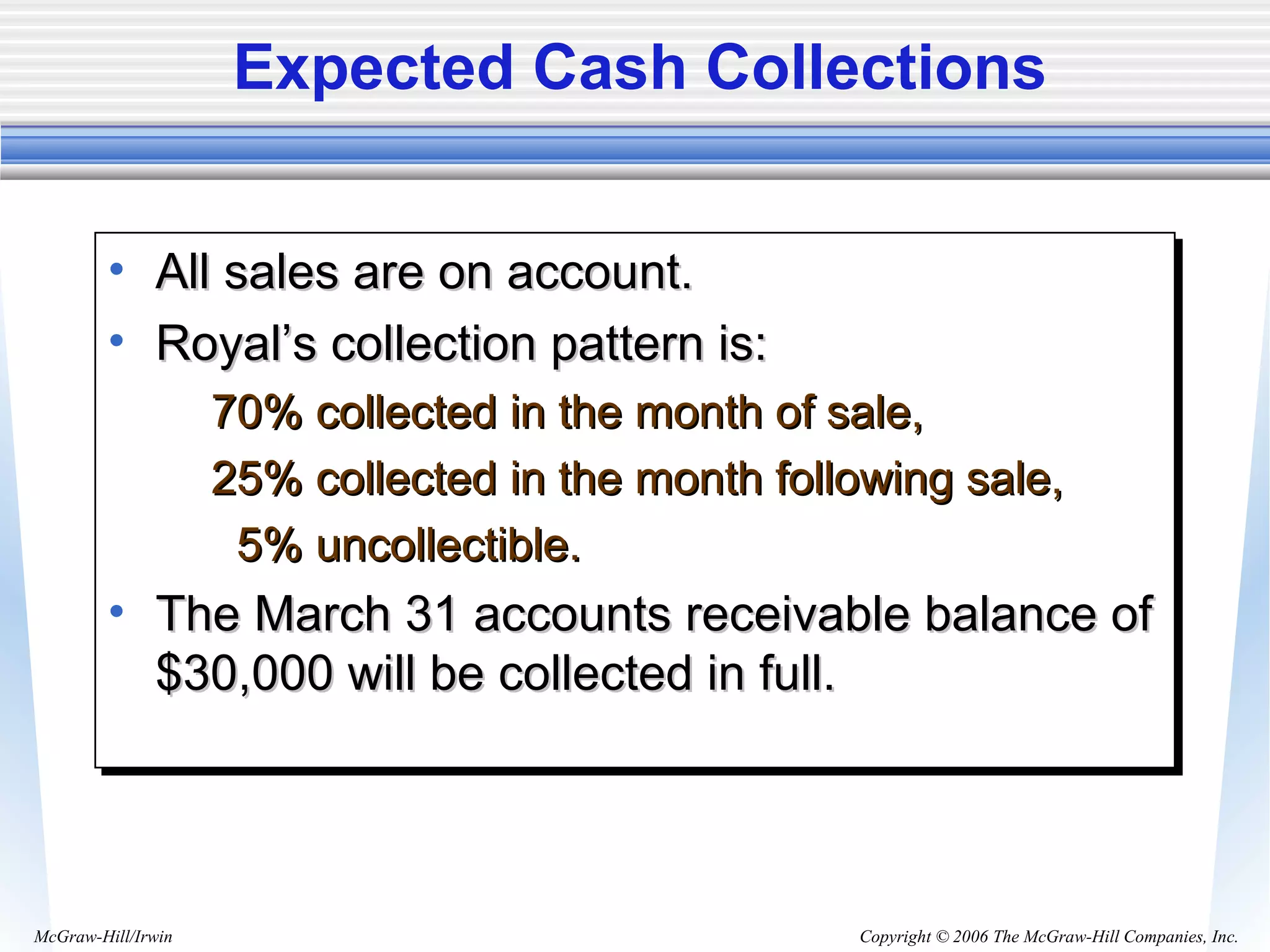

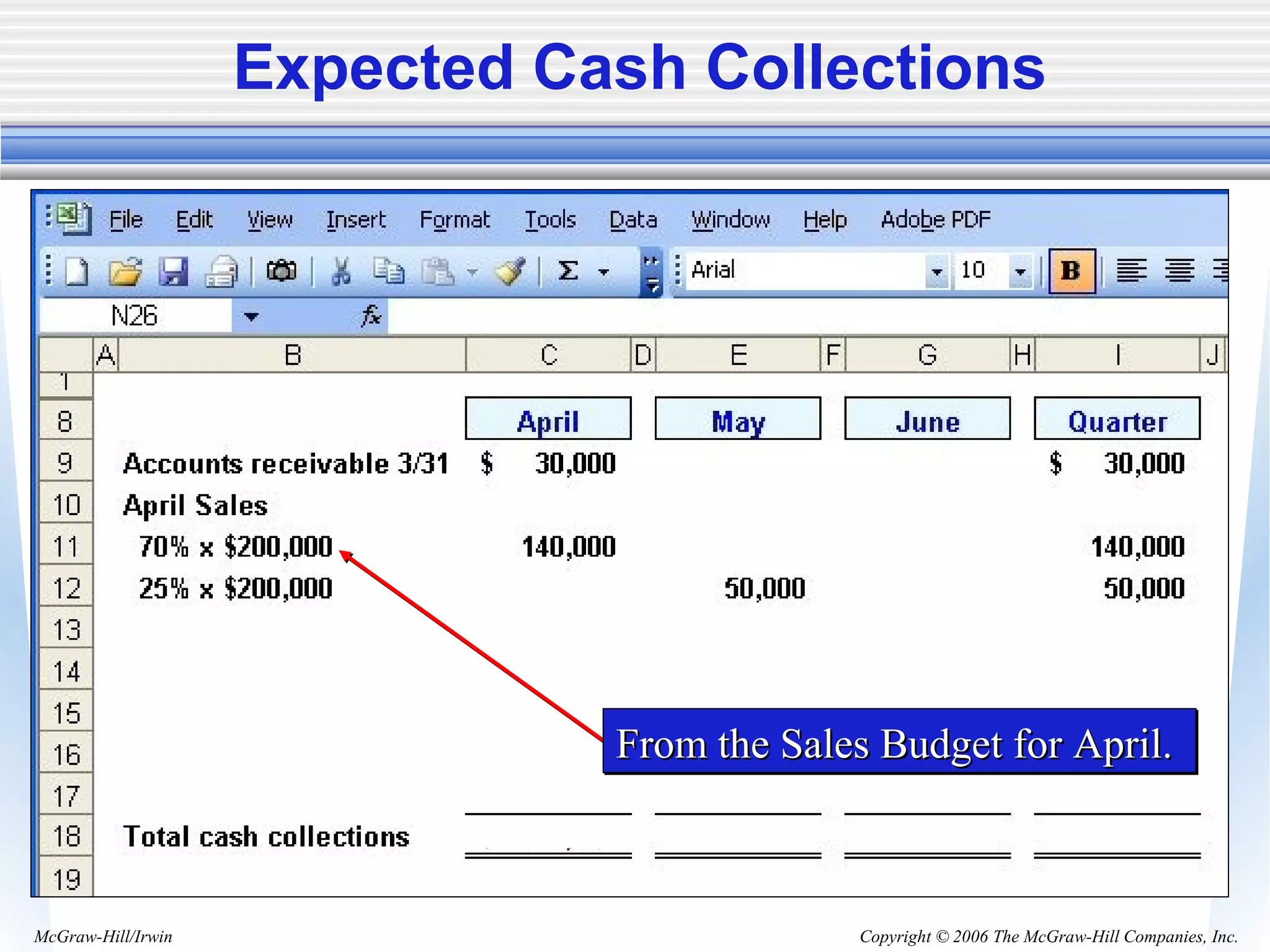

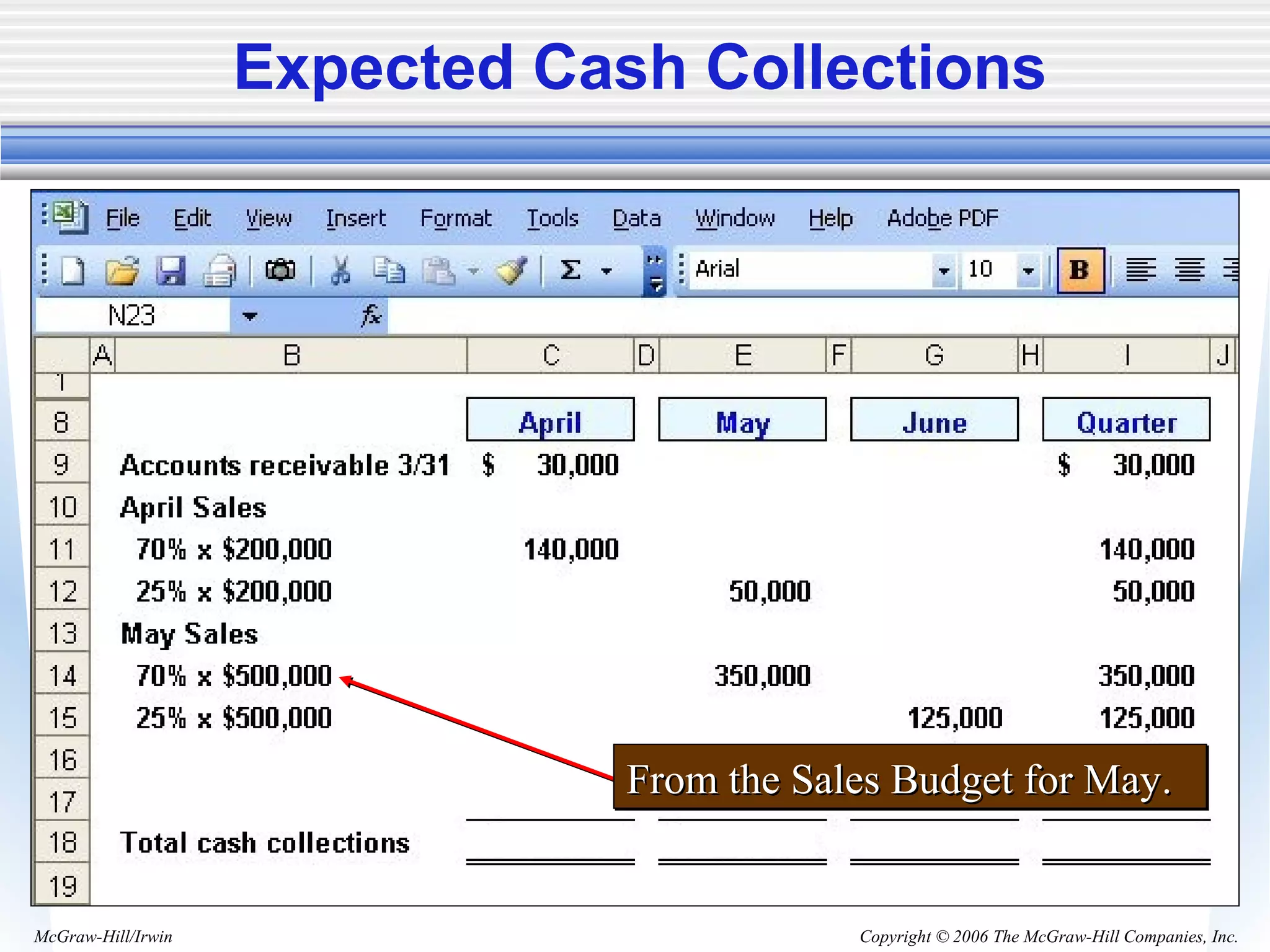

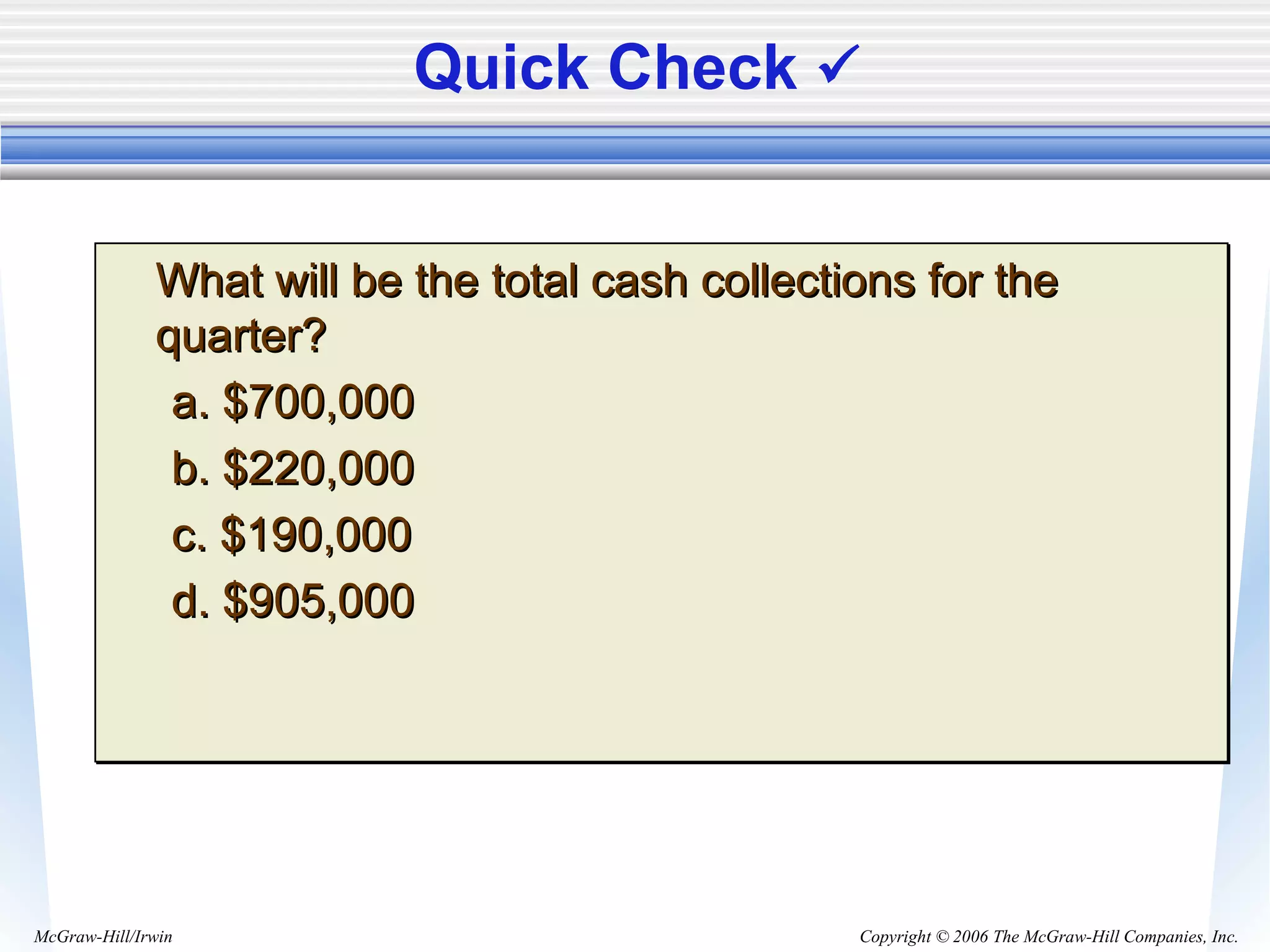

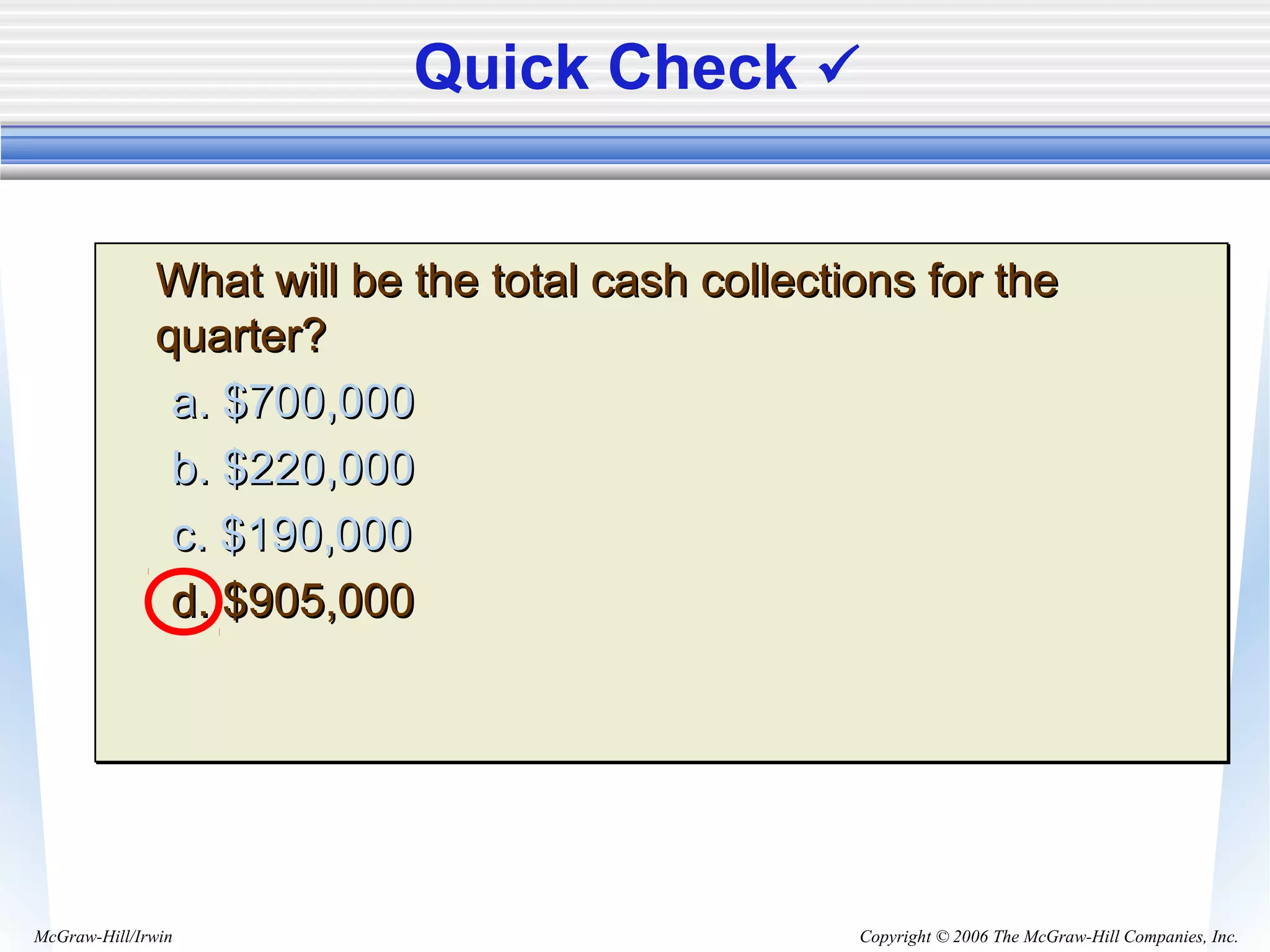

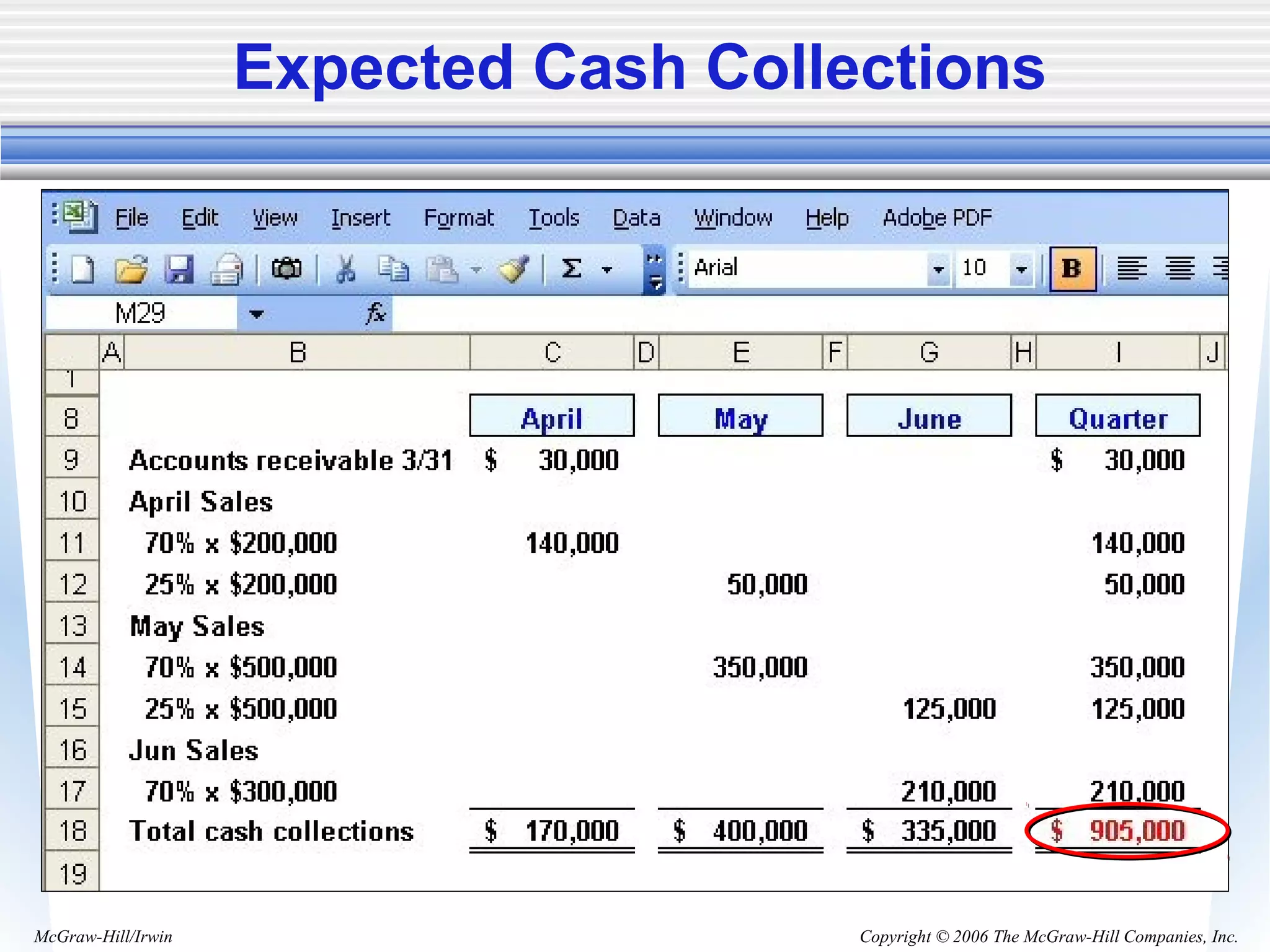

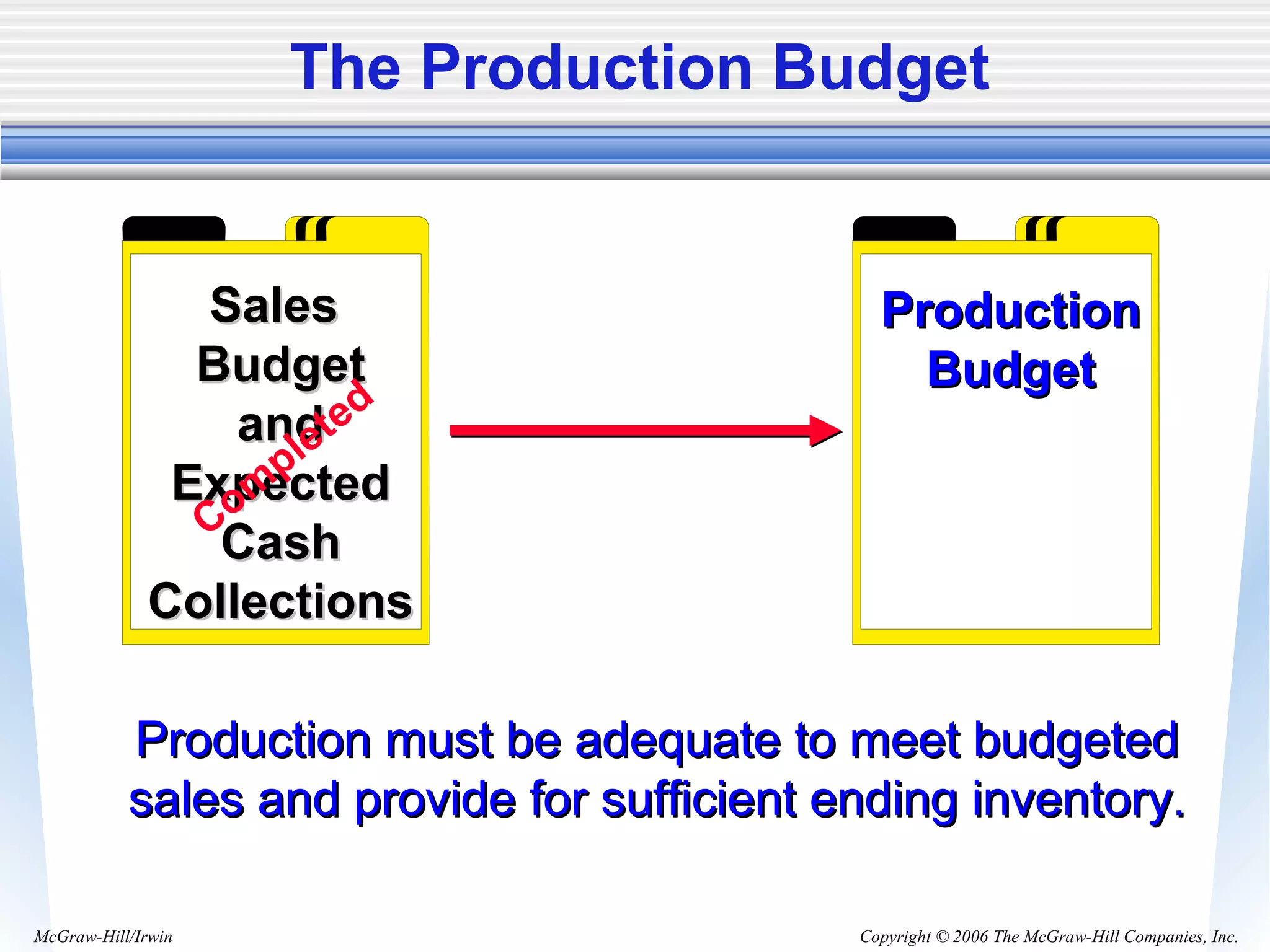

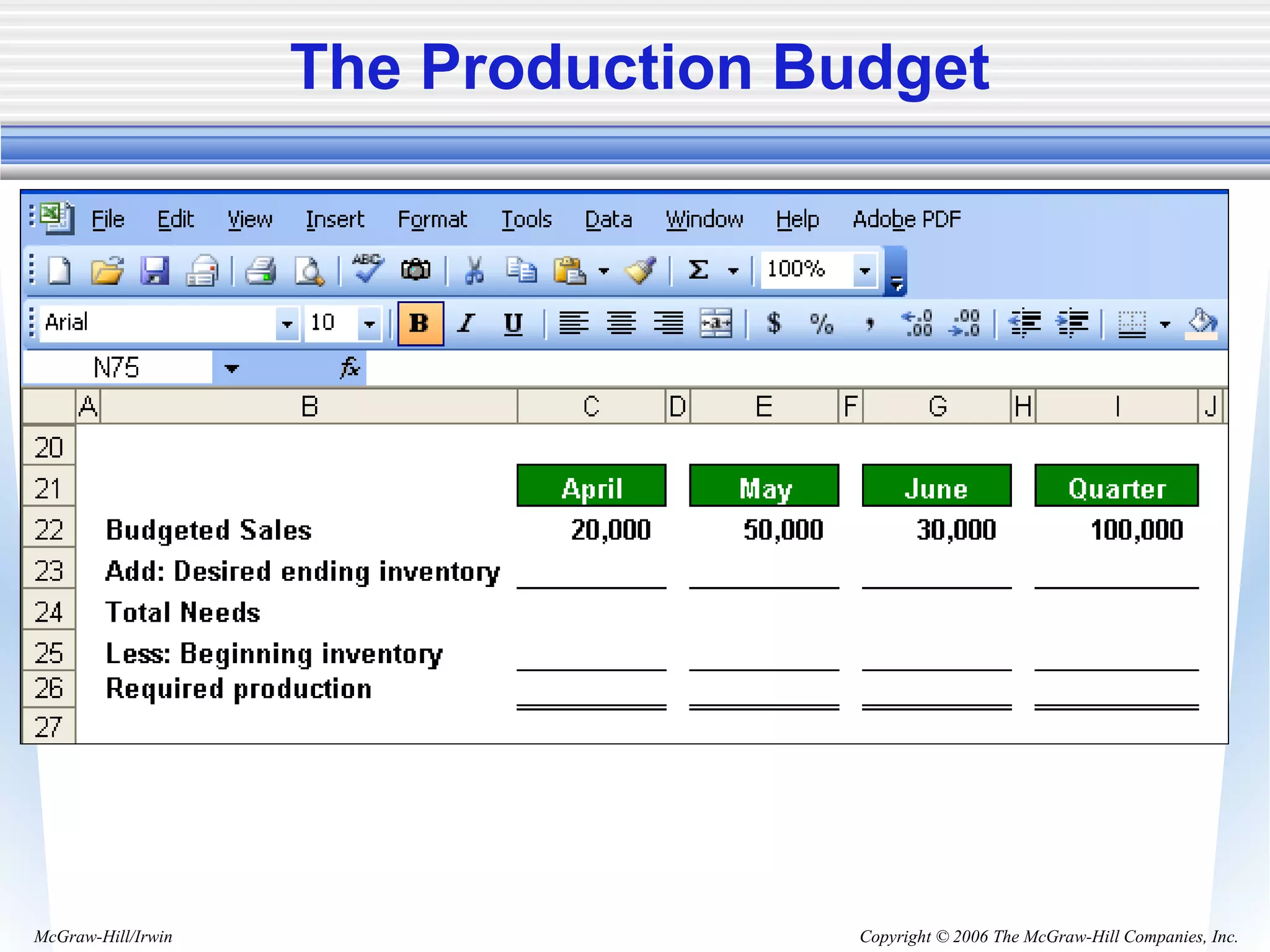

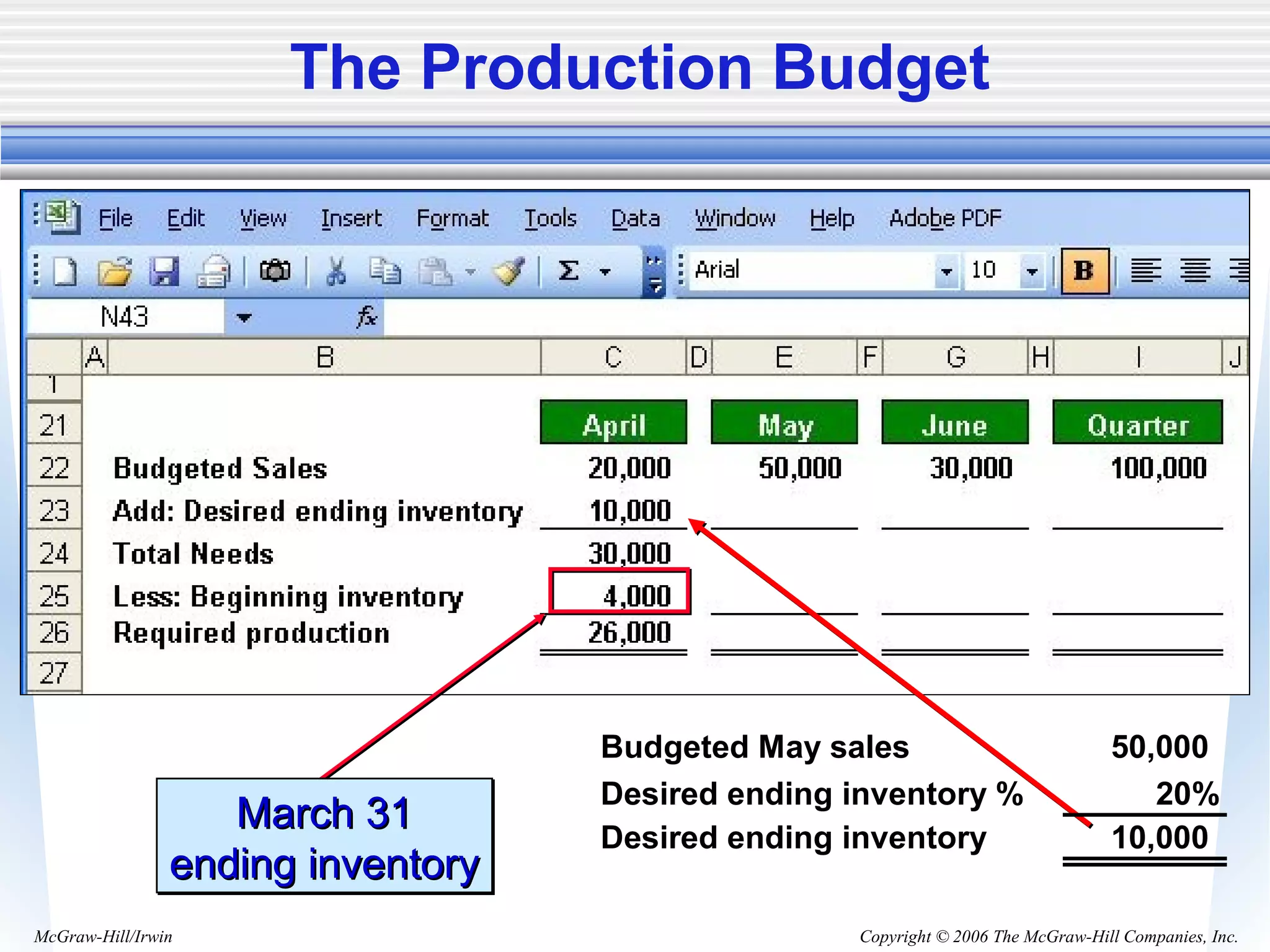

