CHAPTER 3

Flexible Budgets,Variances and Management Control

The use of Variances

Variances represent the difference between the cost that was incurred and the budgeted cost.

Each variance wecompute is the difference between an actual result and a budgeted amount. The

budgeted amount is a benchmark, a point of reference from which comparisons may be made.

Variances assist managers in their planning and control decisions. Management byexception is

the practice of concentrating on areas not operating as anticipated (such as a cost over run on a

defense project) and giving less attention to areas operating as anticipated. Managers use

information from variances when planning how to allocate their efforts. Areas with sizable

variances receive more attention by managers on an ongoing basis than do areas with minimal

variances. Variances are also used in performance evaluation.

Static Budget and Flexible Budgets

Distinguish a static budget from a flexible budget.

The Master budget or static budget is based on the level of output planned at the start of

the budget period.

Based on

In other words, the static budget is the “original” budget. It’s static in the sense that the budget is

developed for a single planned output level. A static budget is prepared at the beginning of the

budgeting period and is valid for only the planned level of activity. It is suitable for planning,

but it is inadequate for evaluating how well costs are controlled because the actual level of

activity is unlikely to equal the planned level of activity, thus resulting in “apples-to-oranges”

cost comparisons. When variances are computed from a static budget at the end of the period,

adjustments are not made to the budgeted amounts for the actual output level in the budget

period.

A Flexible budget (variable budget) – calculatesbudgeted revenues and budgeted costs

based on the actual output level in the budget period.

Based on

A flexiblebudget is calculated at the end of the period when the actual output is known; a static

budget is developed at the start of the budget period based on the planned output level for the

period. A flexible budget is dynamic rather than static; it can be tailored for any level of activity

1 | P a g e

Static budget

Planned level of output at start

of the budget period

Flexible budget

Budgeted revenues and cost

based on actual level of

output.

2.

within the relevantrange. A flexible budget provides estimates of what costs should be for any

level of activity within a specified range. A flexible budget is a performance evaluation tool.

When used for performance evaluation purposes, actual cost are compared to what the costs

should have been for the actual level of activity during the period. This enables “apples-to-

apples” cost comparisons. A flexible budget enables managers to compute variances that provide

more information than the information from variances in a static budget. A flexible budget can

be prepared for various levels of output whereas a static budget is based on one specific level of

output. A flexible budget adjusts the static budget for the actual level of output. It cannot be

prepared before the end of the period.

A flexible budget asks the question:

“If I had known at the beginning of the period what my output volume (units produced or units

sold) would be, what would my budget have looked like?”

Question: If the flexible budget (FB) is based on the level of output, which isn’t known until the

end of the period, how can it be a budget?

Answer: The flexible budget (FB) shows the costs that should have been incurred (the budgeted

costs) to achieve the actual output level. The FB is the budget we would have made at the

beginning of the period if we had perfectly predicted the actual output level.

Budgets, both static and flexible, can differ in the level of detail they report. Companies present

budgets with broad summary figures than can then be broken down into progressively more

detailed figures via computer software programs. The level of detail increases in the number of

line items examined in the income statement and the number of variances computed. “Level”

followed by a number denotes the amount of detail shown by a variance analysis.

Level 0 reports the least detail.

Level 1 offers more information, and so on.

Illustration 2.1

Webb manufactures and sells a designer jacket that requires tailoring any hand

operations. Saleare made to distributors who sell to independent clothing stores and

retail chains. Webb’s only costs are manufacturing costs; it incurs no costs in other value

chain functions such as marketing and distribution.

We assume that all units manufactured in April 2003 are sold in April 2003. There are

no beginning inventories or ending inventories. Webb has three variable-cost

categories. The budgeted variable cost per jacket for each category is:

Cost category Variable-cost per jacket

Direct materials costs------------------------------------- $60

Direct manufacturing labor costs----------------------- 16

Variable Manufacturing Overhead costs--------------- 12

Total Variable costs------------------------------------------$88

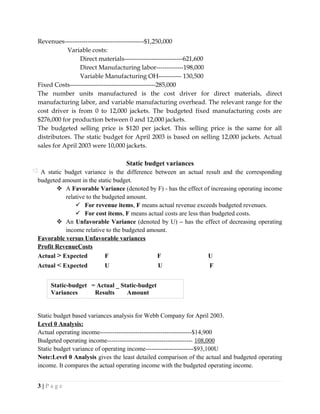

Actual April 2003 results are as follows:

Units sold-------------------------------------------10,000

2 | P a g e

3.

Revenues--------------------------------------$1,250,000

Variable costs:

Direct materials----------------------------621,600

DirectManufacturing labor-------------198,000

Variable Manufacturing OH----------- 130,500

Fixed Costs-----------------------------------------285,000

The number units manufactured is the cost driver for direct materials, direct

manufacturing labor, and variable manufacturing overhead. The relevant range for the

cost driver is from 0 to 12,000 jackets. The budgeted fixed manufacturing costs are

$276,000 for production between 0 and 12,000 jackets.

The budgeted selling price is $120 per jacket. This selling price is the same for all

distributors. The static budget for April 2003 is based on selling 12,000 jackets. Actual

sales for April 2003 were 10,000 jackets.

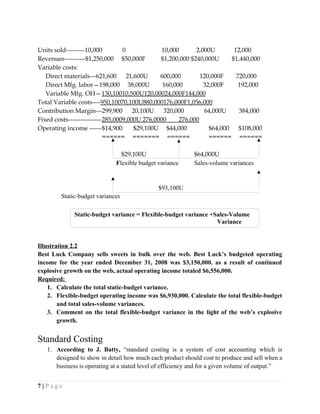

Static budget variances

A static budget variance is the difference between an actual result and the corresponding

budgeted amount in the static budget.

A Favorable Variance (denoted by F) - has the effect of increasing operating income

relative to the budgeted amount.

For revenue items, F means actual revenue exceeds budgeted revenues.

For cost items, F means actual costs are less than budgeted costs.

An Unfavorable Variance (denoted by U) – has the effect of decreasing operating

income relative to the budgeted amount.

Favorable versus Unfavorable variances

Profit RevenueCosts

Actual > Expected F F U

Actual < Expected U U F

Static budget based variances analysis for Webb Company for April 2003.

Level 0 Analysis:

Actual operating income--------------------------------------------$14,900

Budgeted operating income----------------------------------------- 108,000

Static budget variance of operating income-----------------------$93,100U

Note:Level 0 Analysis gives the least detailed comparison of the actual and budgeted operating

income. It compares the actual operating income with the budgeted operating income.

3 | P a g e

Static-budget = Actual _ Static-budget

Variances Results Amount

4.

Level 1 analysis:

ActualStatic-budget Static-budget

ResultsVariances Budget

(1)(2)=(1)-(3)(3)

Units sold--------------------10,000 2,000U 12,000

Revenues--------------------$1,250,000 $190,000 $1,440,000

Variable costs:

Direct Materials--------------621,600 98,400F 720,000

Direct Manufacturing labor—198,000 6,000U 192,000

Variable Mfg. Overhead-------130,500 13,500F144,000

Total Variable costs------------$950,100$105,900F$1,056,000

Contribution margin------------299,900 84,100U 384,000

Fixed costs-----------------------285,000 9,000U 276,000

Operating income---------------$14,900 $93,100 U $108,000

====== ======= =======

$93,100U

Static-budget variances

Level 1 analysis: Provides managers with more detailed information on the operating income. It

also compares actual operating income items with line(each) operating income items.

Steps in Developing Flexible Budget

The following steps are used to prepare a flexible budget:

Step1. Identify the actual quantity of output.

Step2. Calculate the flexible budget for costs based on budgeted variable cost per output

unit, actual quantity of output, and budgeted fixed costs.

Step3. Calculate the flexible budget for costs based on budgeted variable cost per output

unit, actual quantity of output, and budgeted fixed costs.

The only difference between the static budget and the flexible budget is that the static budget is

prepared for the planned output level, whereas the flexible budget is based on the actual output

level.

Webb develops its flexible budget in three steps:

Step1. Identify the actual quantity of output.

In April 2003, Webb produced and sold 10,000 jackets.

