Downloaded 170 times

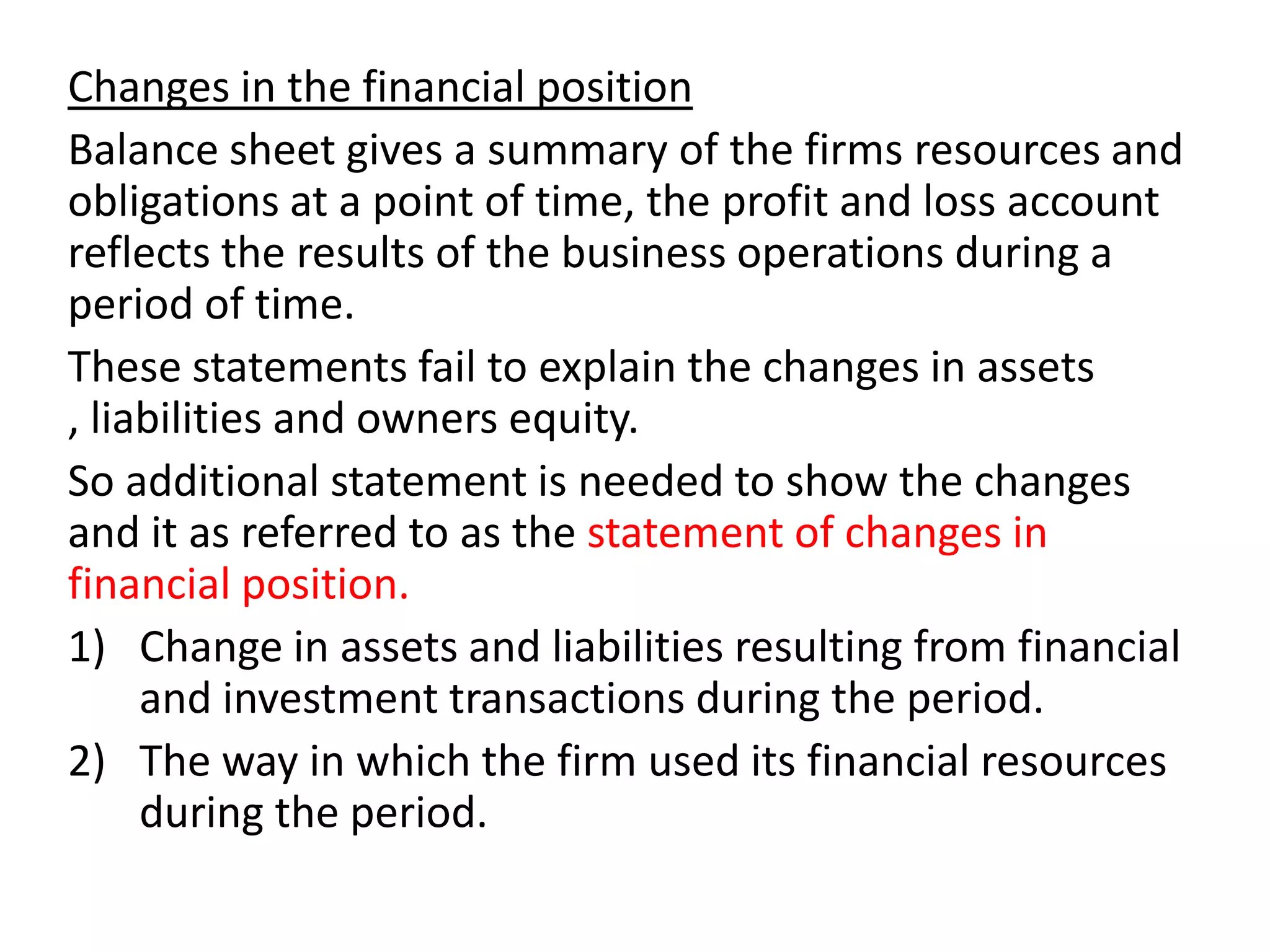

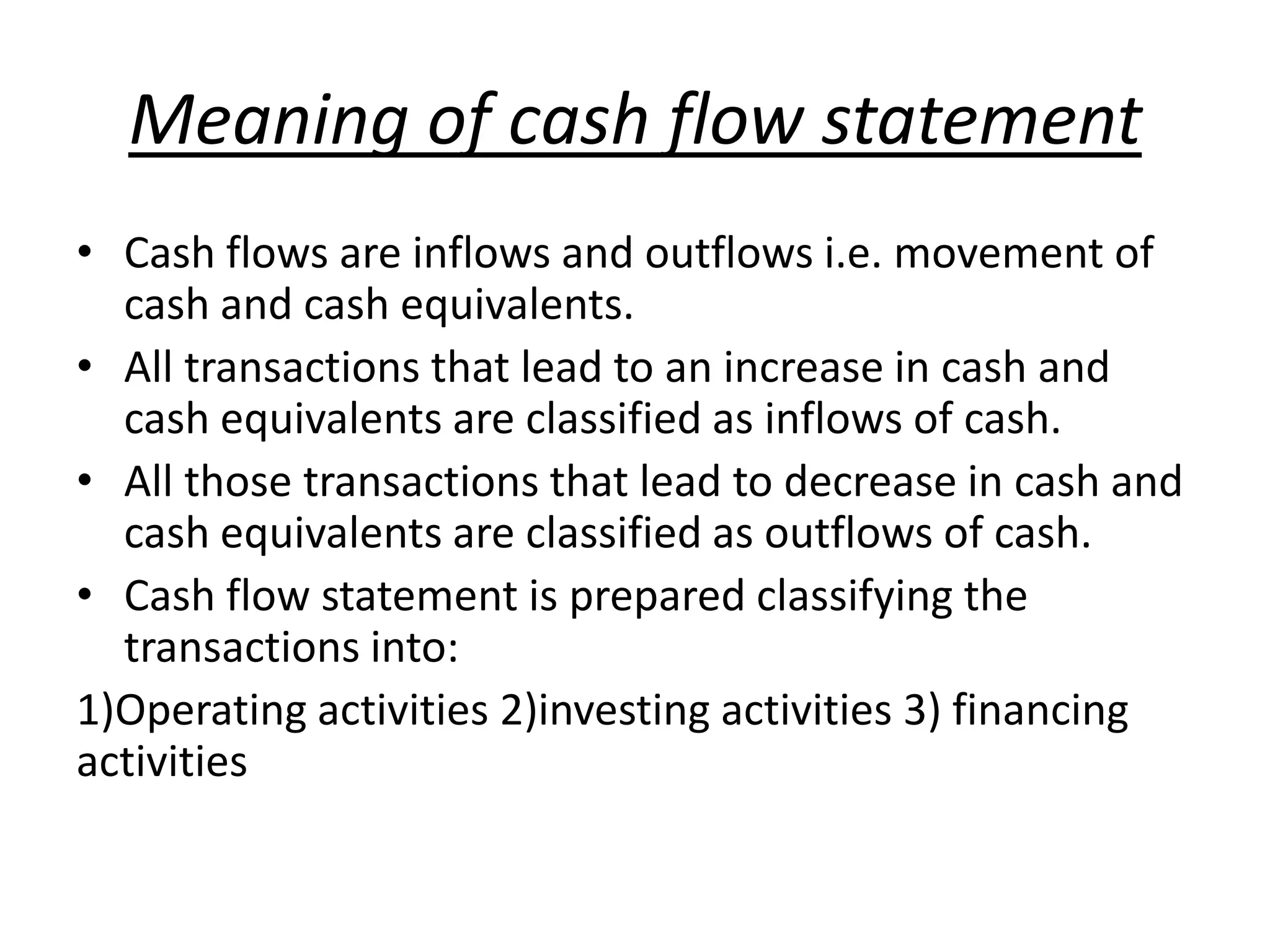

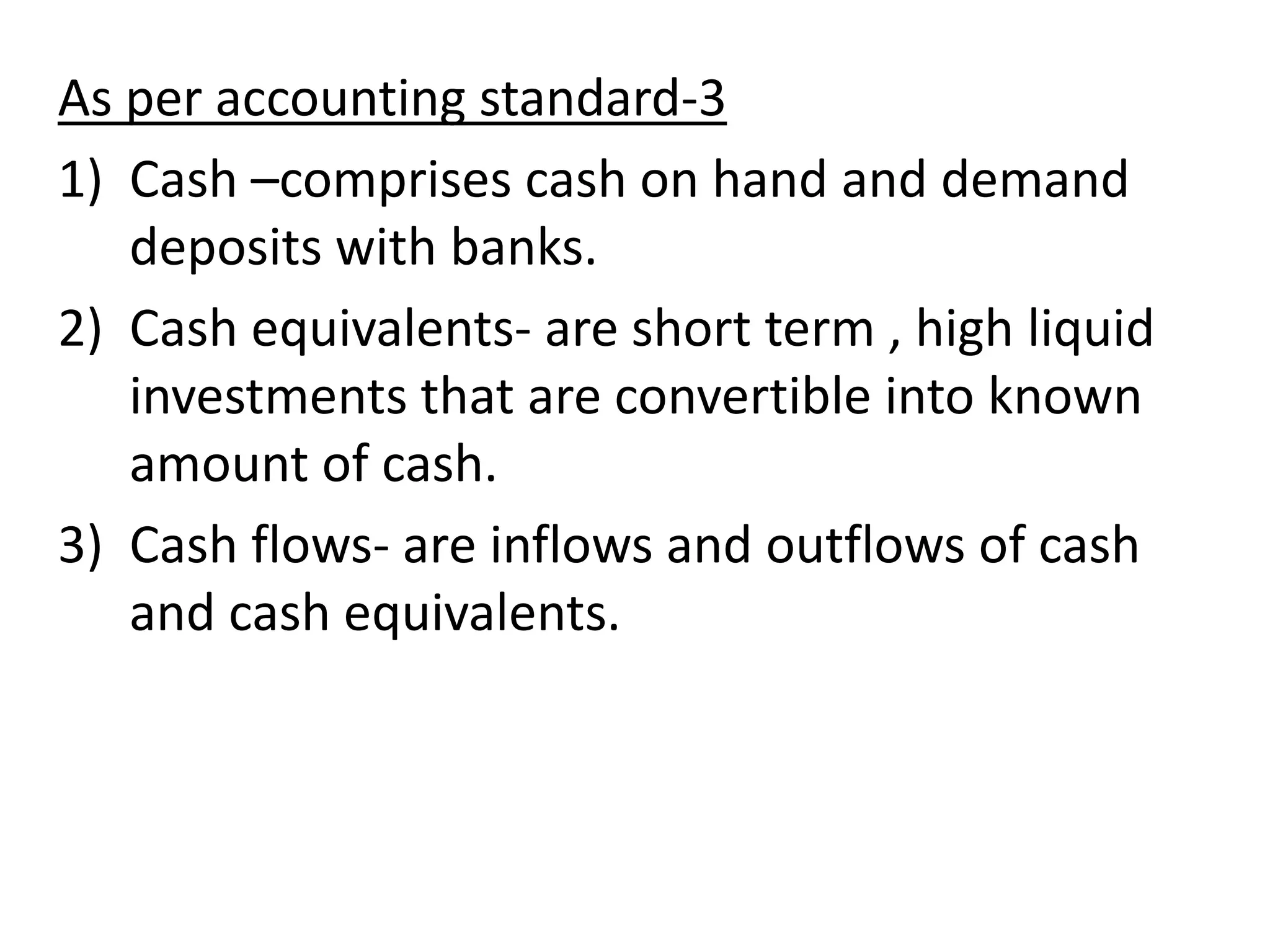

