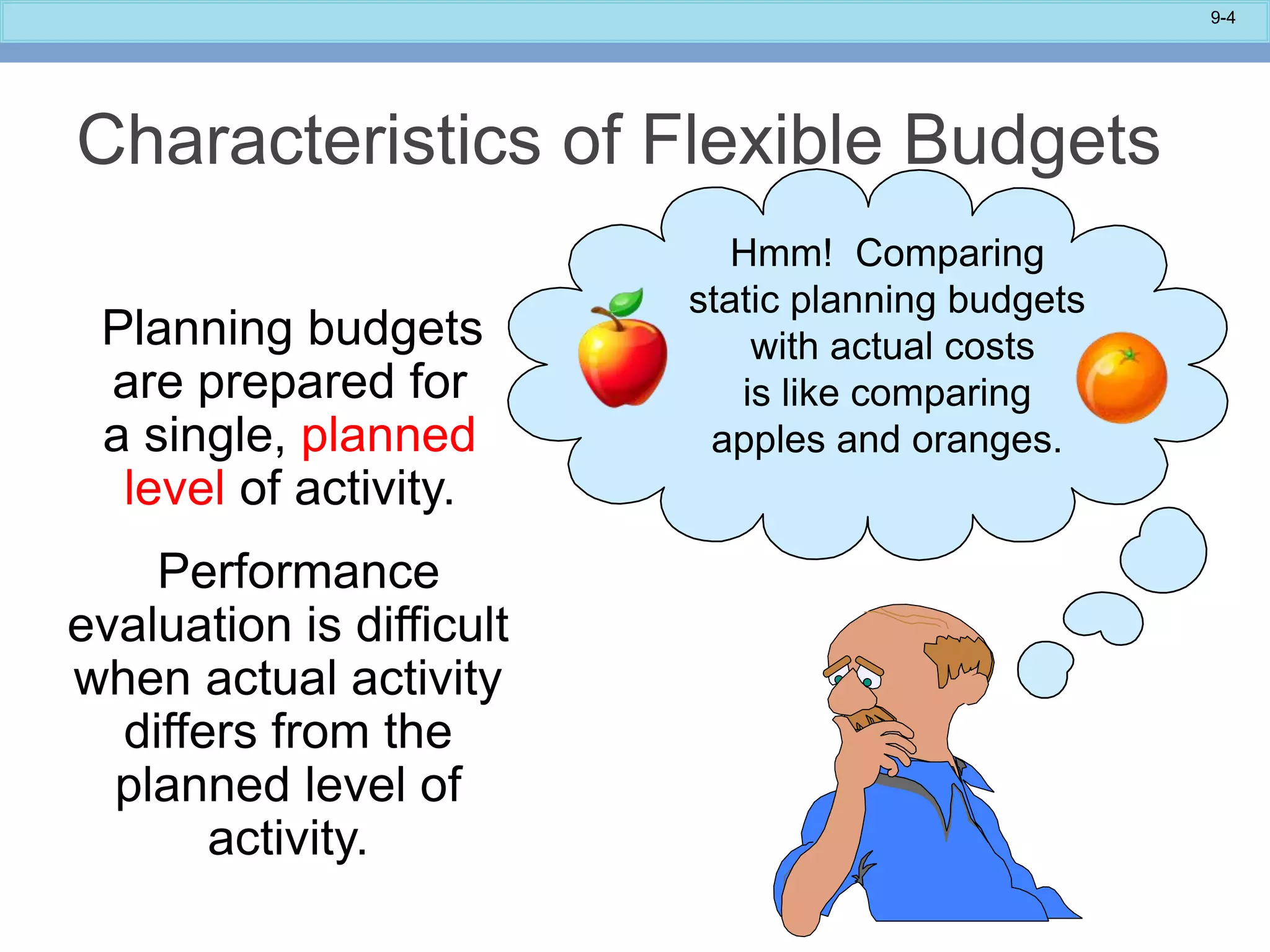

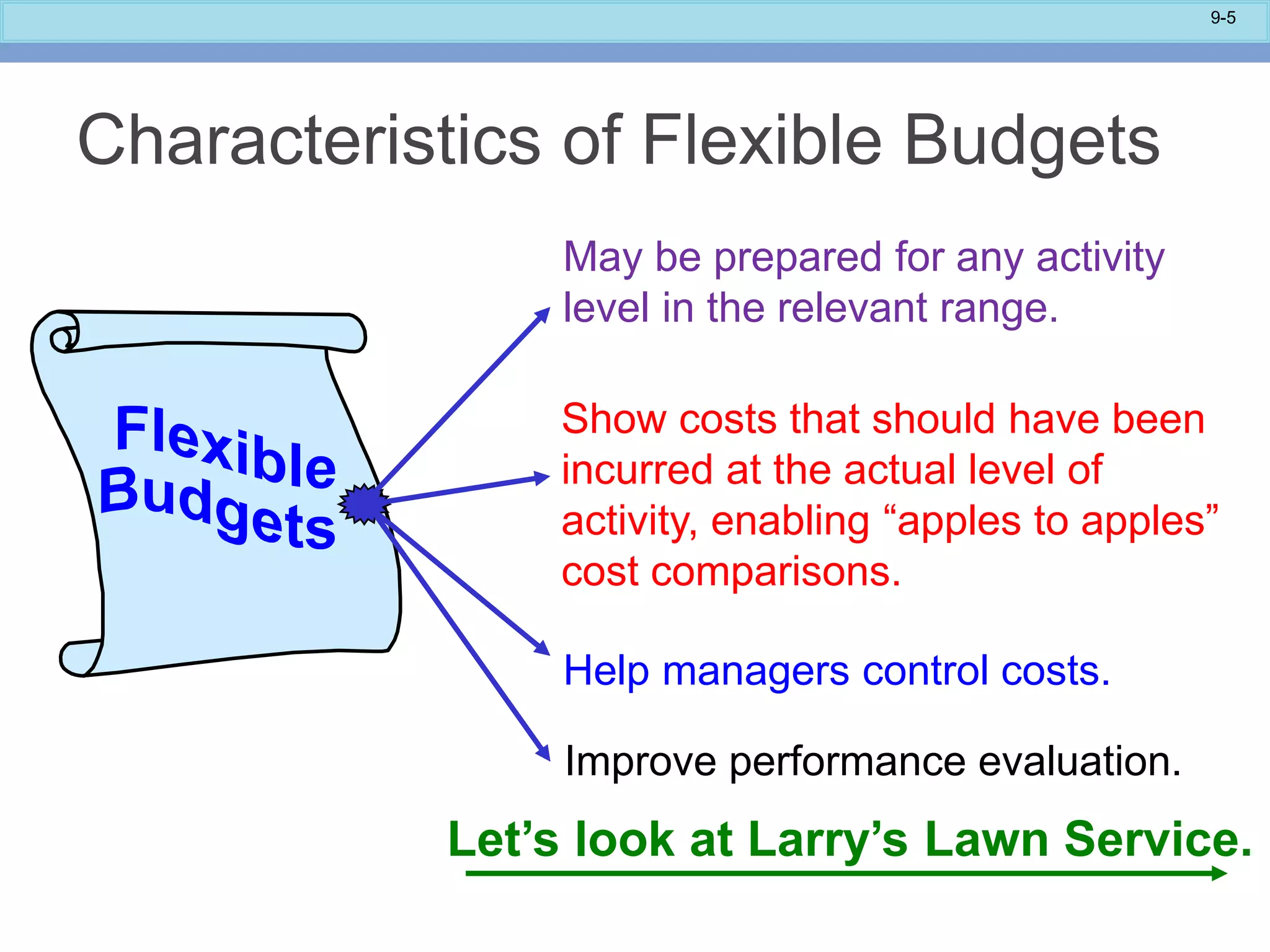

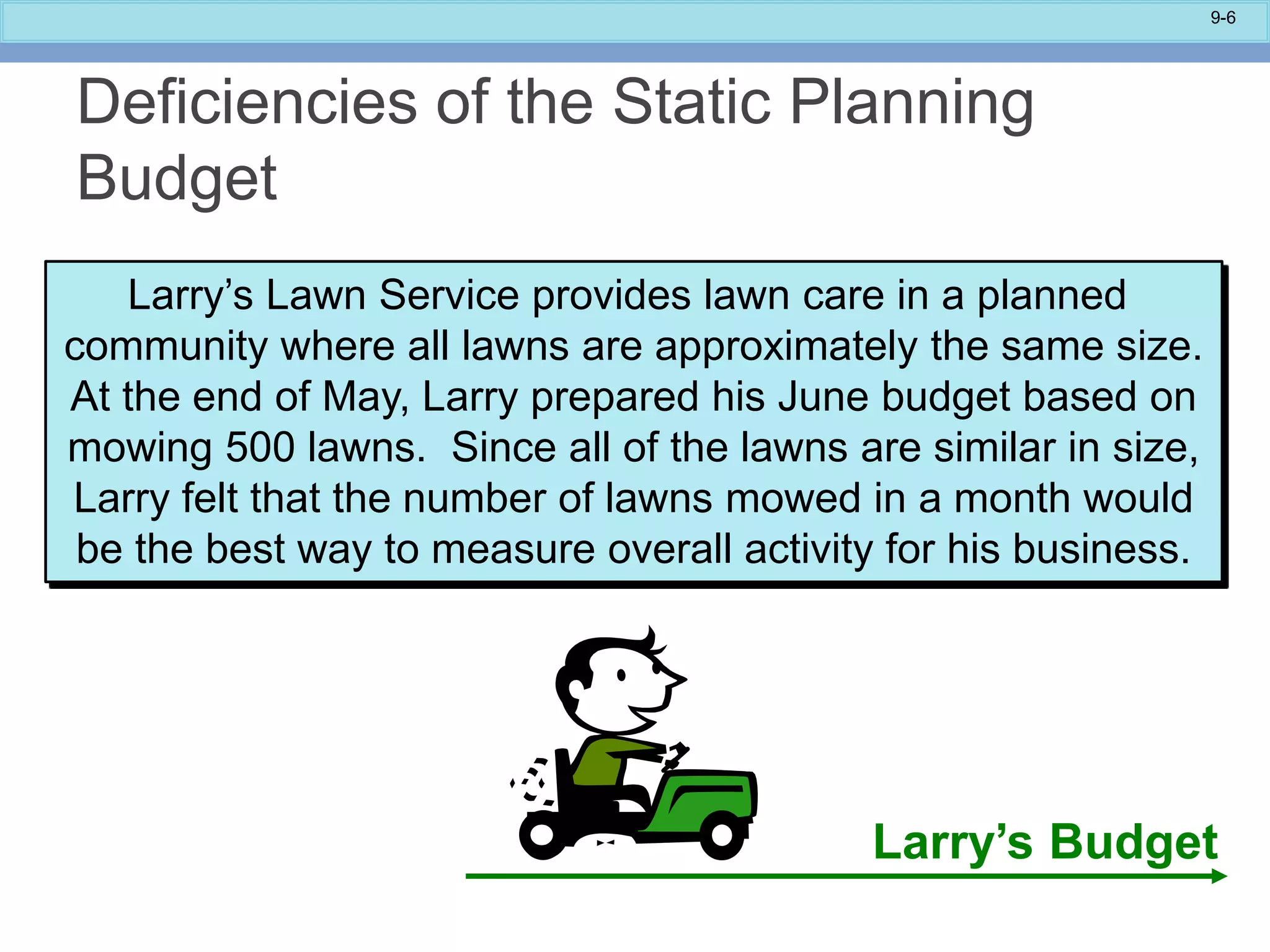

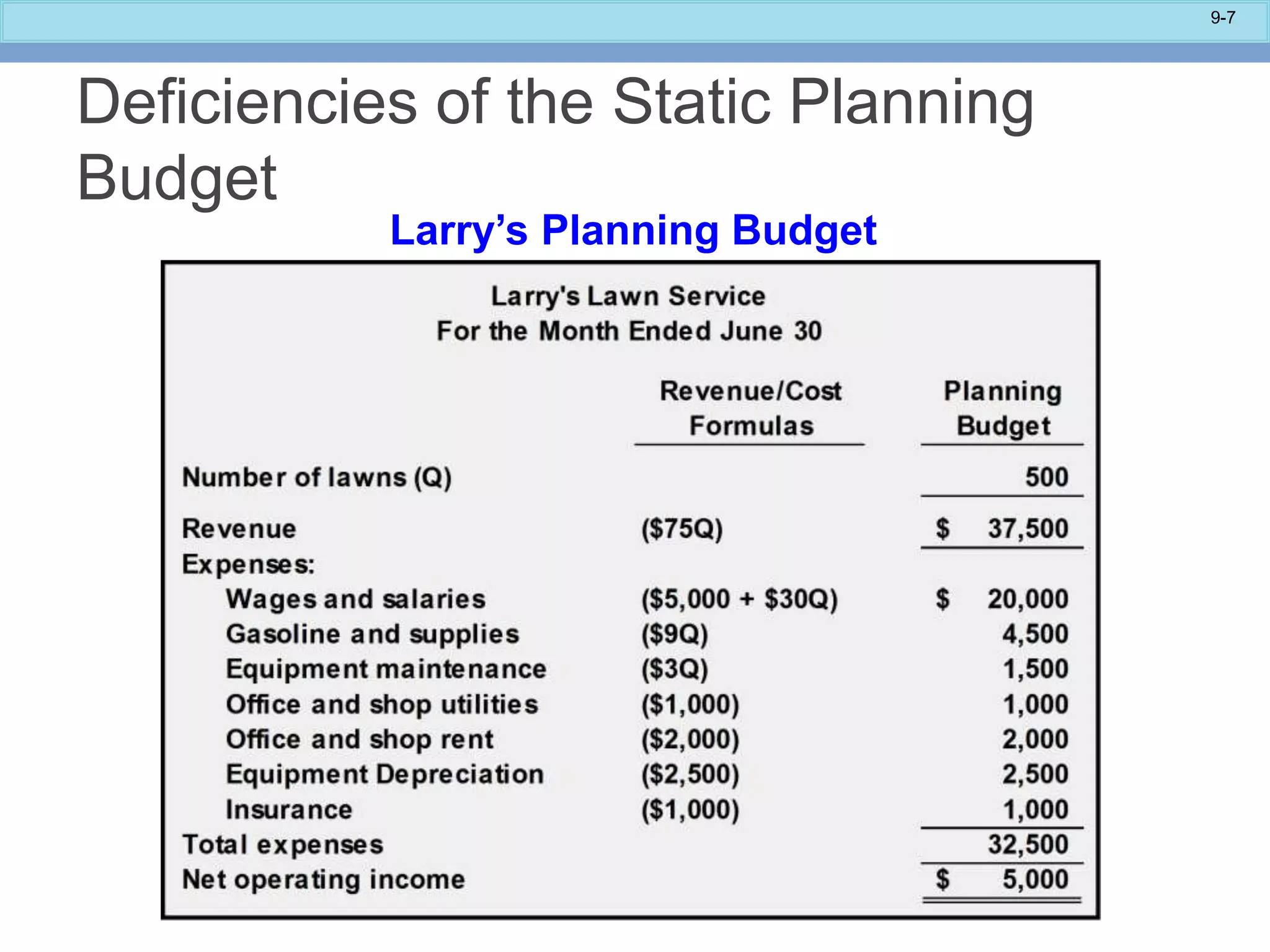

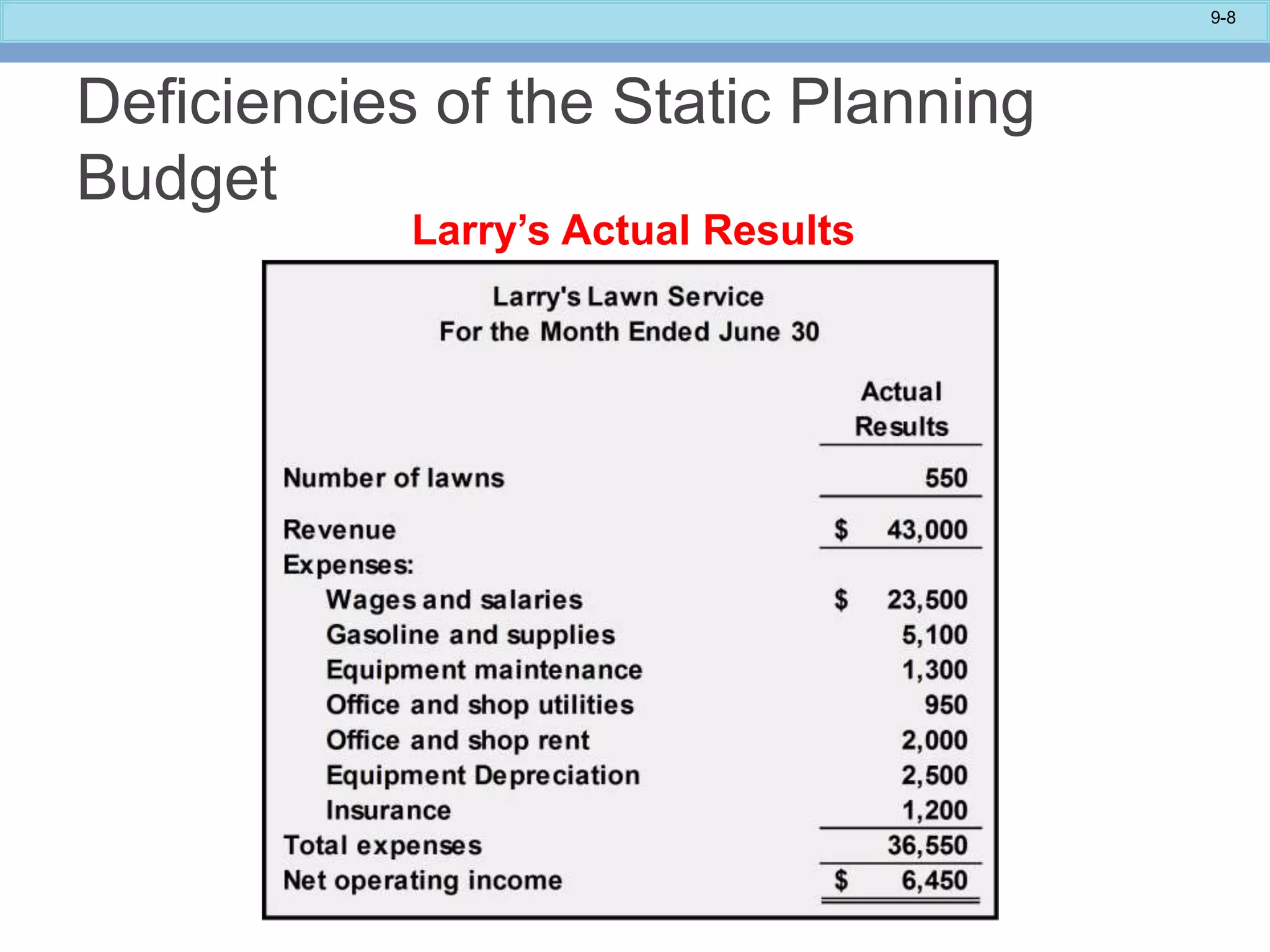