Step2. Calculate the flexible budget for costs based on budgeted variable cost per output unit,

actual quantity of output, and budgeted fixed costs.

Flexible-budget revenues = $120 per jackets x 10,000 jackets = $1,200,000

4 | P a g e

5.

Step3. Calculate theflexible budget for costs based on budgeted variable cost per output unit,

actual quantity of output, and budgeted fixed costs.

Direct materials, ($60/jacket @ 10,000 jackets) ------------------$600,000

Direct manufacturing labor ($16/jacket @ 10,000 jackets) ------160,000

Variable Mfg. overhead ($12/jacket @ 10,000 jackets) -----------120,000

Total flexible budget variable costs-------------------------------880,000

Plus: Flexible budget fixed costs---------------------------------------276,000

Flexible-budget total costs----------------------------------------------$1,156,000

i) Flexible-Budget Variances

The flexible budget variance is the difference between the actual results and the flexible- budget

amount based on the level of output actually achieved in the budget period.

5 | P a g e

Flexible-budget Variance = Actual – Flexible budget

Results Amounts

Static-Budget Variance

Flexible-budget Variance

Sales-Volume Variance

Price (Rate)

Variance

Efficiency

(usage)

Variance

Sales-Mix

Variance

Sales Quantity

Variance

Flexible-budget Variance = Price Variance + Efficiency Variance

6.

The flexible –budgetvariance pertaining to revenues is often called a selling- price variance

because it arises solely from differences between the actual selling price and the budgeted selling

price.

ii) Sales-Volume Variances

The sales-volume variance is the difference between a flexible-budget amount and the

corresponding static-budget budget amount. It’s called the sales-volume variance because it

represents the difference caused solely by the actual quantity of units sold and the quantity of

units expected to be sold in the static budget.

The sales-volume variances arises solely from the differences between the budgeted output level

used to develop the static budget and the actual output level used to develop the flexible budget.

Note particularly that any budgeted selling prices or unit variable costs are always held

constant when sales-volume variances are computed.

Hence:

Level 2 analysis:

Actual Flexible-budget Flexible Sales-volume Static

Results Variance Budget Variance Budget

(1) (2)=(1)-(3) (3) (4)=(3)-(5) (5)

6 | P a g e

Selling-price (Actual _ Budgeted

Variance = selling price selling price)X Actual units sold

Sales-Volume = Flexible-budget _ static-budget

Variance Amount Amount

Sales-volume = (Budgeted _ Budgeted Variable x (Actual _ Static-budget

Variance selling price cost per unit) units sold units sold)

Sales-volume = (Budgeted Contribution x (Actual _ Static-budget

Variance margin per unit units sold units sold)

7.

Units sold---------10,000 010,000 2,000U 12,000

Revenues----------$1,250,000 $50,000F $1,200,000 $240,000U $1,440,000

Variable costs:

Direct materials---621,600 21,600U 600,000 120,000F 720,000

Direct Mfg. labor—198,000 38,000U 160,000 32,000F 192,000

Variable Mfg. OH—130,10010,500U120,00024,000F144,000

Total Variable costs----950,10070,100U880,000176,000F1,056,000

Contribution Margin---299,900 20,100U 320,000 64,000U 384,000

Fixed costs----------------285,0009,000U 276,0000 276,000

Operating income ------$14,900 $29,100U $44,000 $64,000 $108,000

====== ======= ====== ====== ======

$29,100U $64,000U

Flexible budget variance Sales-volume variances

$93,100U

Static-budget variances

Illustration 2.2

Best Luck Company sells sweets in bulk over the web. Best Luck’s budgeted operating

income for the year ended December 31, 2008 was $3,150,000. as a result of continued

explosive growth on the web, actual operating income totaled $6,556,000.

Required:

1. Calculate the total static-budget variance.

2. Flexible-budget operating income was $6,930,000. Calculate the total flexible-budget

and total sales-volume variances.

3. Comment on the total flexible-budget variance in the light of the web’s explosive

growth.

Standard Costing

1. According to J. Batty, “standard costing is a system of cost accounting which is

designed to show in detail how much each product should cost to produce and sell when a

business is operating at a stated level of efficiency and for a given volume of output.”

7 | P a g e

Static-budget variance = Flexible-budget variance +Sales-Volume

Variance

8.

2. According toW.B. Lawrence, “A standard cost system is a method of cost accounting

in which standard costs are used in recording certain transactions and the actual costs are

compared with the standard costs to learn the amount and reason for any variations from

the standard.”

3. According to Brown and Howard, “standard costing may be defined as a technique of

cost accounting which compares the standard cost of each product or service with the

actual cost to determine the efficiency of the operation, so that any remedial action my be

taken immediately.”

4. According to I.C.M.A., London, “standard costing is the preparation and use of

standard costs, their comparison with actual costs and the analysis of variances to their

causes and points of incidence.”

A standard cost is the predetermined cost of manufacturing a single unit or a number of product

units during a specific period in the immediate future. It is the planned cost of a product under

current and / or anticipated operating conditions.

A standard is a "benchmark" or "norm" for measuring performance. Standards are found

everywhere your doctor, for example, evaluates your weight using standards that have been set

for individuals of your age, height and gender. the food we eat in restaurants must be prepared

under specified standards of cleanliness. The buildings we live in must conform to standards set

in building codes. Standards are also widely used in managerial accounting where they relate to

the quantity and cost of inputs used in manufacturing goods and producing services. Engineers

and accountants assist managers to set quantity and cost standards for each major input such as

raw materials and direct labor time. Quantity standards specify how much of an input should be

used to make a product or provide a service. Cost or price standards specify how much should be

paid for each unit of input. Actual quantities and actual costs are then compared with these

standards. In case of significant deviations managers investigate the discrepancies. The purpose

is to find the problem and eliminate it so that it does not recur. This process is

calledmanagement by exception.

In our daily lives, we operate in a management by exception mode most of the time. Consider

what happens when you sit down in the driver's seat of your car. You put the key in the ignition,

your turn the key, and your car starts. Your exception (standard) that the car will start is met; you

do not have to open the car hood and check the battery, the connecting cables, the fuel lines, and

so on. If you turn the key and the car does not start, then you have a discrepancy (variance). Your

exceptions are not met, and you need to investigate why. Note that even if the car is started after

a second try, it would be wise to investigate anyway. The fact that exception was not met should

be viewed as an opportunity to uncover the cause of the problem rather than as simply an

annoyance. If the underlying cause is not discovered and corrected, the problem may recur and

become much worse.

8 | P a g e

9.

This basic approachto identifying and solving problems is exploited in the variance analysis

cycle, the cycle begins with the preparation of standard cost performance reports in the

accounting department. These reports highlight the variances, which are the differences between

actual results and what should have occurred according to the standards. The variances raise

questions. Why did this variance occur? Why is this variance larger than it was last period? The

significant variances are investigated to discover their root causes. Corrective actions are taken

and then next period's operations are carried out. The cycle then begins again with the

preparation of a new standard cost performance for the latest period. The emphasis should be on

flagging problems for attention, finding their root causes, and then taking corrective actions. The

goal is to improve operations - not to find blame.

Who Uses Standard Costs?

Manufacturing, service, food, and not-for-profit organizations all make use of standards to some

extent. Auto service centers like Firestone and Sears, for example, often set specific labor time

standards for the completion of certain work tasks, such as installing a carburetor or doing a

valve job, and then measure actual performance against these standards. Fast-food outlets such as

McDonald's have exacting standards for the quantity of meat going a sandwich, as well as

standards for the cost of the meat. Hospitals have standards costs (for food, laundry, and other

items) for each occupied bed every day, as well as standard time allowances for certain routine

activities, such as laboratory tests. In short, you are likely to run into standard costs in virtually

any line of business that you enter.

Manufacturing companies often have highly developed standard costing systems in which

standards relating to direct materials, direct labor and overhead are developed in detail for each

separate product. These standards are listed on a standard cost card that provides the manager

with a great deal of information concerning the inputs that are required to produce a unit and

their costs.

Direct Materials Price and Quantity Standards:

Direct Materials Price Standards:

9 | P a g e

10.