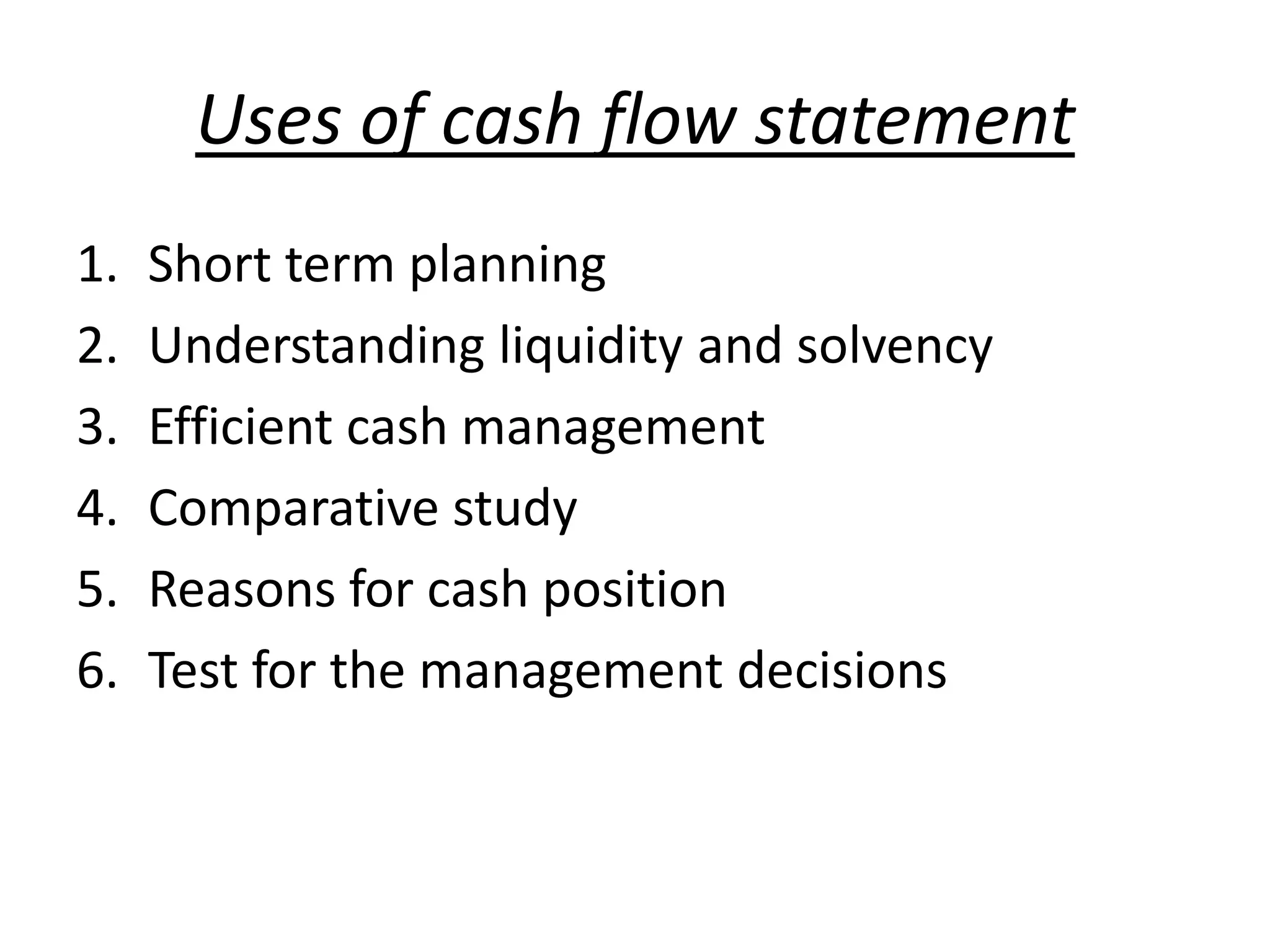

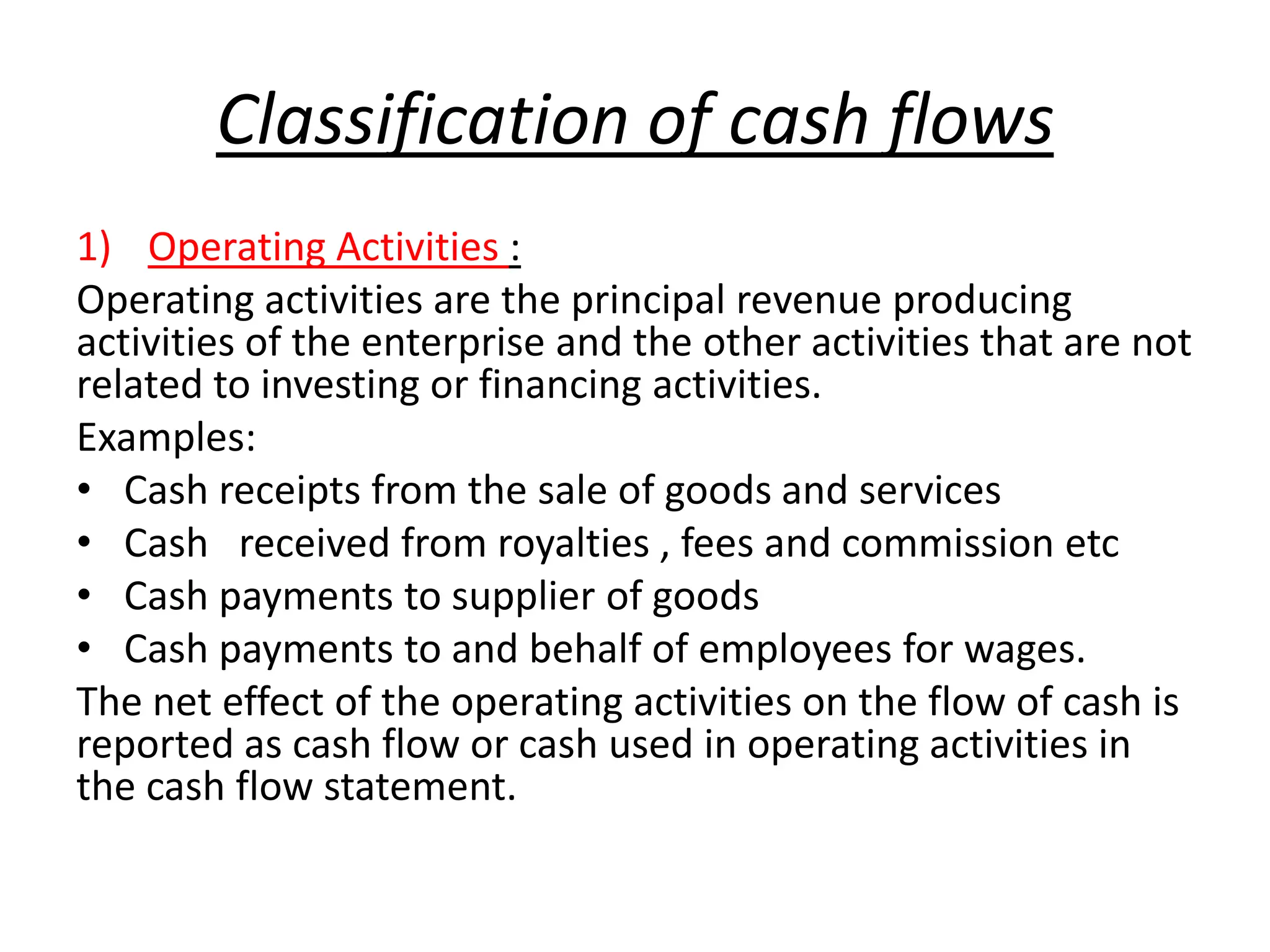

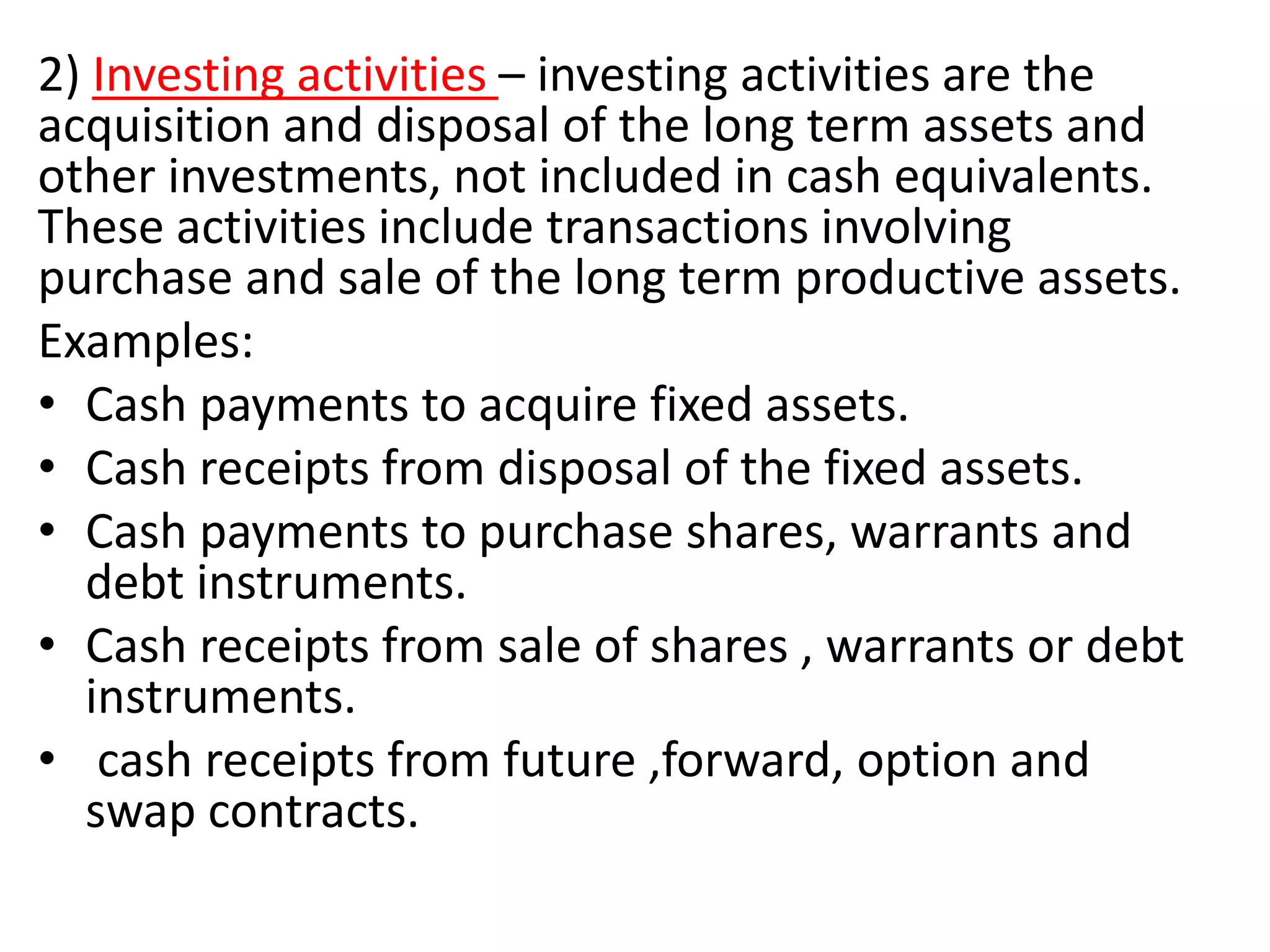

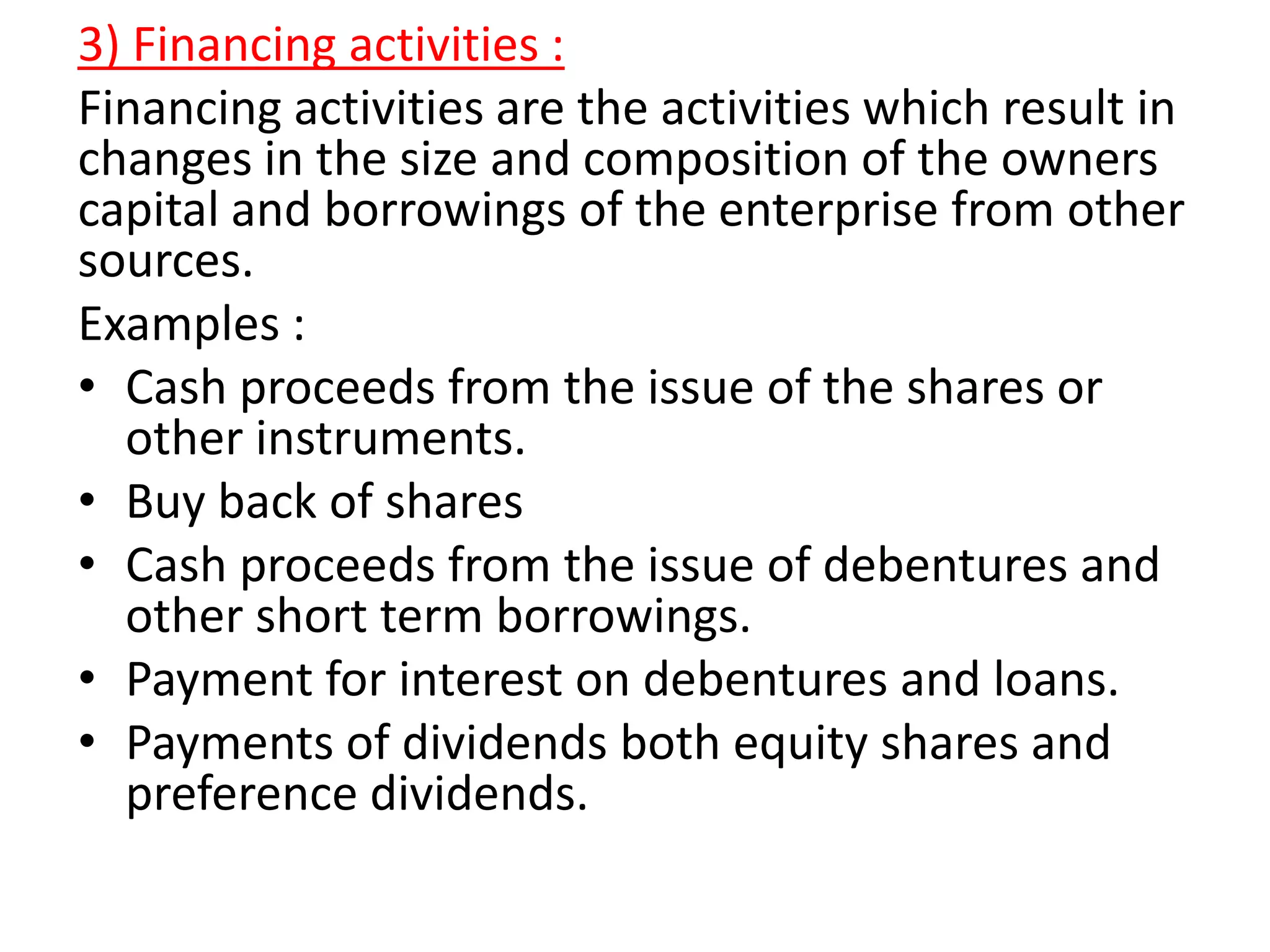

