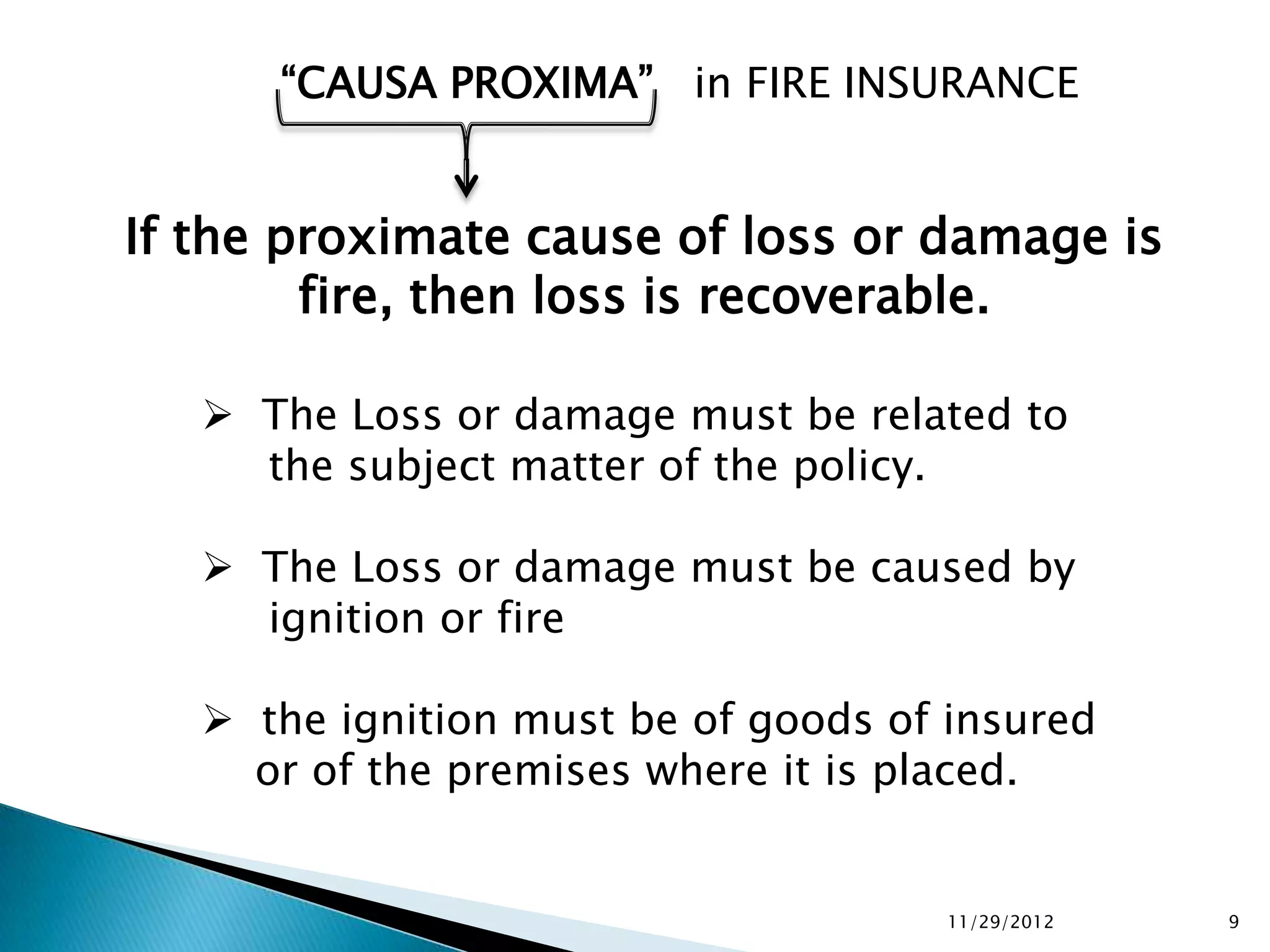

This document discusses fire insurance under the Insurance Act of 1938. It defines fire insurance as a contract where the insurer agrees to indemnify the insured for financial losses caused by fire in exchange for premium payments. It outlines the key principles of fire insurance such as utmost good faith, indemnity only for insured value, and losses must be proximately caused by fire. The document also covers the different types of fire insurance policies, losses that are and aren't covered, and the claims procedure. Overall it provides an overview of fire insurance concepts and practices in India.

![87356964 introduction-to-insurance[1]](https://cdn.slidesharecdn.com/ss_thumbnails/87356964-introduction-to-insurance1-121105111440-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)