Definition and Explanation:

Standardprice per unit of direct materials is the price that should be paid for a single unit of

materials, including allowances for quality, quantity purchased, shipping, receiving, and other

such costs, net of any discounts allowed.

Price standards for direct materials permit checking the performance of the purchasing

department and the influence of various internal and external factors and measuring the effect of

price increments or decrements on the company's profits. Determining the price or cost to be

used as the standard cost often difficult, because the prices used are controlled more by external

factors than by the company's management. Prices selected should reflect current market prices

and are generally used throughout the forthcoming fiscal period. If the actual price paid is more

or less than the standard price, a price variance occurs. This is usually called direct materials

price variance. Price increases or decreases occurring during the fiscal period are recorded in

thematerials price variance account(s). Price standards are revised at inventory dates or whenever

there is a major change in the market price of any of the principle materials or parts

Standard price per unit for direct materials should reflect the final delivered cost of materials, net

of any discounts taken. Allowances for freights and handling should also be taken into account.

Example:

Calculation of standard price per unit of direct materials or raw materials:

Purchase price, top-grade pewter ingots, in 40-pounds ingots

Freight, by truck, from suppliers warehouse

Receiving and handling

Less purchase discount

Standard price per pound

$ 3.60

+0.44

+0.05

-0.09

--------

$4.00

====

Notice that the standard price reflects a particular grade of materials (top grade), purchased in

particular lot size (40 pound ingots), and delivered by a particular type of carrier (truck).

Allowances have also been made for handling and discounts. If every thing proceeds according

to these expectations, the net cost of a pound of pewter (direct material in the example above)

should therefore be $4.00.

Direct Materials Quantity Standards:

Definition and Explanation:

10 | P a g e

11.

Standard quantity perunit of direct materials is the amount of direct materials orraw materials

that should be required to complete a single unit of product, including allowances for normal

waste, spoilage, rejects, and similar inefficiencies.

Quantity of usage standards are generally developed from materials specifications prepared by

the department of engineering (mechanical, electrical, or chemical) or product design. In a small

or medium sized company, the superintendent or even the foremen will state basic specifications

regarding type, quantity, and quality of raw materials need and operations to be performed.

Quantity standards should be set after the most economical size, shape, and quality of the

product and the results expected from the use of various kinds and grades of materials have been

analyzed The standard quantity should be increased to include allowances for acceptable levels

of waste, spoilage, shrinkage, seepage, evaporation, and leakage. The determination of spoilage

or waste should be based on figures that prevail after the experimental and developmental stages

of the product have been passed.

The standard quantity per unit for direct materials should reflect the amount of material required

for each unit of finished product, as well as an allowance for unavoidable waste, spoilage, and

other normal inefficiencies.

Example:

Calculation of standard quantity per unit of direct materials or raw materials:

Materials requirement (in pounds) per unit as specified in the bill of

materials*

Allowance for wastage and spoilage

Allowance for rejects

Standard of materials requirements (in pounds)

2.7

0.2

0.1

------

3.0

====

*A bill of materials is a list that shows the quantity of each type of material in a unit of finished

product. It is a handy source of determining the basic material input per unit, but it should be

adjusted for waste and other factors as shown above, when determining the standard quantity per

unit of product. "waste and spoilage" in the table above refers to materials that are wasted as a

normal part of the production process or that spoil before they are used. "Rejects" refers to the

direct materialcontained in units that are defective and must be scrapped.

Although it is common to recognize allowances for waste, spoilage, and rejects when setting

standard costs, this practice is now coming into question. Those involved in total quality

11 | P a g e

12.

management (TQM) andsimilar other business improvement programs argue that no amount of

waste or defects should be tolerated. If allowances for waste, spoilage, and rejects are built into

the standard cost, the levels of those allowances should be periodically reviewed and reduced

over time to reflect improvement process, better training, and better equipment.

Once the direct materials price and quantity standards have been set, the standard cost of a

material per unit of finished product can be computed as follows.

3 pounds per unit × $ 4.00 per pound = $ 12 per unit

This $12 cost figure will appear as one item on the product's standard cost card as shown by the

following example.

Example of standard cost card:

(1) (2) (3)

Inputs

Standard

Quantity or

Hours

Standard

Price or

Rate

Standard

Cost

(1) × (2)

Direct materials 3.0 pounds $ 4.00 $ 12.00

Direct labor 2.5 hours $ 14.00 $ 35.00

Variable manufacturing overhead 2.5 hours $ 3.00 $ 7.50

--------

Total standard cost per unit $54.50

=====

An important reason for separating standards into two categories - price and quantity - is that

different managers are usually responsible for buying and for using inputs and these two

activities occur at different points in time. In the case of raw materials the purchasing manager is

responsible for the price, and this responsibility is exercised at the time of purchase. In contrast,

the production manager is responsible for the amount of raw materials used, and this

responsibility is exercised when the materials are used in production, which may be many weeks

or months after the purchase date. It is important, therefore, that we cleanly separate

discrepancies due to deviations from price standards from those due to deviations from quantity

standards. Differences between standard prices and actual prices and standard quantities and

actual quantities are called variances. The act of calculating and interpreting variances is called

variance analysis.

Direct Labor Standards:

12 | P a g e

13.

Direct labor priceand quantity standards are usually expressed in terms of a labor rate and

labor hours.

1. Direct labor rate standards

2. Direct labor efficiency | usage | quantity standards

Direct Labor Rate Standards:

The standard rate per hour for direct labor includes not only wages earned but also fringe benefit

and other labor costs.

Example of Standard rate per direct labor hour:

Basicwagesrateperhour

Employment taxes at 10% of the basic rate

Fringe benefits at 30% of the basic rate

Standard rate per direct labor hour

$10

$ 1

$ 3

-----

$14

====

Many companies prepare a single standard rate for all employees in a department. This standard

rate reflects the expected "mix" of workers, even though the actual wage rates may very

somewhat from individual to individual due to different skills of seniority. A single standard rate

simplifies the use of standard costs and also permits the managers to monitor the use of

employees within department.

Direct Labor efficiency | Usage | Quantity Standards:

The standard direct labor time required to complete a unit of product (called the standard

hours per unit) is perhaps the most difficult standard to determine. One approach is to divide

each operation performed on the product into elemental body movements (such as reaching,

pushing, and turning over). Standard times for such movements are available in reference works.

These standard times can be applied to the movements and then added together to determine the

total standard time allowed per operation. Another approach is for an industrial engineer to do a

time and motion study, actually clocking the time required for certain tasks. The standard time

should include allowances for breaks, personal needs of employees, cleanup, and machine

downtime.

Example of standard labor hours per unit:

Basic labor time per unit, in hours

Allowance for breaks and personal need

allowance for cleanup and machine downtime

1.9

0.1

0.3

13 | P a g e

14.

Allowance for rejection

Standardlabor hours per unit of product

0.2

-------

2.5

====

Standard labor hours per unit and standard direct labor rate per hours computed above shall be

used in calculating labor rate variance and labor efficiency variance. Once the rate and time

standards have been set, the standard labor cost per unit of product can be computed as follows:

2.5 hours per unit × $14 per hour = $35 per unit

This $35 per unit standards labor cost appears along with direct materials on the standard cost

card of the product as shown by the following example.

Example of Standard Cost Card:

(1) (2) (3)

Inputs

Standard

Quantity or

Hours

Standard

Price or

Rate

Standard

Cost

(1) × (2)

Direct materials 3.0 pounds $ 4.00 $ 12.00

Direct labor 2.5 hours $ 14.00 $ 35.00

Variable manufacturing overhead 2.5 hours $ 3.00 $ 7.50

----------

Total standard cost per unit $54.50

=====

APPLICATION OF STANDARD COSTING

The application of standard costing requires the following conditions to be fulfilled:

1. a sufficient volume of standard products or components should be produced

2. Methods, procedures and materials should be capable of being standardized.

3. A sufficient number of costs should be capable of being controlled.

ADVANTAGE S OF STANDARD COSTING

The various advantages of standard costing are as follows:

1) Simplification of cost bookkeeping: It is very simple in comparison to historical

costing. Once the standards are fixed for the product, the records can be simplified

through uniformity which saves the time and money.