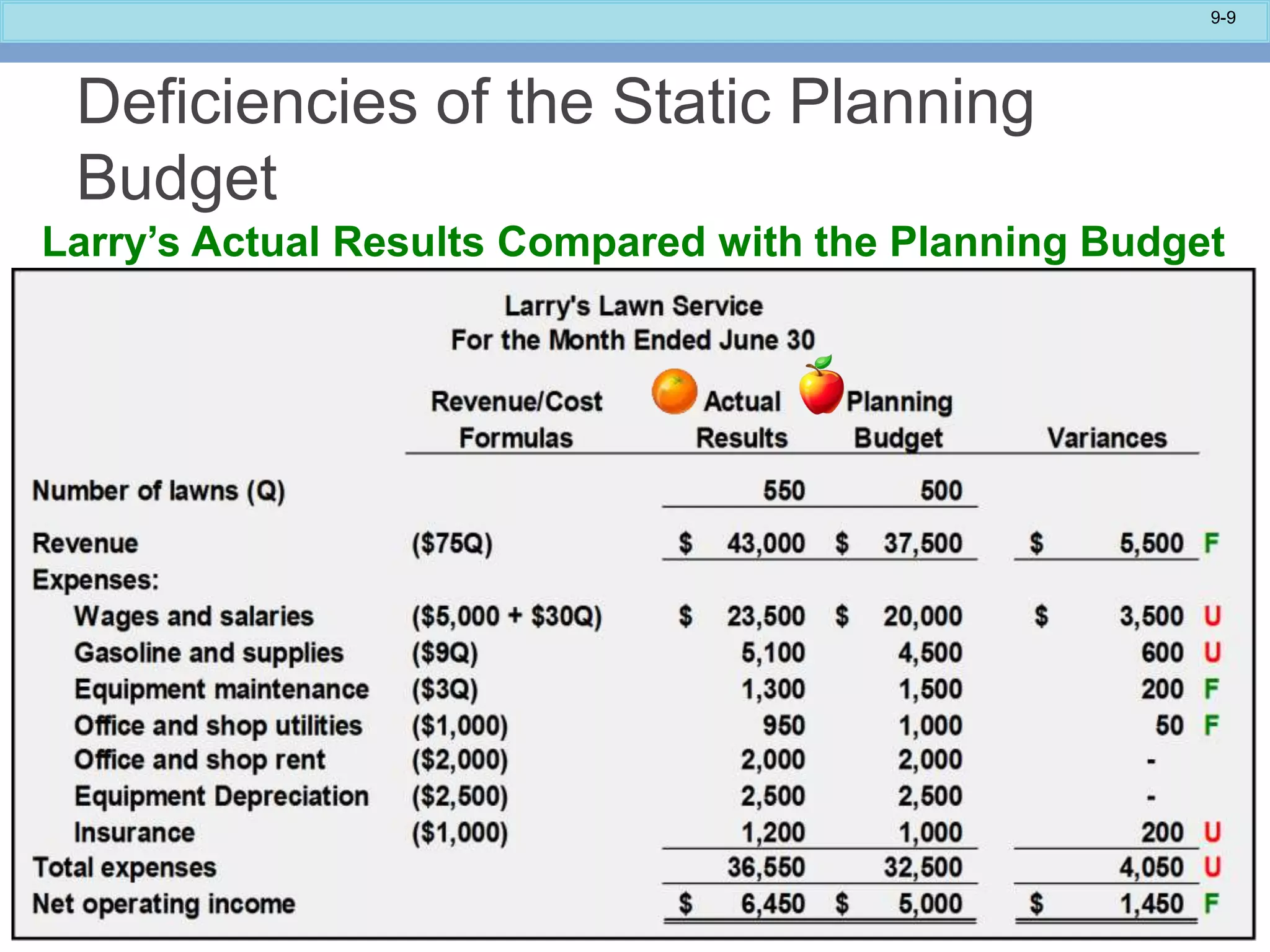

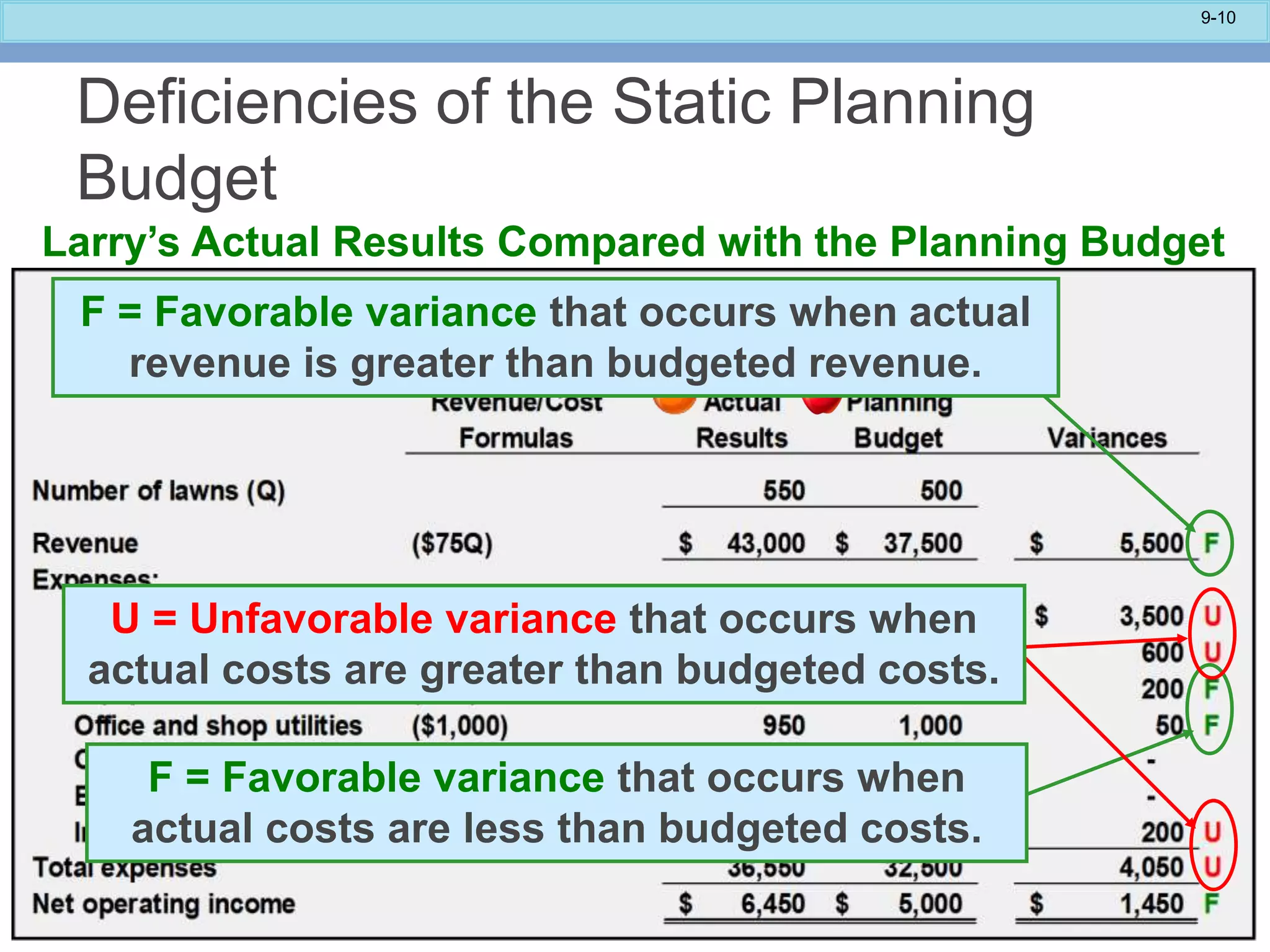

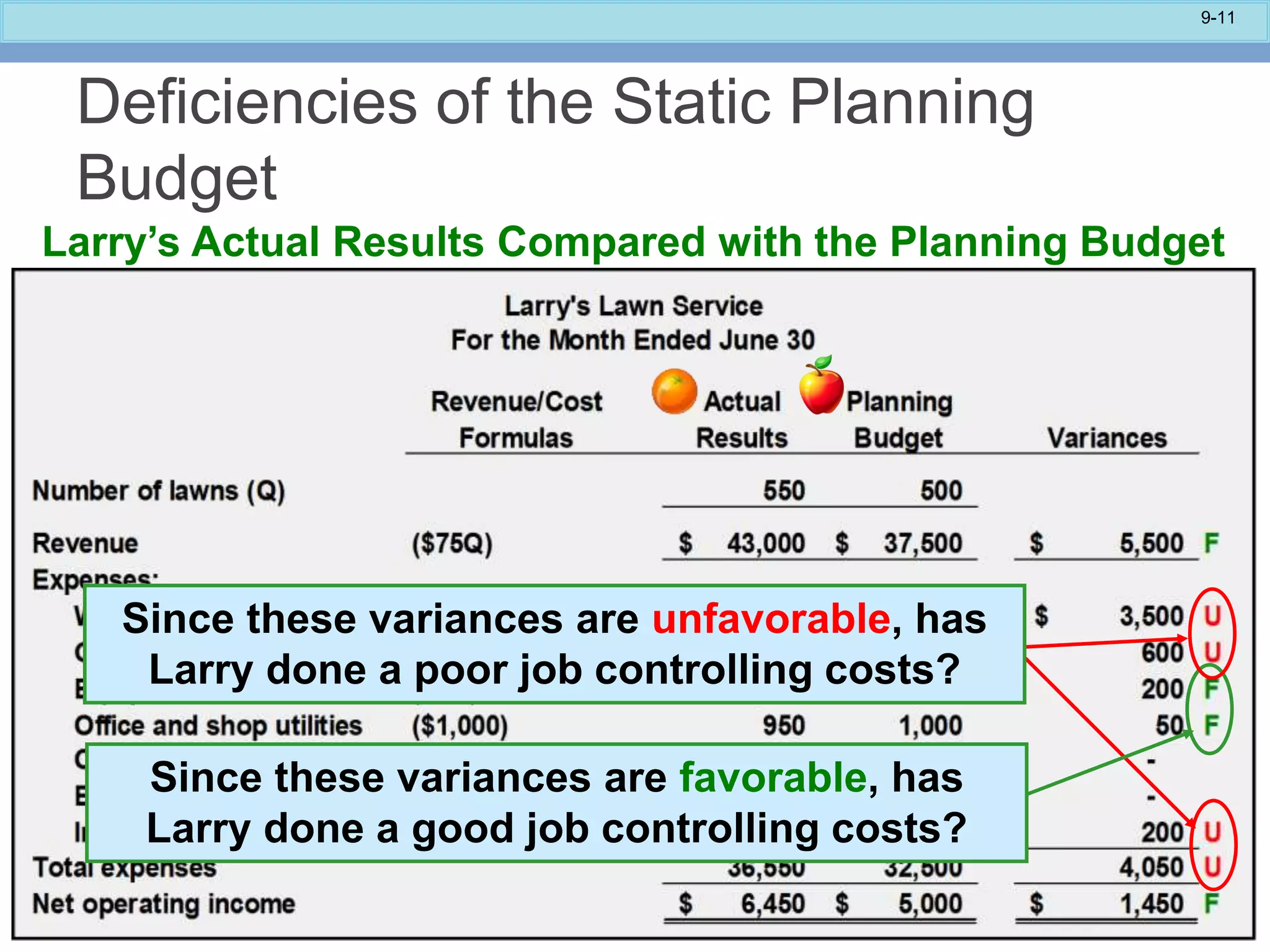

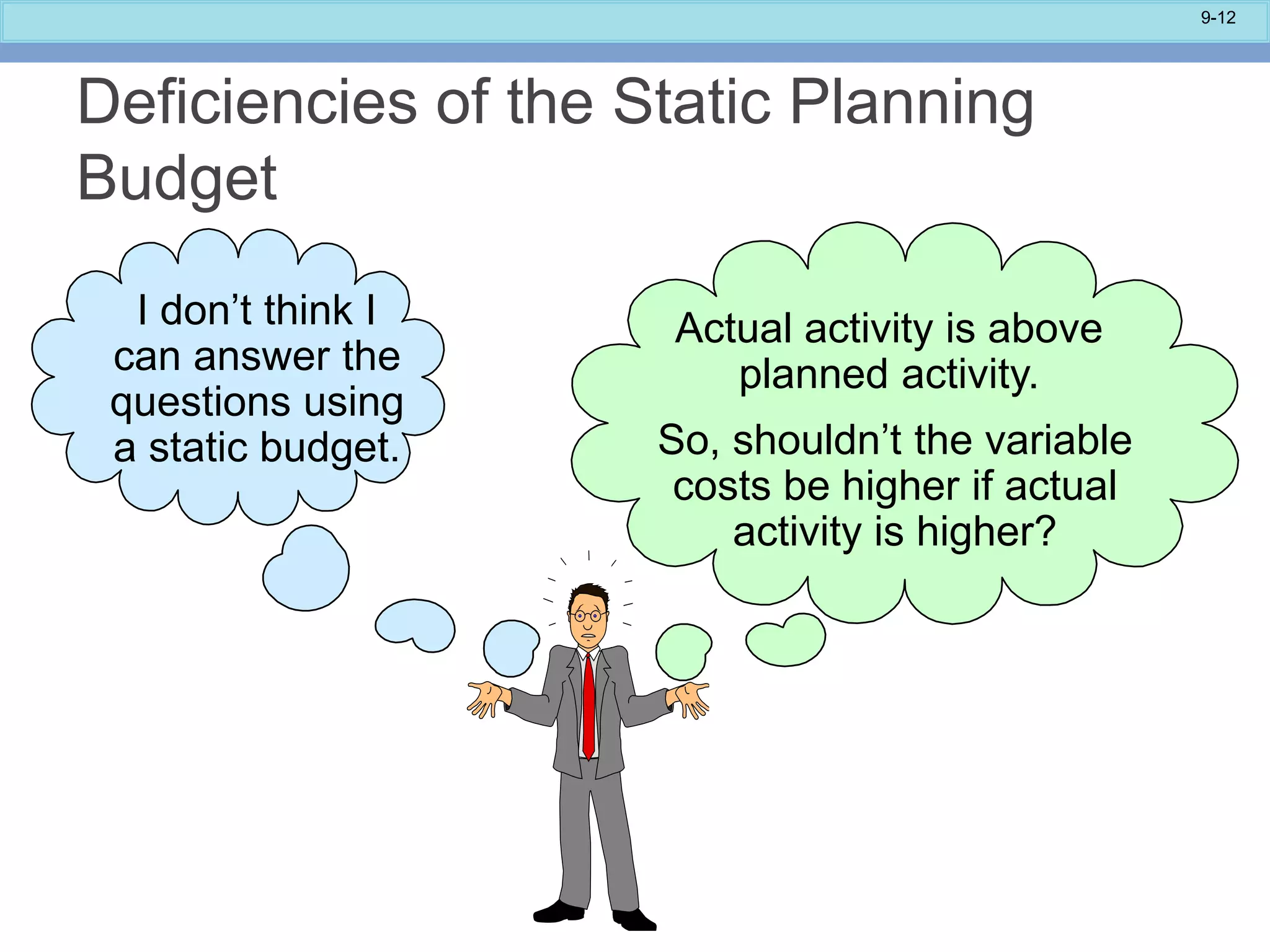

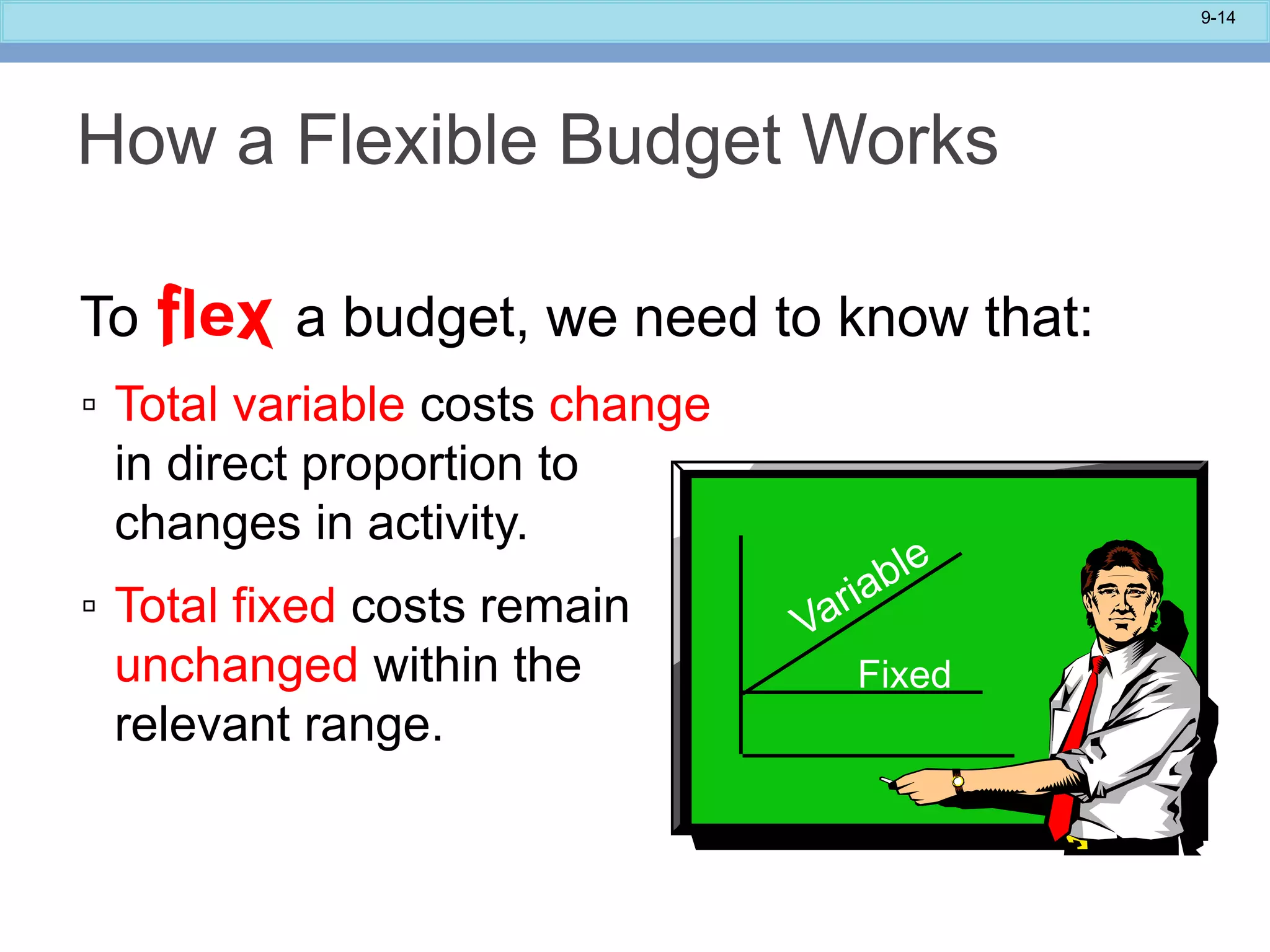