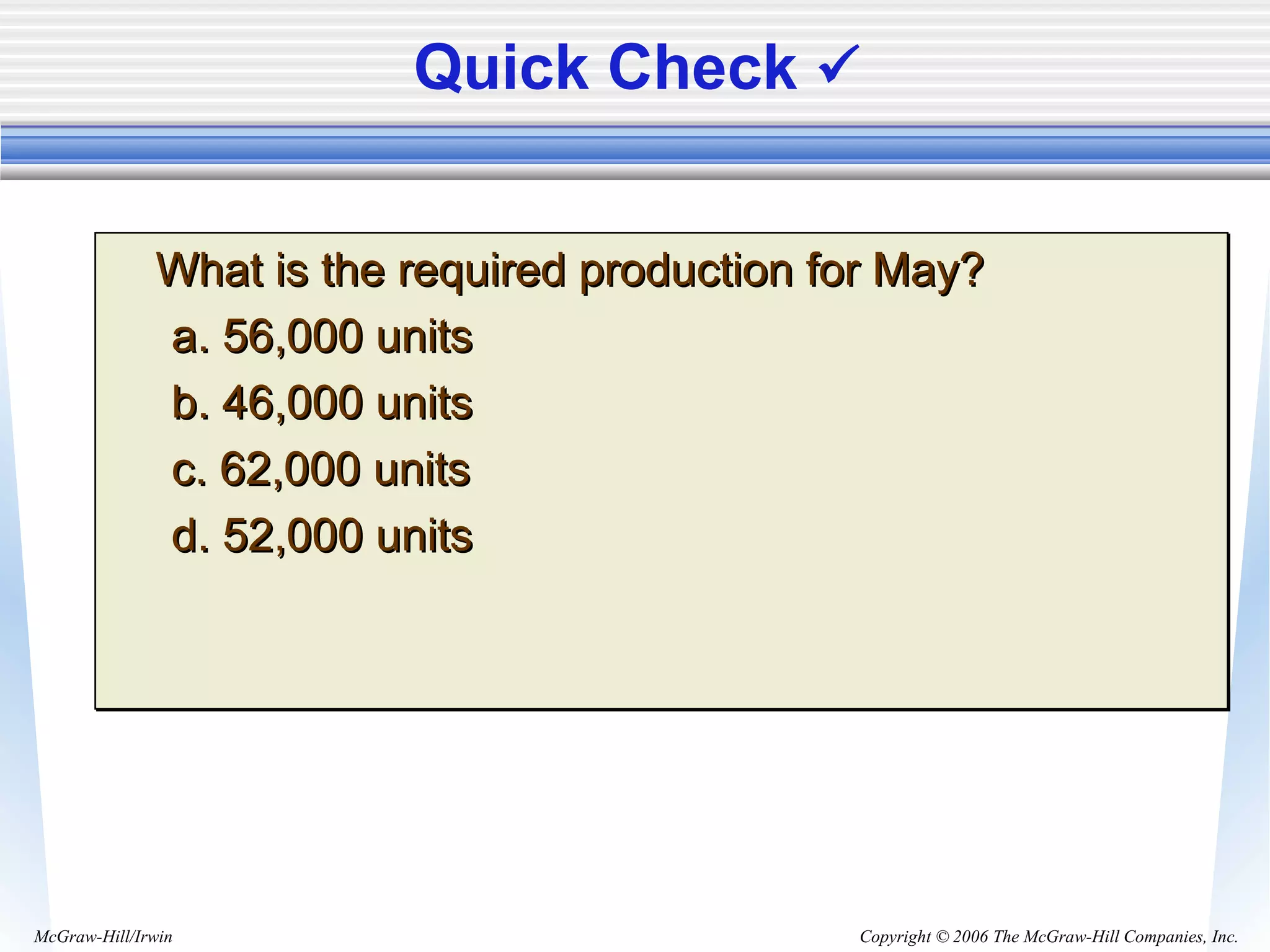

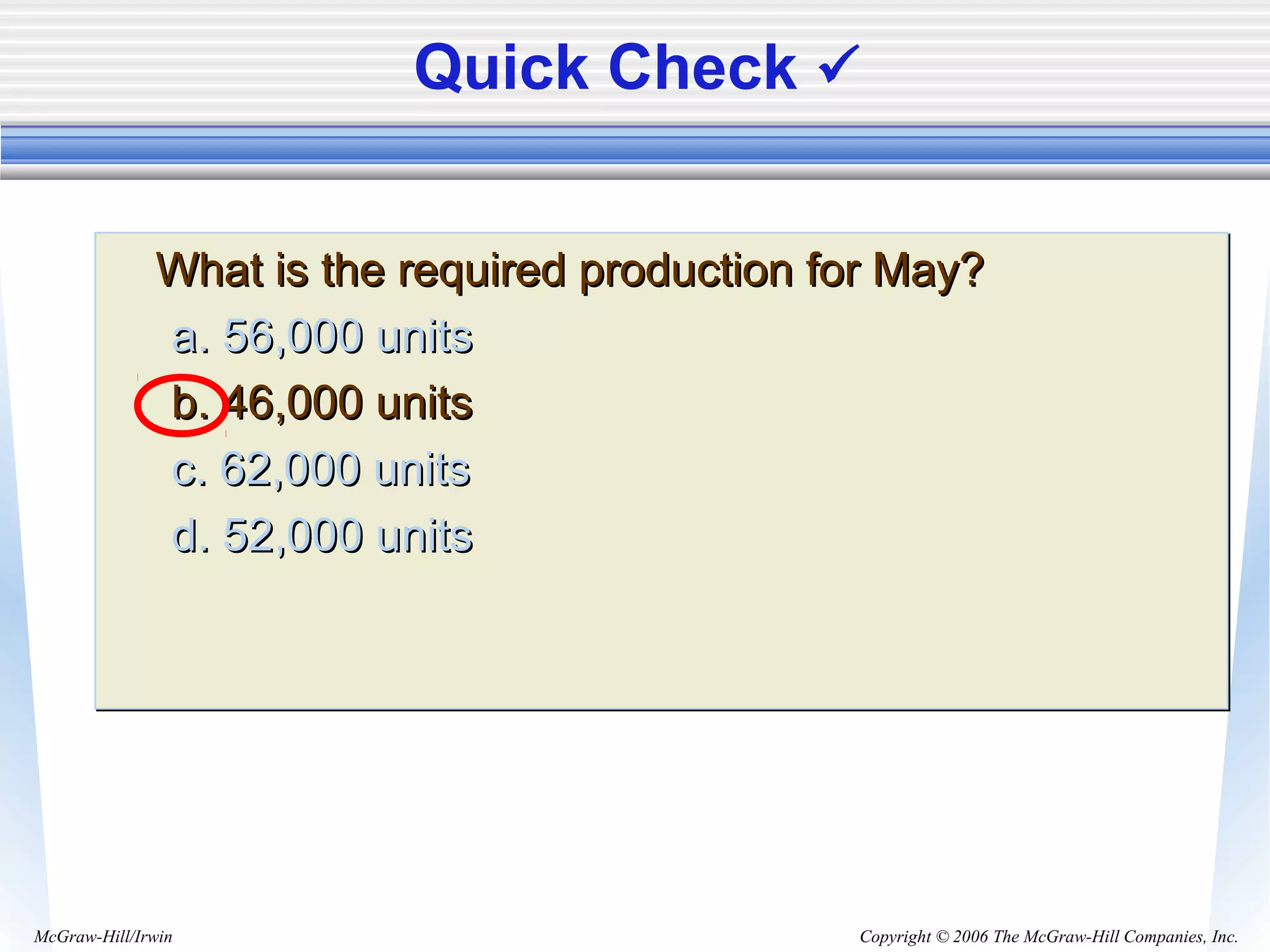

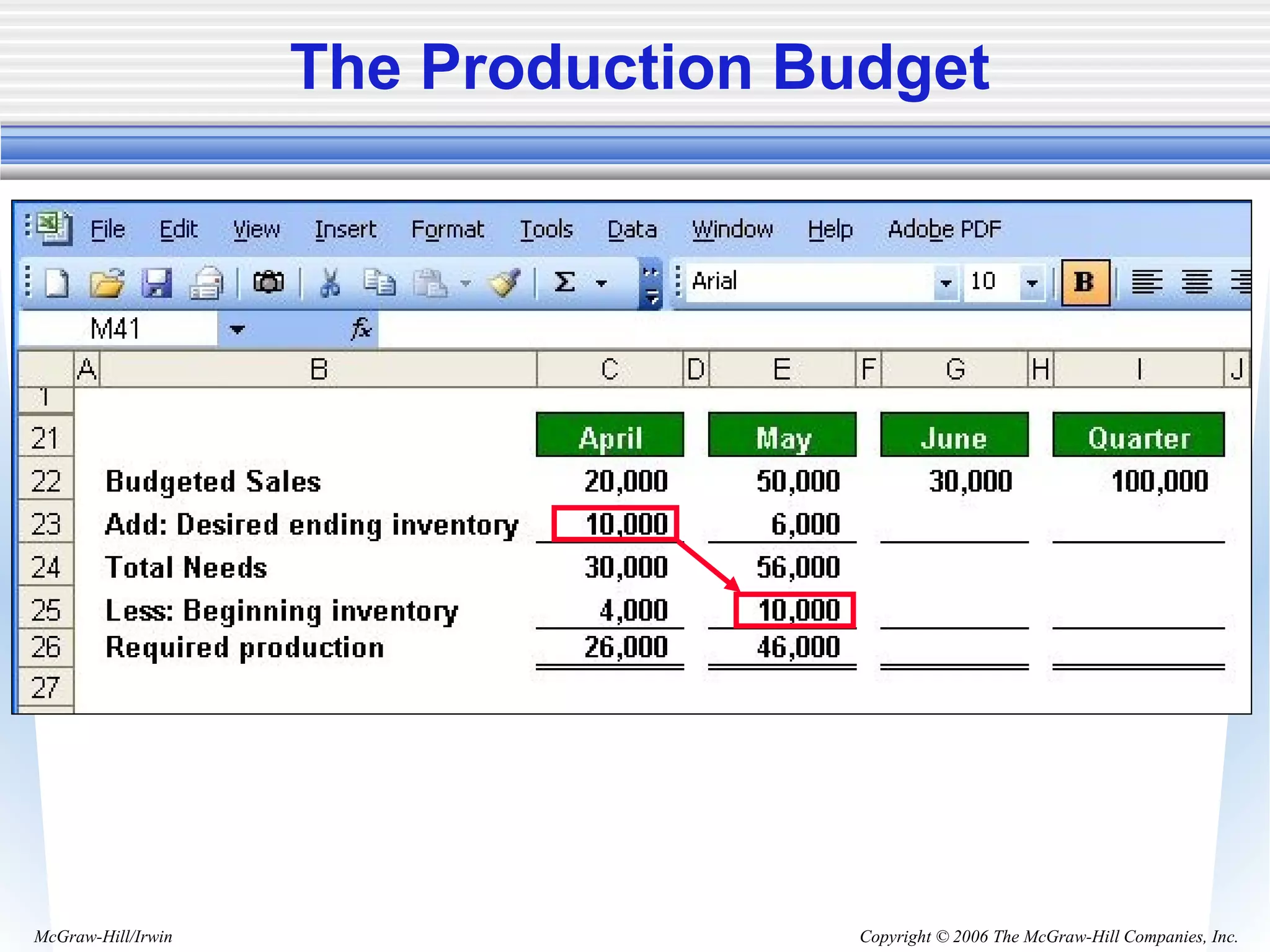

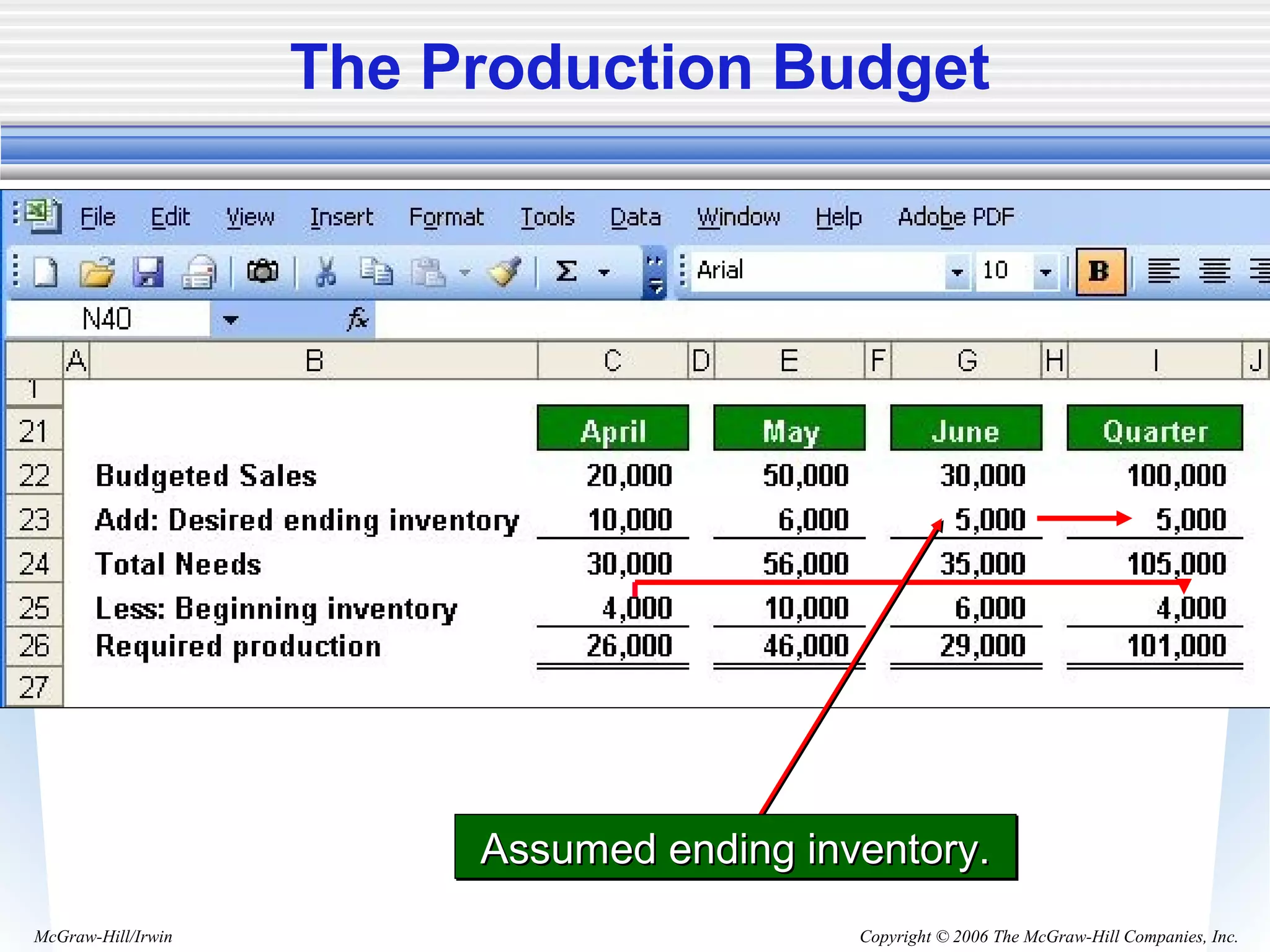

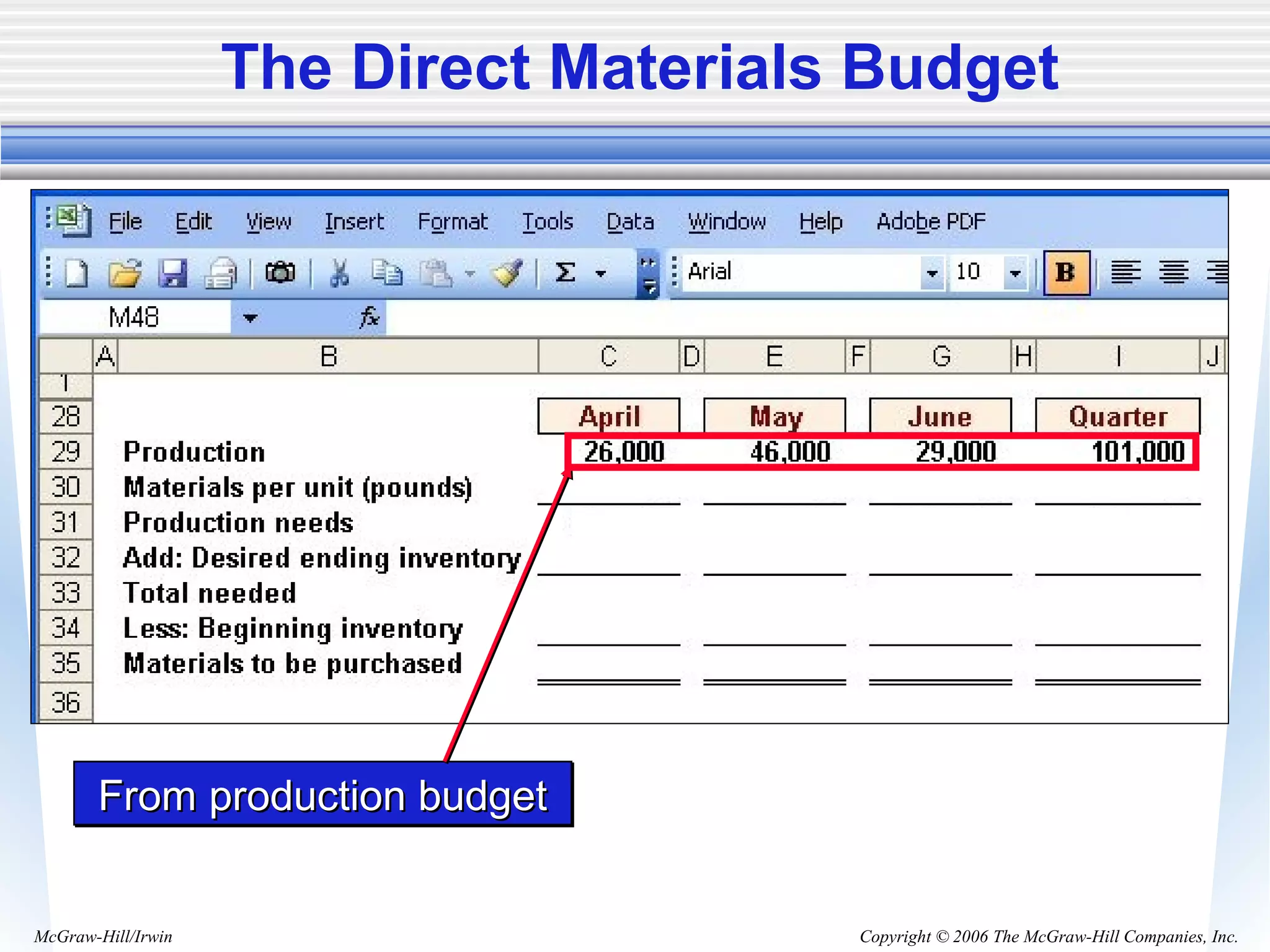

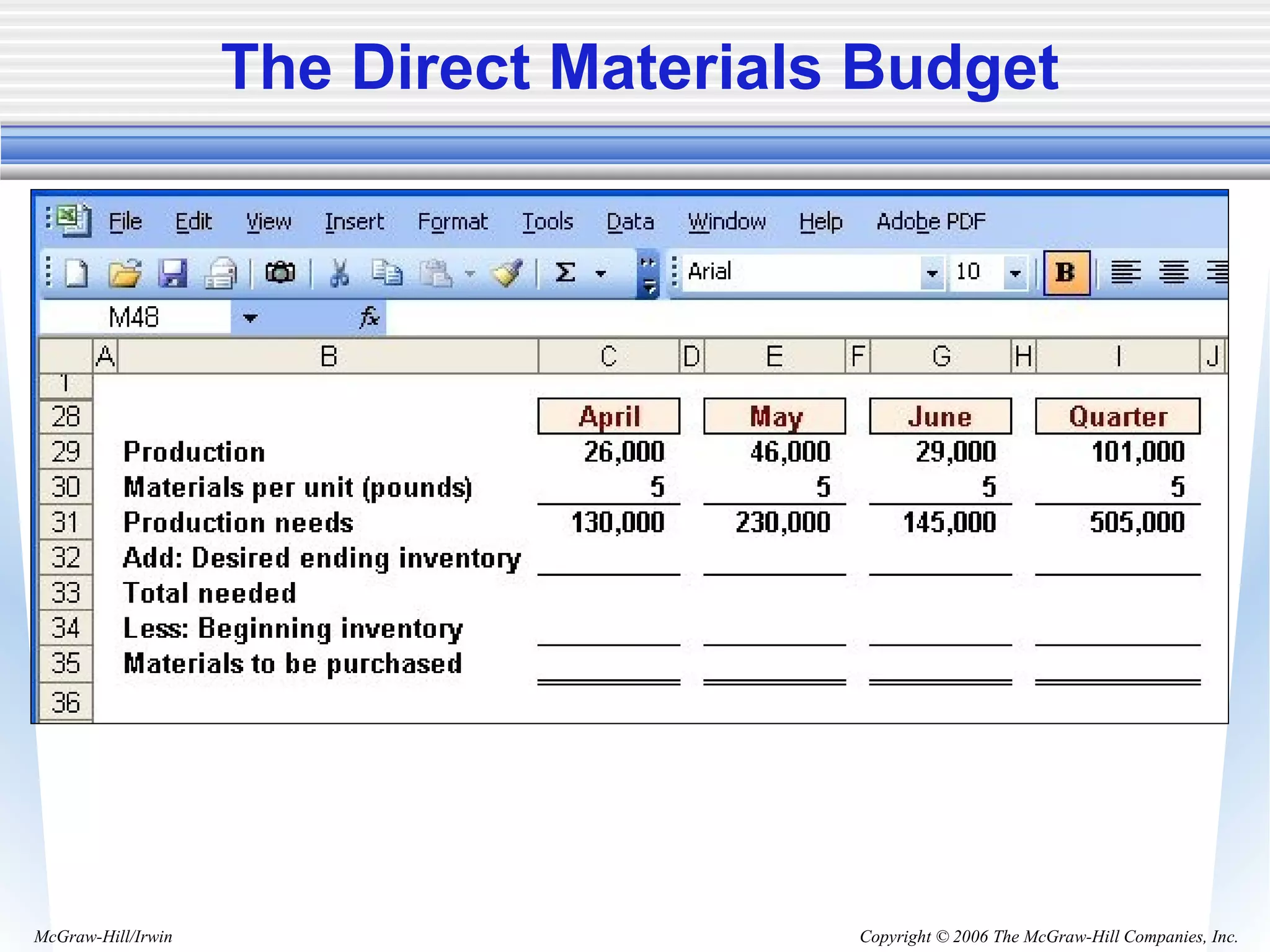

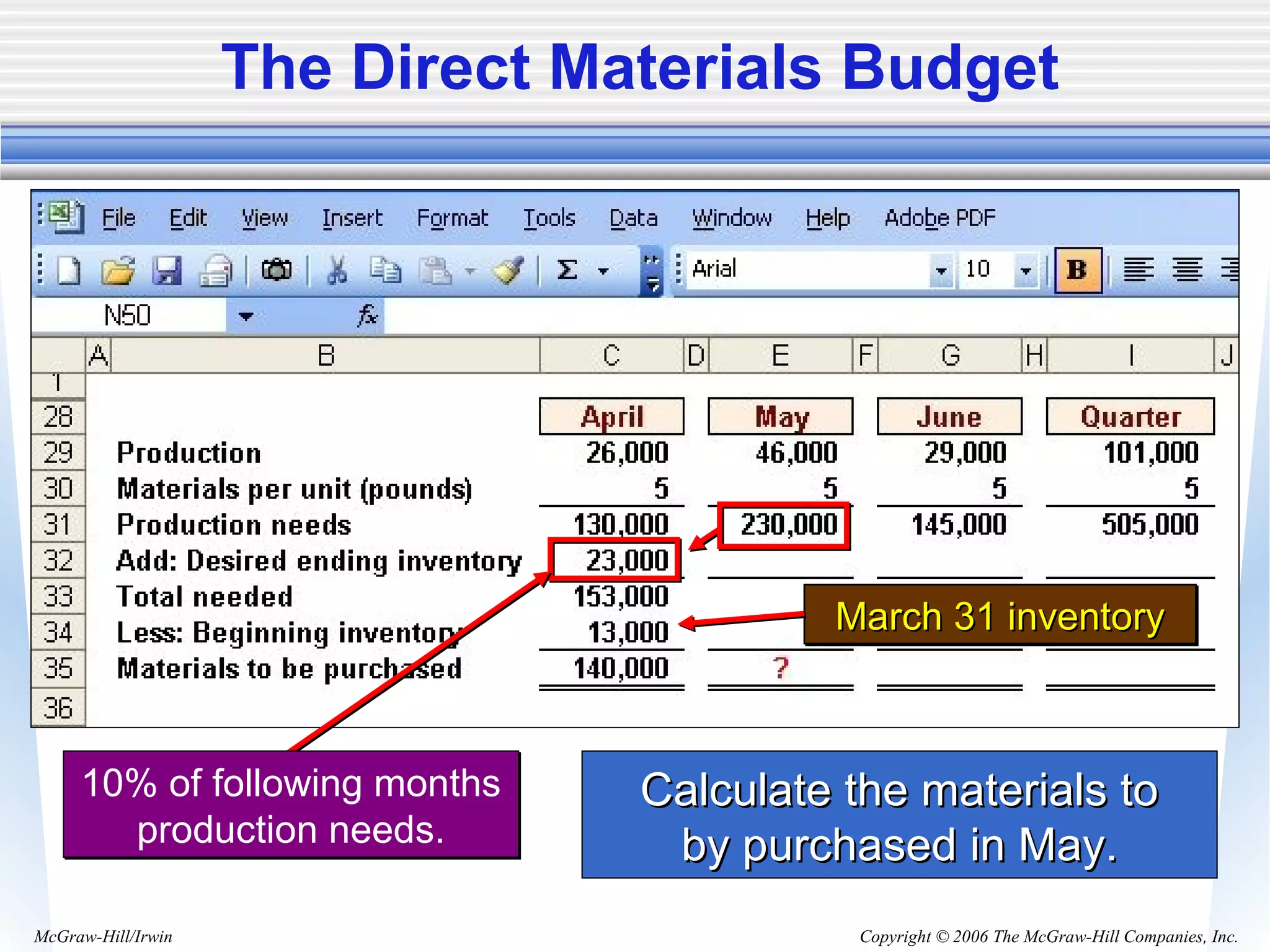

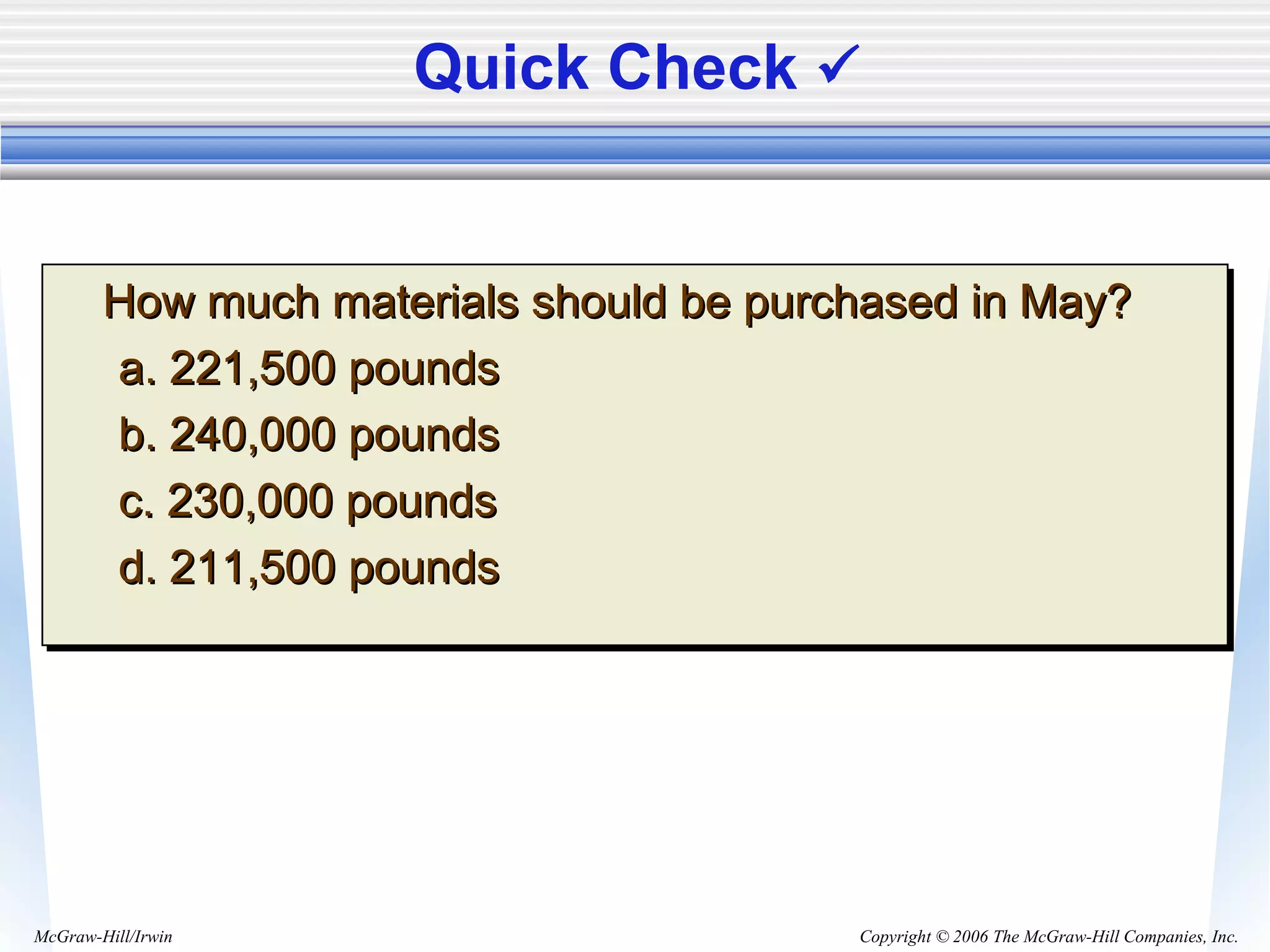

