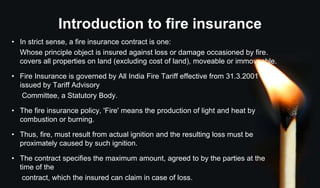

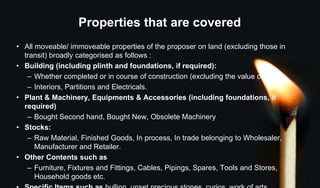

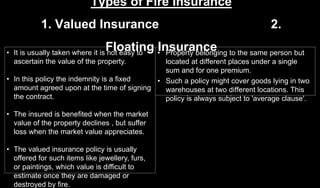

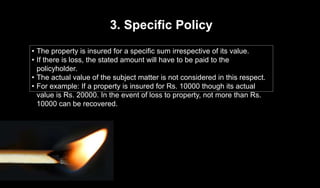

Fire insurance is designed to protect against losses due to fire, covering various properties on land, and governed by the All India Fire Tariff. Insurers must have insurable interest, and the policy specifies the maximum claim amount; certain losses, such as those from earthquakes or theft, are not covered. There are different types of fire insurance policies, including valued, floating, specific, and comprehensive policies, each with distinct coverage terms and conditions.

![Chapter 1[definition and nature of insurance]](https://cdn.slidesharecdn.com/ss_thumbnails/chapter1definitionandnatureofinsurance-150912031826-lva1-app6891-thumbnail.jpg?width=640&height=640&fit=bounds)

![87356964 introduction-to-insurance[1]](https://cdn.slidesharecdn.com/ss_thumbnails/87356964-introduction-to-insurance1-121105111440-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)