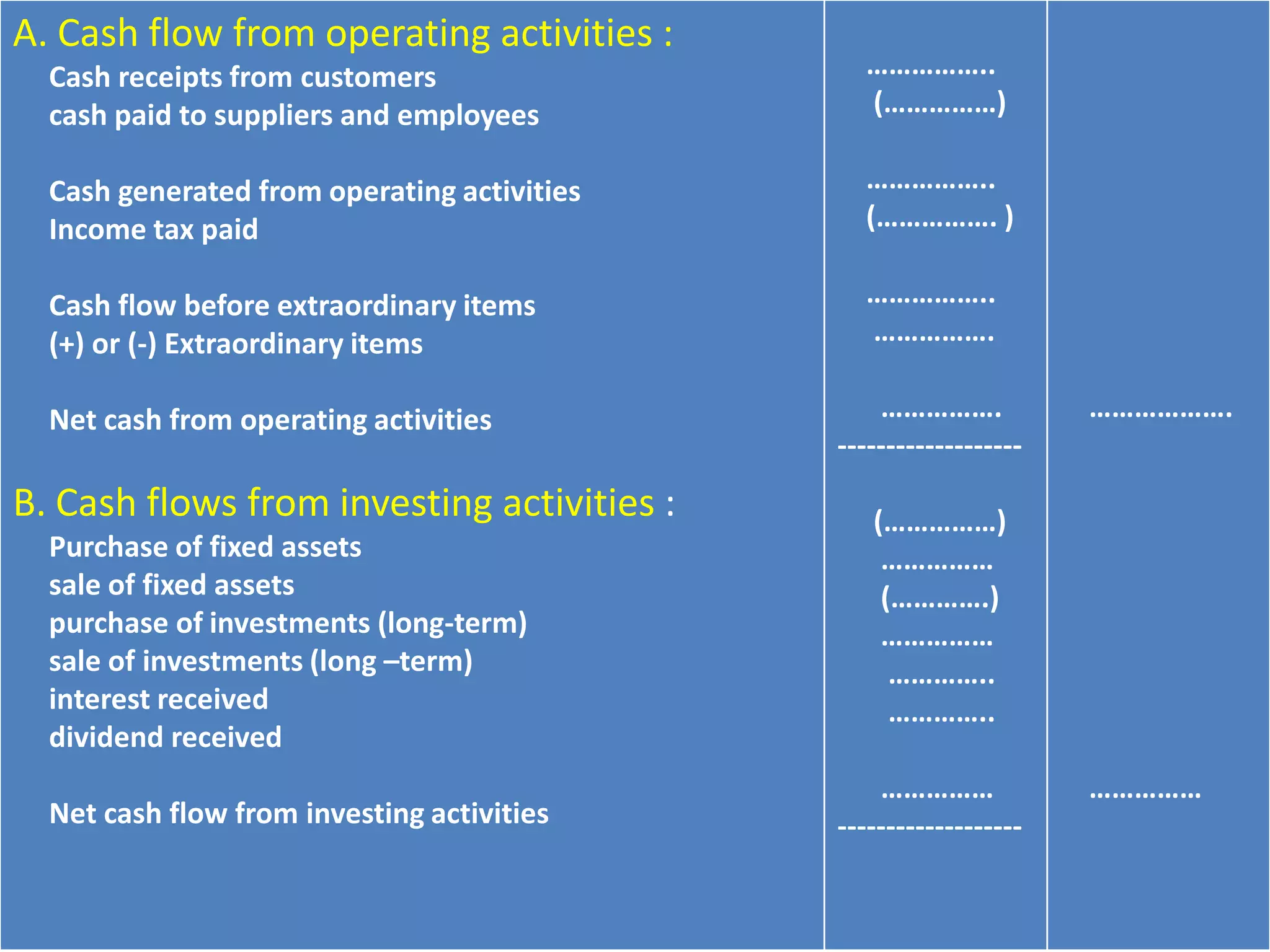

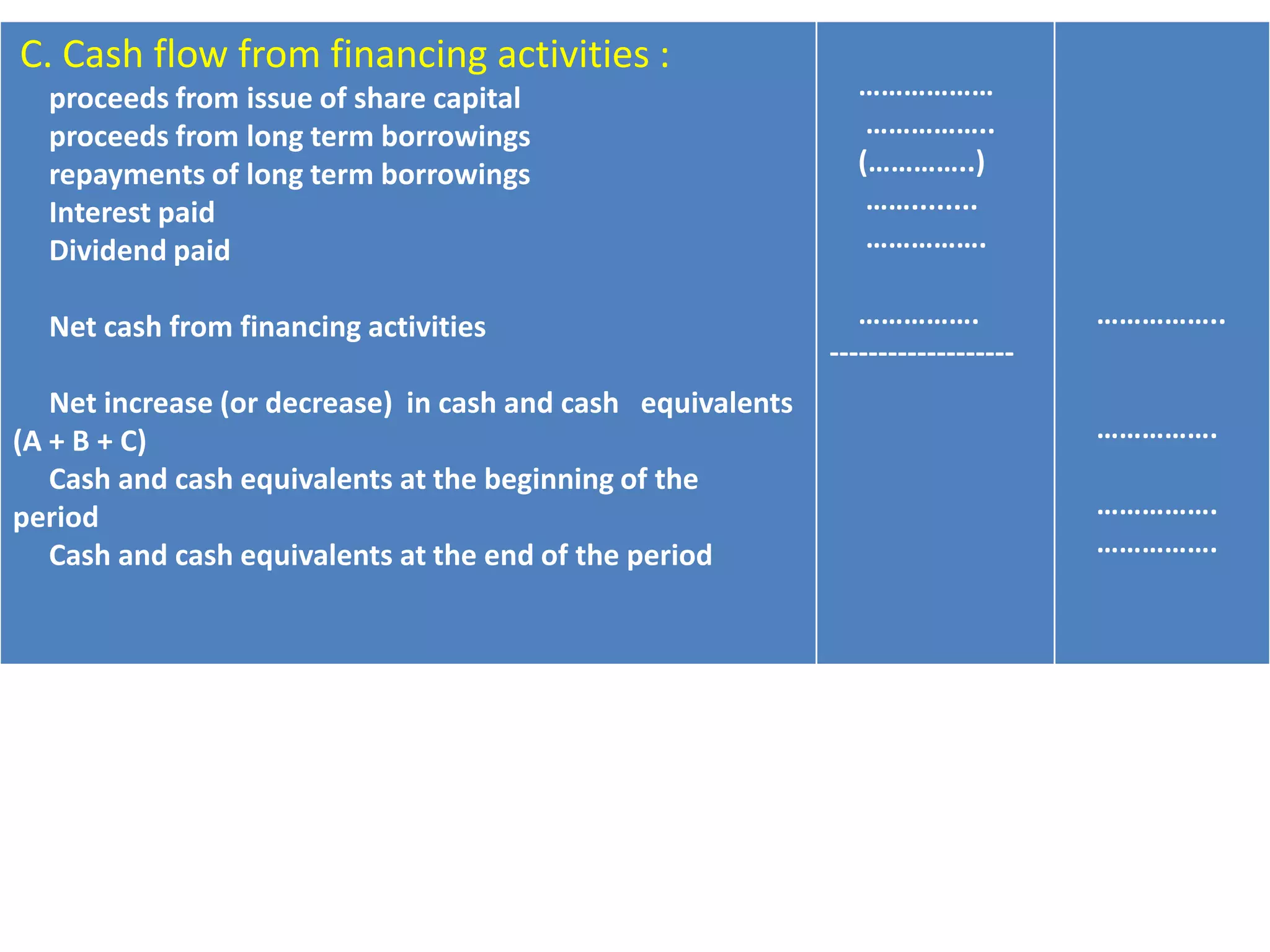

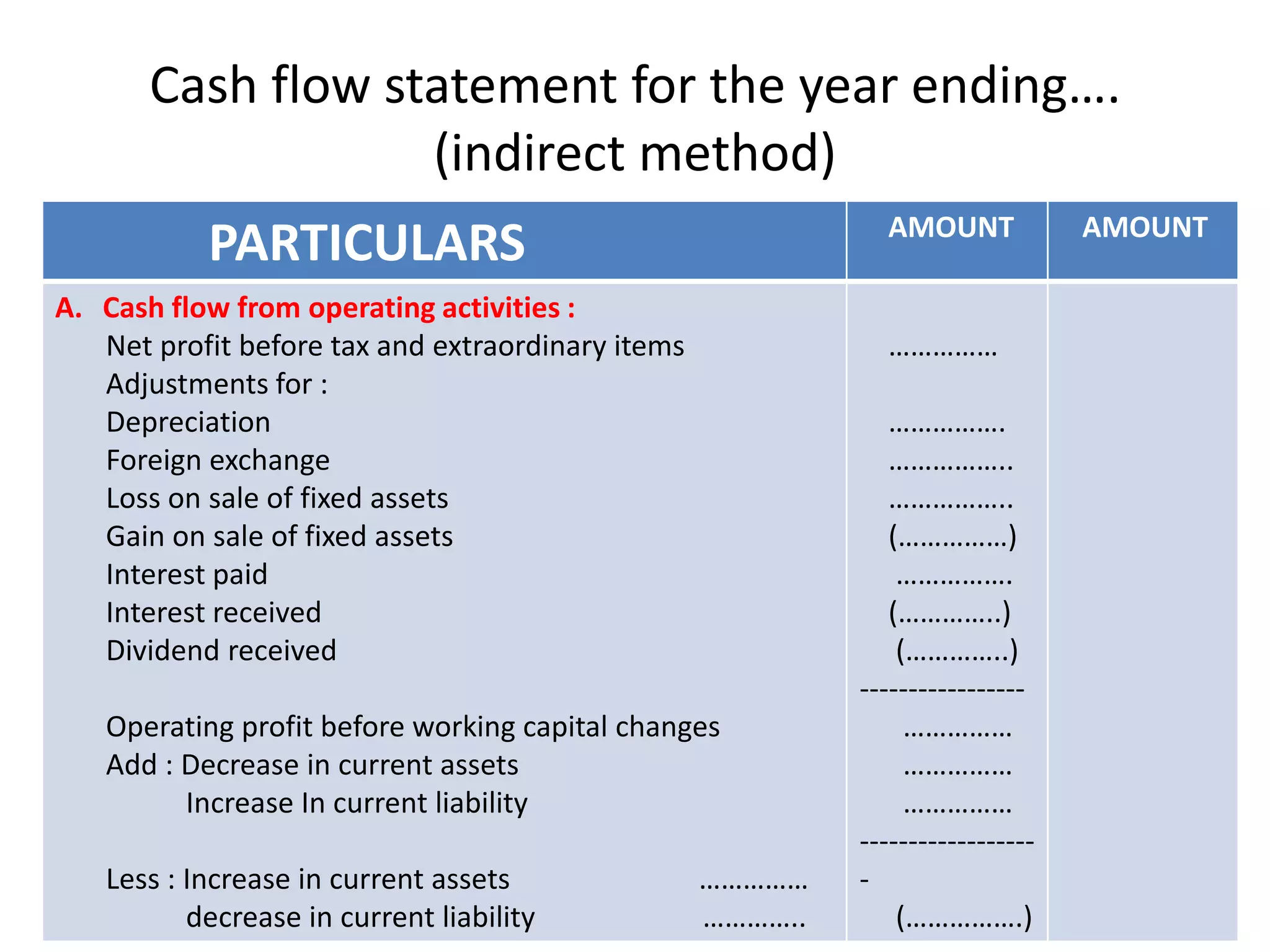

