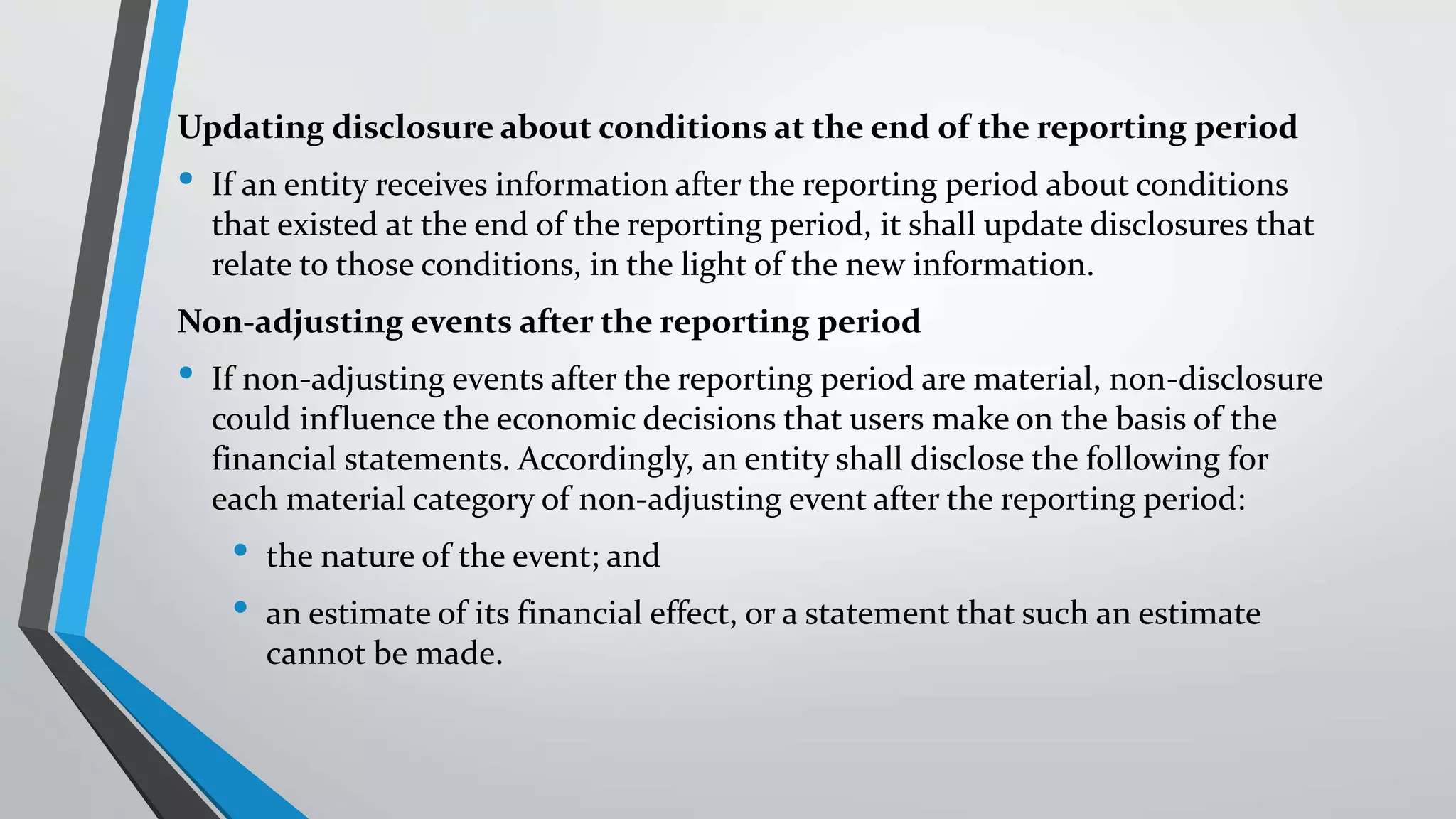

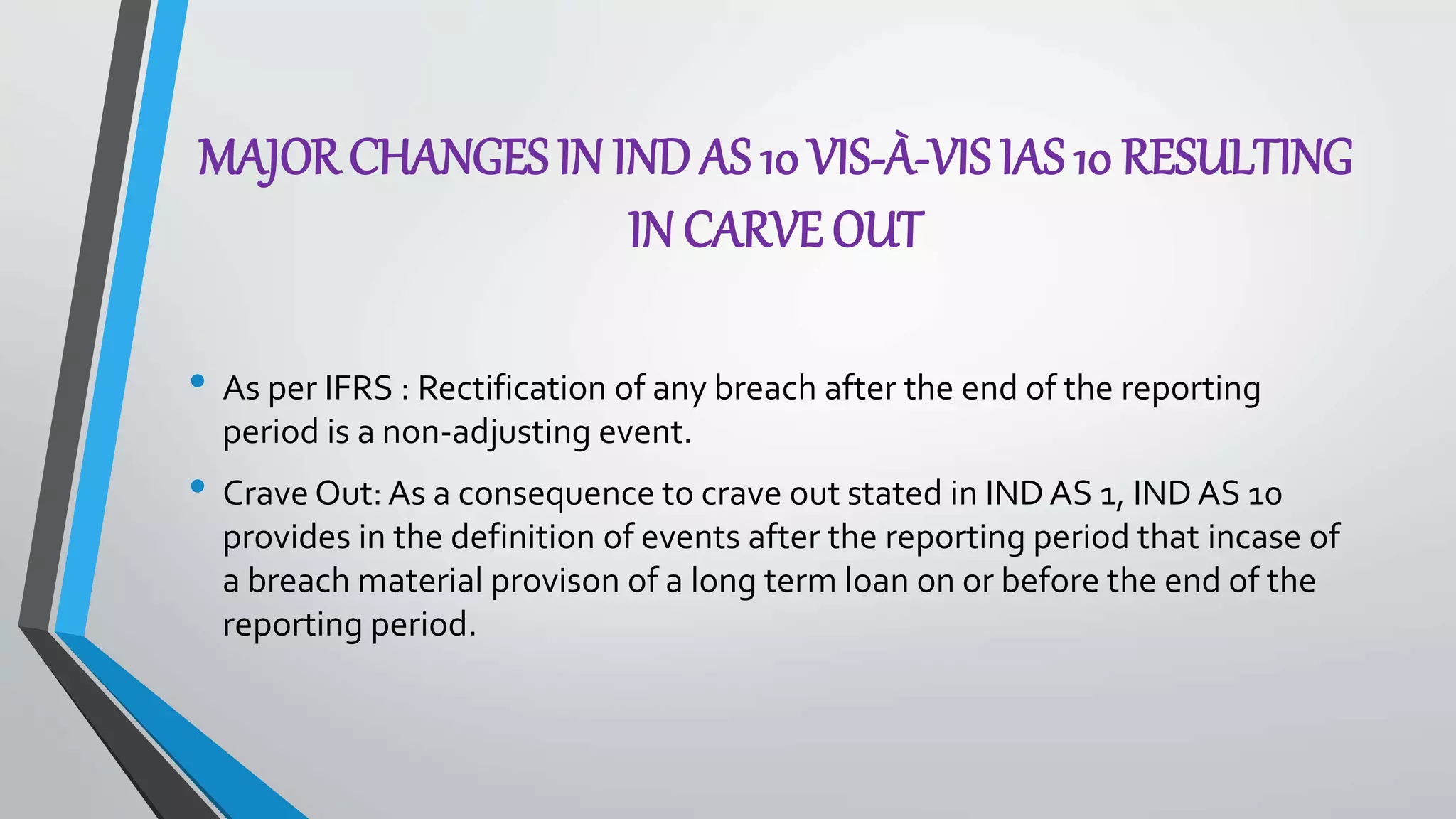

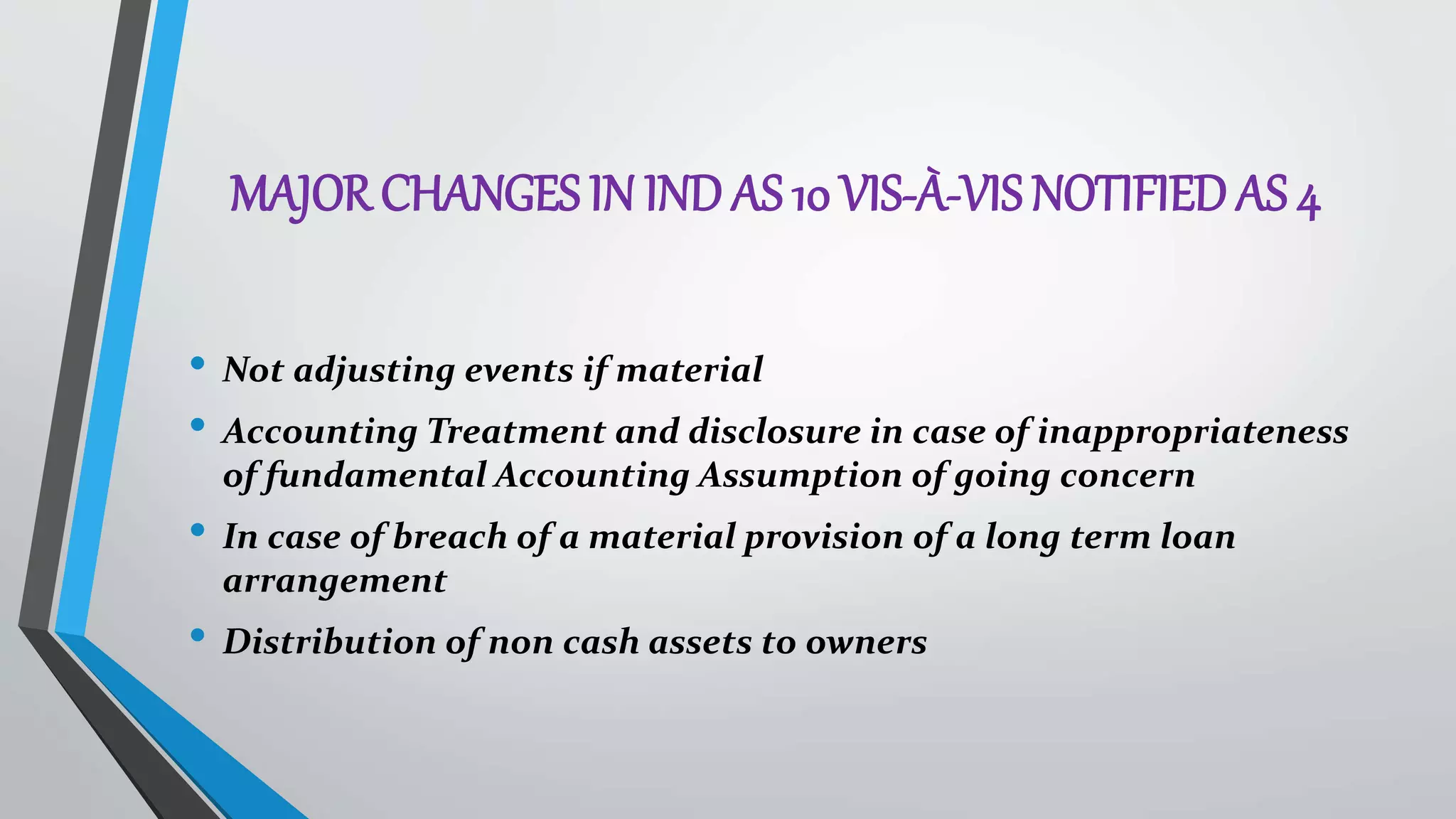

This document provides an overview of Indian Accounting Standard 10 (Ind AS 10) which deals with events after the reporting period. It defines key terms and outlines the accounting treatment and disclosure requirements for adjusting and non-adjusting events that occur after an entity's reporting period but before its financial statements are authorized for issue. The standard requires an entity to adjust amounts recognized in its financial statements for adjusting events and provide updated disclosures for certain non-adjusting events. It also addresses the assessment of an entity's ability to continue as a going concern if events after the reporting period indicate otherwise.