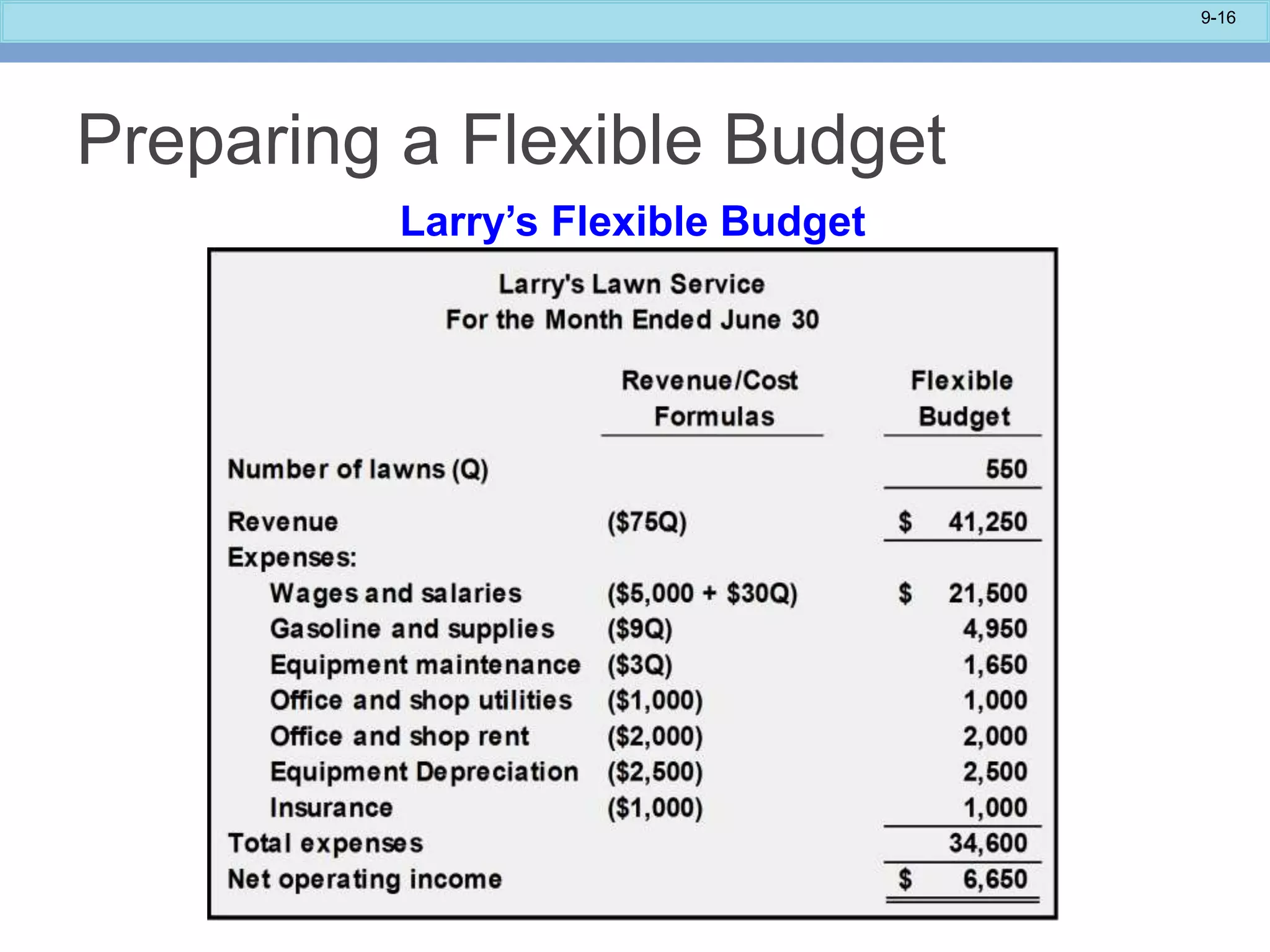

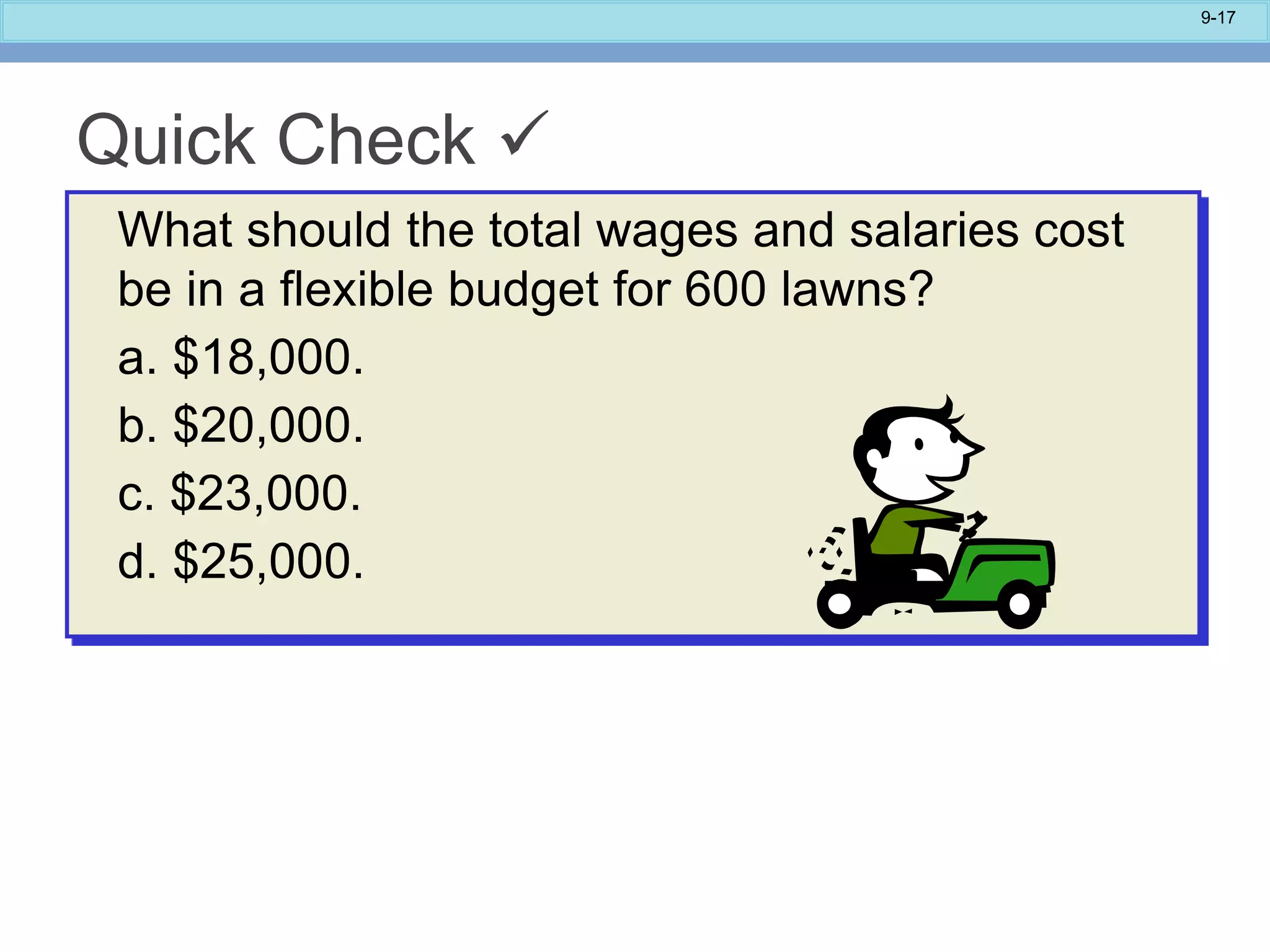

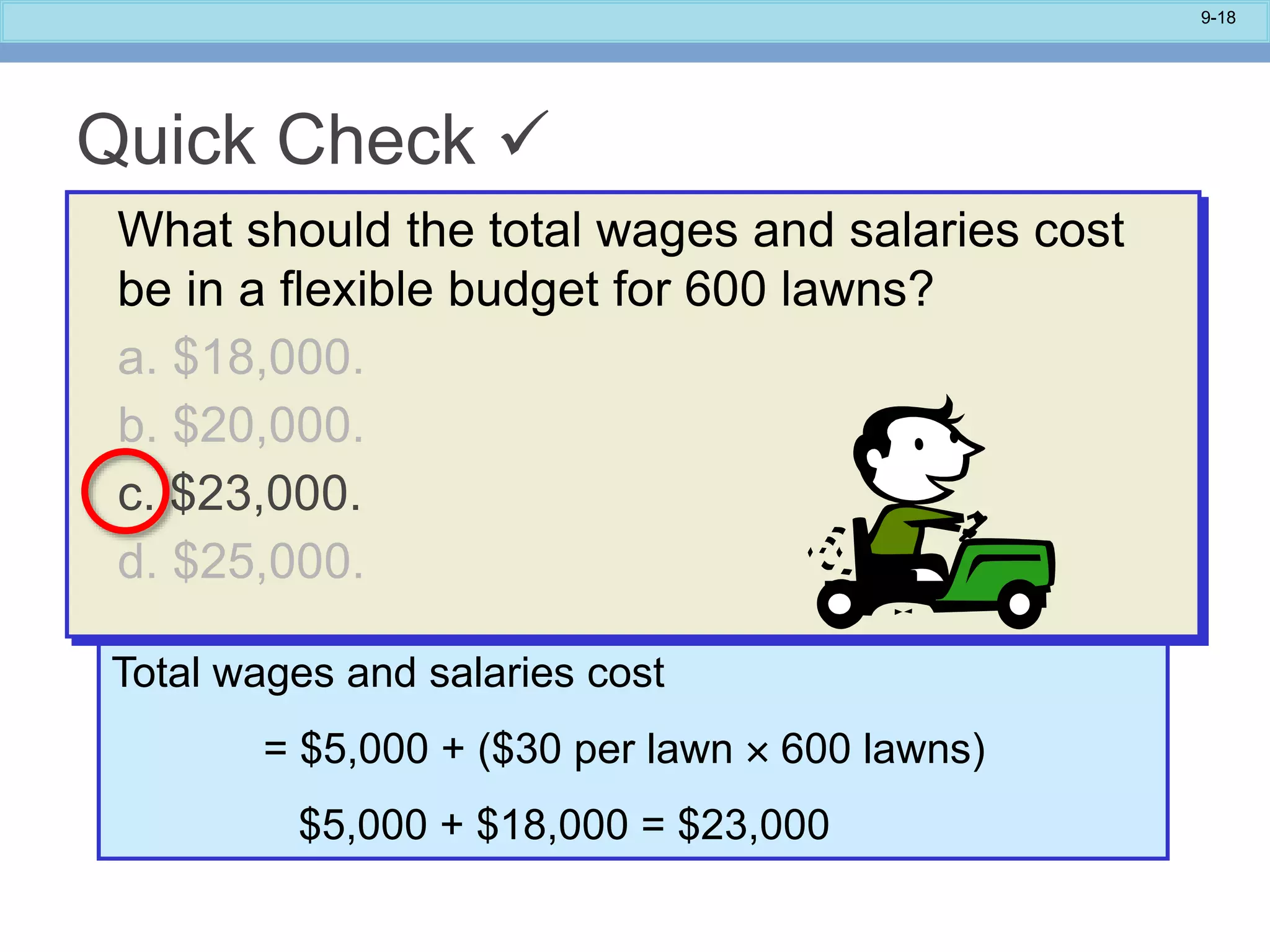

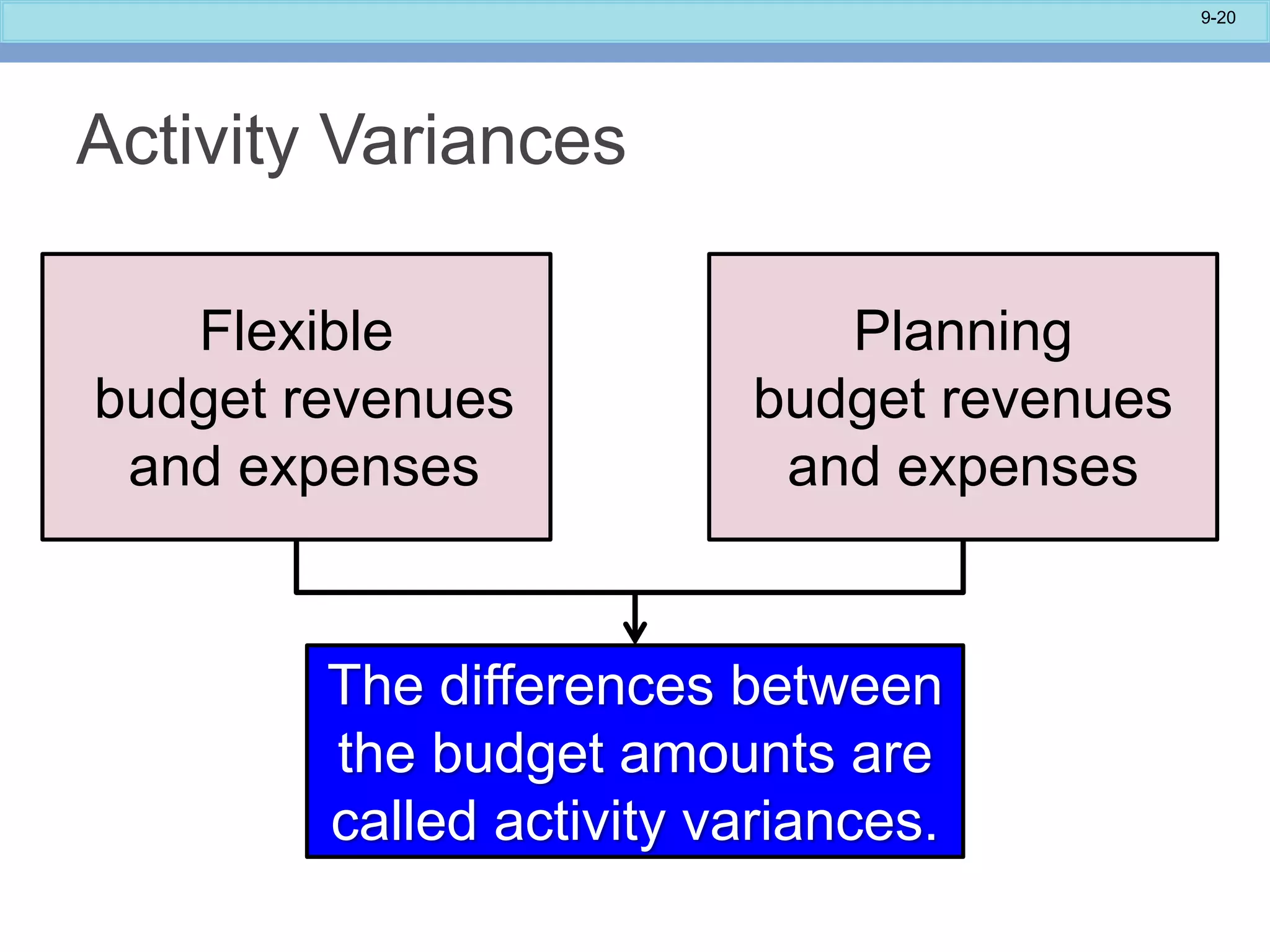

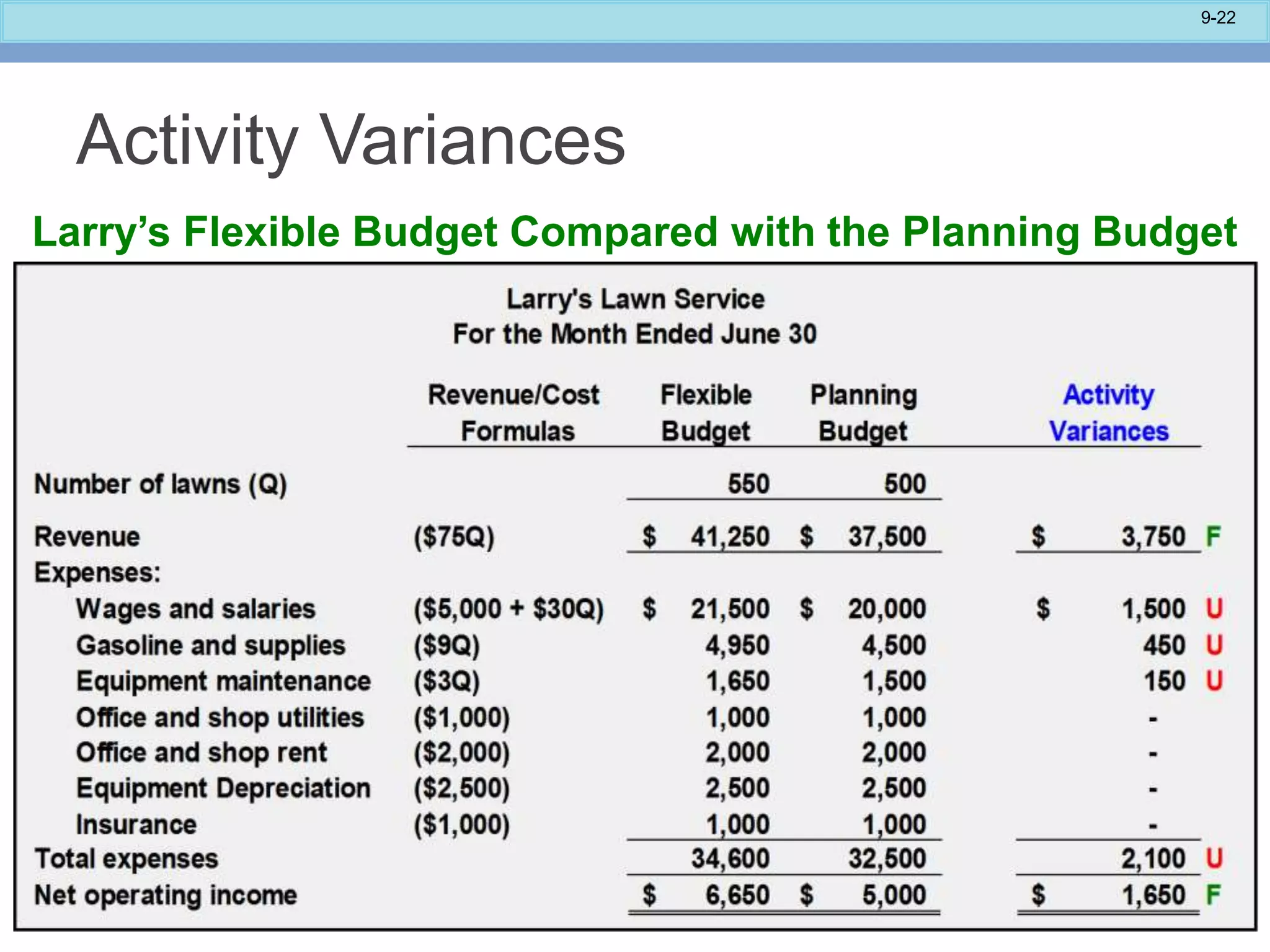

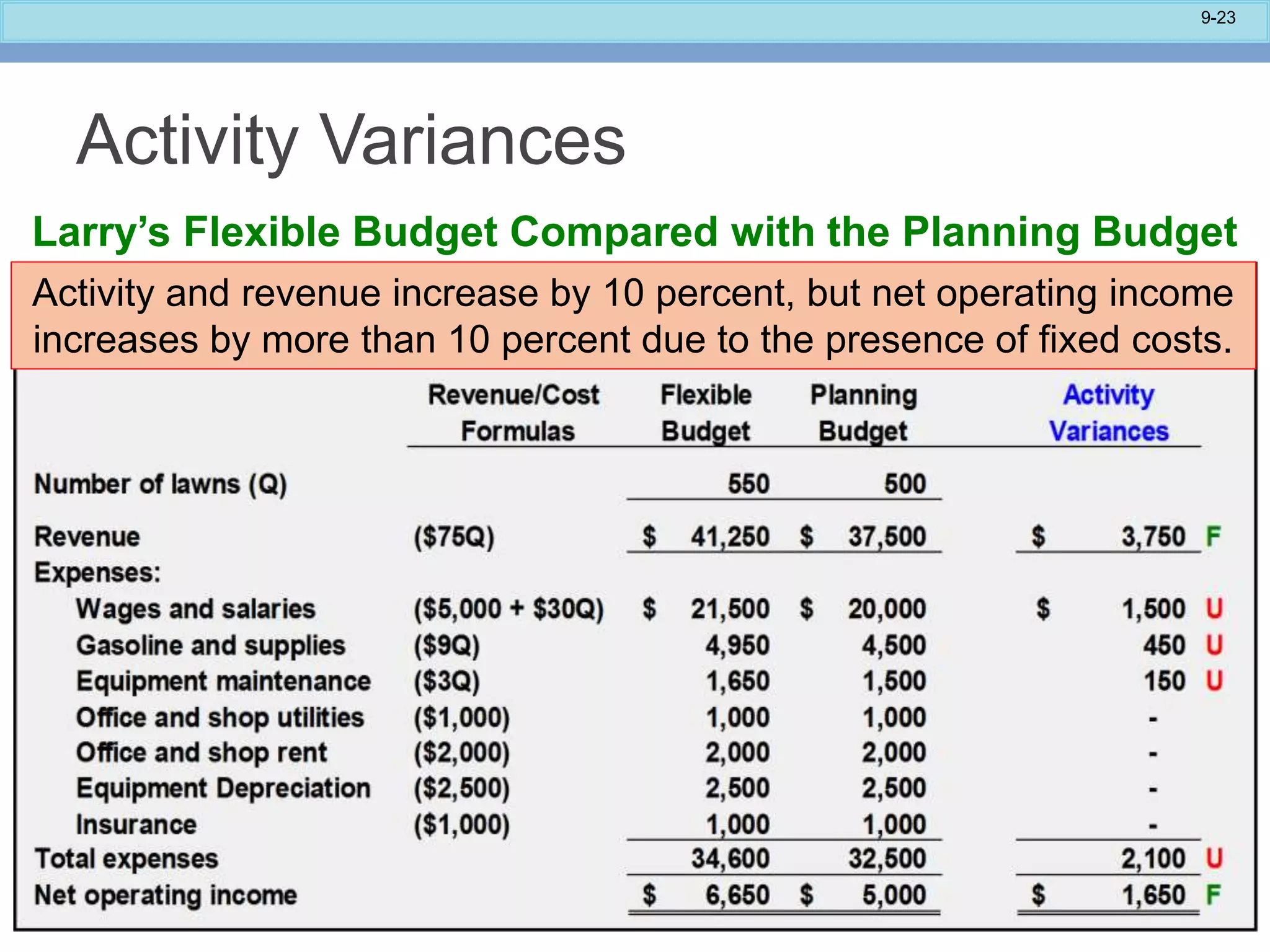