2) Basis for measuring operating performance:

3) Cost reduction and control:

4) Helpful in budgeting:

14 | P a g e

15.

5) Management byexception: standard costing is helpful in applying the principle of

management by exception. Variance analysis brings the inefficient operations in light and

management can focus its attention towards those matters only.

6) Prompt reporting:

7) Formulation of production and price policies:

8) Implementing incentive schemes:

9) Facilitates comparison:

10) Promotes cost consciousness and efficiency:

Direct Material Variances

1. Material Cost Variance (MCV): Material Cost Variance is the difference between the

standard costs of materials allowed for actual output and actual cost of materials used. It

can be calculated as follows:

Material cost Variance = standard cost —Actual cost

Or = (SQ x SR) – (AQ x AR)

If the actual cost is less than the standard cost, then it will be called as favourable variance

and vice-versa. It is the sum total of material price variance and material usage variance.

2. Material Price Variance (MPV): it arises when the price paid for materials is different

from the pre-determined price. The price variance may arise due to the following reasons:

(i) Change in basic price of material.

(ii) Discount is not received on purchase.

(iii) No bulk discount is received.

(iv) Cash discount is not received.

(v) Material is not purchased at appropriate time.

It can be calculated as follows:

Material Price Variance = Actual Quantity (Standard Rate ─ Actual rate)

= SR x AQ ─ AR x AQ

= AQ (SR ─ AR)

It will be favourable if the actual price is less than the standard price and vice-versa.

3. Material Usage Variance (MUV): It is also known as material efficiency variance or

material quantity variance. It is that part of material cost variance which measures the

difference in actual material cost and standard material cost for actual output. It may arise

due to less or more consumption of raw material. The other reason may be:

(i) Negligence in use of material.

(ii) Loss due to theft or fire.

(iii) Defective production needing more material for production.

(iv) Difference in standard and actual yield.

It can be calculated as follows:

Material Usage Variance = Standard Rate (Standard Quantity ─ Actual Quantity)

= SR x SQ ─ SR x AQ

= SR (SQ ─ AQ)

15 | P a g e

16.

If actual quantityused is less than the standard quantity, it will be favourable otherwise it

will be unfavourable or adverse.

Timing of Recognition of the Price Variance:

Some firms recognize the price variance for direct materials when the raw materials are

purchased, rather than waiting until the raw materials are put into production. In this

case, the AQ in the price variance will generally differ from the AQ in the quantity

variance, which is denoted in the following expressions for these variances:

PV = AQ Purchased x (AP – SP)

QV = SP x (AQ Used – SQ)

Where usually, AQ Purchased AQ Used

Recognizing the price variance when raw materials are purchased provides more timely

information to management about the cost of direct materials and the performance of the

purchasing department. Hence, this method for calculating the price variance has much to

commend it. However, in this situation, the sum of the price variance and quantity variance

will not equal the flexible budget variance, except by coincidence or when beginning and

ending quantities of raw materials are zero.

Direct Labour Variance

Labour Cost Variances: It is the difference between the standard direct wages given for the

activity and the actual wages paid. This variance arises due to change in wage rate or time

consumed or both. It can be calculated as follows:

Labour Cost Variance = Standard Cost ─ Actual Cost

= (SR x ST) ─ (AR x AT)

Labour Cost Variance is a sum total of labour rate variance, labour efficiency variance,

idle time variance and labour calendar variance

The formulas for splitting the flexible budget variance into a “price” variance and

“quantity” variance are the same for direct labor as direct materials. However, the

terminology differs slightly. What is called the price variance for direct materials is called

the rate variance or wage rate variance for direct labor.This variance measures any

deviation from standard in the average hourly rate paid to direct labor workers. In other

words, direct labor rate variance is the difference between the amount of actual hours

worked at actual rate and actual hours worked at standard rate.

[Labor rate variance = (Actual hours worked × Actual rate) − (Actual hours

worked × Standard rate)]

Or

LRV = AH (AR – SR)

16 | P a g e

17.

Where AH; theactual labor hours used in production, AR isthe actual wage rate, and SR is

the budgeted wage rate.

Rates paid to the workers are usually predictable. Nevertheless, rate variances can arise

through the way labor is used. Skill workers with high hourly rates of pay may be given

duties that require little skill and call for low hourly rates of pay. This will result in an

unfavorable labor rate variance, since the actual hourly rate of pay will exceed the standard

rate specified for the particular task. In contrast, a favorable rate variance would result

when workers who are paid at a rate lower than specified in the standard are assigned to

the task. However, the low pay rate workers may not be as efficient. Finally, overtime work

at premium rates can be reason of an unfavorable labor price variance if the overtime

premium is charged to the labor account.

Who is responsible for the labor rate variance?

Since rate variances generally arise as a result of how labor is used, production supervisors

bear responsibility for seeing that labor price variances are kept under control.

Direct Labor Efficiency Variance

Definition and Explanation:

The quantity variance for direct labor is generally called direct labor efficiency

variance or direct labor usage variance. This variance measures the productivity of

labor time. No variance is more closely watched by management, since it is widely believed

that increasing the productivity of direct labor time is vital to reducing costs

What is called the quantity or usage variance for direct materials is called the efficiency

variance for direct labor. We abbreviate this variance as EV:

EV = SP x (AQ – SQ)

Or

[Labor efficiency variance = (Actual hours worked × Standard rate) − (Standard

hours allowed × Standard rate)]

Where SP and AQ are the same as above and SQ is the flexible budget quantity of labor

hours (the labor hours the factory should have used for the volume of output units

produced).

The issue discussed earlier in this chapter regarding the timing of the recognition of the

price variance for direct materials does not arise for direct labor. Consequently, for direct

labor, the sum of the wage rate variance and efficiency variance always equals the flexible

budget variance.

Assume the following additional data for Webb to illustrate price and efficiency variance

The standard direct manufacturing labor cost of a jacket at Webb.

Standard direct material cost per jacket: 2 square yards of cloth input allowed per output unit

(jacket) manufactured, at $30 standard price per square yard

Standard direct material cost per jacket = 2 square yards * $30 per square yard = $60

Standard direct manufacturing labor cost per jacket:0.8 manufacturing labor-hour of input

allowed per output unit manufactured, at $20 standard price per hour

Standard direct manufacturing labor cost per jacket = 0.8 labor-hour * $20 per labor-hour = $16

17 | P a g e

18.

Overhead Variance

The flexibleoverhead budget is the managerial accountant’s primary tool for the control of

manufacturing overhead costs. At the end of each accounting period, the managerial

accountant uses the flexible overhead budget to determine the level of overhead cost that

should have been incurred, given the actual level of activity. Then the accountant compares

the overhead cost in the flexible budget with the actual overhead cost incurred. The

marginal accountant, given the necessary data computes four separate overhead variances,

each of which conveys information useful in controlling overhead costs.

Examp. 1. To illustrate overhead variance analysis, we will continue the illustration of the

XYZ Carpenters Share Company. During the month of January, the company produced

2,500 tables. Since production standards allow 4 machines–hours per table, the total

standard allowed number of machine hours for the actual output is computed as follows:

Actual Production Output 2,500 Tables

Standard Allowed Machine Hours Per

Table

X 4

Total Standard Allowed Machine Hours 10,000 Machines Hours

Thus, 10,000 machines–hours represent the standard machine-hours allowed for the actual

production of 2,500 tables. This means, according to the standard, only 10,000 hours of

machine time should have been used to manufacture the 2,500 tables actually produced in

January. From the 10,000 machine-hours column in the columnar flexible budget prepared

earlier, the budgeted overhead cost for January is follows:

Budgeted Overhead Cost For January

Variable Overhead Birr 65,000

Fixed Overhead 42,000

From the cost-accounting records of the company, the controller determined that the

following overhead costs were actually incurred during January to produce the 2,500 tables:

Actual Costs For January

Variable Overhead Birr 71,400

Fixed Overhead 43,800

Total Overhead Birr 115,200

The production supervisor’s records of the company indicate that the actual machine-hours

used during January to produce the 2,500 tables were 10,500 hours. Notice that the actual

number of machine-hours used (10,500 hours exceeds the standard allowed number of

machine hours 10,000 hours), given the actual production output 2,500 tables. Now all of

the information necessary to compute XYZ Carpenters Share company’s overhead variances

for January is assembled. Therefore, in the discussions that follow in this section, you will

study how overhead cost variances are computed and interpreted.

