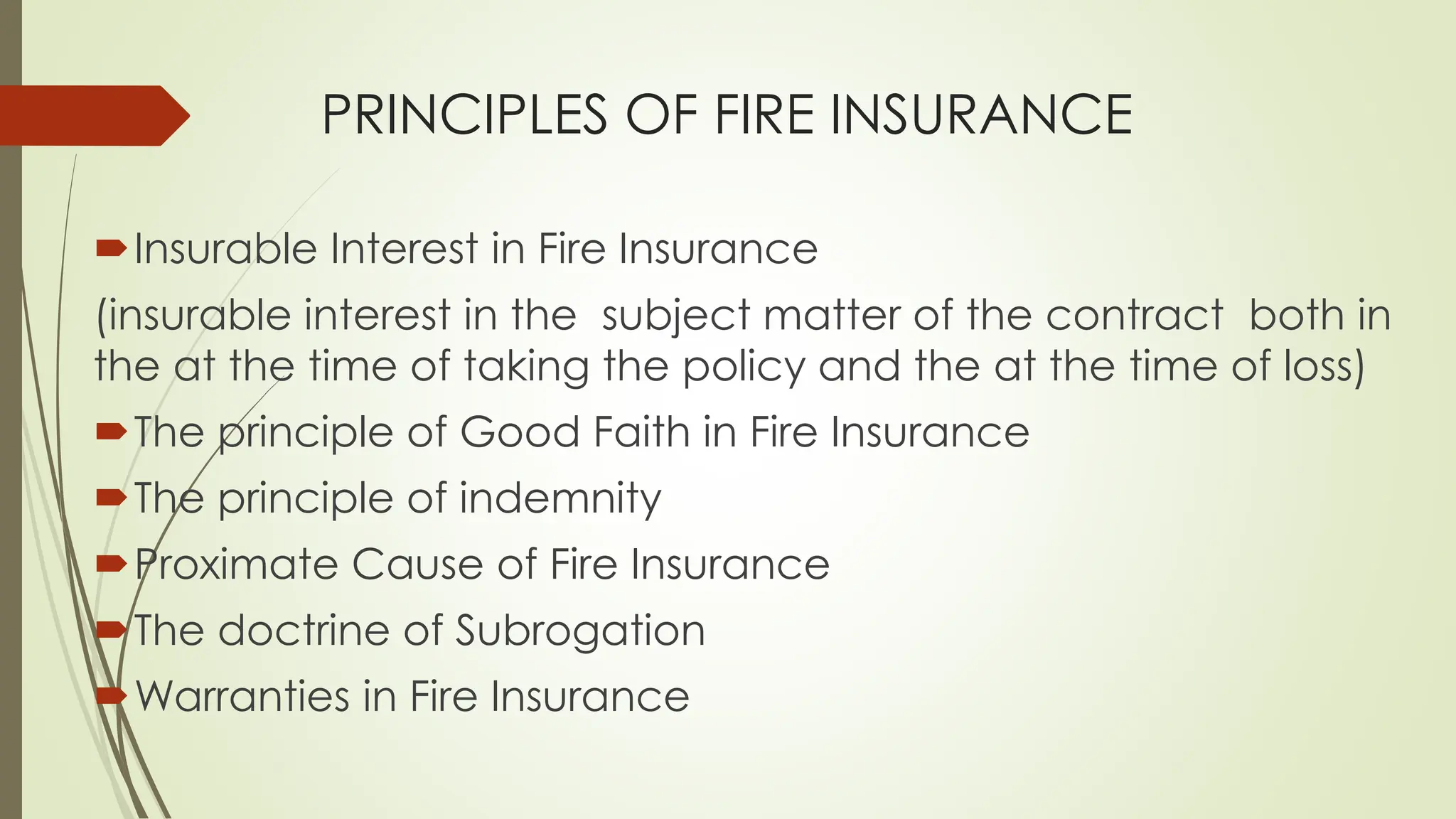