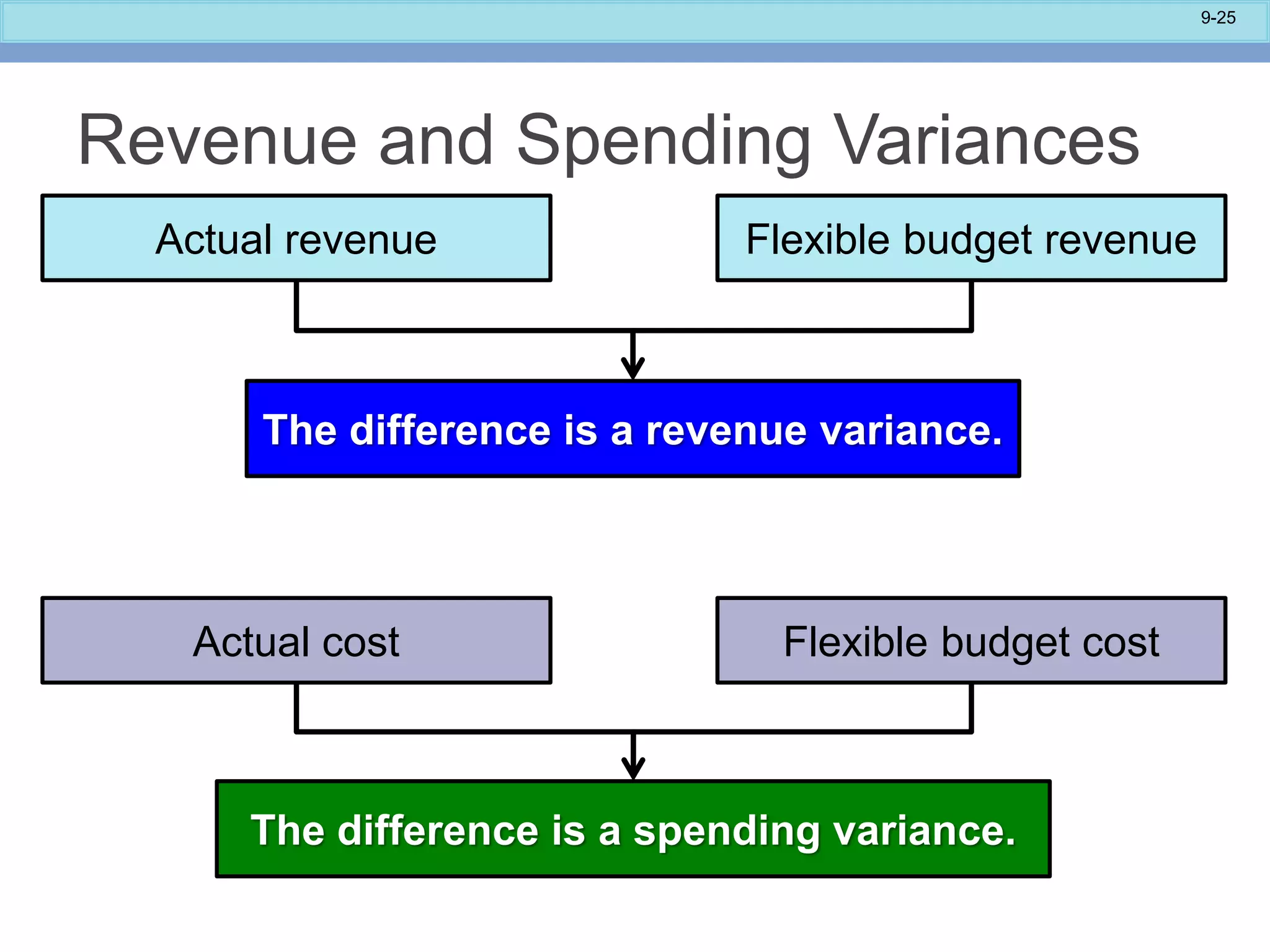

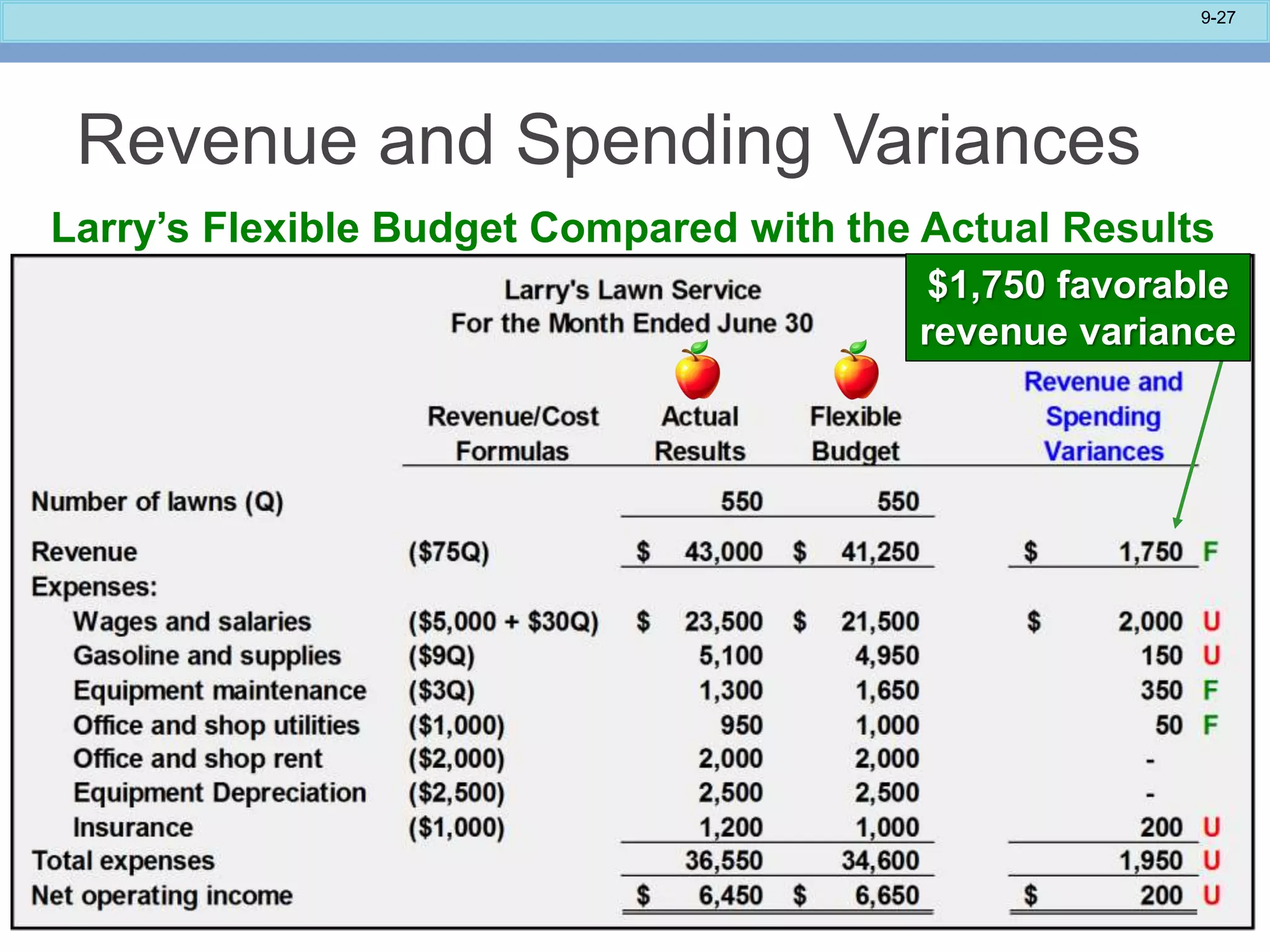

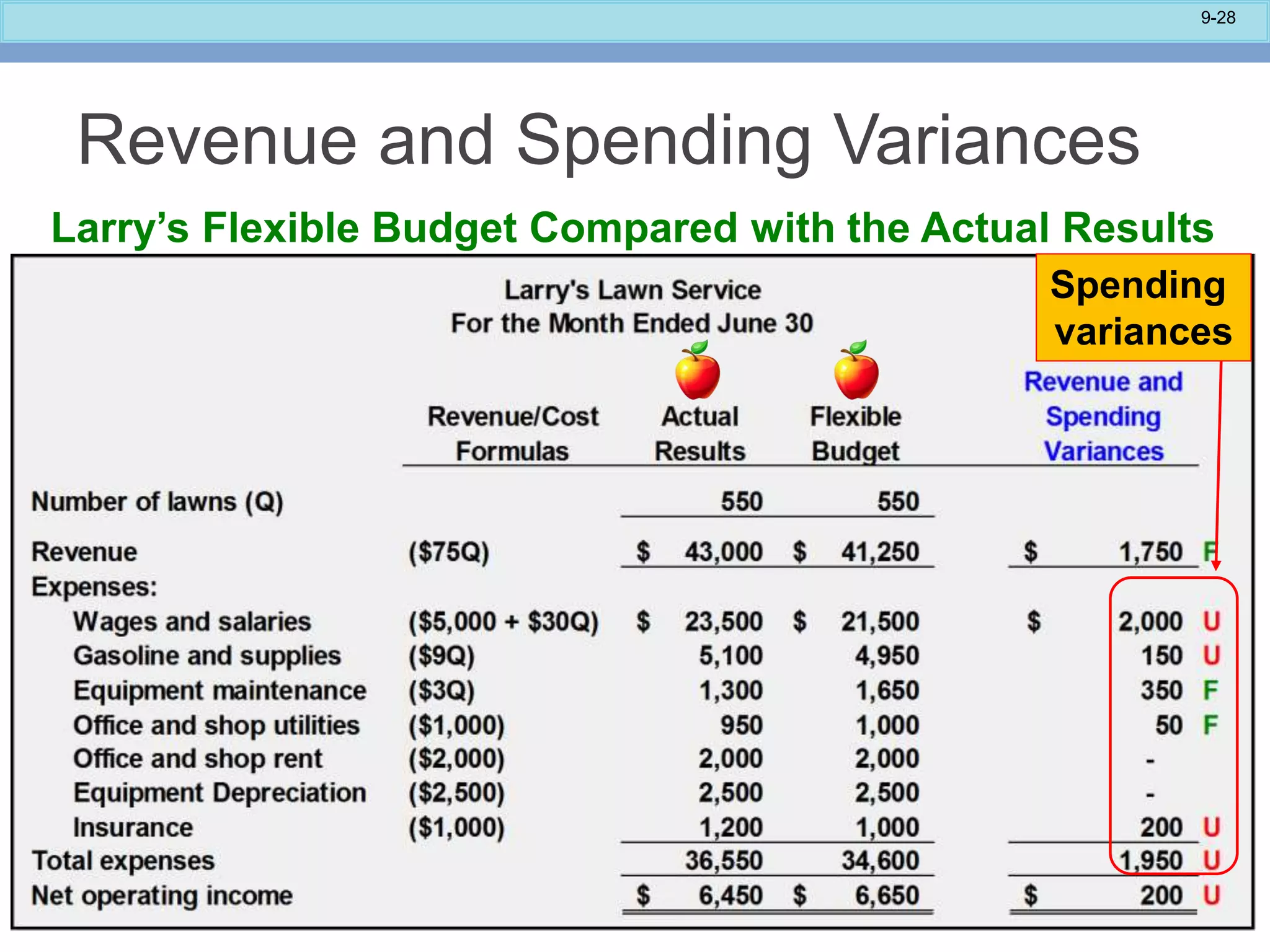

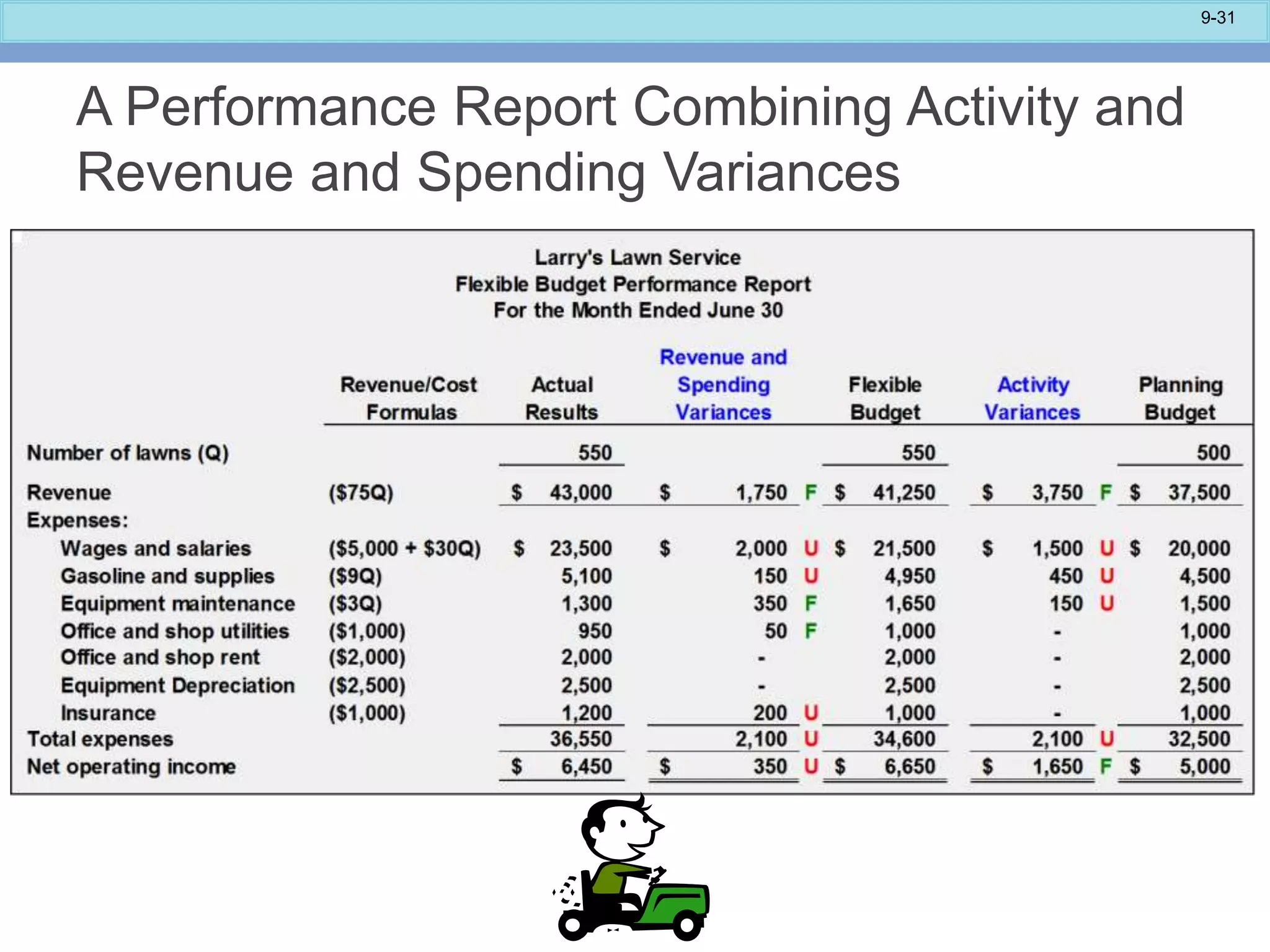

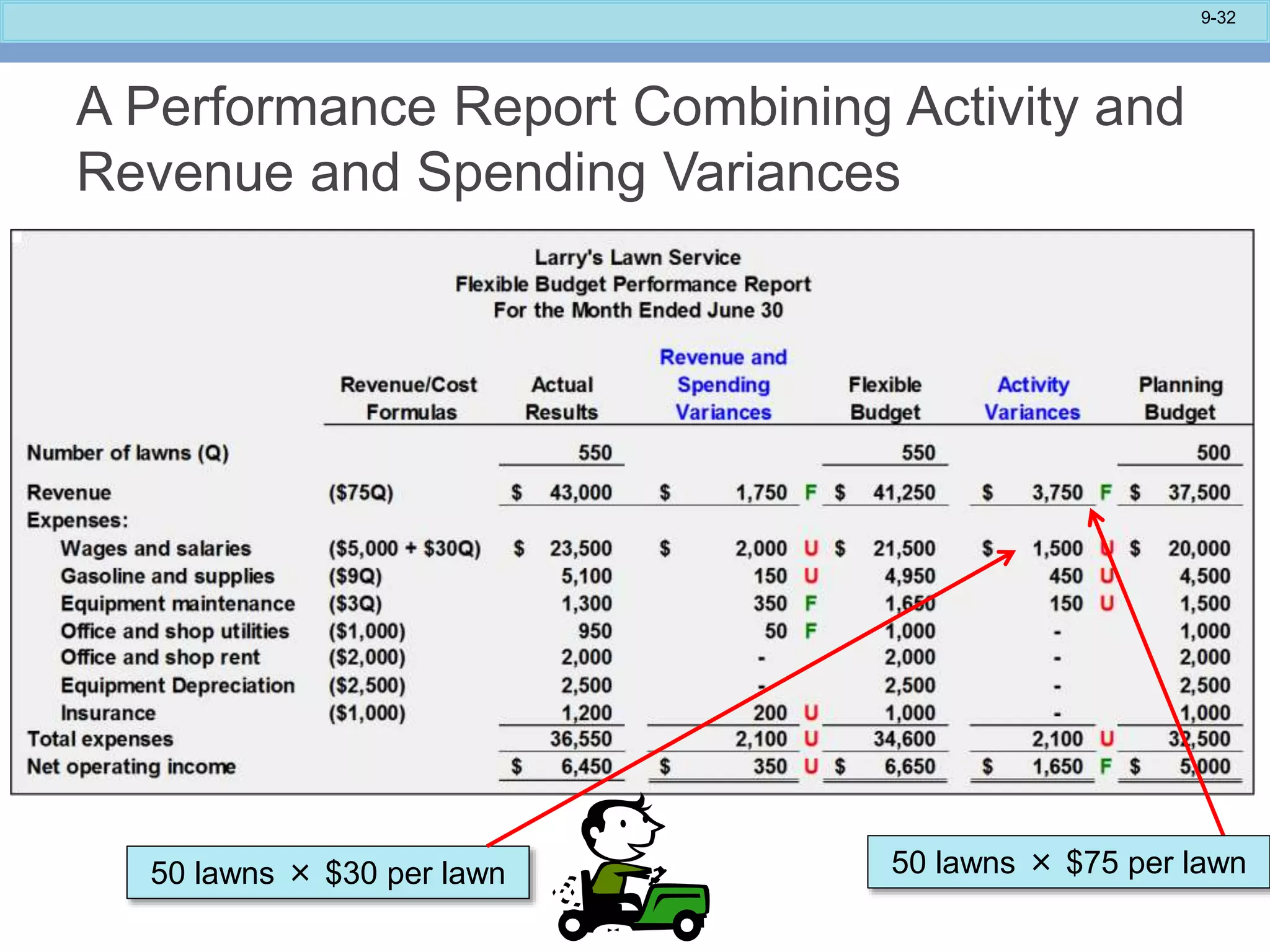