18 | P a g e

19.

The company’s totalvariable-overhead variance for January is computed below:

Actual Variable Overhead Birr 71,400

Budgeted Variable Overhead 65,000

Total Variable–Overhead Variance Birr 6,400 U

Variable Overhead Variance

What caused the company to spend Birr 6,400 more than the budgeted amount on variable

overhead? To discover the reasons behind this performance, the managerial accountant

computes the following variable overhead variances variable–overhead spending variance,

and variable–overhead efficiency variance.

Before we move in to the computation of these variances, carefully note the following

symbols:

AH = Actual hours (machine-hours in our case)

AR = Actual variable-overhand rate

SR = Standard variable-overhand rate

SH = Standard hours (machine hours in our case) allowed for actual output

1. Variable Overhead Spending Variance

The spending variance addresses the question, “How much should have been spent on

overhead, given the actual input?” It is a comparison of actual overhead with a flexible

budget based on actual hours.

To compute this variance, we use the formula given below:

SR

x

AH

OH

Variable

Actual

Variance

Spending

OH

Variable

Because actual variableoverhead is equal to actual hours (AH) times the actual variable

overhead rate (AR), the above formula could be rewritten as follows:

Variable−OH Spending Variance=[( AH x AR)−(AH x SR)]=AH x [ AR−SR]

Notice that the actual variable–overhead rate (AR) is computed using the formula giving

below.

AR=

Actual Variable OH

Actual Hours

The AR for the XYZ Carpenters Share Company is Birr 6.80 per machine hair as computed

below:

AR=

$71,400

10,500 Hours

=$6.80

Using the information at hand, let us now compute the variable-overheard spending

variance for the company.

Variable−OH Spending Variance=[ Actual Variable OH−(AH x SR)]

19 | P a g e

20.

Variable−OH Spending Variance=[$71,400−(10,500 x $6.80)]=$3,150 Unfavourable

You can also apply the other formula given above to compute variable-overheard spending

variance for the company as indicated below:

Variable−OH Spending Variance=[( AH x AR)−(AH x SR)]=AH x [ AR−SR]

Variable−OH Spending Variance=[(10,500 x $6.80)−(10,500 x $6.50)]=$3,150 U

The variable-overhead spending variance is unfavorable because the actual variable-

overhead cost exceeded the expected amount, after adjusting that expectation for the actual

number of machine hours used or worked. Notice that the Birr 6.50 standard variable

overhead rate was calculated in our previous discussions under the topic “Flexible overhead

budget”

2. Variable–Overhead Efficiency Variance

The efficiency variance measures the amount of overhead variance attributable to using

more or less inputs than allowed by the standards, given the amount of production. If

actual hours worked are fewer than standard hours, the efficiency variance is favorable. An

unfavorable variance occurs when actual hours exceed standard hours. To compute this

variance, we use the formula given below:

Variable−OH Efficiency Variance=[( AH x SR )−(SH x SR)]

XYZ Carpenter Share Company’s variable- overhead efficient variance for January is

computed as follows:

Variable−OH Efficiency Variance=[(10,500 x $6.80)−(10,000 x $6.50)]=$3,250 U

The above formula can be simplified by expressing it in factored from as follows:

Variable−OH Efficiency Variance=SR x [AH−SH]

The variable-overhead efficiency variance is unfavorable because actual machine hours

(10,500 hours) exceeded the standard allowed machine hours (10,000 hours) for the actual

output (2,500 tables) manufactured in January. Now carefully observe that, as shown

below, the total variable –overhead variance is the sum of the variable – overhead spending

and efficiency variances:

Variable–Overhead Spending Variance Birr 3,150 U

Variable–Overhead Efficiency Variance 3,250 U

Total Variable–Overhead Variance Birr 6,400 U

The variable–overhead spending variance measures the aggregate effect of differences

between the actual variable–overhead rate and the standard efficiency variance, in

contrast, measures the aggregate effect of differences between the actual activity base and

the standard activity base allowed for the actual out put achieved. Recall that the activity

base in the XYZ Carpenters Share Company problem is machine hours. A summary of

variable variances is presented in the table that follows. Notice, in this table, that “hours”

represent machine hours and rates per “hour” stand to indicate rates per machine hour.

20 | P a g e

21.

(a)

Actual variable

overhead-

(AH) x(AR)

10,500 x Birr6.80

Hours x per hour

Birr 71,400

(b)

Flexible Budget Based

on Actual Hours

(AH) x (SR)

10,500 x Birr6.50

= Birr 68,250

(c)

Flexible Budget Based on

Standard Hours

(SH) x (SR)

10,000 x Birr 6.50

= Birr 65,000

(d)

Variable OH Applied to

Work-In-Process

(SH) x (SR)

10,000 x Birr6.50

= Birr 65,000

Birr 3,150 U Birr 3,250U

No Difference

Variable OH

Spending Variance

Birr 6,400 U

Total Variable OH Variance

Variable OH

Efficiency Variance

Columns (a), (b), and (c) in the above table are used to compute the variances for cost-

control purposes. Column (d), in contrast, is not used to compute the variances. This last

column is included to point out that the flexible–budget amount for variable overhead (Birr

65,000) is the amount that will be applied to work in process inventory for product-

costing purposes. In brief, column (d) shows the variable overhead applied to work in

process for the product costing purpose.

What do the variable–overhead variances mean? What information do they convey to

management? Let us see the interpretations of the variable-overhead spending variance

and that of the variable–overhead efficiency variance in the discussion that follows.

3. Interpreting Variable-Overhead Spending variance

The variable overhead spending variance is useful only if the cost driver for variable

overhead really is the actual hours worked. Then the flexible budget based on the actual

hours worked is a valid benchmark that tells us how much should have been spent in total

on variable overhead items during the period. The actual overhead costs would be larger

than this benchmark, resulting in an unfavorable variance, if either:

(a) The variable overhead items cost more to purchase than the standards allow, or

(b) More variable overhead items were used than the standards allow.

So the spending variance includes both price and quantity variances. In principle, these

variances could be separately reported, but this is seldom done. Ordinary, the price element

21 | P a g e

22.

in this variancemay be small, so the variance will mainly be influenced by how efficiently

variable overhead resources such as production supplies are used.

In brief, an unfavorable spending variance simply means that the total actual cost of

variable overhead is greater than expected, after adjusting for the actual quantity of

machine hours used. An unfavorable spending variance could result from paying a higher

than expected price per unit for variable-overhead items, or the variance could result from

using more of the variable-overhead items than expected. Suppose for example, that

electricity were the only variable-overhead cost item. An unfavorable variable-overhead

spending variance could result from paying a higher than expected price per kilowatt-hour

for electricity, from using more than the expected amount of electricity, or from both.

4. Interpreting Variable-Overhead Efficiency Variance

Like the variable-overhead spending variance, the variable-overhead efficiency variance is

useful only if the cost driver for variable overhead really is the actual hours worked.

Then any increase in hours actually worked should result in additional variable overhead

costs. Consequently, if too many hours were used to produce the actual output, this is likely

to result in an increase in variable overhead. The variable-overhead efficiency variance is

an estimate of the effect on variable overhead costs of inefficiency in the use of the base

(i.e., hours). In a sense, the term variable-overhead efficiency variance is a misnomer.

It seems to suggest that it measures the efficiency with which variable overhead resources

were used while it does not. It is rather an estimate of the indirect effect on variable

overhead cost of inefficiency in the use of the activity base (machine hours in our case).

Notice from the discussions made earlier that the variable–-overhead efficiency variance is

a function of the difference between the actual hours worked and the hours that should

have been worked to produce the period’s actual output. If more hours are worked than are

allowed at standard, then the overhead efficiency variance will be unfavorable. However, as

discussed above, the efficiency is not in the use of overhead but rather in the use of the

base itself.