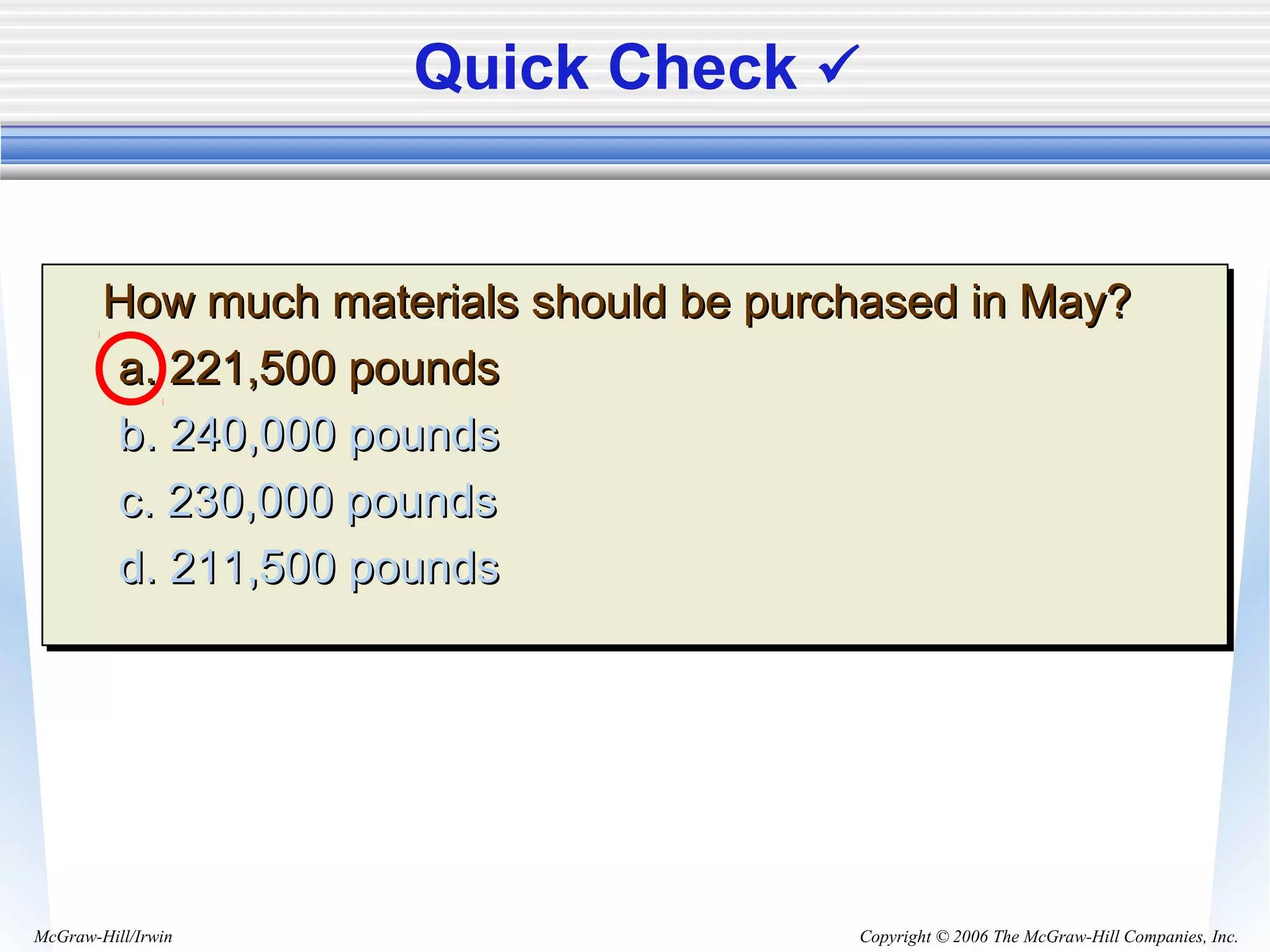

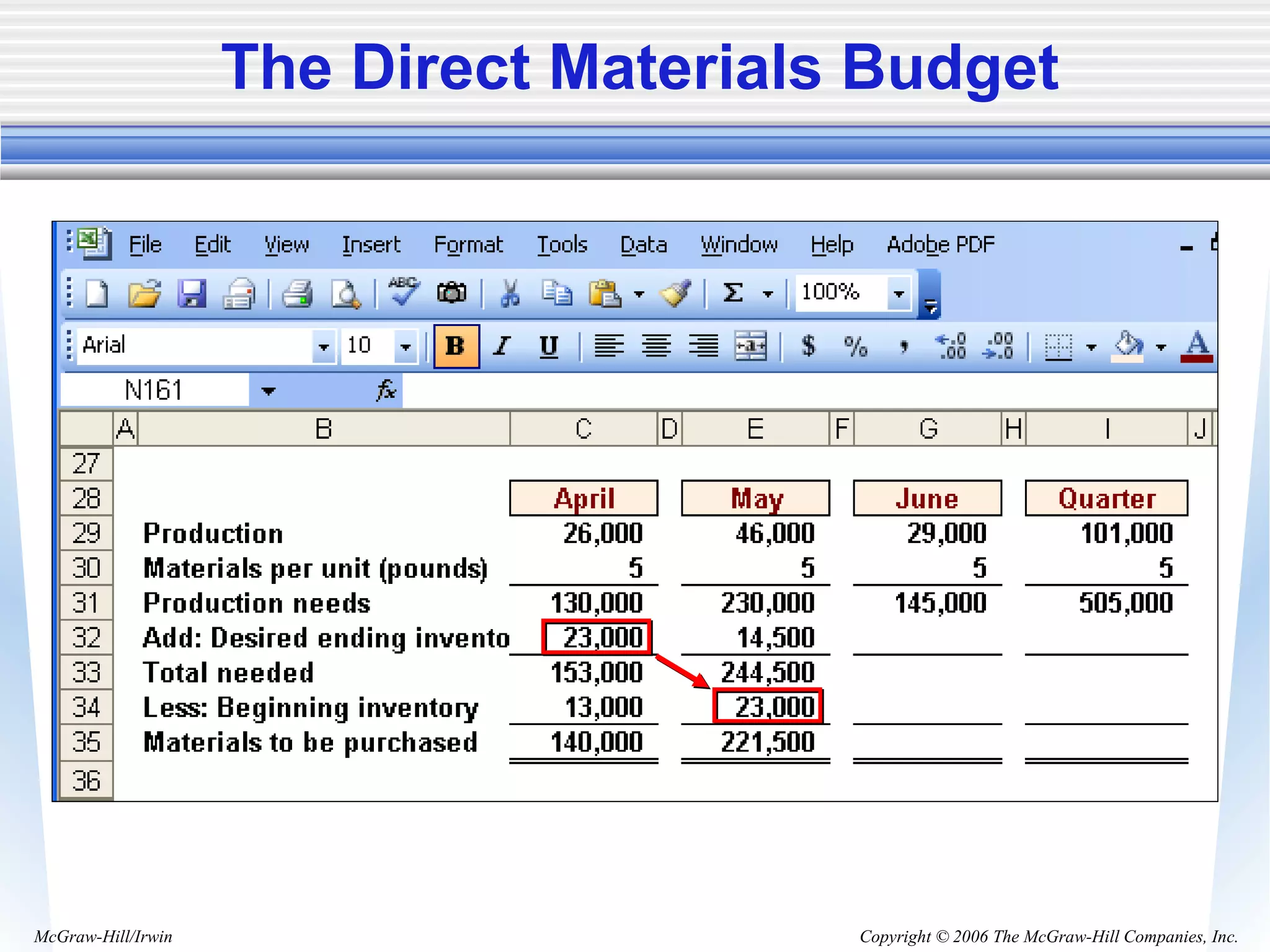

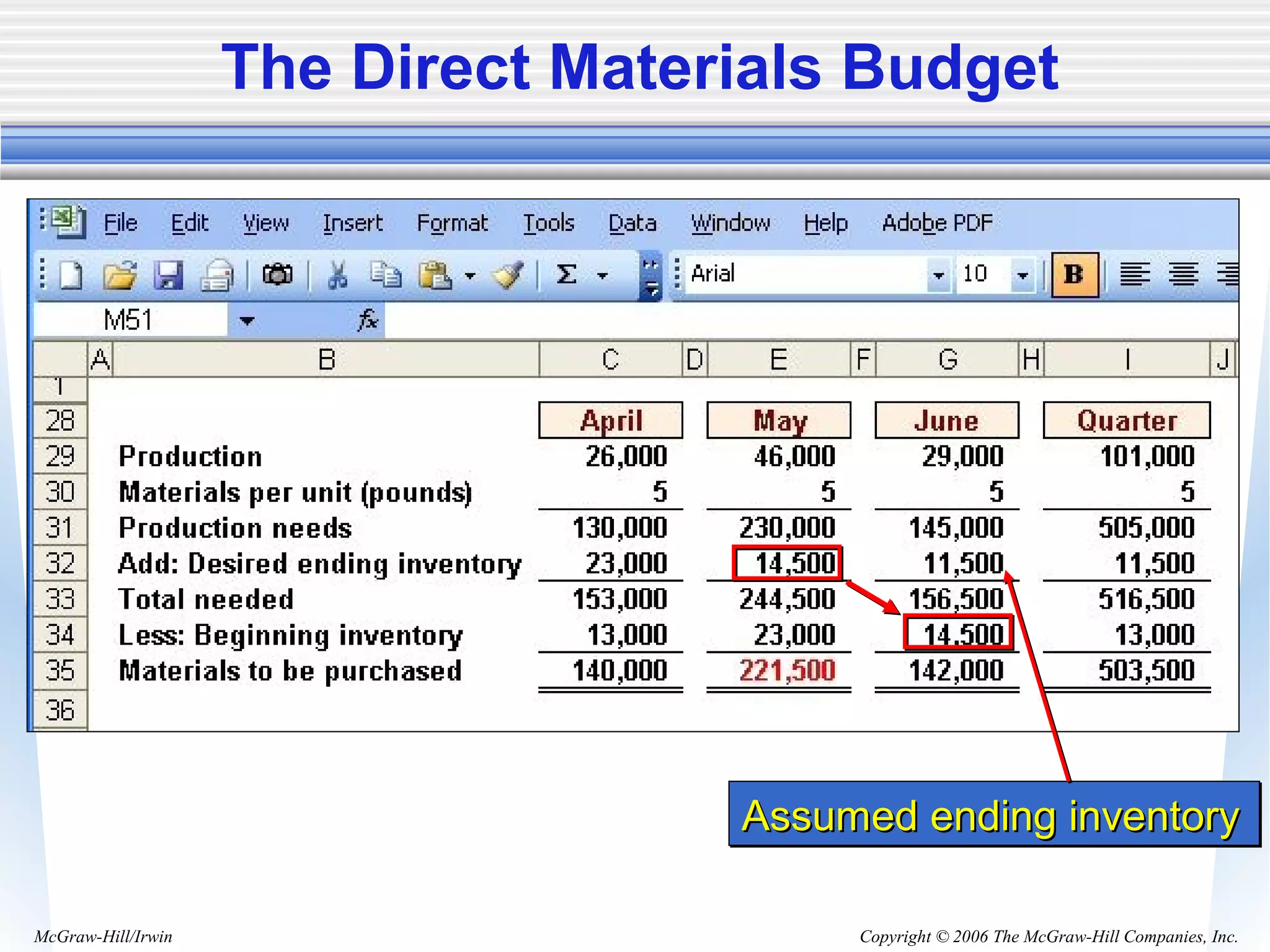

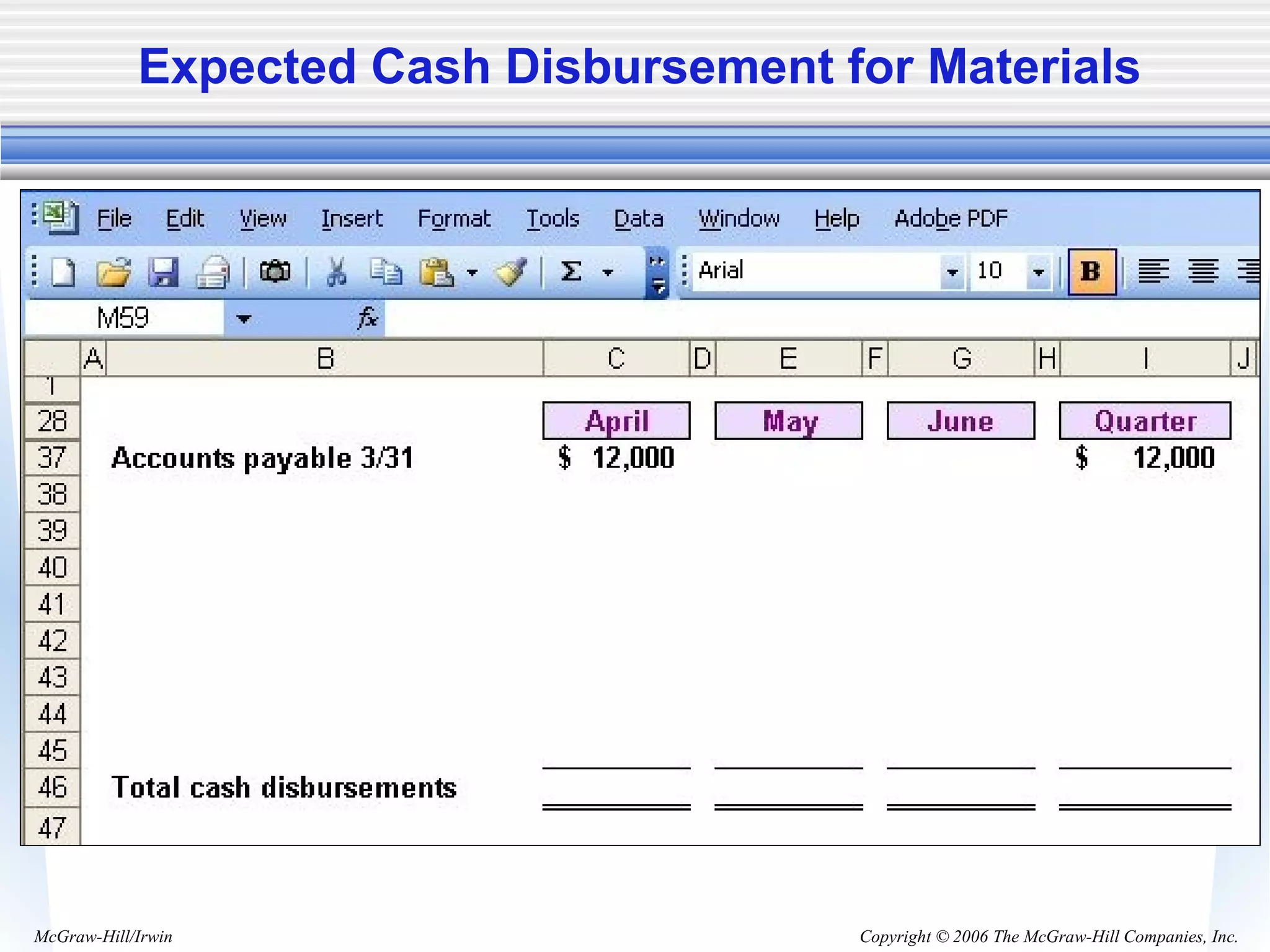

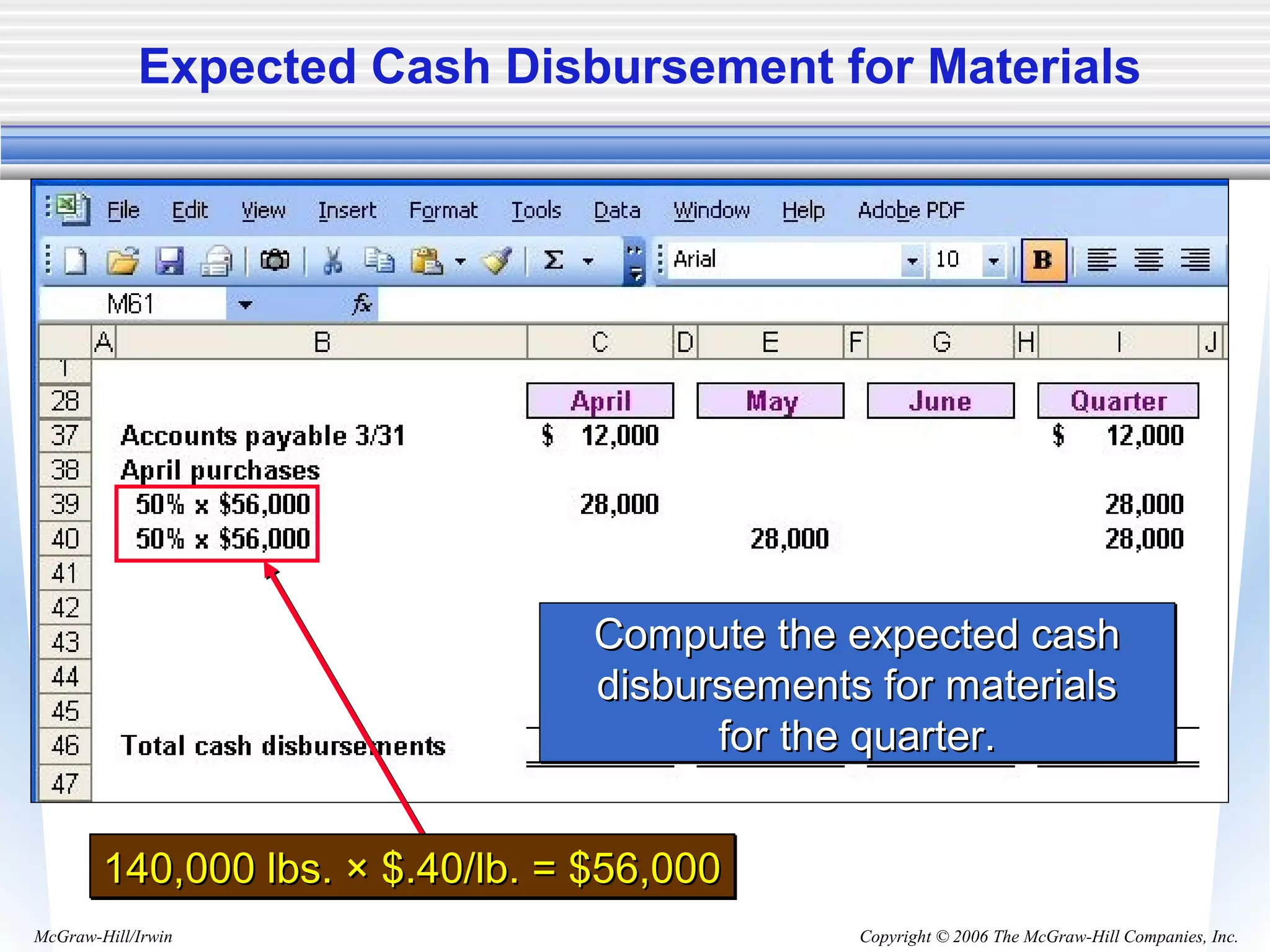

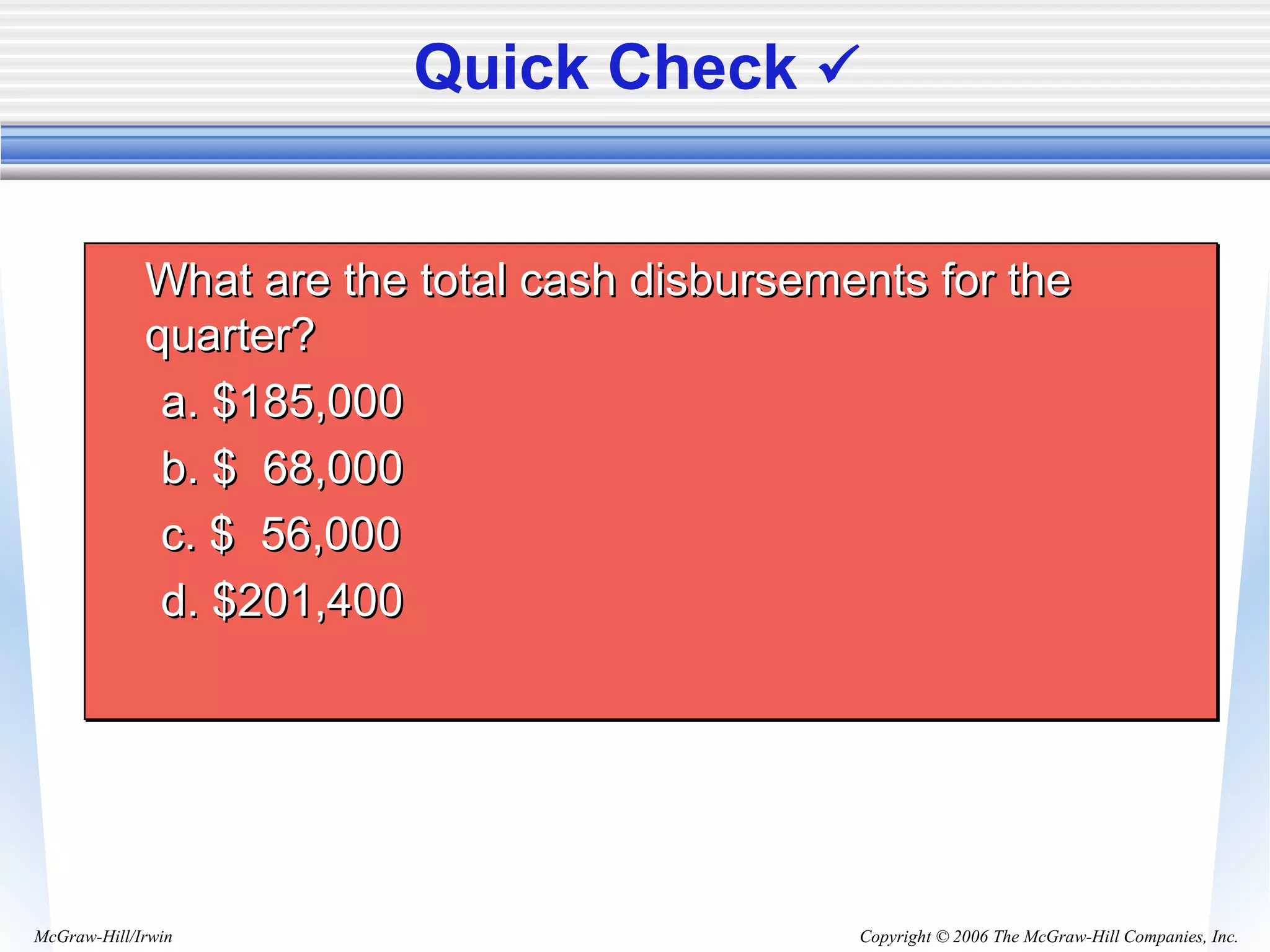

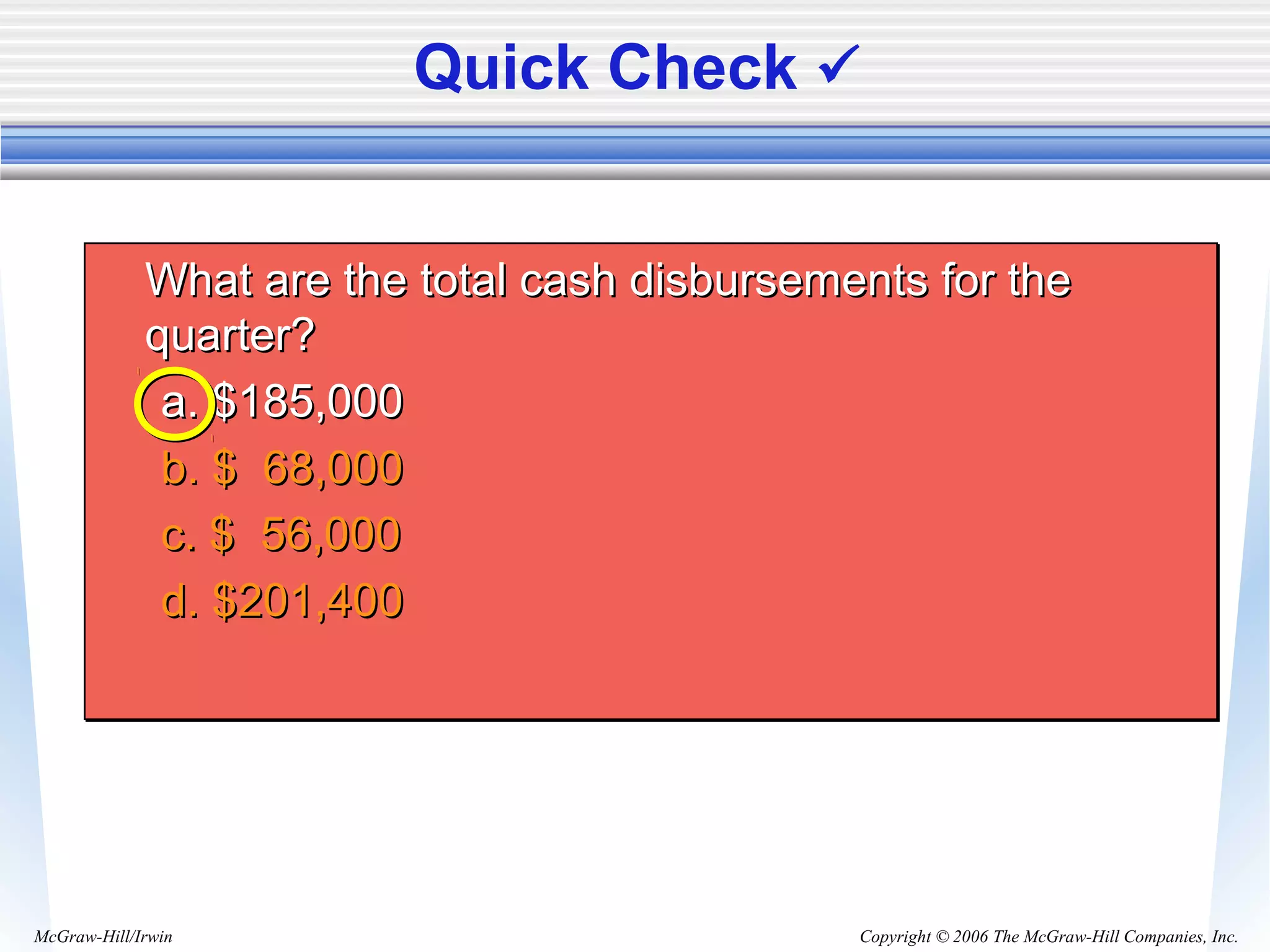

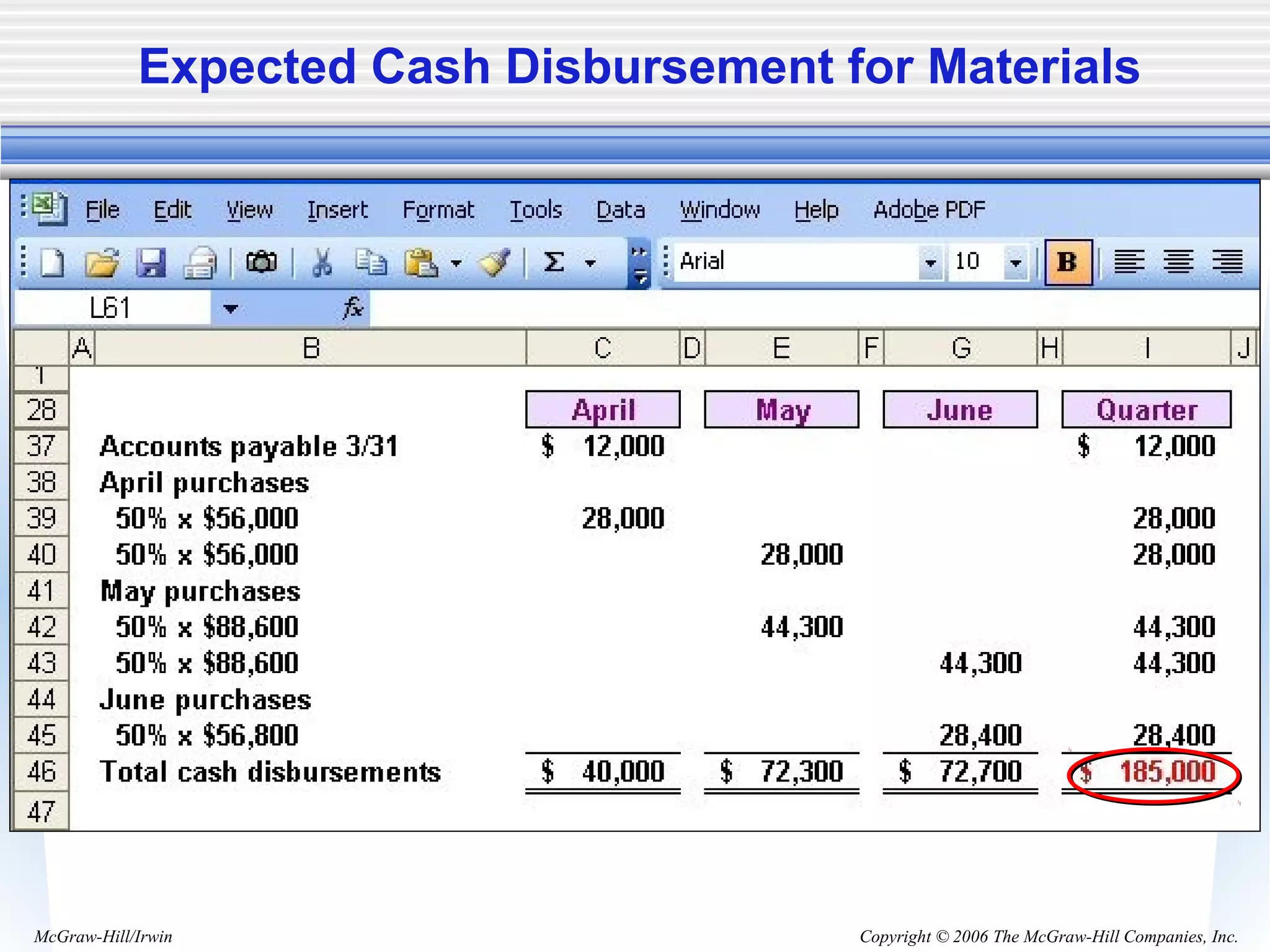

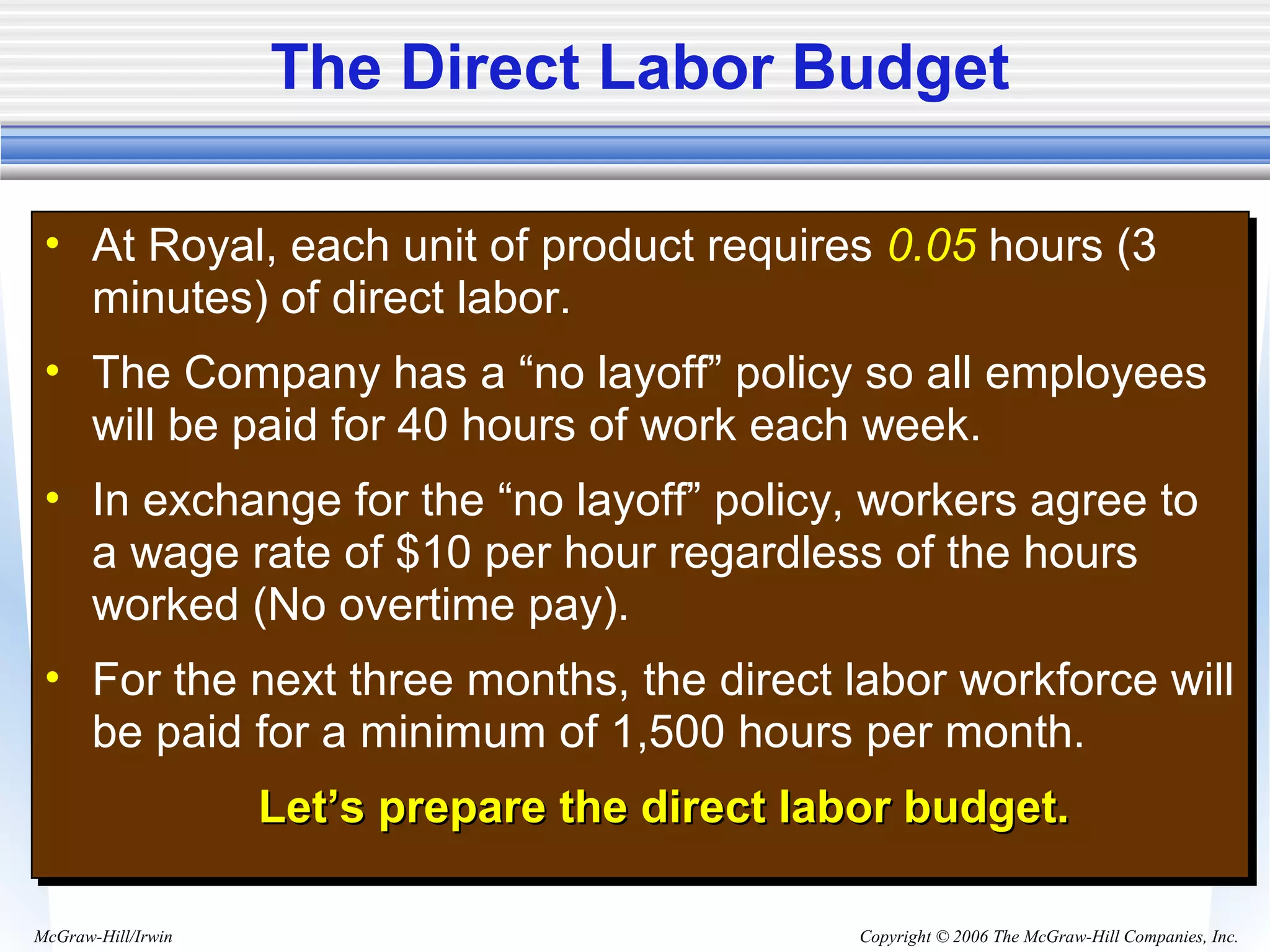