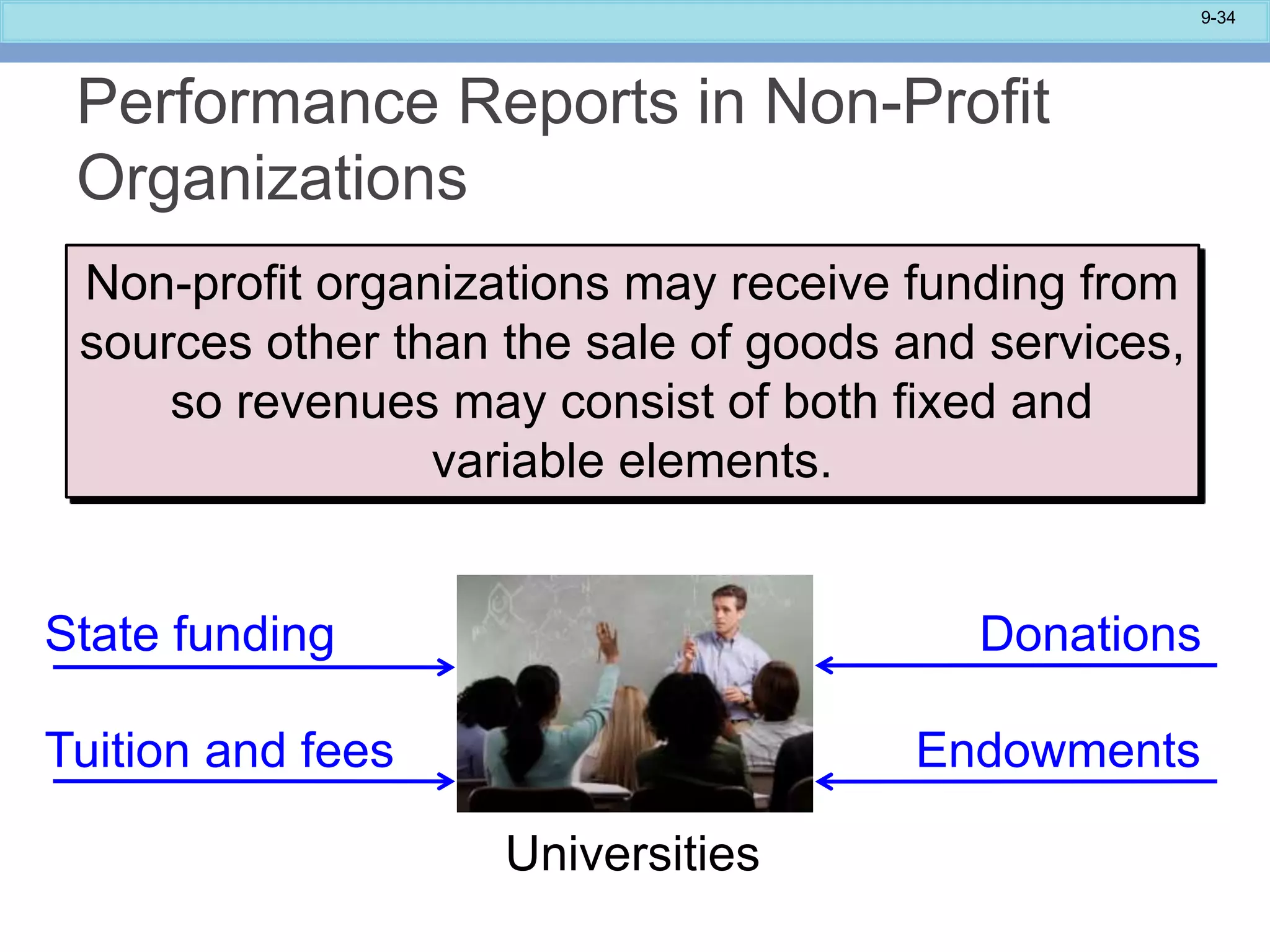

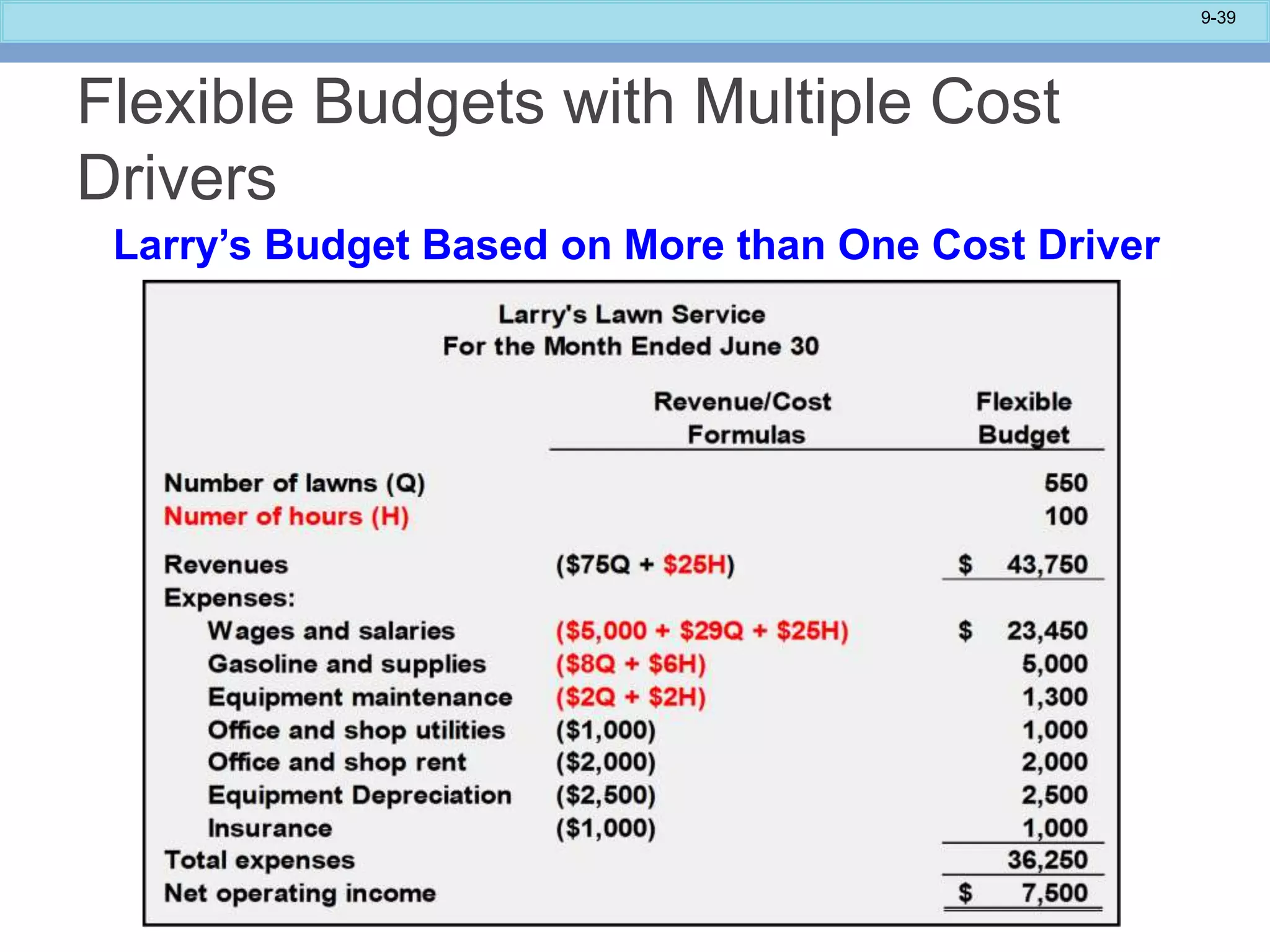

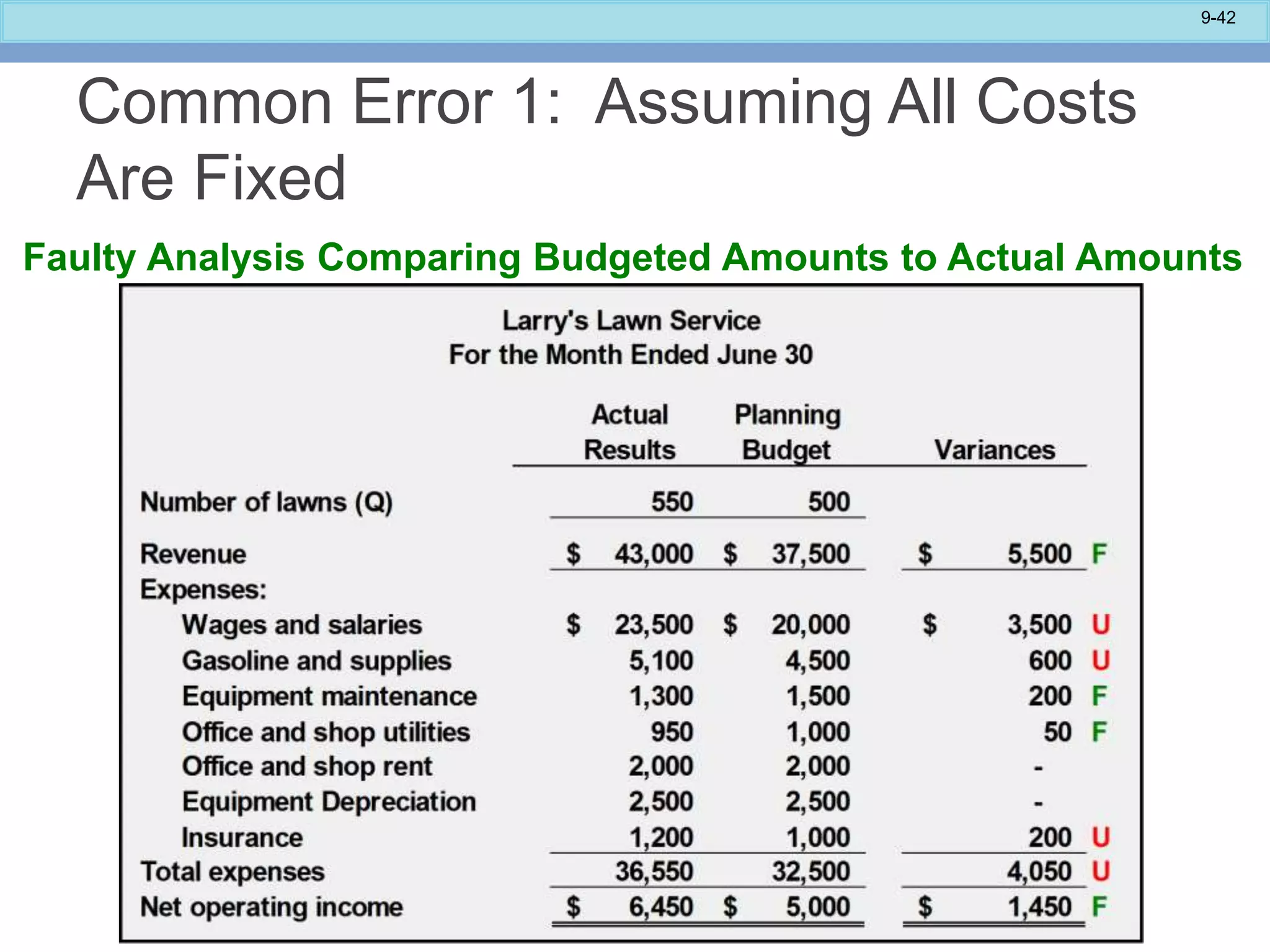

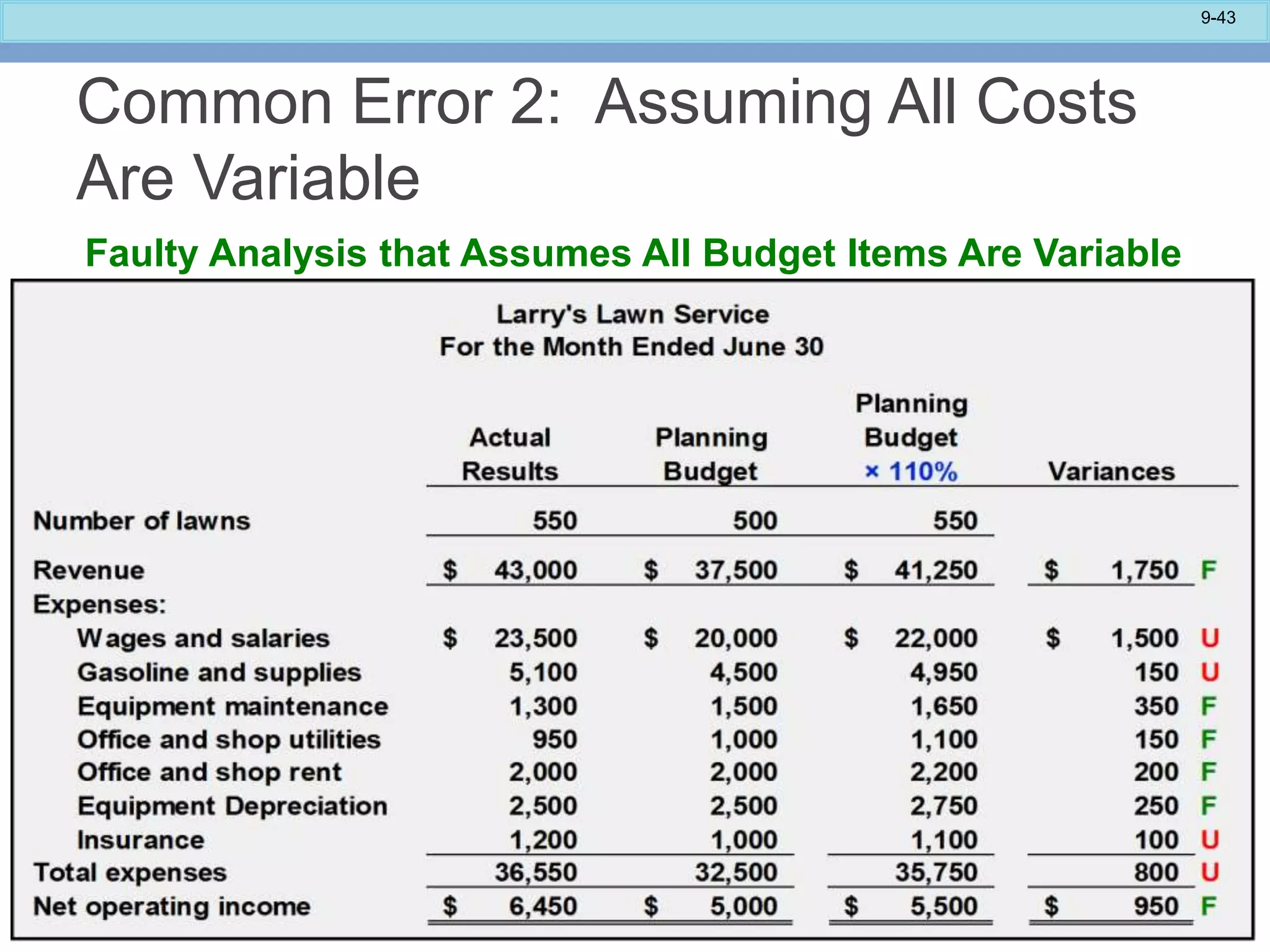

This document provides an overview of chapter 9 from a PowerPoint presentation on flexible budgets and performance analysis. It discusses the benefits of flexible budgets over static planning budgets, including their ability to improve performance evaluation when actual activity differs from planned levels. It then walks through an example of preparing a flexible budget for a lawn care company using number of lawns as the cost driver. The chapter covers calculating activity, revenue, and spending variances and combining these into a performance report. It also discusses using multiple cost drivers and common errors in flexible budget preparation, such as assuming all costs are fixed or variable.