Exercise.1. In the XYZ Carpenters Share Company example, 500 more machine hours

(10,500 actual hours less 10,000 stand and hours) were used during January than should

have been used to produce the January’s actual output (2,500 tables). Each of these 500

more hours presumably required the incurrence of Birr 6.50 of variable overhead cost,

resulting in an unfavorable variance of Birr 3,250 (500 hours x Birr 6.50 = Birr 3,250).

Although this Birr 3,250 variance is called an overhead efficiency variance it could better be

called a machine-hours efficiency variance, since it results from using too many

machine–hours rather than from inefficient use of overhead resources.

Example

Item Actual Results Flexible Budget Amount

Out Put Units 10,000 10,000

Machine Hours 4,500 4,000

22 | P a g e

23.

Machine Hour PerOut

Put

0.45 0.40

VMOH Cost $130,500 $120,000

VMOH Cost/machine

hours

$29 $30

VMOH Cost/Out Put 13.05 12

Required: Compute the following VMOH Variance

VMOH Flexible Budget Variance

VMOH Efficiency Variance

VMOH Spending Variance

Fixed Overhead Variances

The process of analyzing the difference between standard and actual costs, called variance

analysis, can be applied to overhead costs just as we applied it to direct materials and

direct labor in the preceding parts. Direct materials and direct labor are variable costs only;

they contain no fixed component. On the other hand, overhead includes relatively large

amounts of fixed costs as well as some variable costs, making the analysis of overhead

variances somewhat more complicated. Without flexible budgets it is difficult to assess the

impact on overhead costs of activity levels that differ from the budgeted level. The purpose

of overhead variance analysis is the same as that of other types of variance analysis: to

determine how much actual results differ from expected outcomes and why the variance

occurred.

Examp. 2. To analyze performance with regard to fixed overhead, the managerial

accountant calculates fixed-overhead variances. The company’s total fixed-overhead

variance for January is computed below:

Actual Fixed Overhead Birr 43,800

Fixed Overhead Applied to Work-In–Process* 35,000

Total Fixed Overhead Variance Birr 8,800 U

*Applied Fixed OH = Predetermined Fixed OH Rate X Standard Allowed

hours

= Birr 3.50 X 10,000 machine hours = Birr 35,000

Notice that overhead has been applied to work in process on the basis of 10,000 standard

machine hours allowed for the actual output of January (2,500 tables) rather than on the

basis of 10,500 actual hours worked. This keeps unit costs from being affected by any

variations in efficiency. What caused the company to spend Birr 8,800 more than the fixed

overhead applied to work-in-process based on standard machine hours allowed for actual

output? To find out the reasons behind this performance, the management accountant

computes the following two variances for fixed overhead:

(a) A fixed–overhead budget variance, and

(b) A fixed–overhead volume variance.

1. Fixed-Overhead Budget Variance

23 | P a g e

24.

The budget varianceis the difference between the actual fixed overhead costs incurred

during the period and the budgeted fixed overhead costs as contained in the flexible

overhead budget. This variance, used by managers to control fixed overhead costs, and that

is computed by using the following formula:

Fixed−OH Budget Variance=[ Actual Variable OH Cost−Flexible Budget Fixed OH Cost]

XYZ Carpenters Share Company’s fixed-overhead budget variance for January is, applying

the formula given about, computed as follows:

Fixed−OH Budget Variance=[ Actual Variable OH Cost−Flexible Budget Fixed OH Cost]

Fixed−OH Budget Variance=[$ 43,800−$ 42,000]=$1,800 Unfavourable

2. Fixed-Overhead Volume Variance

The volume variance is a measure of utilization of plant facilities. The variance arises

whenever the standard hours allowed for the actual output of a period are different from

the dominator activity level that was planned when the period began. This variance can

be commuted using any one of the following two formulas:

Fixed OH Volume Variance=[Predeter mined FOH Rate(Denominators Hrs−Standard Hrs Allowed)]

Fixed OH Volume Variance=[Flexibe Budget FOH Cost−Applied FOH]

Let’s now compute the fixed –overhead volume variance for the XYZ Carpenters Share

Company’s problem, using the above two formulas.

Fixed OH Volume Variance=[Pr edeter mined FOH Rate(Denominators Hrs−S tandard Hrs Allowed)]

Fixed OH Volume Variance=[$ 3.50(12,000 Hrs−10,000 Hrs )]=$7,000 Unfaourable

Notice that, to compute the predetermined overhead rate for XYZ Carpenters Share

Company, 12,000 machine-hours per month was taken as planned activity when the

period began. Using this base, recall that, the predetermined fixed overhead rate was

computed to be Birr 3.50 per machine hour as follows:

Predetermined Fixed overhead rate =

Flexible budget fixed overhead cost

Denominator activity

=

$42,000

12,000 Hrs

=$3.50

The budgeted activity level for the moth (12,000 machine hours) is used as the denominator

activity in the formula for the predetermined overhead rate. These 12,000 machine hours

are what we called denominator hours in the formula for volume variance. In general,

the estimated total units in the base (machine hours, direct-labor hours, etc.) in the formula

for the predetermined overhead rate are the denominator activity. Once an estimated

activity level (denominator activity) has been chosen, it remains unchanged throughout the

year even if the actual activity turns out to be different from what was estimated. The

reason for not changing the denominator is to maintain stability in the amount of overhead

applied to each unit of product regardless of when it is produced during the year.

24 | P a g e

25.

Birr 8,800 unfavorable

TotalFixed–OH variance

Actual Fixed OH Cost

Birr 43,800

Flexible Budget

Fixed OHCost

Birr 42,000

Fixed OHCost Applied to Work-In-Process10,000 standard hours X Birr 3.50 per hours

= Birr 35,000

Birr 1,800 Unfavorable

Fixed–OH

Budget variance

Birr 7,000 Unfavorable

Fixed– OH

Volume variance

U

Recall that 10,000 machine hours represent the standard hours allowed for actual output of

January (2,500 tables) at 4 standard machine hours per table. You can as well arrive at the

same result of fixed overhead volume variance applying the second formula as shown below:

Fixed OH Volume Variance=[$ 42,000−$35,000]=$7,000 Unfavourable

Now carefully observe that, as shown blow, the total fixed-overhead variance is the sum of

the fixed-overhead budget and volume variances:

Fixed-Overhead Budget Variance Birr 1,800 U

Fixed–Overhead Volume Variance 4,000 U

Total Fixed Overhead Variance Birr 8,800 U

A summary of fixed–overhead variance is presented in the table that follows.

The fixed–Overhead variances convey useful information to management. Let’s see, in the

discussion that follows, at the interpretation of these variances.

3. Interpreting Fixed–Overhead Budget Variance

The budget variance is the real control variance for fixed overhead, because it compares

actual expenditures with budgeted fixed – overhead costs. The budget variances for fixed

overhead can be very useful, since they represent the difference between how much should

have been spent (according to the flexible overhead budget) and how much was actually

spent. An unfavorable fixed – overhead budget variance calls for an explanation of why it

happened. If, for instance, the production supervisor’s salary shows an unfavorable budget

variance, it could be due to many reasons. The reasons could be an increase in salaries,

overtime work, or another supervisor could have been hired. Proper explanation should be

given as to why another supervisor was hired, if this was not included in the budget when

activity for the period was planned. In brief, the fixed – overhead budget variance for XYZ

Carpenters Share Company’s problem is unfavorable, because the company spent

25 | P a g e

26.

morethan the budgetedamount of fixed overhead. Notice that an activity level to

determine budgeted fixed overhead needs no specification. This is so because all the three

columns in the columnar flexible budget prepared earlier specify Birr 42,000 as budgeted

fixed overhead per month.

