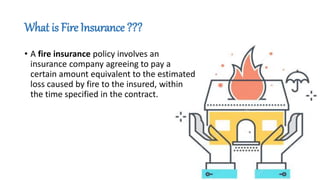

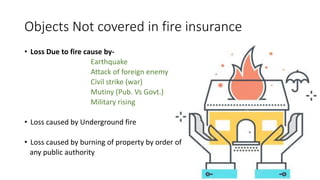

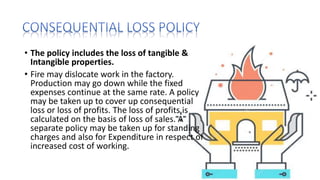

The document outlines the history and development of fire insurance, starting from its establishment after the Great Fire of London in 1666. It explains key concepts such as objects covered under fire insurance, various types of fire insurance policies, causes of fire, principles of fire insurance, and the procedure for obtaining it. Additionally, it highlights the advantages of fire insurance for both enterprises and homeowners.

![Chapter 1[definition and nature of insurance]](https://cdn.slidesharecdn.com/ss_thumbnails/chapter1definitionandnatureofinsurance-150912031826-lva1-app6891-thumbnail.jpg?width=640&height=640&fit=bounds)

![87356964 introduction-to-insurance[1]](https://cdn.slidesharecdn.com/ss_thumbnails/87356964-introduction-to-insurance1-121105111440-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)