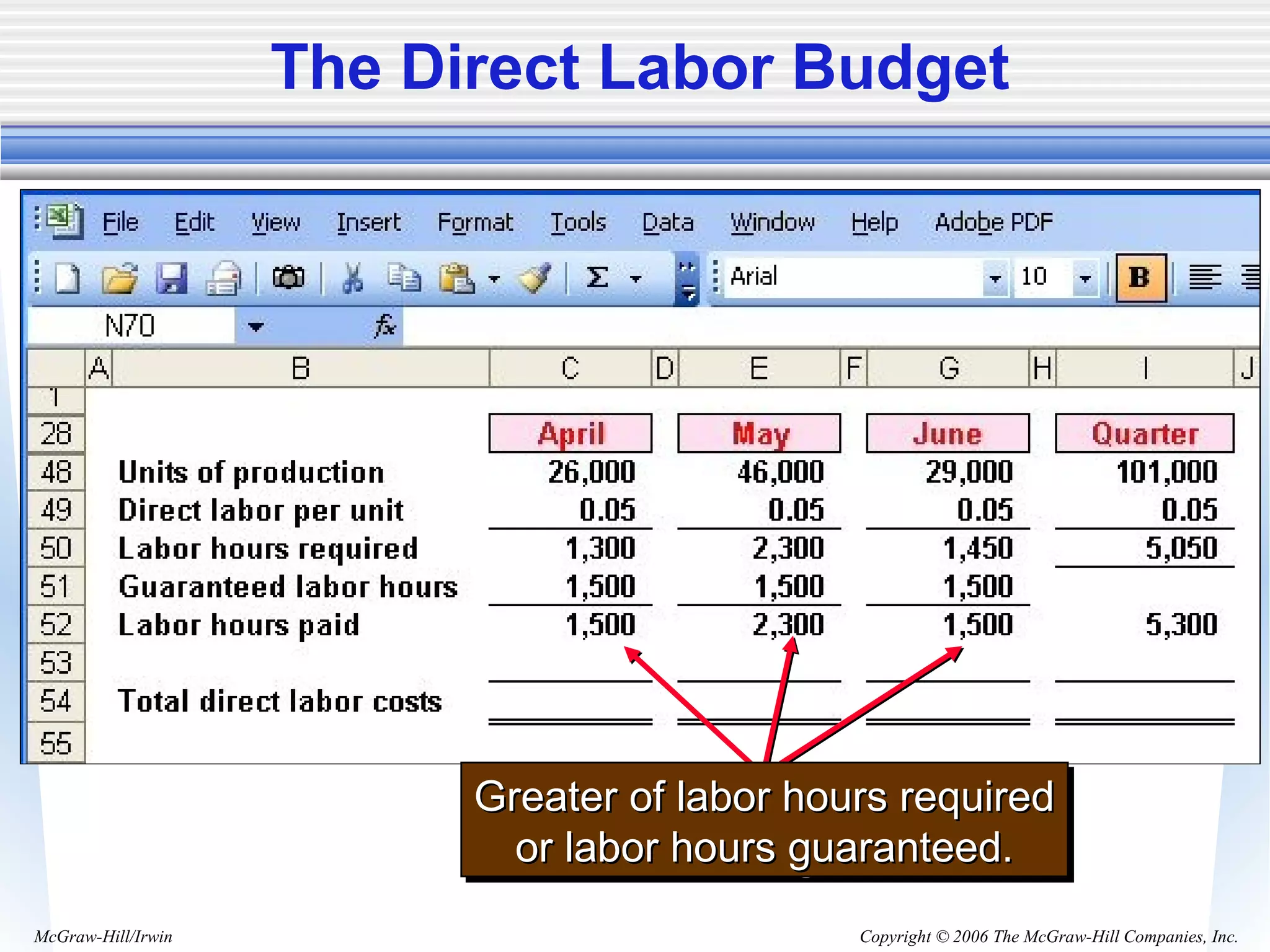

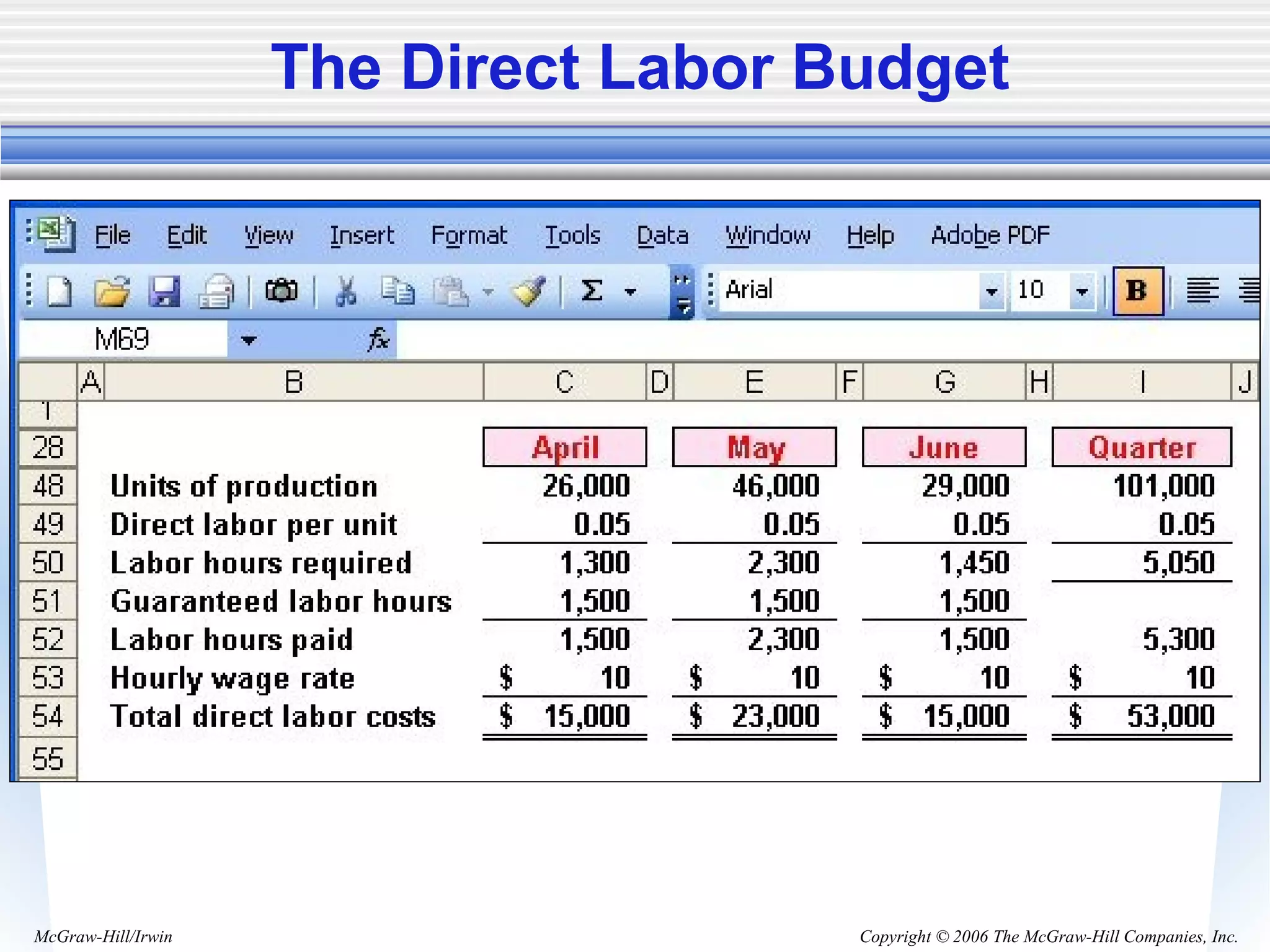

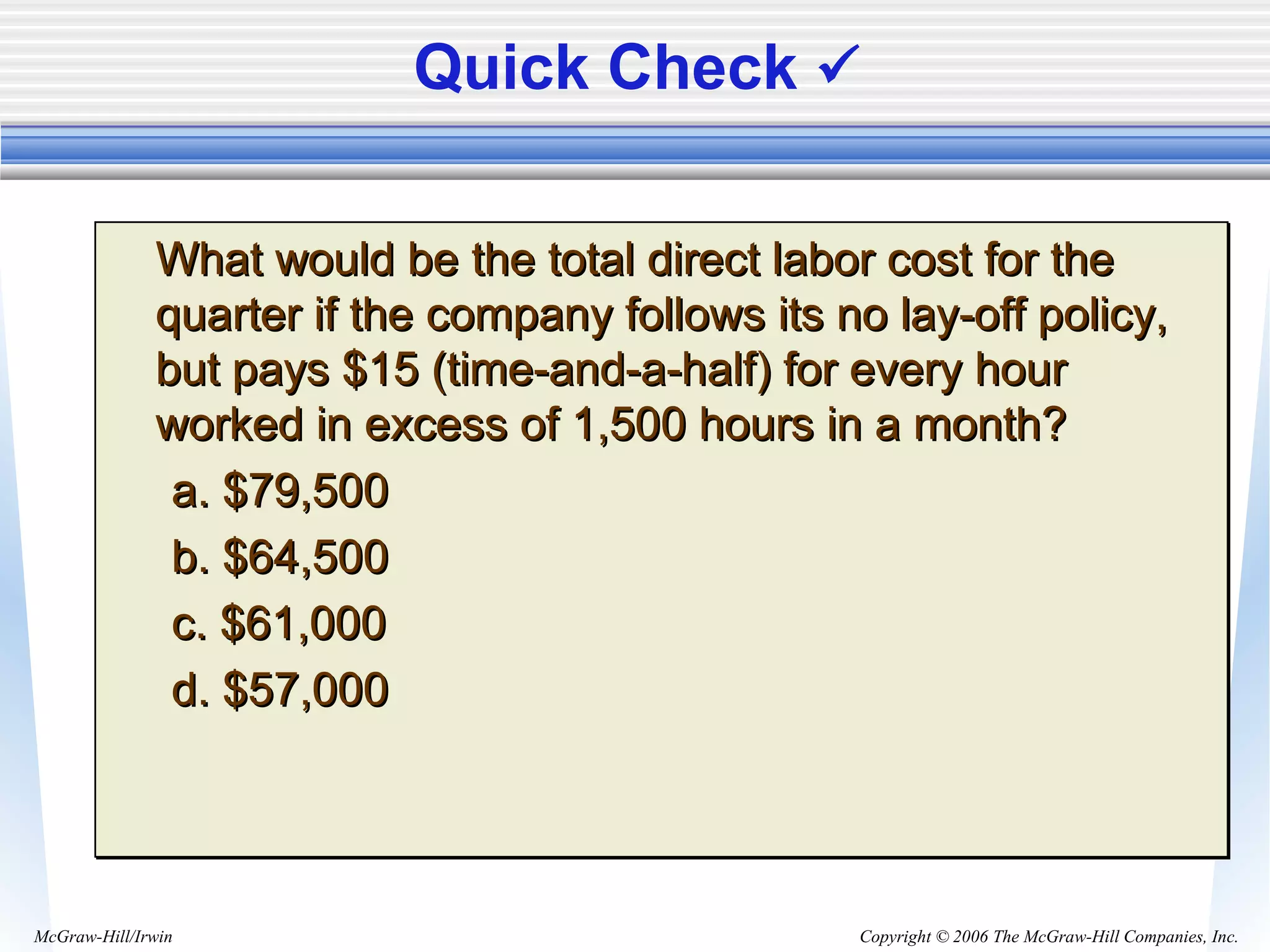

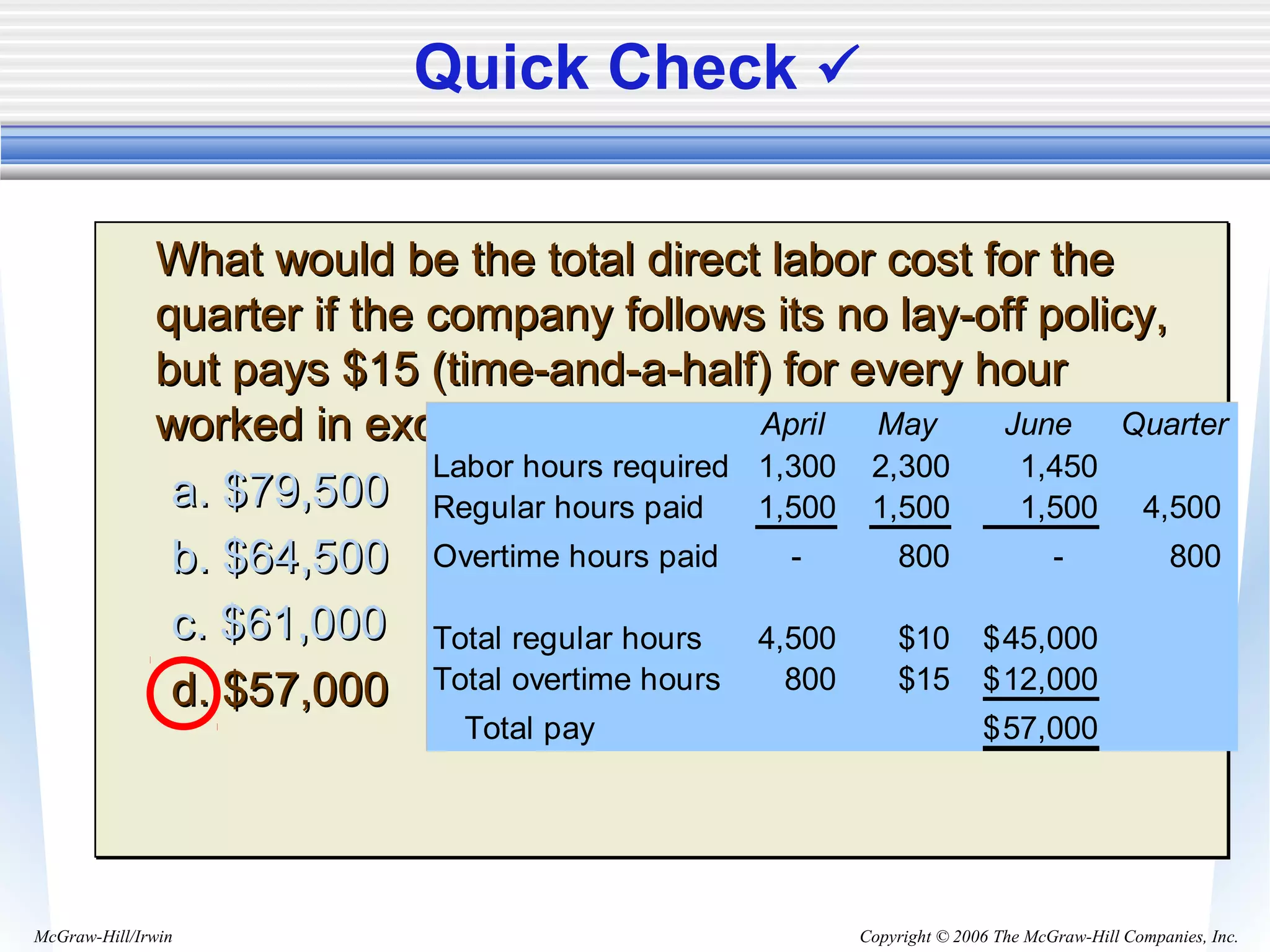

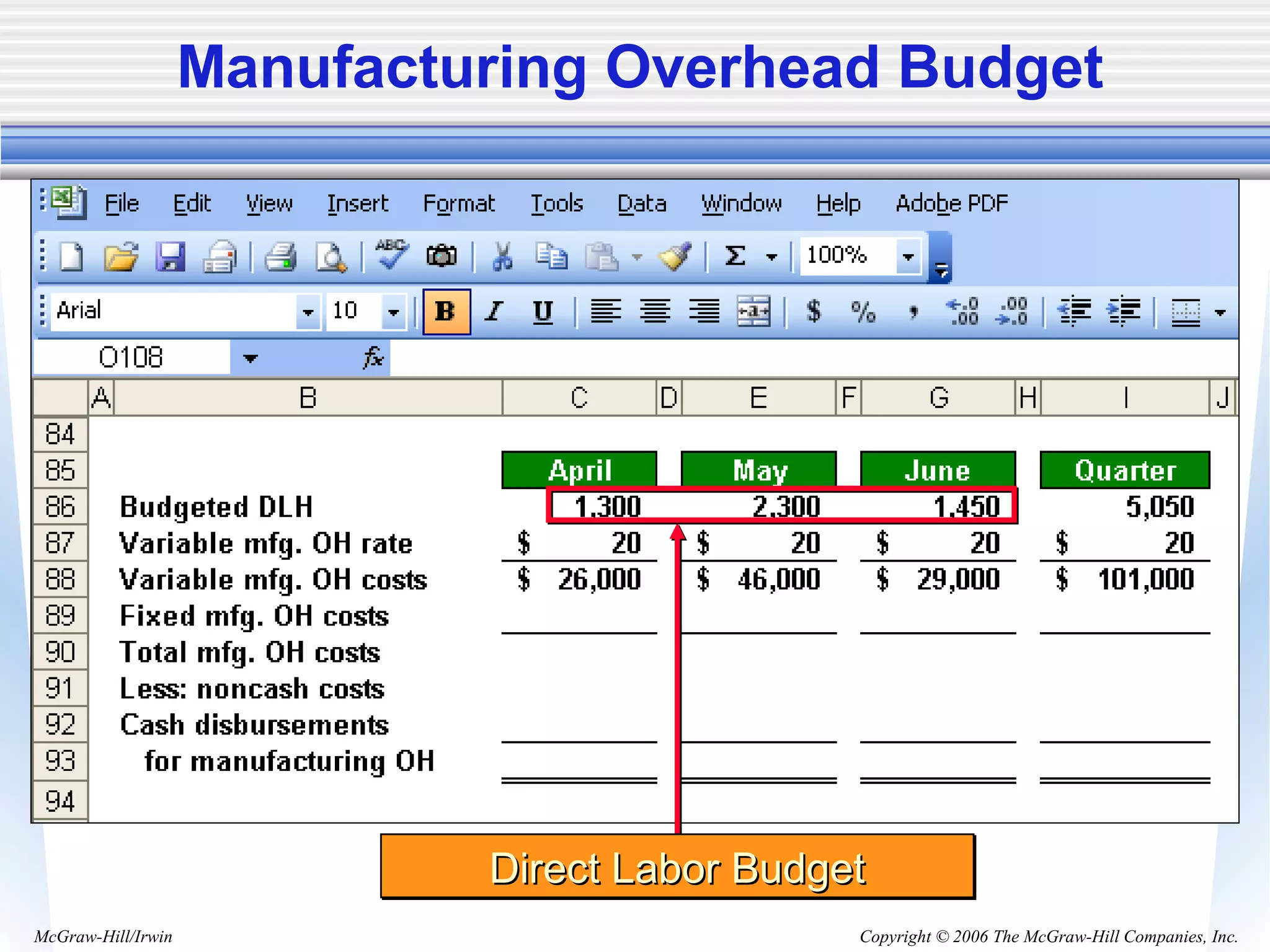

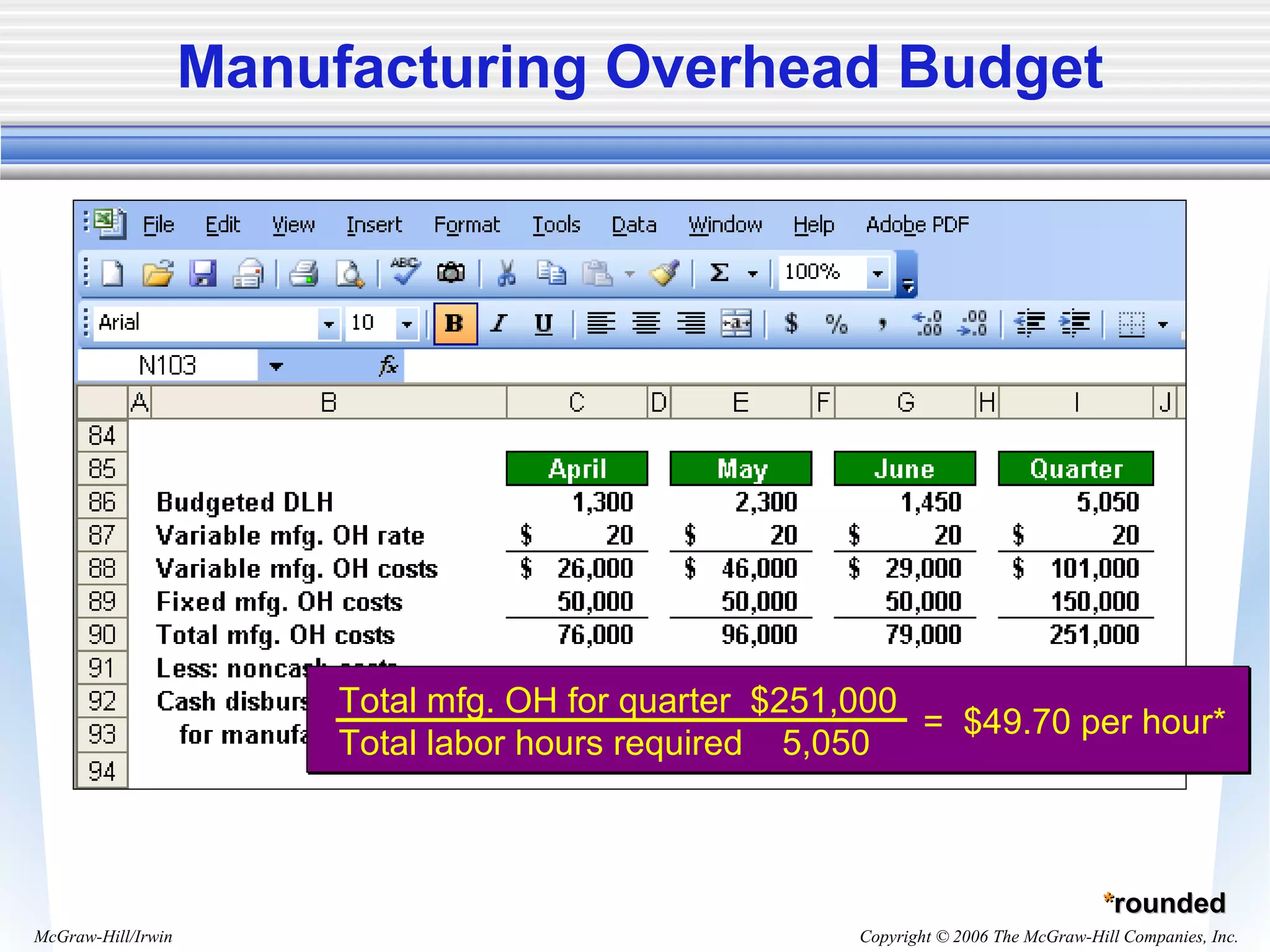

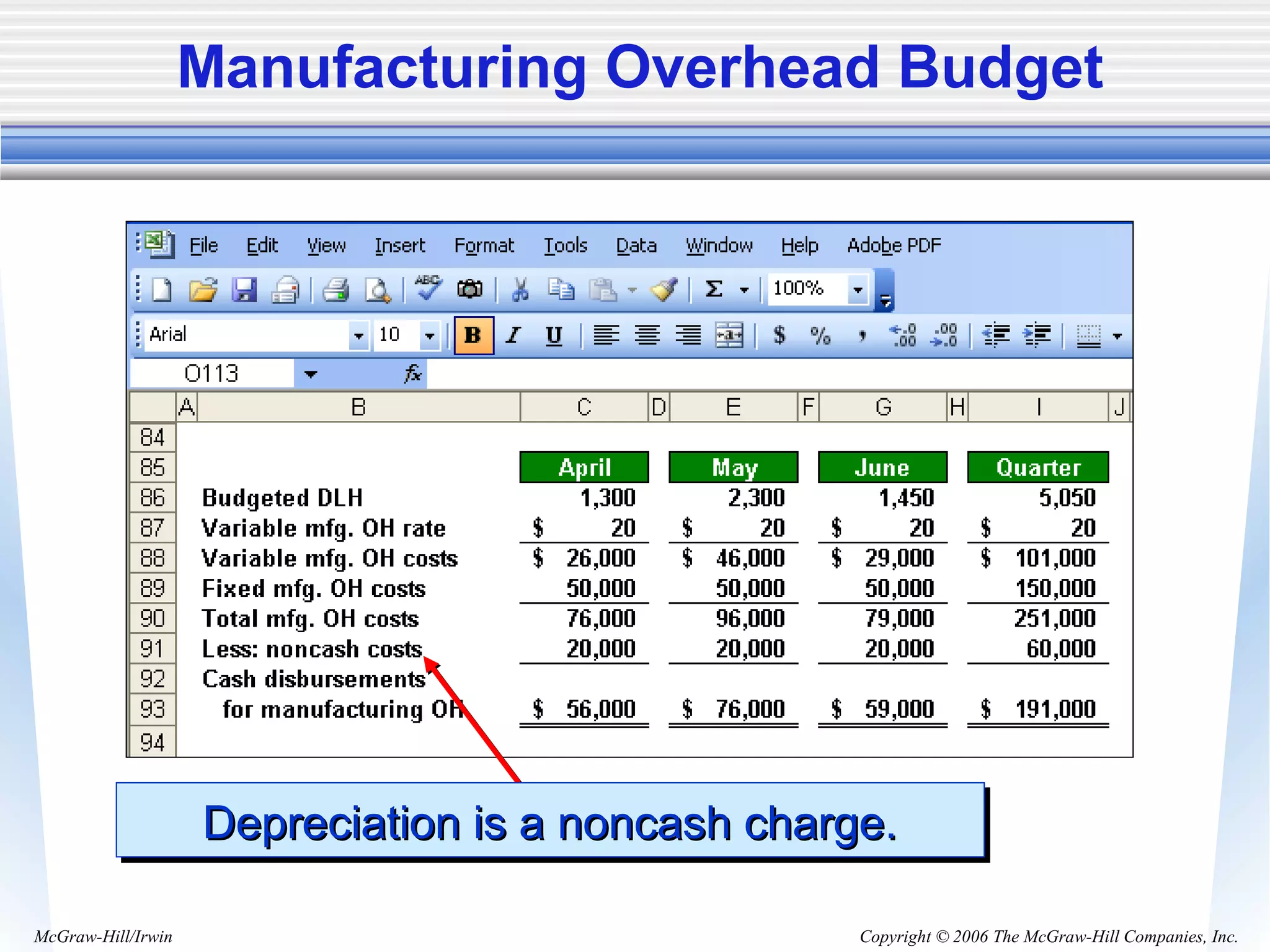

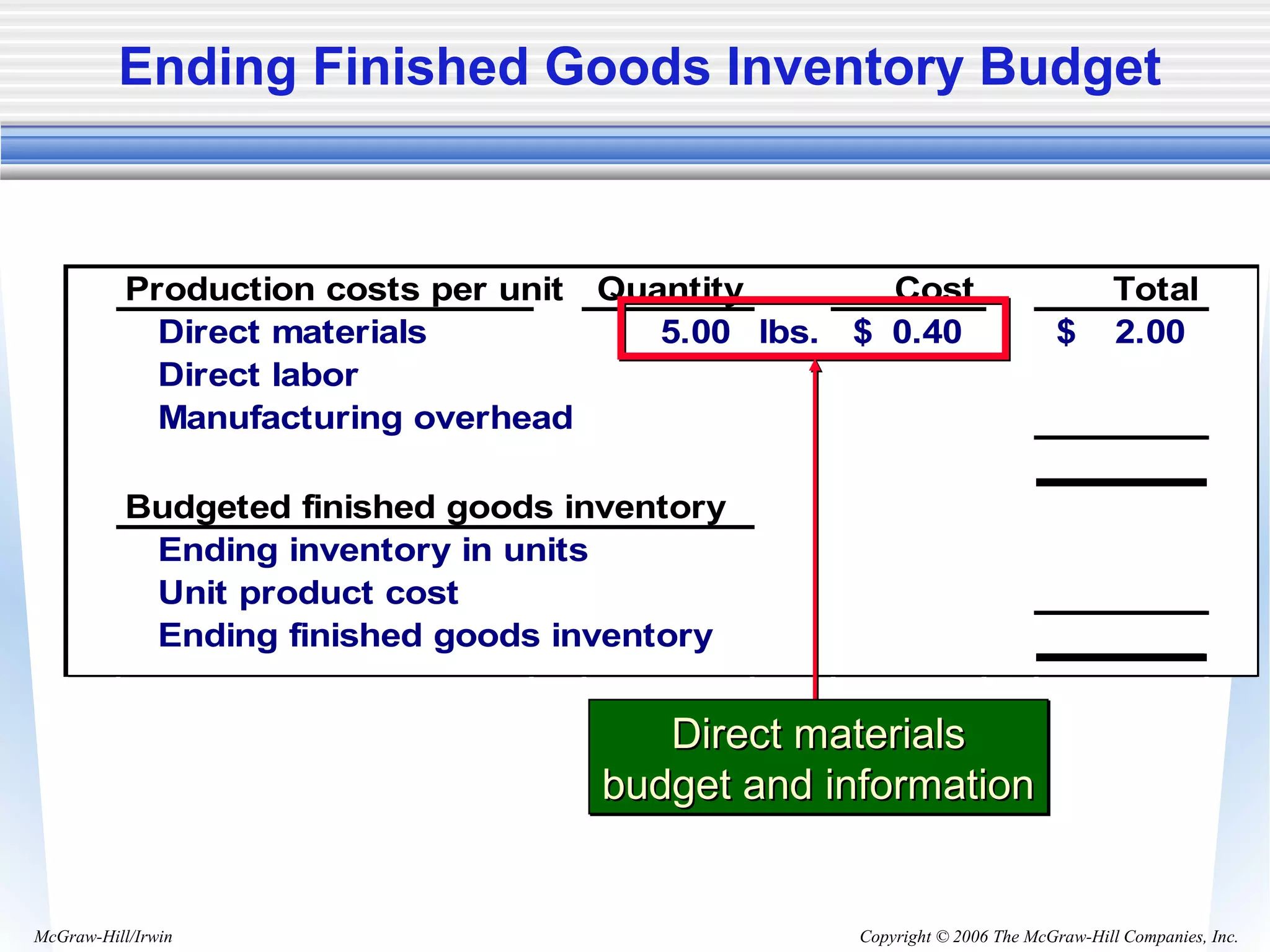

