Downloaded 281 times

![Thank you [email_address]](https://image.slidesharecdn.com/intangibleassetsias38-111024064901-phpapp02/85/Intangible-assets-ias-38-36-320.jpg)

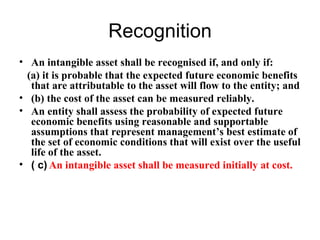

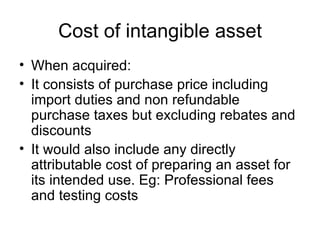

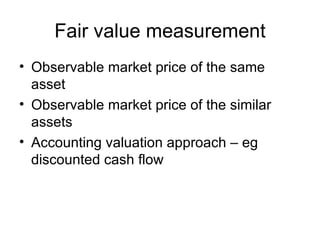

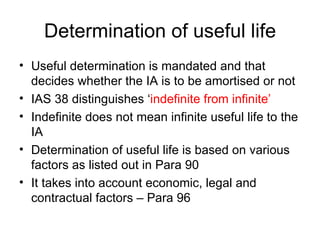

The document provides an overview of accounting for intangible assets under IAS 38. It discusses the definition of intangible assets, recognition criteria, measurement at cost or fair value, amortization of intangible assets with finite useful lives, impairment testing, and disclosure requirements. The document also covers topics such as government grants, internally generated intangible assets, revaluation model, and differences between IFRS and Indian GAAP treatment of intangible assets.

![Brennan, Niamh and Connell, Brenda [2000] Intellectual Capital: Current Issue...](https://cdn.slidesharecdn.com/ss_thumbnails/0410brennanconnellintellectualcapitalcurrentissuesandpolicyimplications-121116102513-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![Contingencies and provisioning[1]](https://cdn.slidesharecdn.com/ss_thumbnails/contingenciesandprovisioning1-111024070333-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

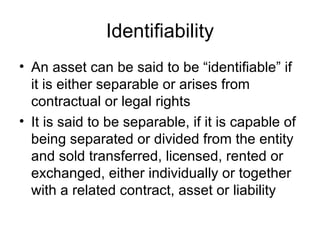

![Definitions[1]](https://cdn.slidesharecdn.com/ss_thumbnails/definitions1-111024070329-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)