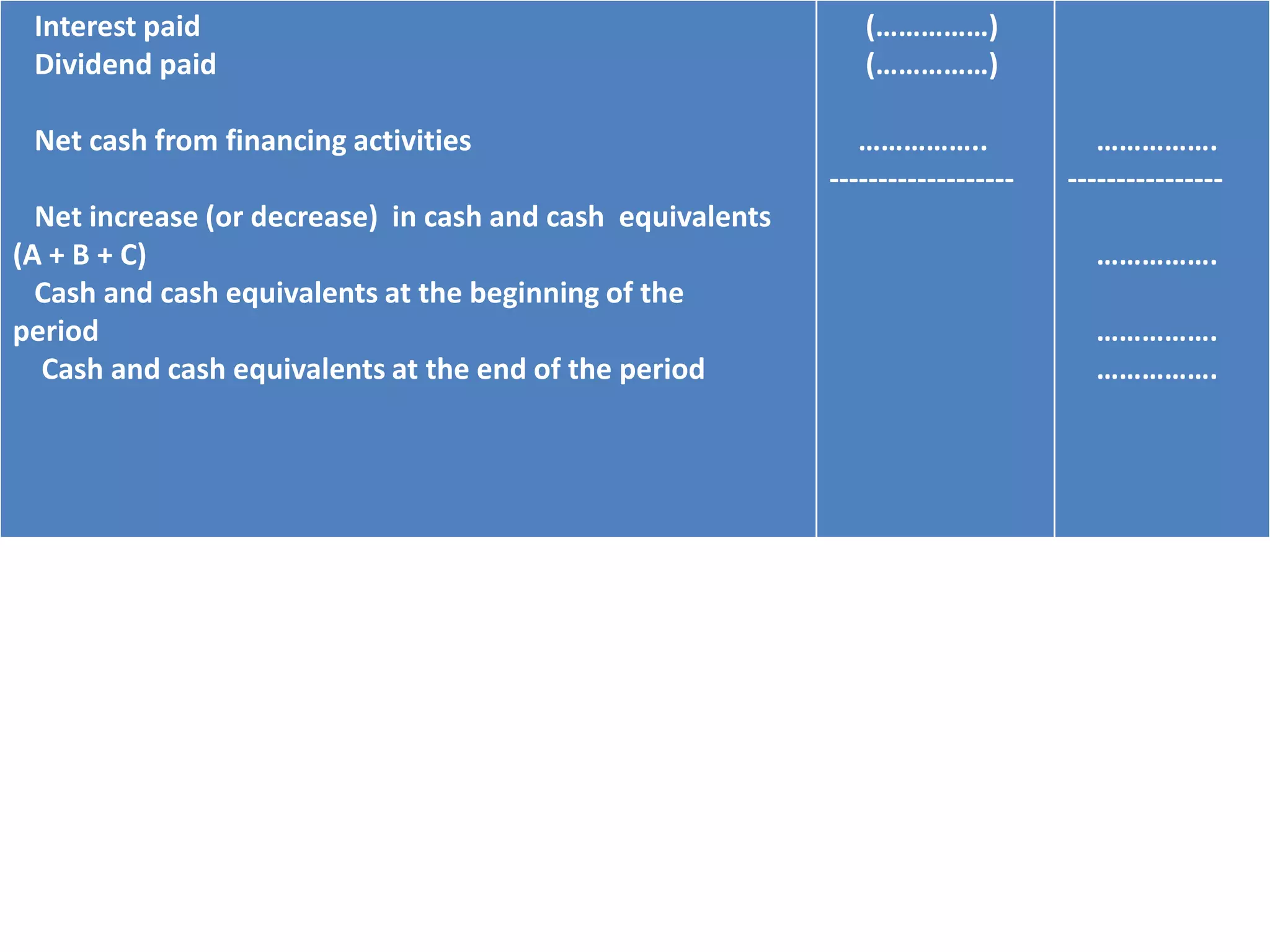

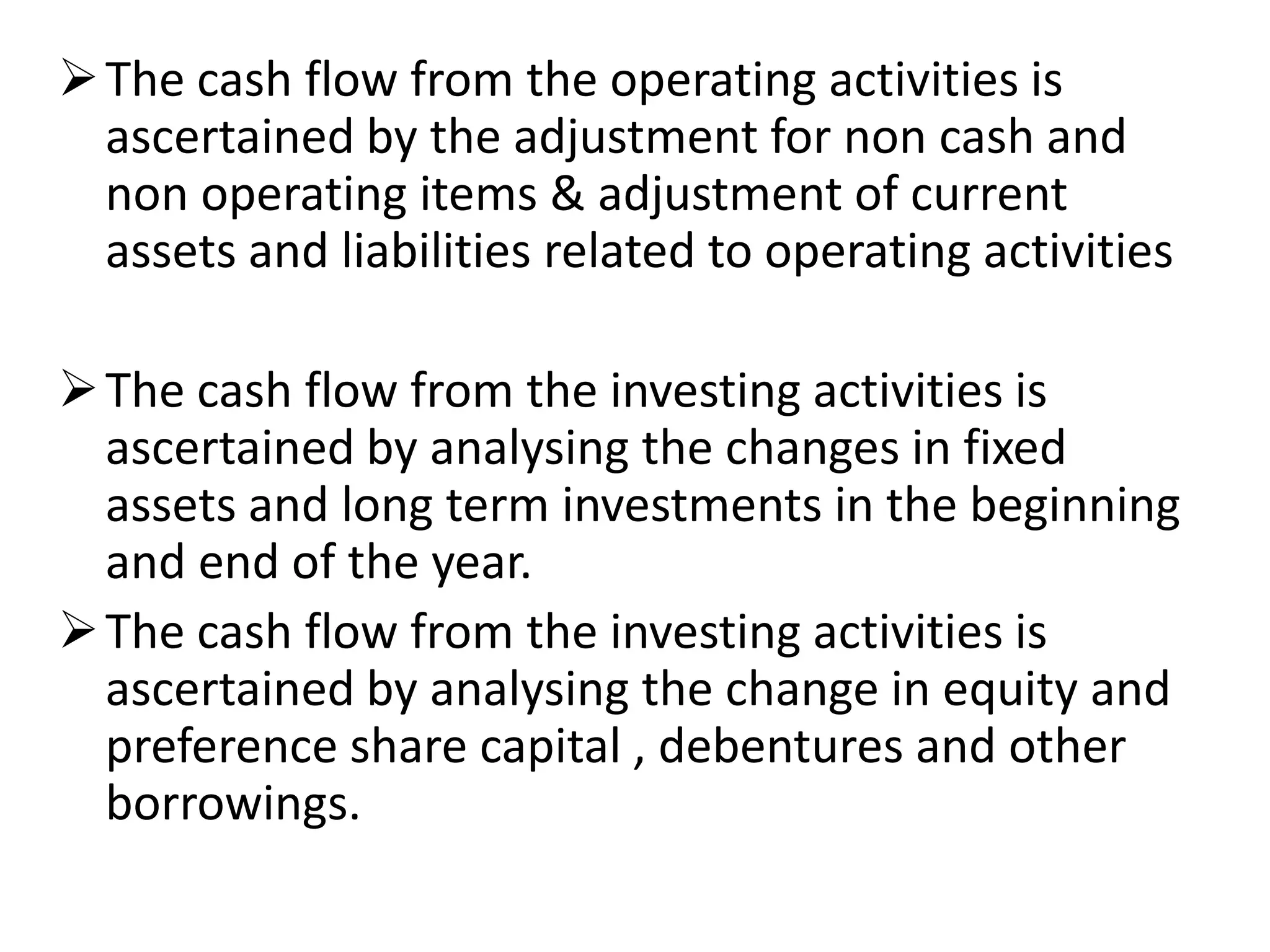

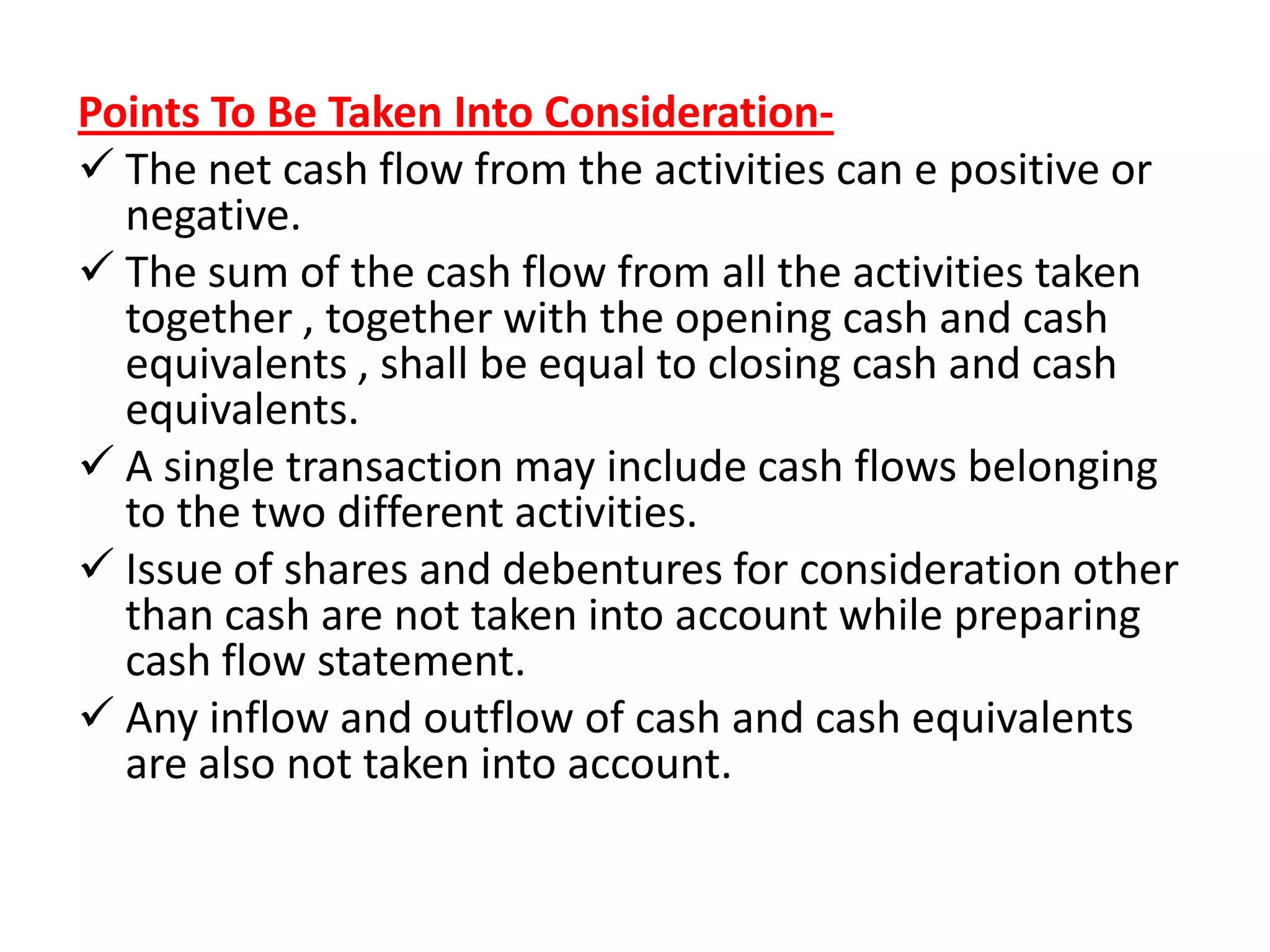

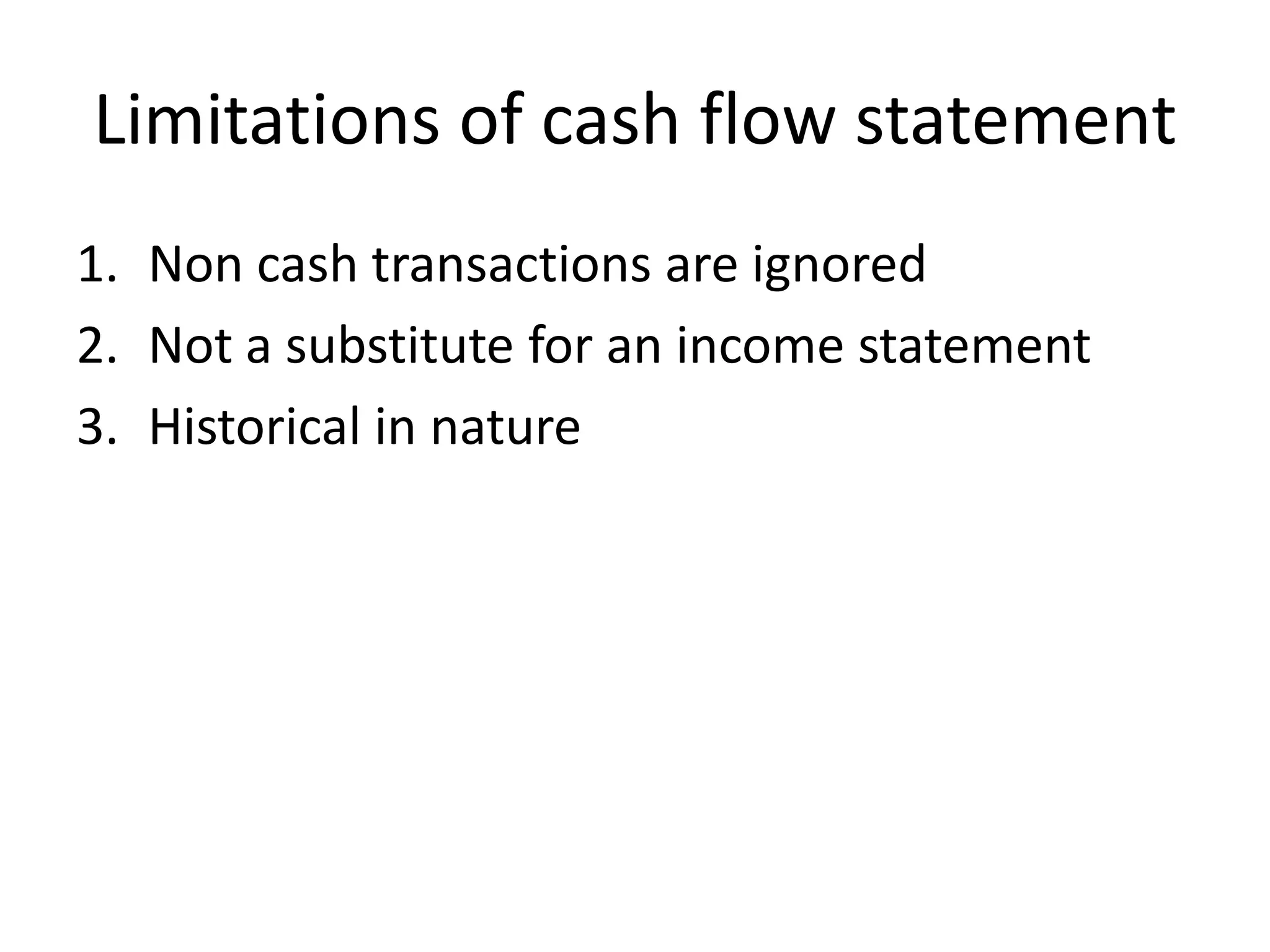