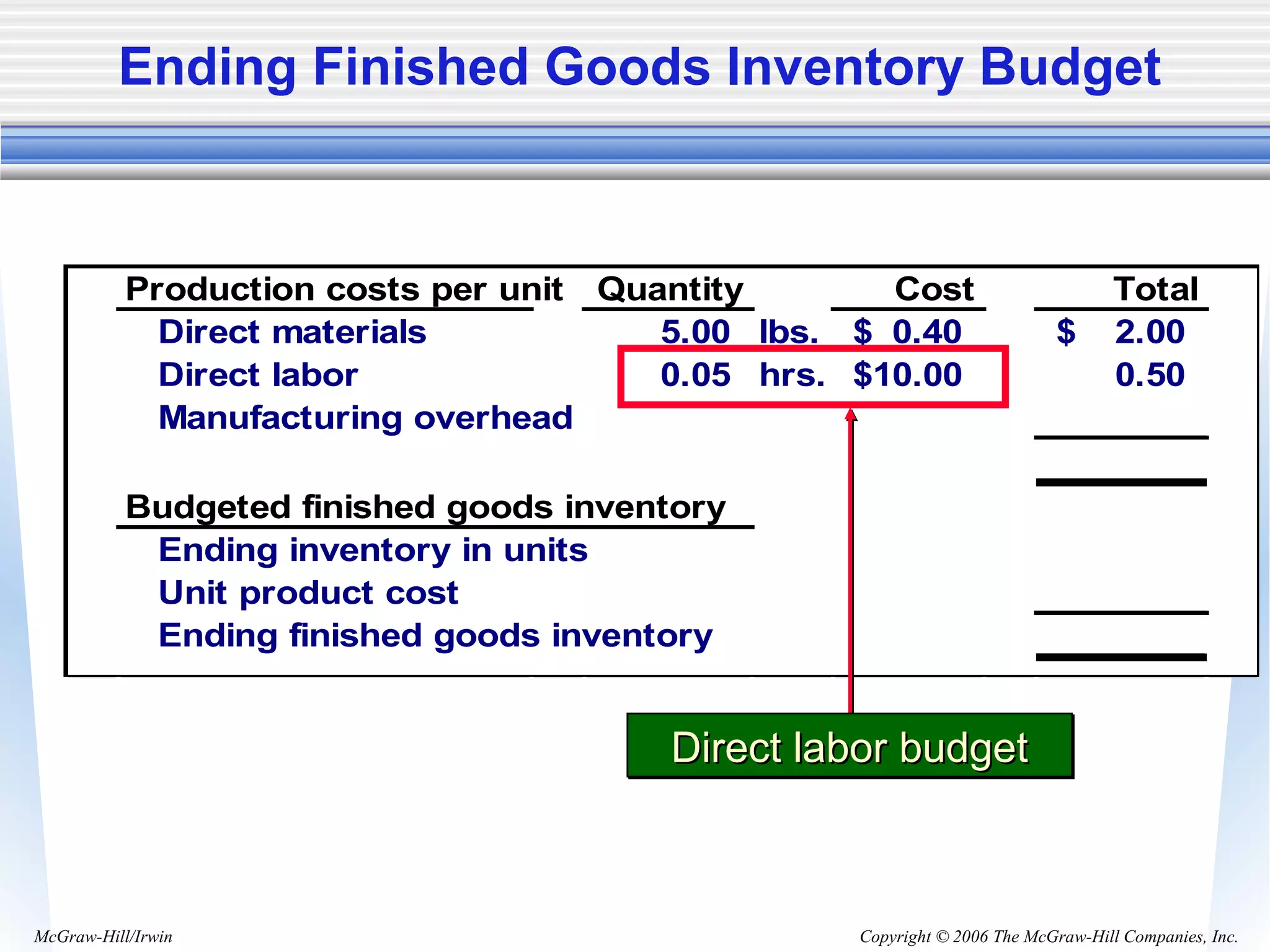

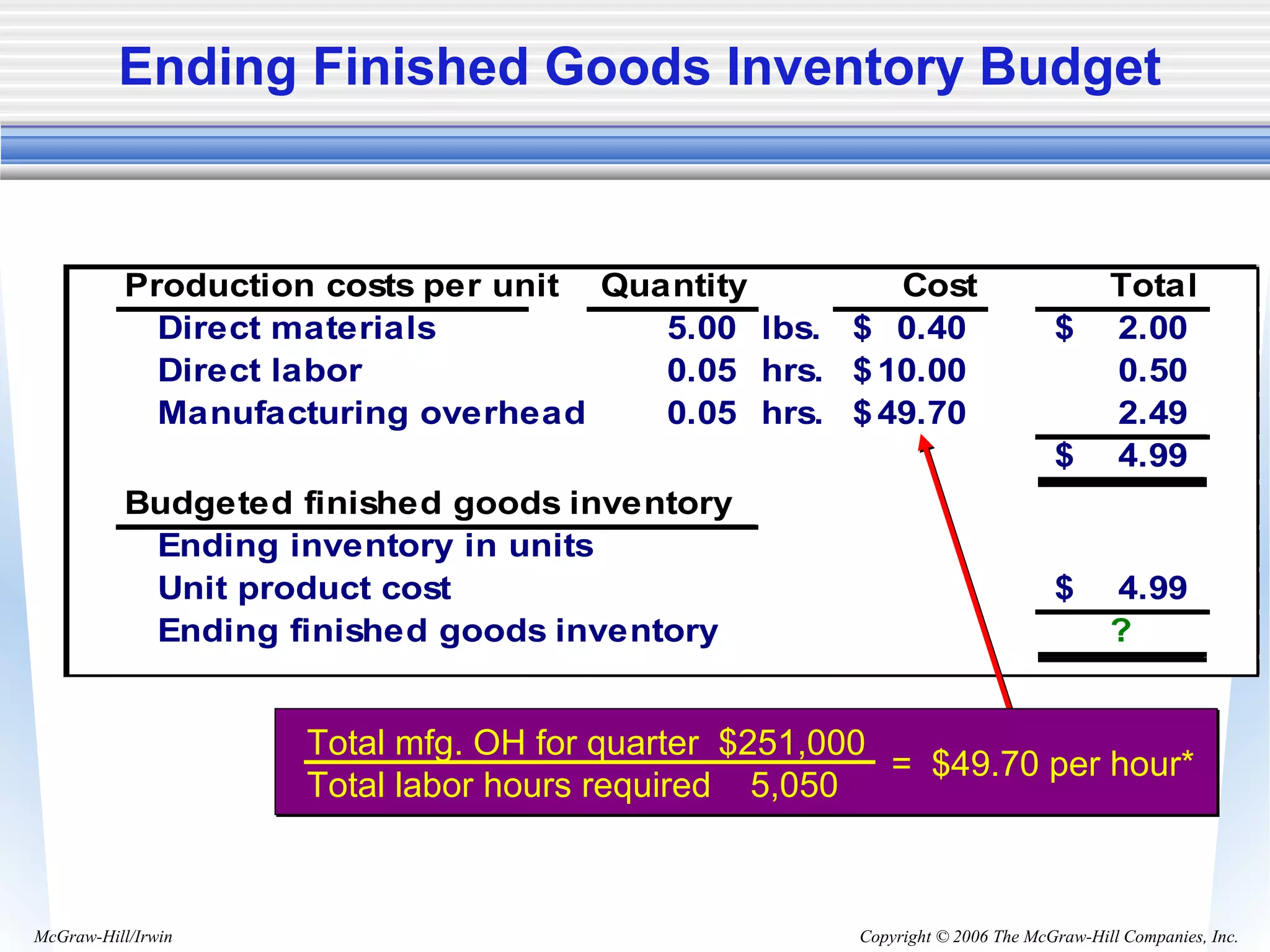

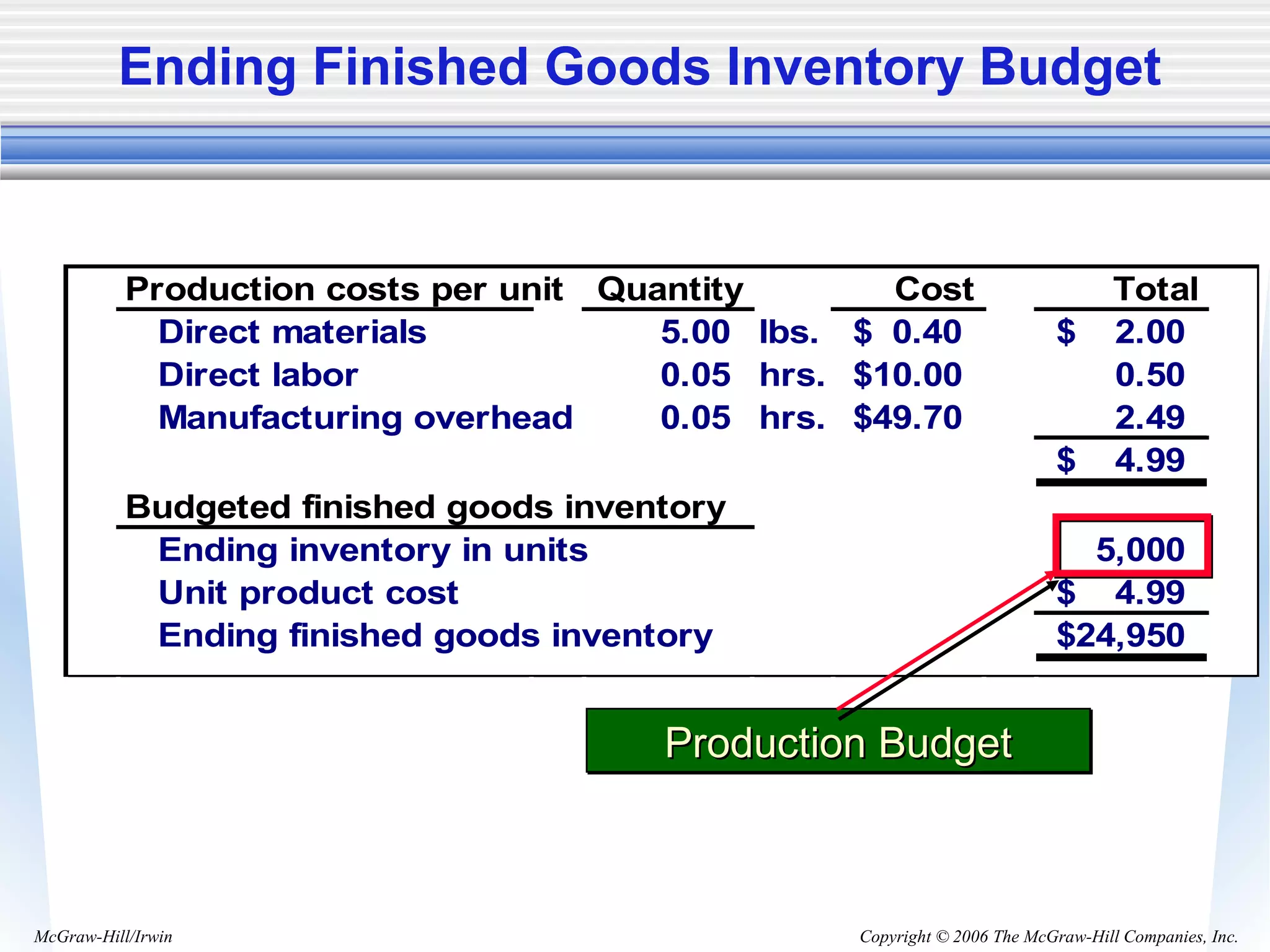

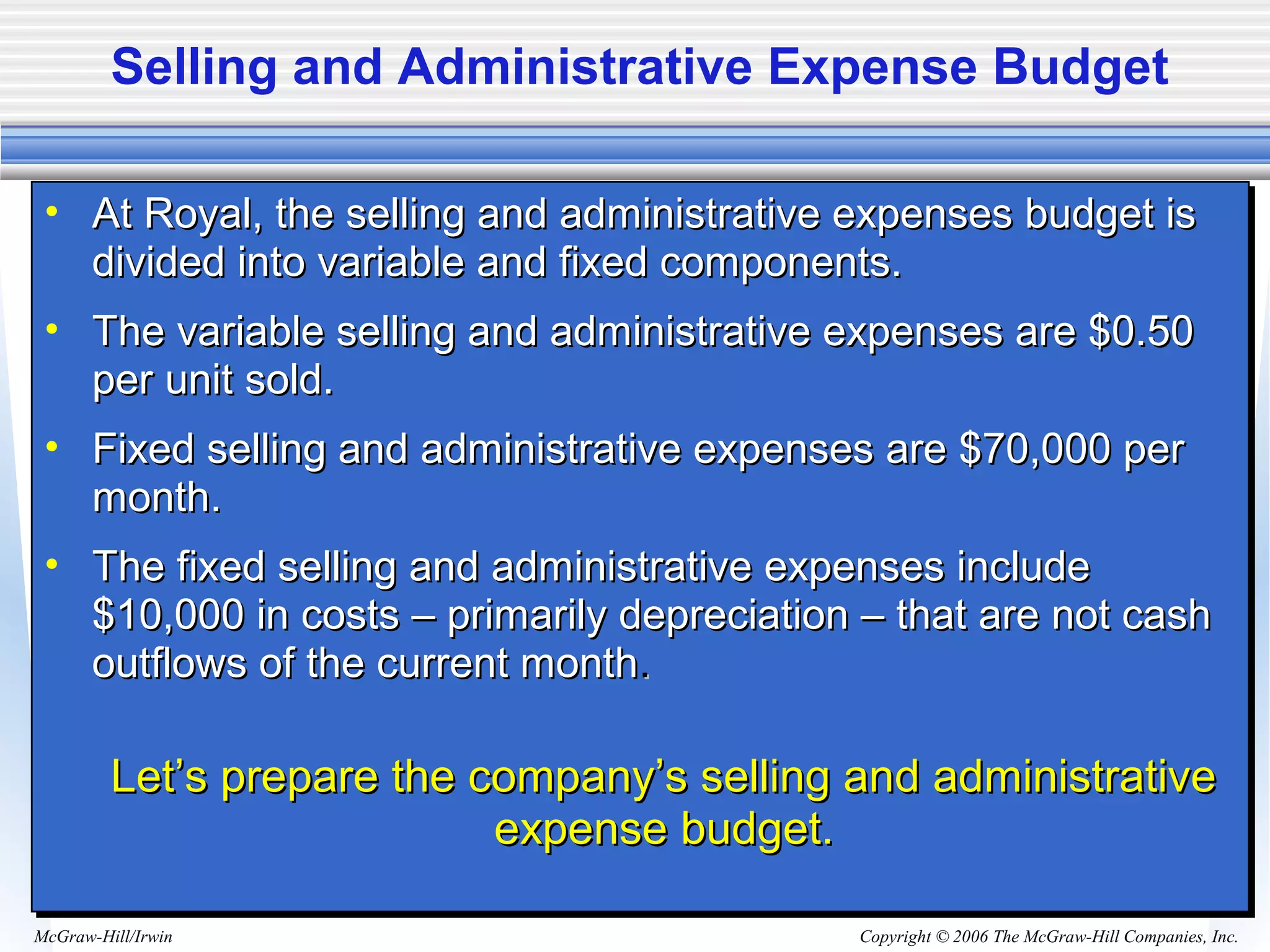

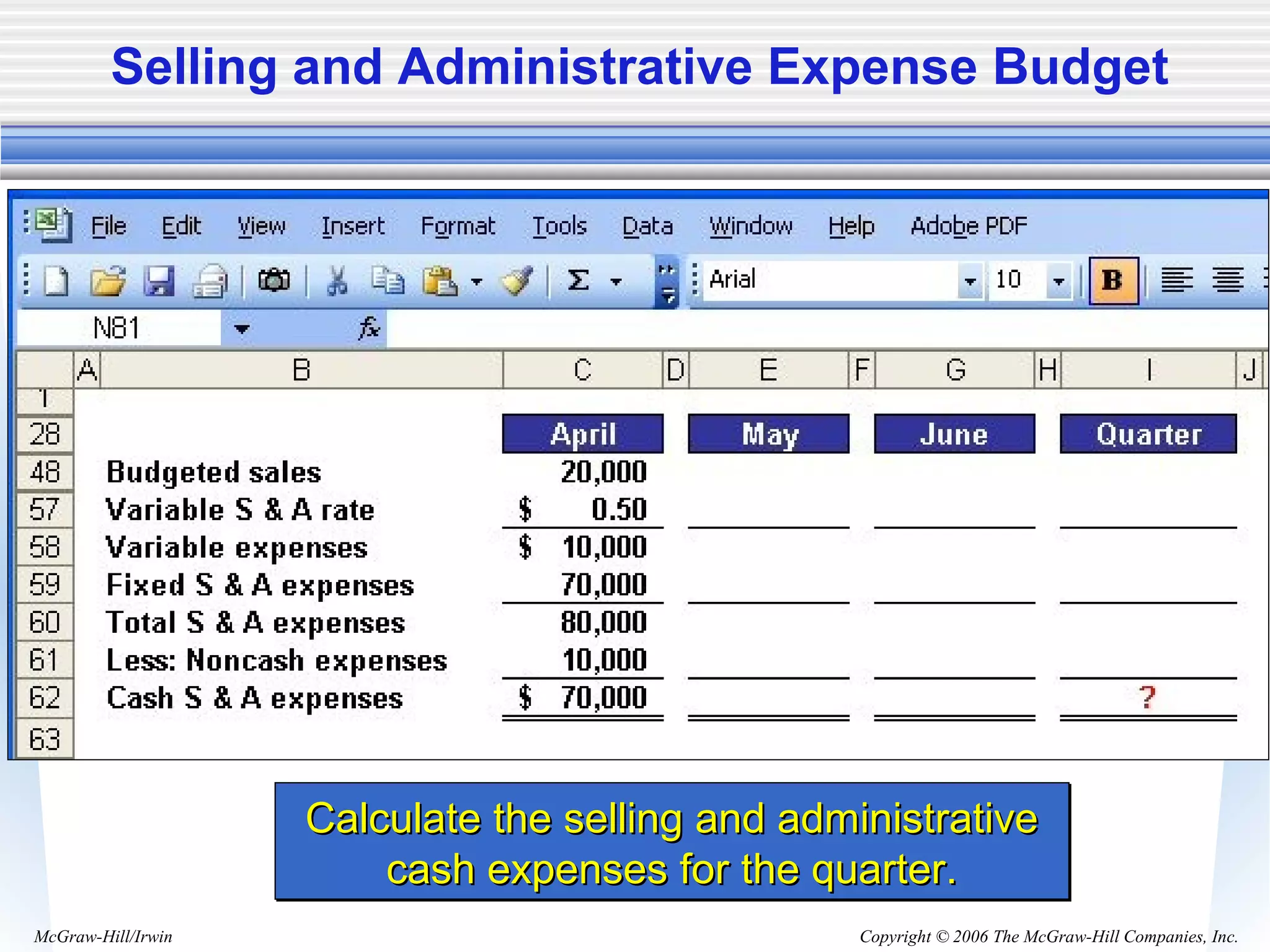

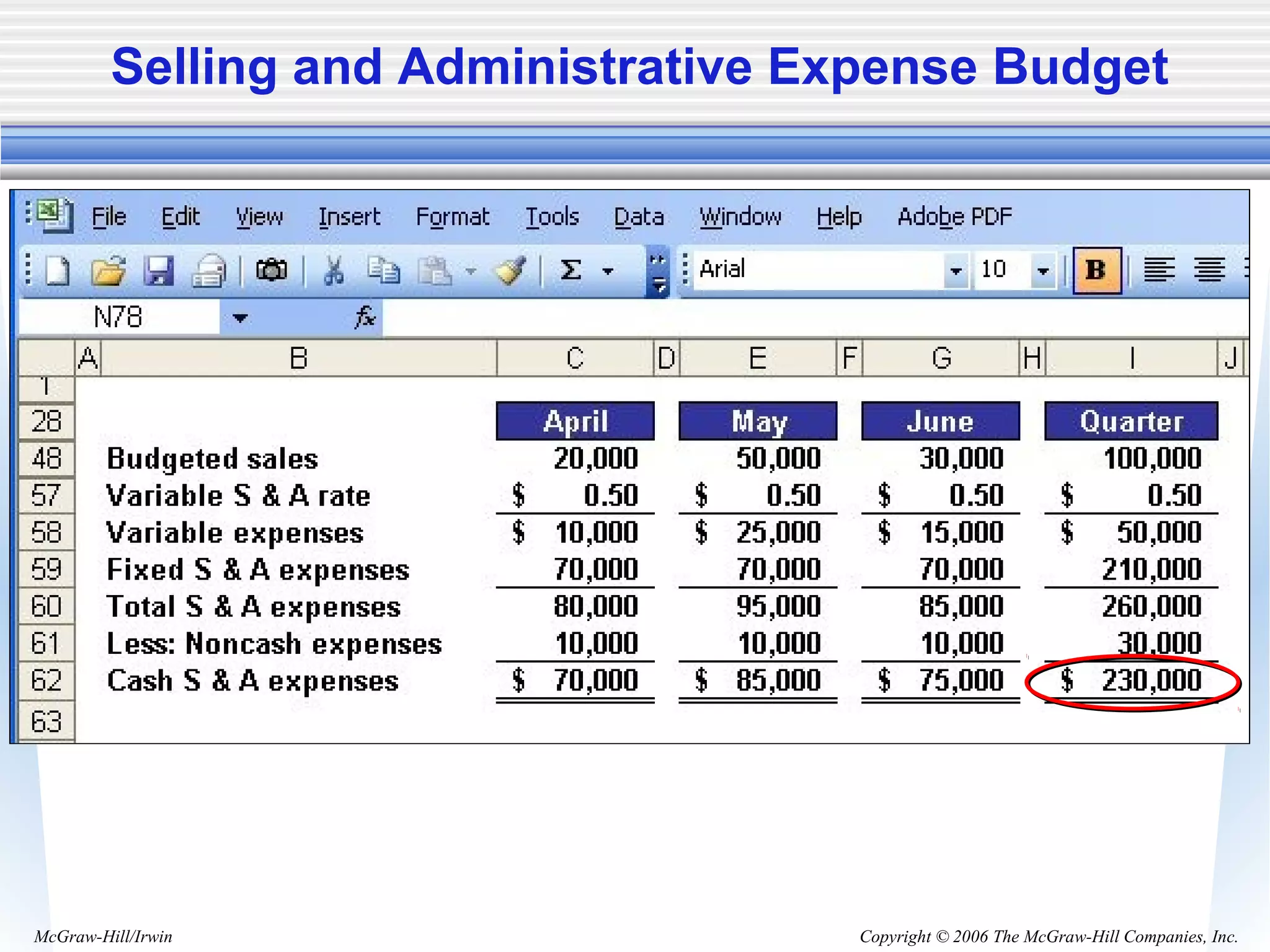

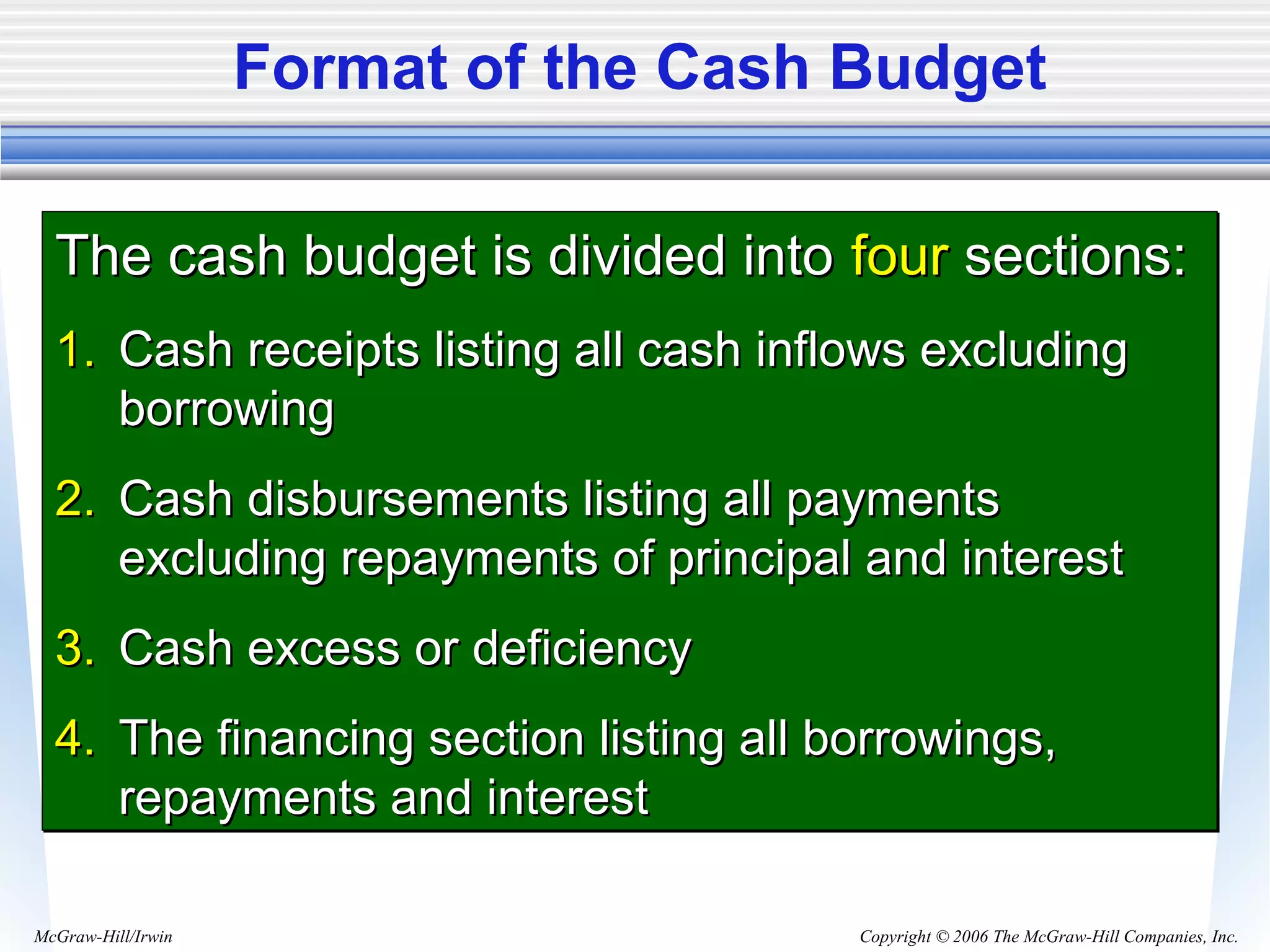

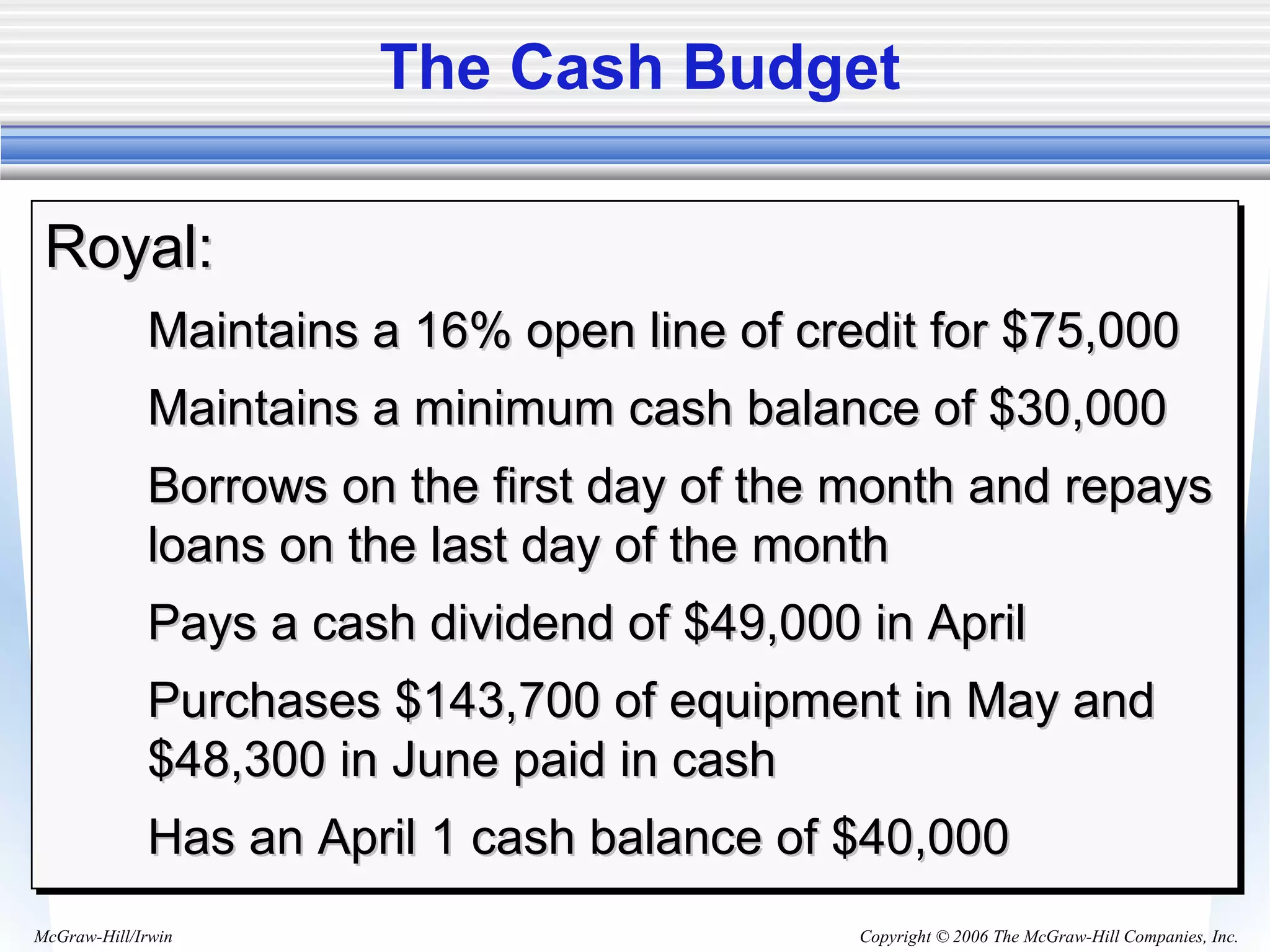

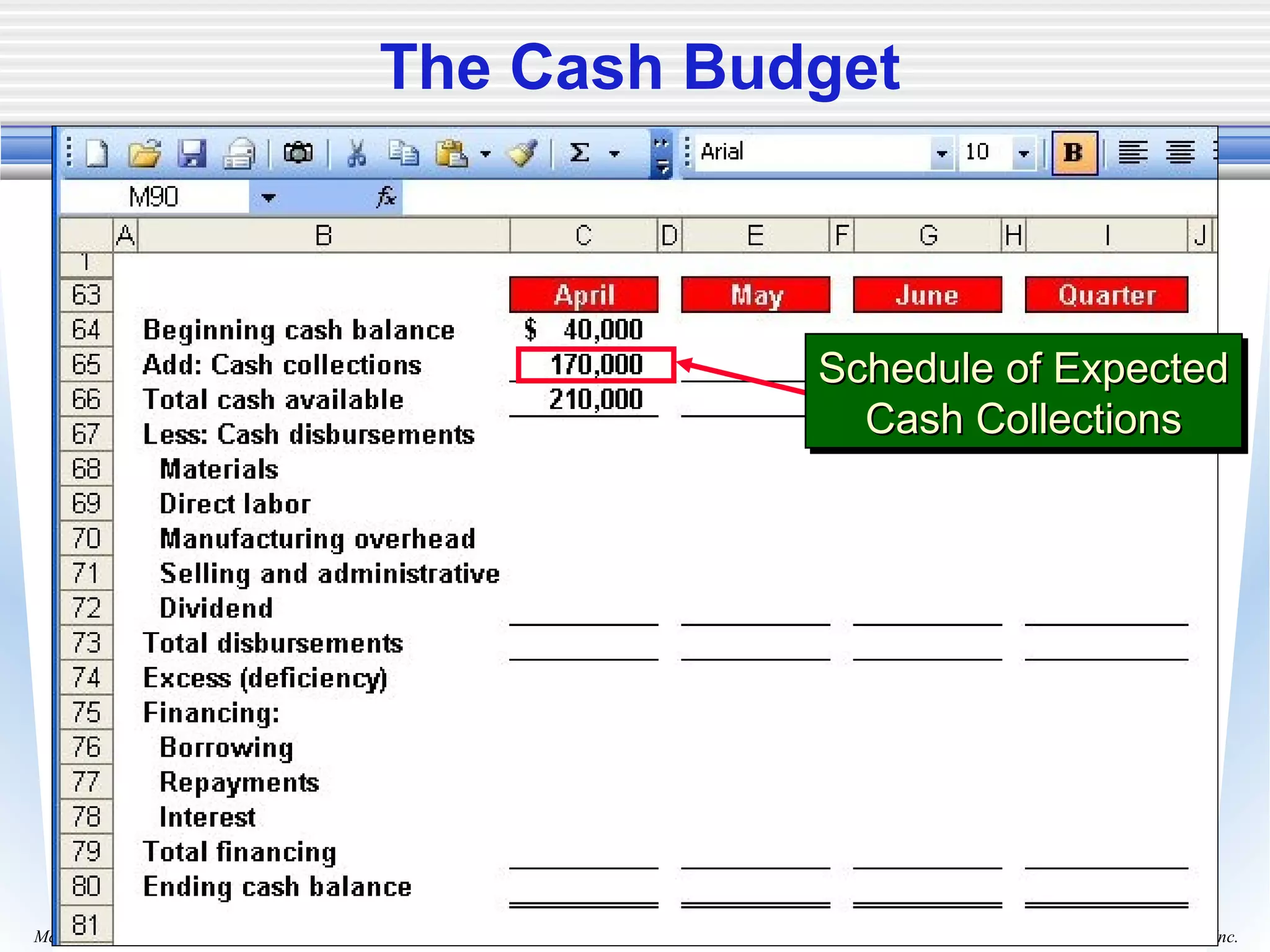