4. Interpreting Fixed–Overhead Volume Variance

It has been stated earlier that the volume variance is a measure of utilization of available

plant facilities. An unfavorable variance, as you have seen in our computations, means that

the company operated at an activity level below that planned for the period. A favorable

variance would, on the other head, mean that the company operated at an activity level

greater than that planned for the period. It is important to note that the volume variance

does not measure over–orunder–spending. Accompany would normally incur the same

Birr amount of fixed overhead cost regardless of whether the period’s activity was above or

below the planned (denominator) level of activity. In short, the volume variance is an

activity–related variance. It is explainable only by activity and is controllable only thought

activity. The following three points could summarize the fixed– overhead volume variances:

(a) If the denominator activity (12,000 machine hours in our case) and the standard

hours allowed for the actual output of the period are the same, then there is no

volume variance.

(b) If the denominator activity is greater than the standard hours allowed for actual

output of the period, then the volume variance is unfavorable. This indicates an

underutilization of available facilities.

(c) If the denominator activity is less than the standard hours allowed for the actual

output of the period, then the volume variance is favorable. This indicates a

higher utilization of available faculties than was planned.

Example

1. VMOH is allocated products using direct marketing labour hours per out put.

FMOH is allocated to product on a perout put basis.

2. budgeted amount for the period are

(a) Direct marketing labour hours 0.25 hours per out put.

(b) Variable marketing overhead rate $20 per direct marketing labour hours.

(c) Fixed marketing Over Head: $434,000

(d) Out put which is used as denominator level is equal to 12,000 out put (Budgeted

Out Put)

3. Actual Results for the period are:

(a) Fixed Marketing Over Head: $420,000

(b) Variable Marketing Over Head: $47,700

(c) Direct Marketing Labour Hours:2,304

(d) Actual Out Put: 10,000 units

Required: Compute the following MOH Variances

Variable Marketing Over Head Variance

26 | P a g e

27.

Fixed MarketingOver Head Variance

Prepare the necessary journal entries

CHAPTER THREE

VARIANCE: MIX, YIELD AND INVESTIGATION

Direct Material Yield Variance

27 | P a g e

28.

Material yieldvariance is the portion of material usage variance which is due to the

difference between standard yield specified and actual yield obtained.

One important feature of yield variance which differentiates it from other material

variances (price, usage and mix variance) is that yield is an out put variances which

others are input variance.

Its formula is as follows:

Direct Materials Mix variance

The DM mix variance is defined as the portion of the material usage variance which is

due to the difference between standard and actual composition of materials.

Its formula is as follows:

- X X

Example: The RAM Corporation makes tomatoes ketch up produce ketchup of the desired

consistency, color& taste, RAM mixes three types of tomatoes such as Latoms, caltoms and

flotoms. RAM`s production standards required 1.6 tones of tomatoes to produce 1 tone of

ketch up, with 50% of the tomatoes being latom, 30% caltoms and 20% flotoms.

The direct materials input standards to produce one tones of ketch up are

0.8 (50% X 1.6) tones of latoms at $70 per ton = $ 56.00 (0.5 X 70 X1.6)

0.48 (30% X 1.6) tone of catoms at $ 80 per ton = $ 38.40

0.32 (20% X 1.6) tone of flotoms at $ 90 per tone = $ 28.80

Total Standard cost of 1.6 tomatoes……………...= $ 123.20

Budgeted cost per tone of tomatoes is

($ 123.20

1.6 tone

= $ 77)

Actual result show that a total of 6.500 tone of tomatoes were used to produce 4,000 tone of

ketch up”

3,250 tons of latoms at actual cost of $ 70 per tone = $227,500

2,275 tone of catoms at actual cost of $ 82 per tone = $186,550

975 tone Flotoms at actual cost of $ 96 per tone = $93,600

6500 tones of tomatoes $507,650

28 | P a g e

Direct Material

Yield variance =

for each input

Actual Quantity of all

direct Material input-

used

Budgeted total

quantity of all

DM input allowed X

for actual out put

achieved

Budgeted

DM input

%age

Direct Material

Mix variance =

for each input

Actual Quantity of

all direct Material

input %age

Budgeted

DM input

%age

Budgeted

price of DM

input

Actual

Quantity

of all

direct

Material

inputuse

d

Budgeted

price of

DM input

29.

Required: From theabove data compute

1. FBV of direct Material

2. Price Variance of direct Material

3. Efficiency Variance of Direct Material (DMMV + DMYV)

4. Direct Material Mix Variance (DMMV)

5. Direct Material Yield variance (DMYV)

Solution

4) DM Mix Variance

L = (50% - 50%) X 6500 X $70 = 0

C = (35% - 30%) X 6500 X $80 = 26,000 (U)

F = (15% - 20%) X 6500X $90 = 29,250 (F)

Total Material Mix Variance = $3250 (F)

5) Direct Material Yield Variance

L = (6500 – (1.6 x 4000) ) X 50% x $70 = $3,500 (U)

C = (6500 – 6400) X 30% x $80 = $2400(U)

F = (6500 – 6400) X 20% x $90 = $1800(U)

Total DM yield variance = $7700(U)

1) Flexible budget variance

Actual X actual Actual X Budgeted budgeted

Input price input price input allowed X budgeted price

For actual out

Put

Total Flexible Budget Variance

= $3,500 /U/ + $32,950/U/ + $21,600 /F/ = $14,850 /U/

2) Price Variance

L = ($ 70 – 70) X 3250 = 0

C = ($ 82 – 80) X 2275 = $ 4550 /U/

F = ($ 96 – 90) X 975 = $ 5850 /U/

$10400 /U/

3) Efficiency Variance

L = (3250 - 0.8 (4000) X $ 70 = $ 3500 /U/

C = (2275 - 0.48 (4000) X $ 80 = $ 28,400 /U/

F = (975 - 0.32 (4000) X $ 90 = $ 27,450 /F/

$ 4450 /U/

FBV = PV + EV

= $ 10 400 /U/ + $ 4450 /U/ = $14,850 /U/

Mix Variance Interpretation

29 | P a g e

30.

The favorable totalDM mix variance occurs because the average budgeted cost per tone of

tomatoes in the actual mix is less than the average budgeted cost per tone tomatoes in the

budget mix. i.e.497,250

6,500

Less than 500,500 = (76.5 – 77) X 6,500 = 3,250 |F|

6500

Yield variance interpretation

The total DM yield variance is unfavorable, because the Delpino Corporation uses 6500

tones if tomatoes rather than the 6400 tones, i.e. should have been used to produce 4000

tones of ketch up. The unfavorable yield variance represents the budgeted cost of using 100

more tones of tomatoes, (6,500 – 6400) x 77= 7700(U)

Direct Mfg Labour yield & Mix Variance

DIRECT MFG LABOUR YIELD VARIANCE

This variance is quite similar to material yield variance. This variance also reveals the

effect on labour cost of actual out put or yield being more or less than the standard yield.

Its formula is as follows:

=

DIRECT MFG LABOUR MIX VARIANCE

This variance is similar to material mix variance. It arises only when more than one

grade of workers is employed and the composition of actual grade of workers differs

from those specified.

Its formula is as follows:

=

30 | P a g e

Actual total

Quantity of

All direct __

Manufacturing

Labour inputs used

Budgeted total

Quantity of all

Direct mfg

labour inputs X

Allowed for

Actual out

Put achieved

Budgeted direct

Mfg labour X

input

Mix % age

Budgeted

Price of

direct Mfg

Labour

inputs

actual

Actual direct

Mfg labour __

Input

Mix %age

Budgeted direct

Mfg labour X

input

Mix % age

Budgeted

price of

direct mfg

labour input

Actual total

quantity of all X

mfg labour

Input used

Direct Mfg

Labour Yield

Variance for

Each input

Direct Mfg

Labour Mix

Variance for

Each input

31.

Example: RAM Corporationhas three grades of direct mfg labour:

Grade 1, Grade 2 & Grade 3

Budgeted cost for the period in as follows:

3000 hrs of grade 3 labour at $24 per hour…………. $72,000

2100hrs of grade 2 labour at $ 16 per hour……...….. $33,600

900hrs of grade 1 labour at $12 per hour………….. $10,800

6000 Total hours $116,400

Actual results for the period show that the work was completed in 5,900 hours.