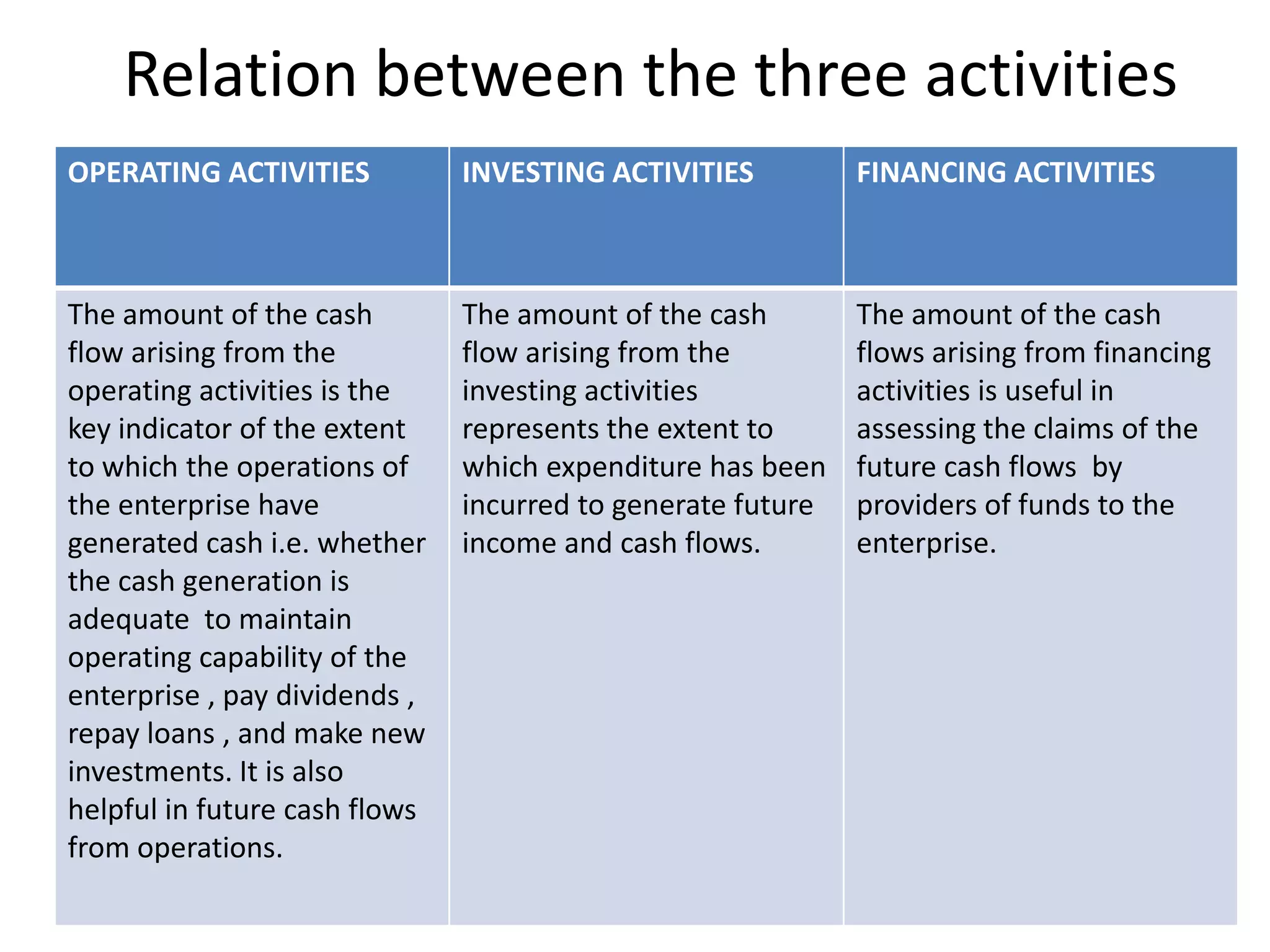

The document discusses analysis of cash flow statements. It defines cash flow statements and explains that they classify transactions into operating, investing and financing activities. Operating activities include cash from sales and payments for supplies. Investing activities involve purchases and sales of long-term assets. Financing activities comprise items like share issuances and debt repayments. The document also outlines the preparation of cash flow statements, uses of the statements, and limitations like ignoring non-cash transactions.