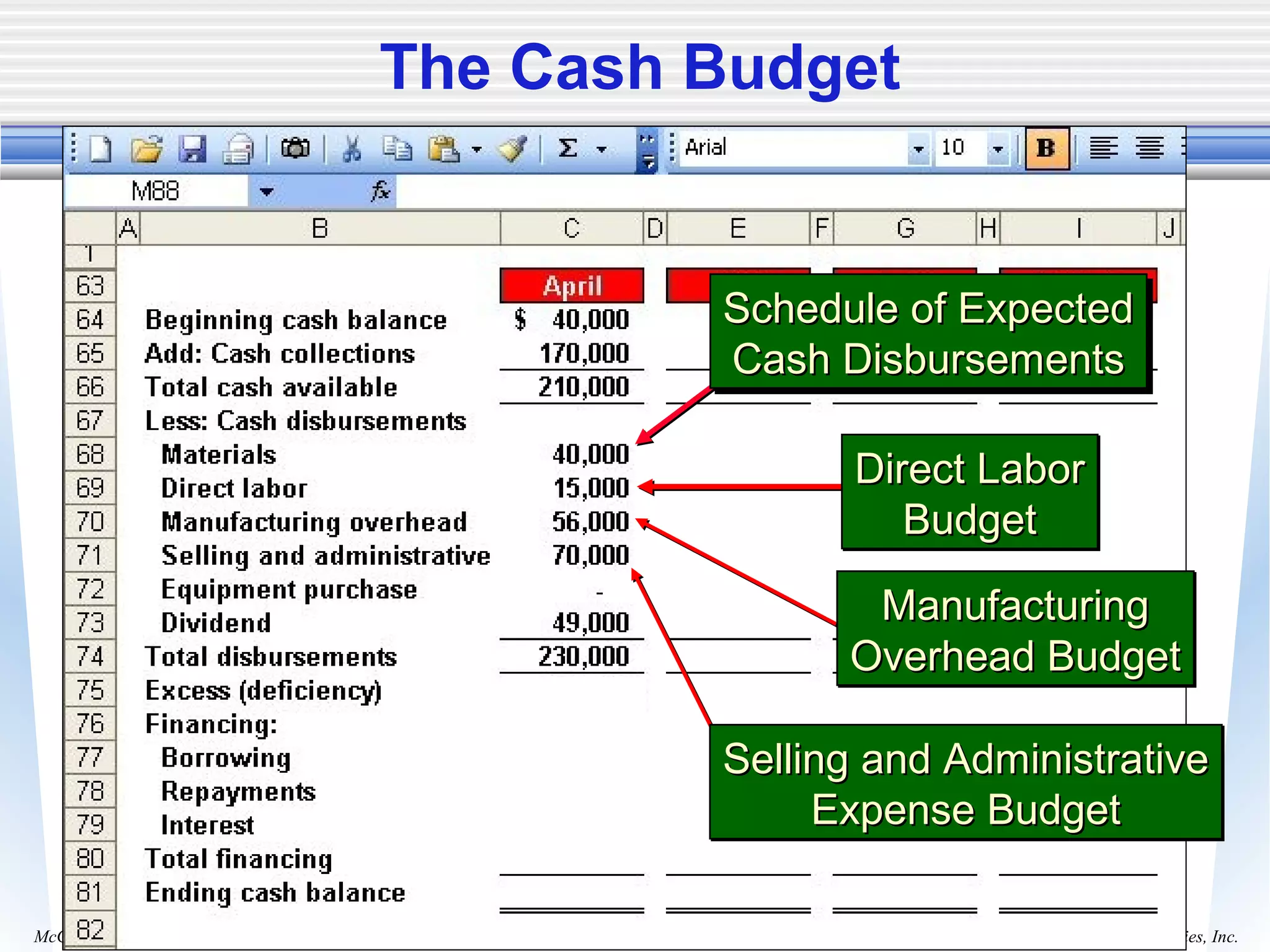

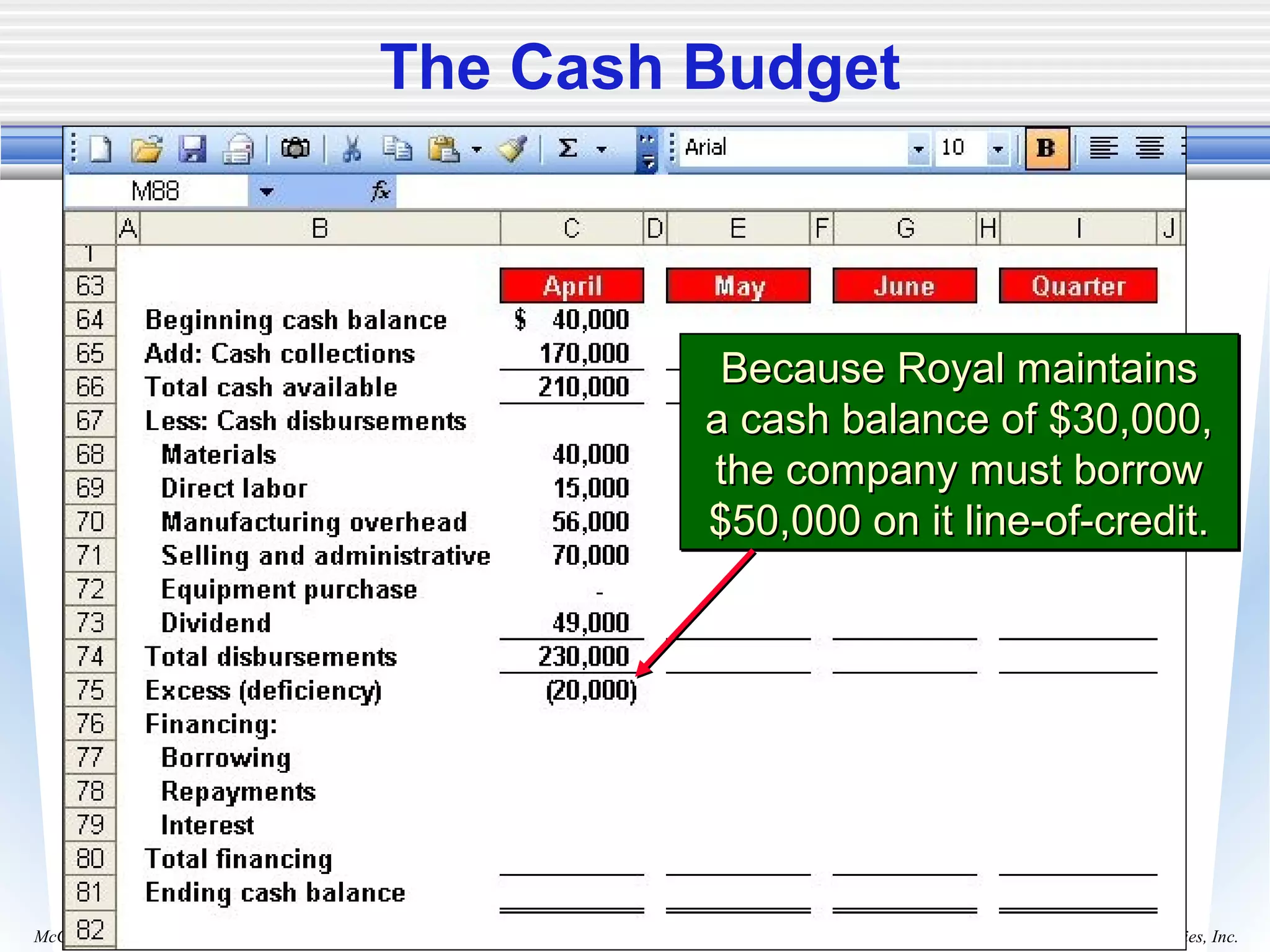

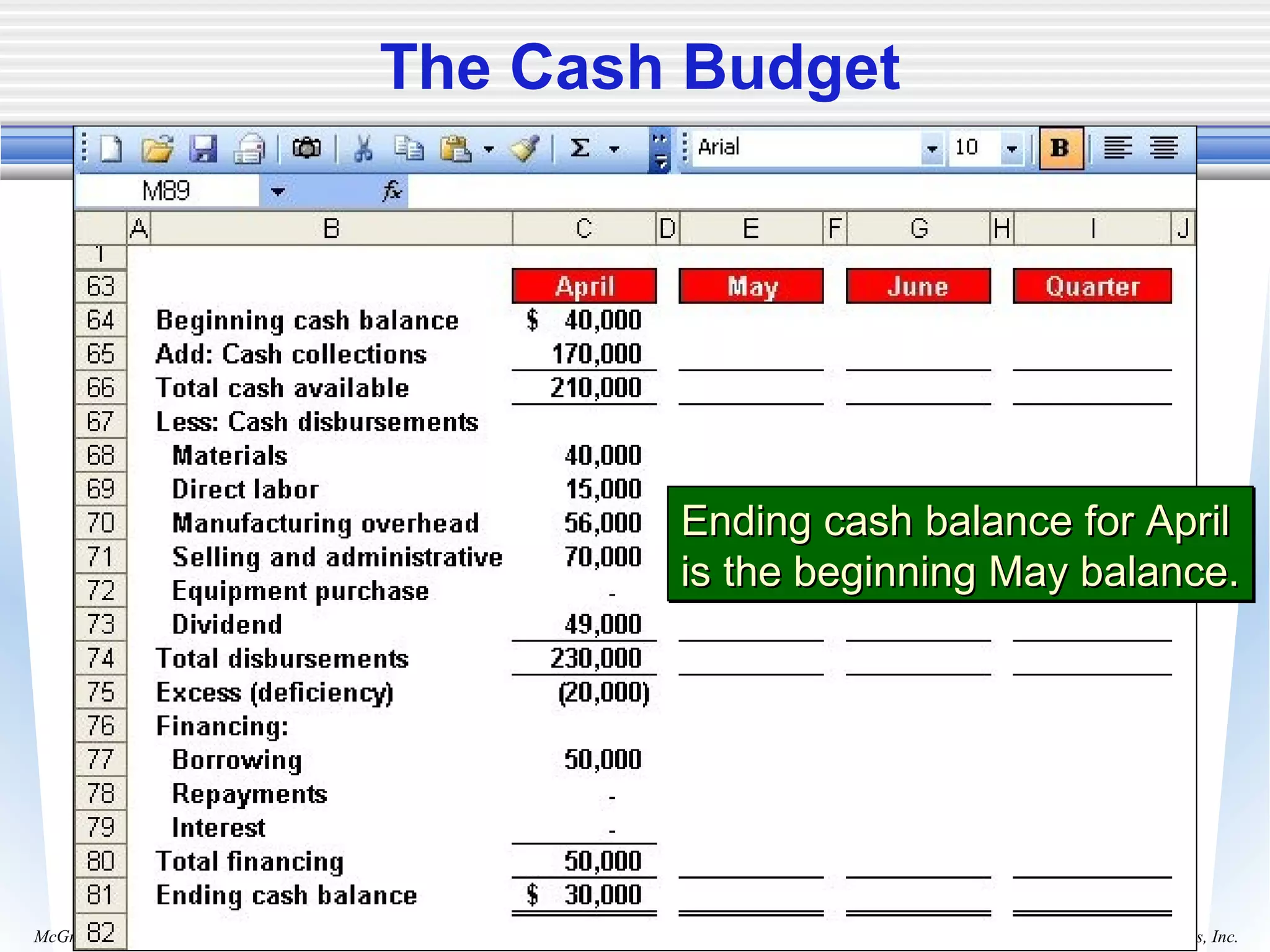

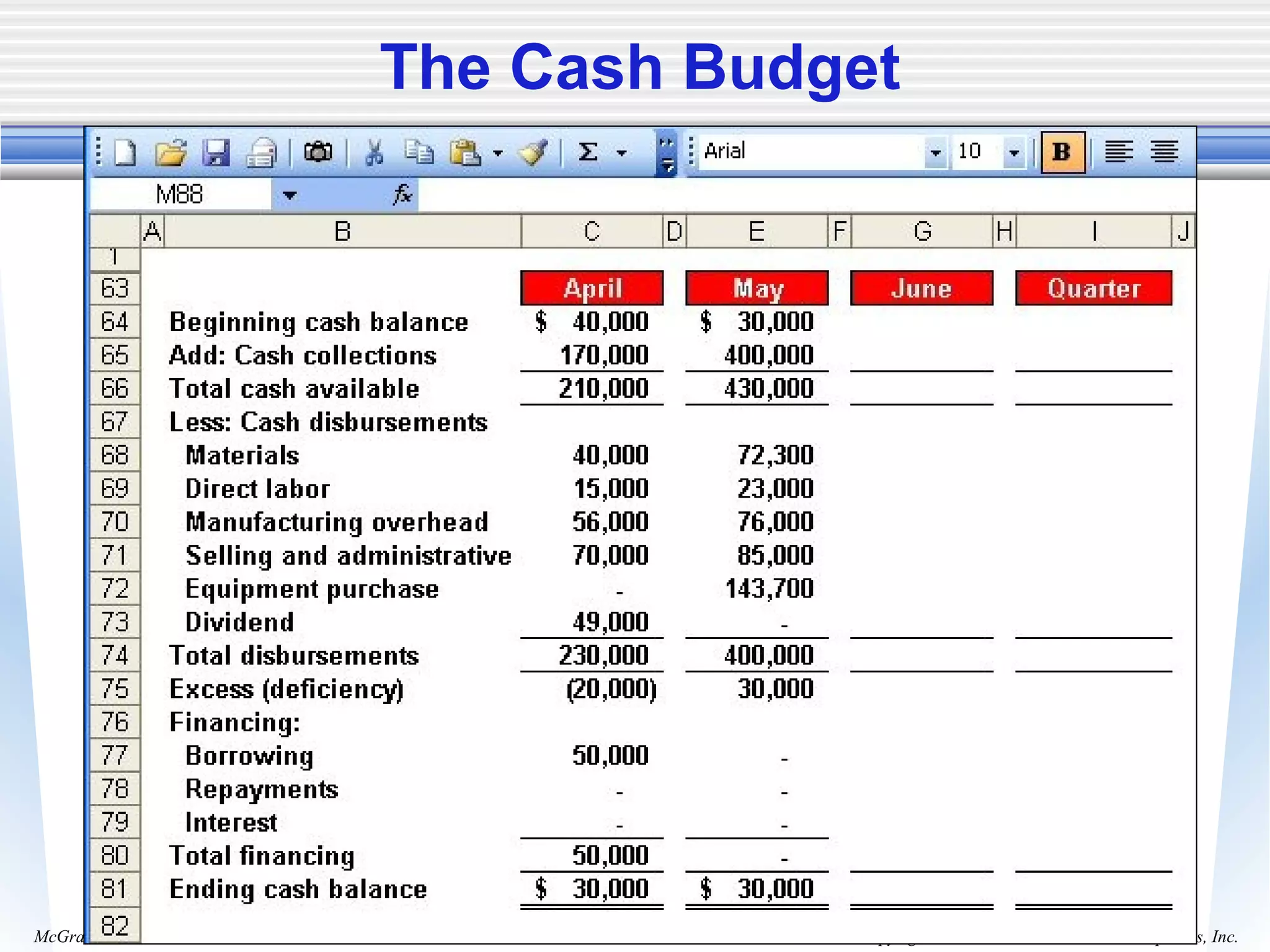

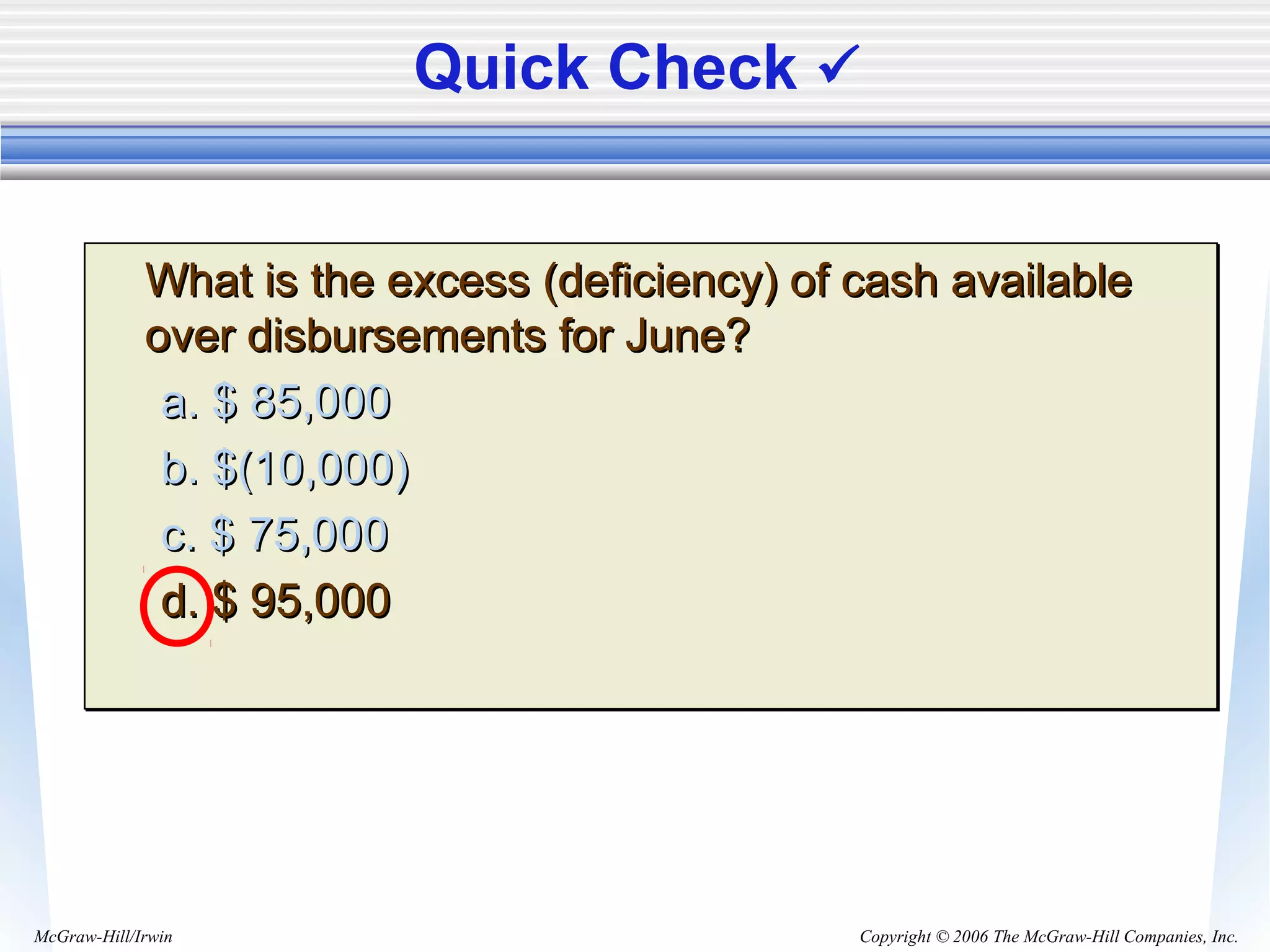

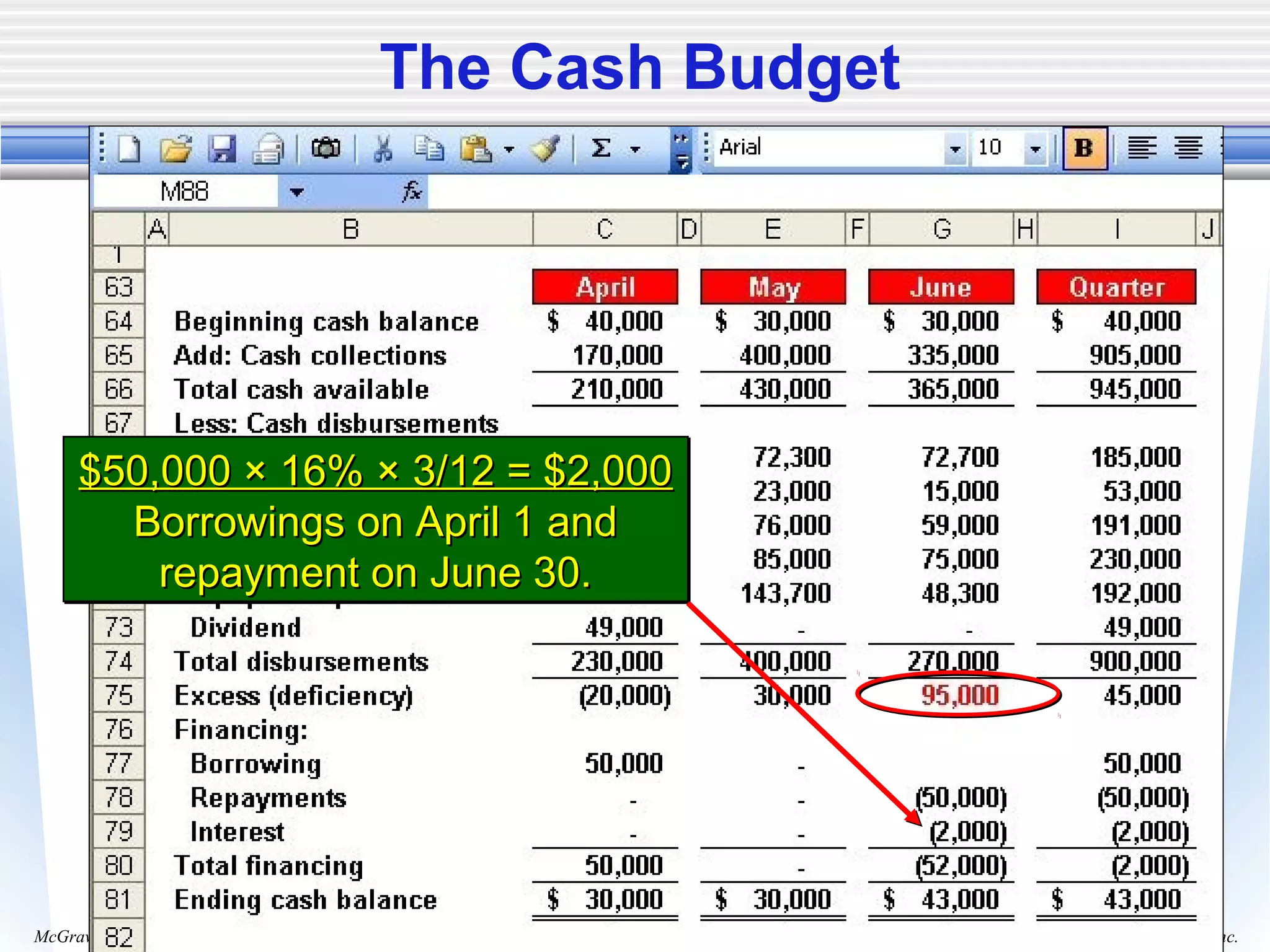

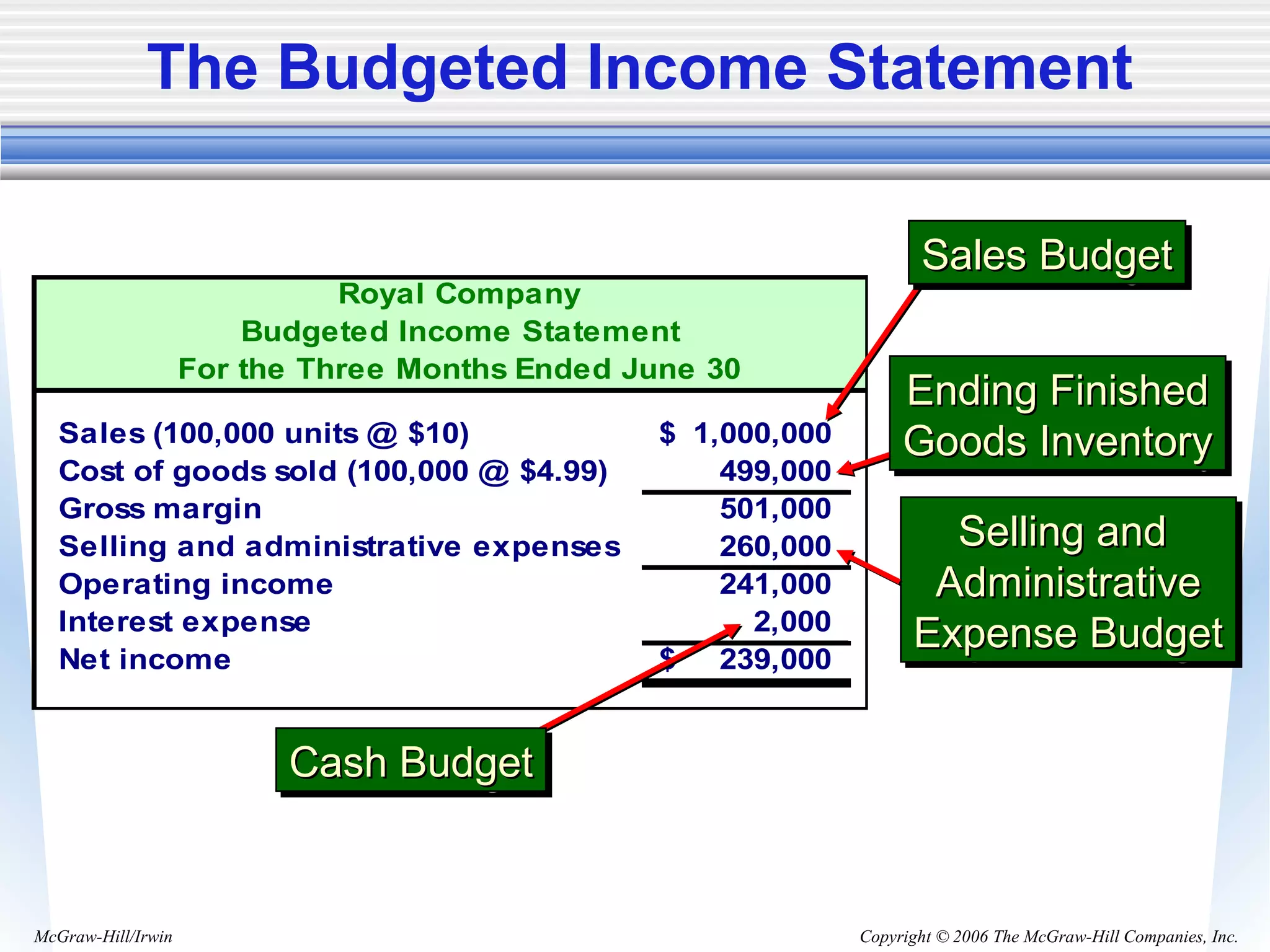

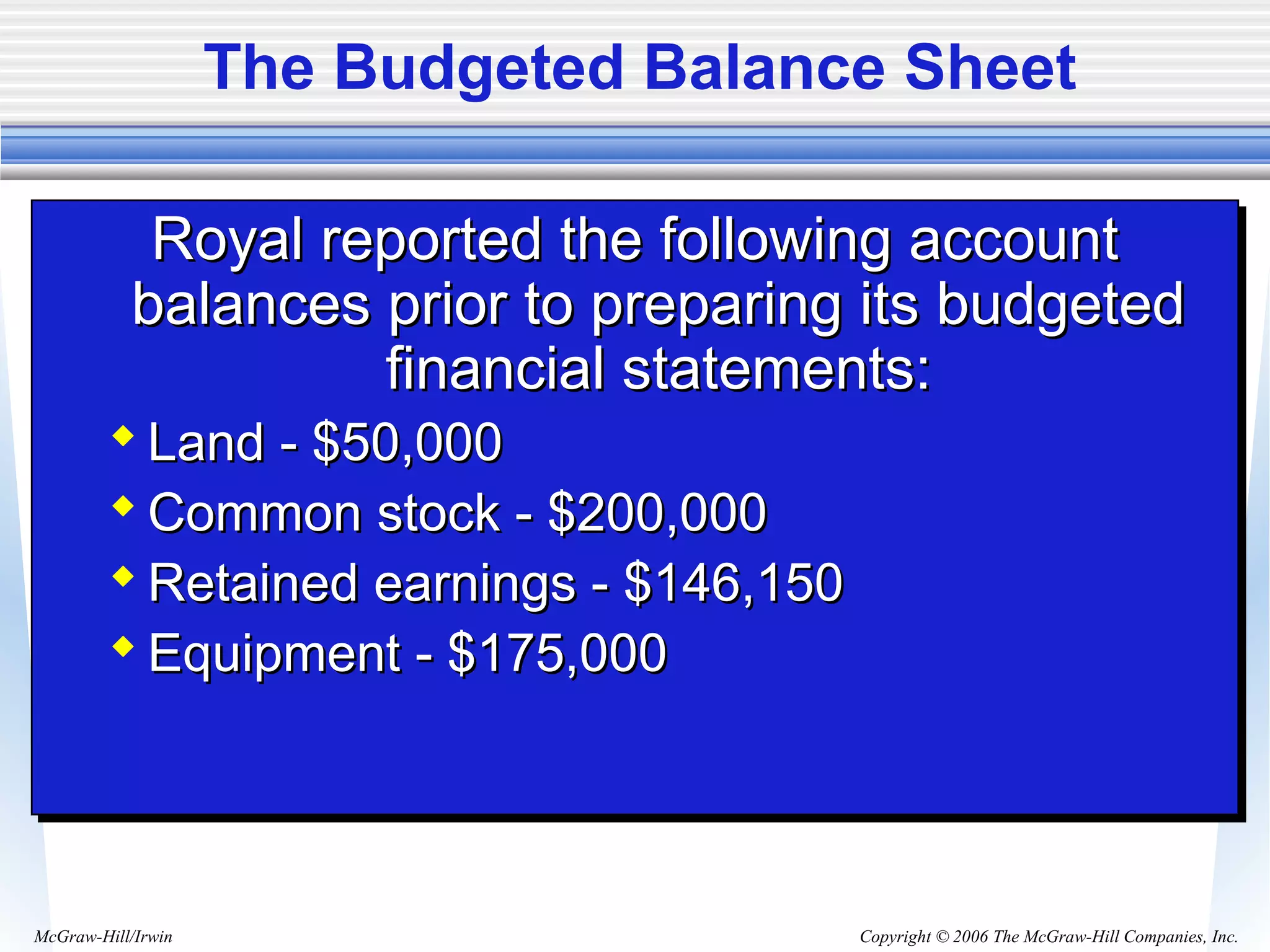

