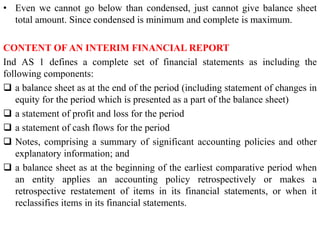

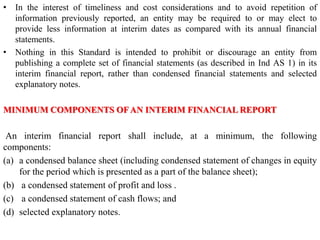

Ind AS 34 provides the requirements for interim financial reporting, requiring listed companies to publish interim financial reports on a quarterly basis. These interim reports must include at a minimum condensed statements of financial position, comprehensive income, changes in equity and cash flows, along with selected explanatory notes. The standard specifies the recognition and measurement principles to be applied in interim reports, which should use the same accounting policies as the annual financial statements.