3,245 hours of grade 3 labour at $23 per hour…………$74,635

1,770 hours of grade 2 labour at $18 per hour…………$31,860

885 hours of grade 1 labour at $13 per hour…………$11,505

5900 Total hours $118,000

Required: Compute (1) - FBV of direct labour

(2) - price variance of direct labour

(3) - efficiency variance of direct labour

(4) - Direct labour mix variance

(5) - Direct labour yield variance

SOLUTION

(1) Flexible budget Variance of Direct Labour

G3 = $74,635 -$72,000 = $2,365 (U)

G2 = $31,830 -$33,000 = $1,740 (F)

G1 = $11,505 -$10,800 = $705 (U)

Total FBV $1,600(U)

(2) Price Variance of Direct Labour

G3 = ($23 -$24) X 3,245 = $3,245 (F)

G2 = ($18 -$16) X 1,770= $3,540 (U)

G1 = ($13 -$12) X 885 = $885 (U)

Total PV $1,180(U)

(3) Efficiency Variance of Direct Labour

G3 = (3,245 – 3,200) X $24 = $5,880 (U)

G2 = (1,770 – 2,100) X $16= $5,280 (F)

G1 = (885 – 900) X$12 = $180 (F)

Total EV $420(U)

(4) Direct Labour Mix Variance

G3= (0.55 – 0.5) X 5900 x $24 = $7080(U)

G2= (0.3 - 0.35) X 5900 x $16 = $4720(F)

G1= (0.15 – 0.15) X 5900 x $12 = $ 0

Total DL Mix Variance = $2,360 (U)

(5) Direct manufacturing labour yield variance

G3 = (5,900 – 6000) x 0.5 x $24 = $1,200(F)

31 | P a g e

32.

G2 = (5900– 6000) x 0.35 x $16 =$560(F)

G1 = (5900 – 6000) x 0.15 x $12 =$180(F)

D. mfg labour yield variance= $1940 (F)

INTERPRETATION

The unfavorable mix variance occurs because a greater proportion of works was done by the

more costly grade three labours. As a result of the change in mix, the average budgeted cost

per direct mfg labour hour in the actual mix was higher than the average budgeted cost per

direct mfg labour hour in the budget mix

(116,820

5900

>

114,460

5900 )(19.8 – 19.4) X 5,900 =

$2360

The favorable yield variance indicates that the work was completed faster in 5,900 actual

total hours compared with 6000 budgeted total hours. Perhaps this result is due to the

extra time spent by grade 3 labour.

SALES VARIANCE

Sales volume variance

Volume refers to the number of physical units.

SVV refers the portion of the sales value variance which is due to the change

between the actual volume and standard volume sales.

Its formula is as follows:

SVV = (Actual Quantity – Budgeted Quantity) X Standard Price

Sales Quantity and Mix Variance

Sales Mix Variance

When a company is selling more than one types of products, a budget will be prepared to

show the budgeted sales of each product. If actual sales of different products are not the

same proportion as budgeted, a sales mix variance will arise.

Sales mix variance is “the portion of sales volume variance which is due to the

difference between the standard and the actual inter relation ship of the quantity of

each product group of which sales are composed.”

Sales mix variance

This variance indicates the effect on profit of changing the mix of actual sales from the standard

mix.

It can be calculated in one of two ways.

The difference between the actual total quantity sold in the standard mix and the actual

quantities sold, valued at the standard margin per unit.

The difference between actual sales and budgeted sales, valued at (standard profit per unit

– budgeted weighted average profit per unit

32 | P a g e

33.

Its formulais as follows:

Sales Quantity Variance

This variance indicates the effect on profit of selling a different total quantity from the budgeted

total quantity.

It can be calculated in one of two ways.

The difference between actual sales volume in the standard mix and budgeted sales

valued at the standard margin per unit.

The difference between actual sales volume and budgeted sales valued at the budgeted

weighted average profit per unit.

KEY.

With all variance calculations, from the most basic (such as variable cost

variances) to the more complex (such as mix and yield / mix and quantity

variances), it is vital that you do not simply learn formulae. You must

understand what your calculations are supposed are supposed to show.

Its formula is as follows:

Example: Global air operator flights between New York & London. It has three class of

service; first class, business class & economics class. Unit volume is measured in terms of a

round trip ticket.

Budgeted amount for the period are as follows:

USP Unit volume Mix Revenue

First class $ 3200 1,000 5 % 3.2 m

33 | P a g e

Sales mix

variance =

Of revenues

Sales quantity

variance =

Of revenues

Actual unit

of all X

Product sold

Actual sales

Mix % __

age

Budgeted

Sales mix X

% age

Budgeted

Selling

Price per unit

Sales

mix

Budgeted

Unit of all X

product sold

Actual unit

Of all __

Product sold

Budgeted

Sales mix X

% age

Budgeted

Selling

Price per unit

34.

Business class $2400 3,000 15 % 7.2 m

Economic class $ 900 16,00080 %14.4 m

Total 20,000100%$ 24.8 m

Actual results for the period are as follows:

USPUnit volume Mix Revenue

First class 2,600 2,400 10% $6.24m

Business class 1,600 6,000 25% $9.6m

Economic class 70 15,60065%$10.92m

Total 24,000100%$26.76m

Required

1) Static budget variance = $1.96m (F)

2) FBV = 9.36m (U)

SVV = 11.32m (U)

3) Sales mix variance

4) Sales quantity variance

Solution

3) FC = 24,000 (10% - 5%) X 3,200 = 3.84m (F)

BC = 24,000 (25% - 15%) X 2,400 = 5.76m (F)

EC = 24,000 (65% - 80%) X 9,00 = 3.24m (U)

$ 6.36m (F)

Interpretation

A favorable sales mix variances arises at the individual product level when the actual sales

mix %age exceeds the budgeted sales mix % age (first class & BC). In constant economic

class has an unfavorable variance.

4) Sales quantity variance (SQV)

FC = (24,000 – 20,000) X 5% x $3,200 = $ 0.64m (F)

BC = (24,000 – 20,000) X 15% x $2400 = $1.44m (F)

EC = (24,000 – 20,000) X 80% x $900 = $ 2.88m (F)

$4.96m (F)

Interprétation

This variance is favorable when the actual unit of product sold exceeds the budget units of

product sold. Global sold 4000 more round trip ticket than was budgeted. Hence, its sales

quantity variance for revenue is favorable.

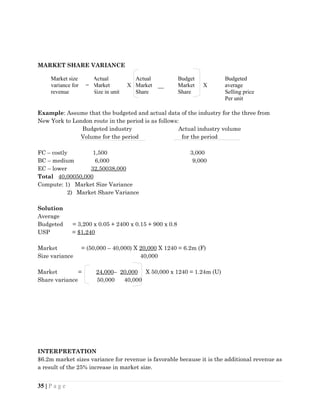

MARKET SIZE VARIANCE

34 | P a g e

Market size

variance in =

revenue

Actual

Market __

Size in unit

Budget

Market X

Share

Budgeted

average

Selling price

Per unit

Budgeted

Market X

Size in

unit

35.

MARKET SHARE VARIANCE

Example:Assume that the budgeted and actual data of the industry for the three from

New York to London route in the period is as follows:

Budgeted industry Actual industry volume

Volume for the period for the period

FC – costly 1,500 3,000

BC – medium 6,000 9,000

EC – lower 32,50038,000

Total 40,00050,000

Compute: 1) Market Size Variance

2) Market Share Variance

Solution

Average

Budgeted = 3,200 x 0.05 + 2400 x 0.15 + 900 x 0.8

USP = $1,240

Market = (50,000 – 40,000) X 20,000 X 1240 = 6.2m (F)

Size variance 40,000

Market = 24,000– 20,000 X 50,000 x 1240 = 1.24m (U)

Share variance 50,000 40,000

INTERPRETATION

$6.2m market sizes variance for revenue is favorable because it is the additional revenue as

a result of the 25% increase in market size.

35 | P a g e

Actual

Market X

Size in unit

Actual

Market __

Share

Budget

Market X

Share

Market size

variance for =

revenue

Budgeted

average

Selling price

Per unit

36.

$1.24m unfavorable variancehighlights the revenue impact of these two percentage point

decline in market share

SBV

$1,960,000(F)

FBV SVV