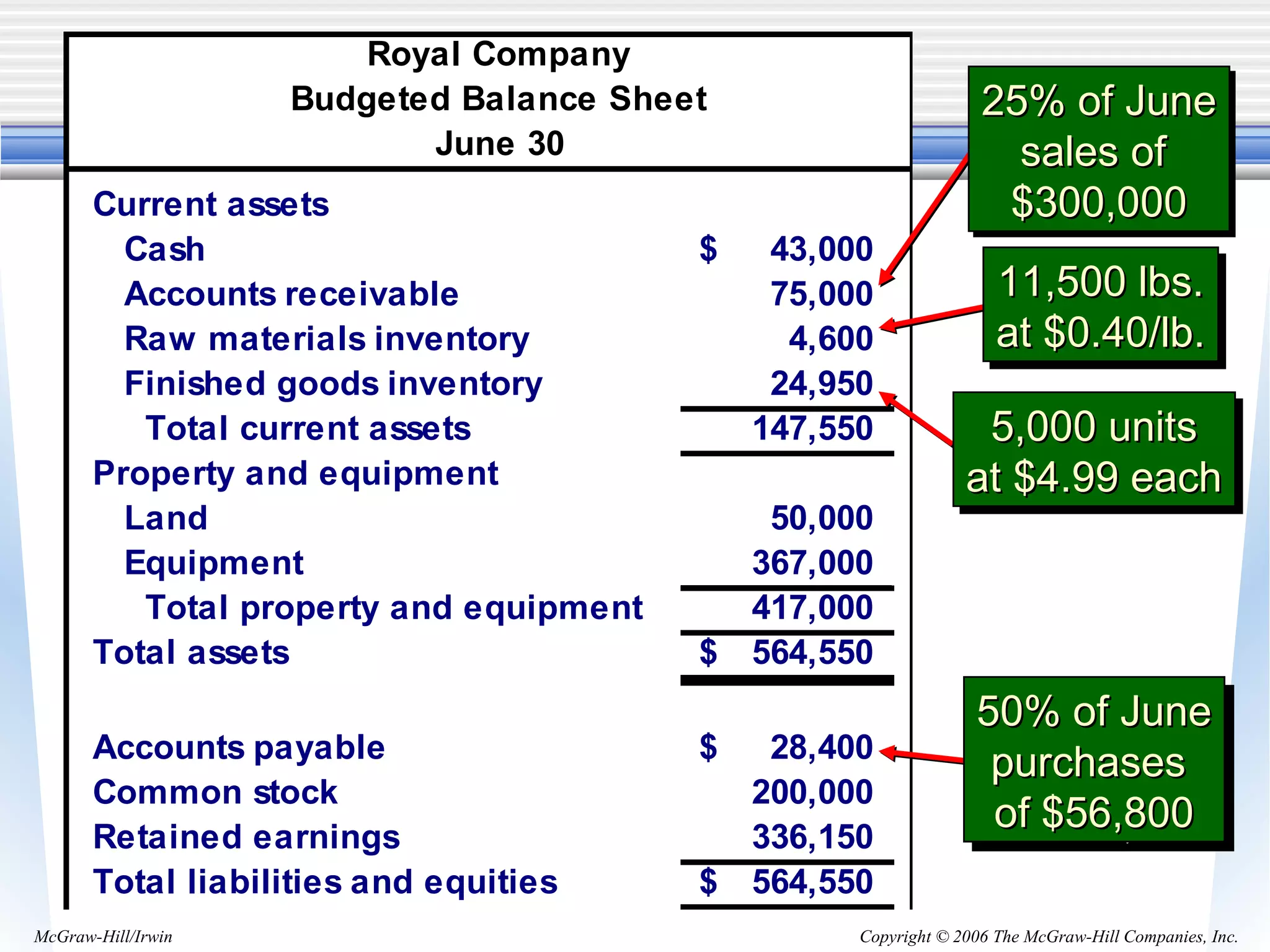

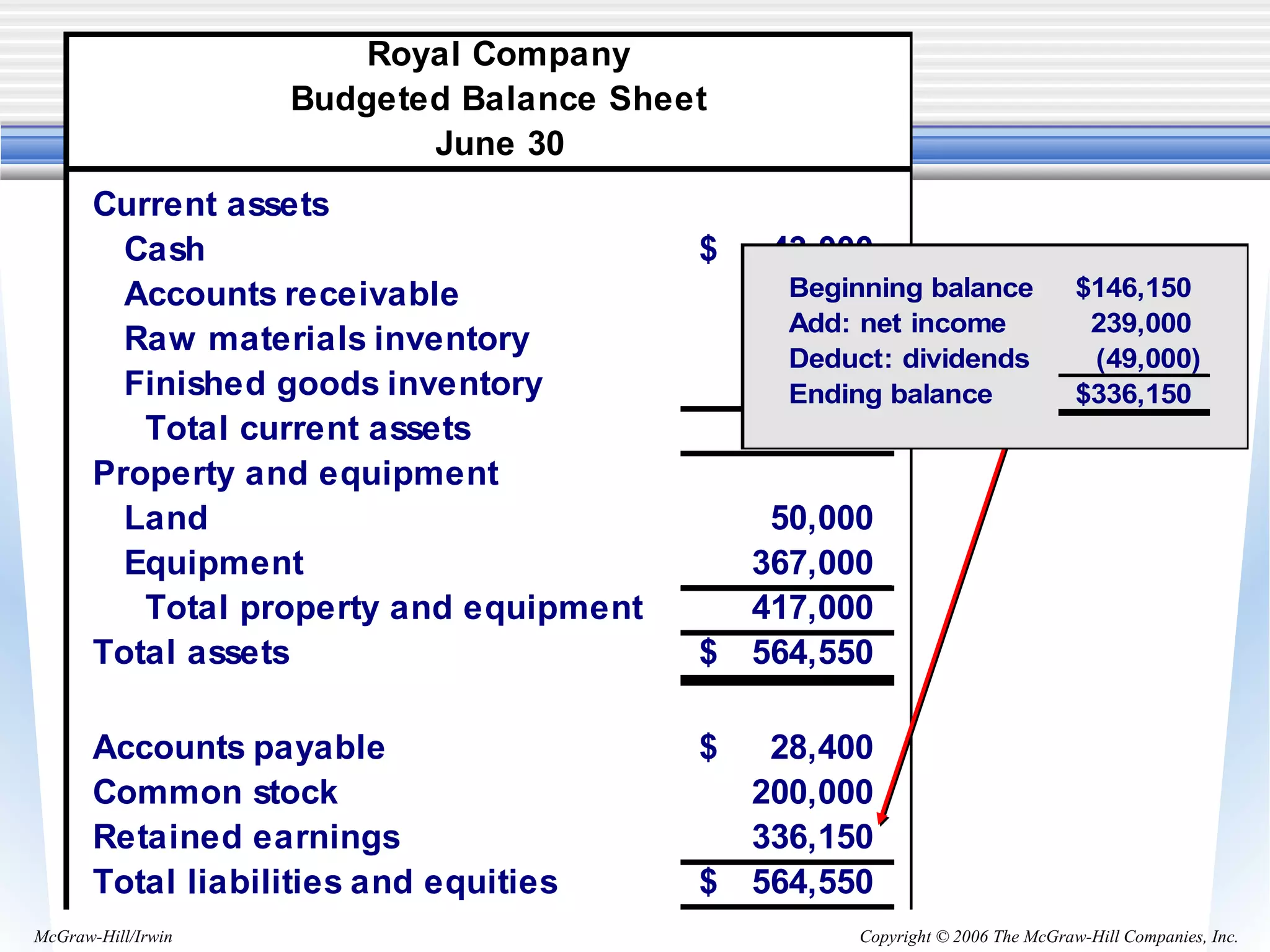

The document discusses various aspects of budgeting including the basic framework of budgeting, planning and control, advantages of budgeting, responsibility accounting, choosing budget periods, self-imposed budgets, human factors in budgeting, zero-based budgeting, the budget committee, an overview of the master budget, and provides an example of a company preparing budgets for sales, cash collections, and production for a quarter. Budgeting involves quantitative planning to achieve objectives, while control ensures the objectives are attained. Budgets are used by companies to coordinate activities, allocate resources, and communicate plans.