Download to read offline

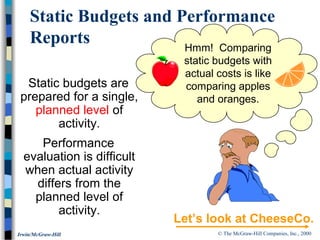

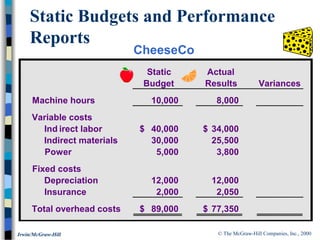

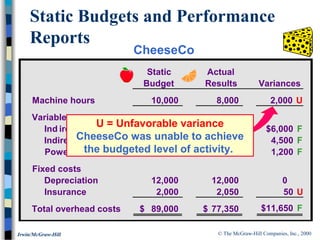

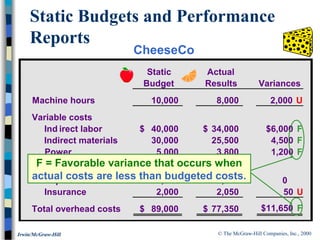

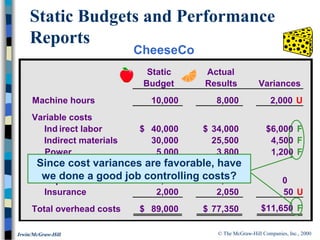

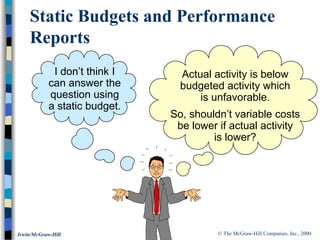

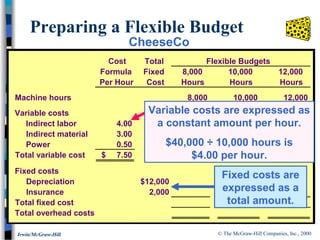

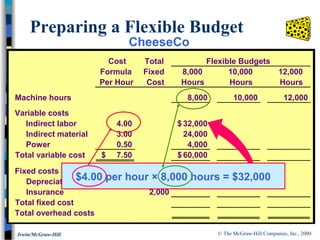

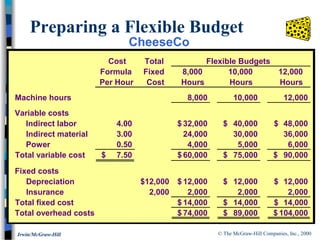

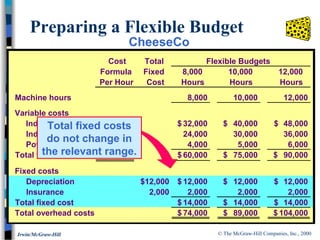

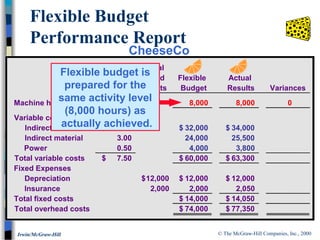

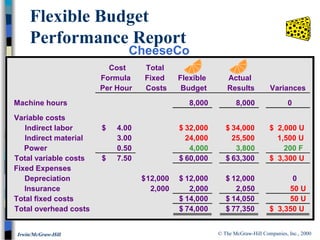

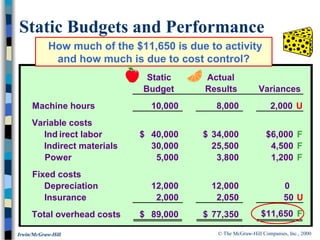

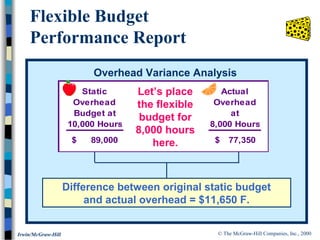

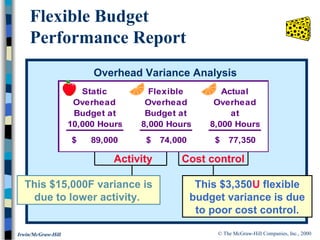

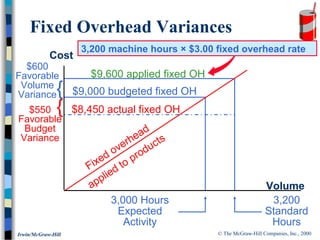

- The document discusses static and flexible budgets and how flexible budgets improve performance evaluation by accounting for actual activity levels. - It provides an example of CheeseCo's static budget analysis which shows favorable cost variances but does not indicate whether good cost control or lower activity caused the variance. - To determine this, a flexible budget is created for CheeseCo's actual activity level of 8,000 machine hours. This reveals an unfavorable cost control variance of $3,350, indicating costs were not well controlled.