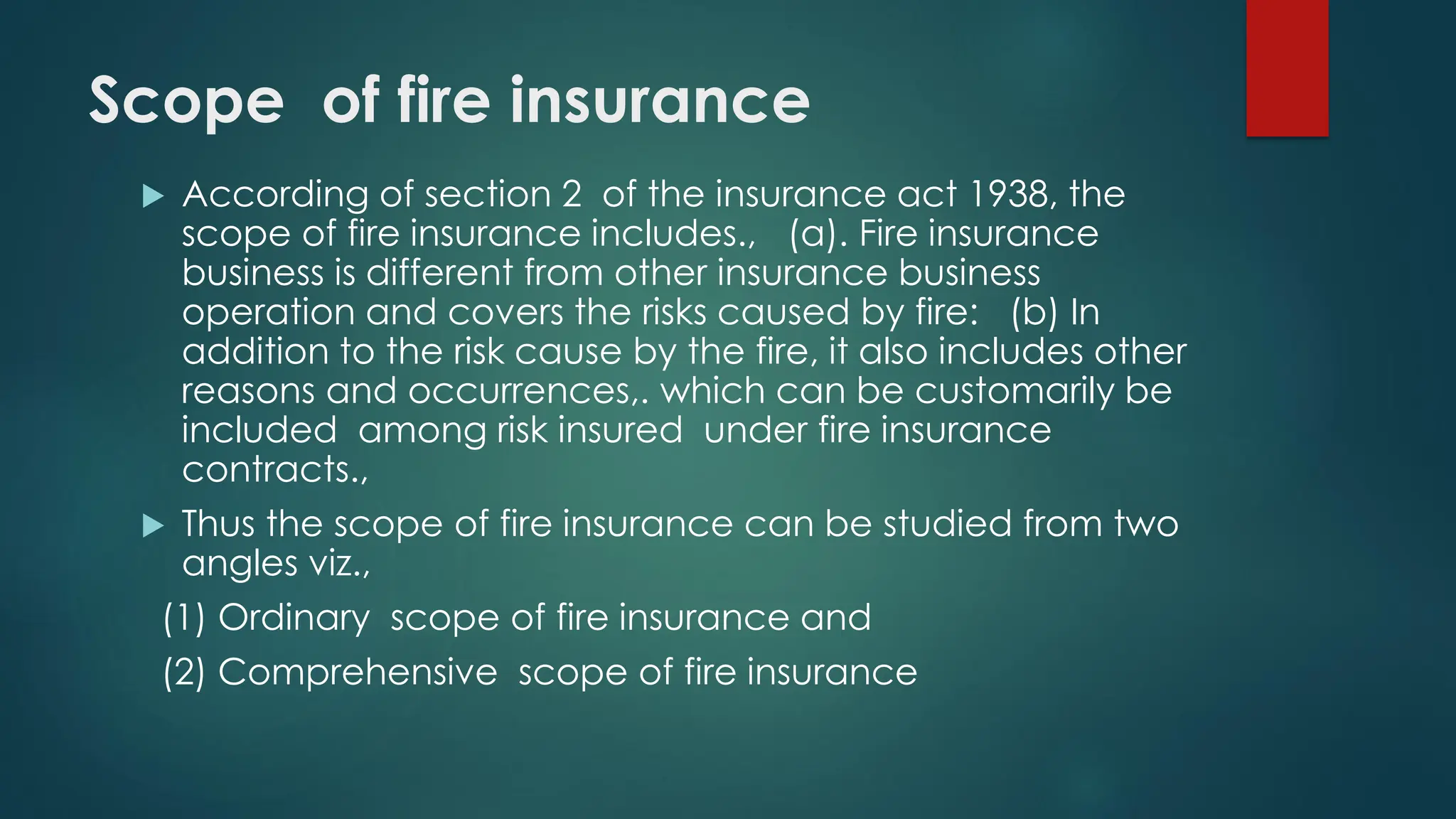

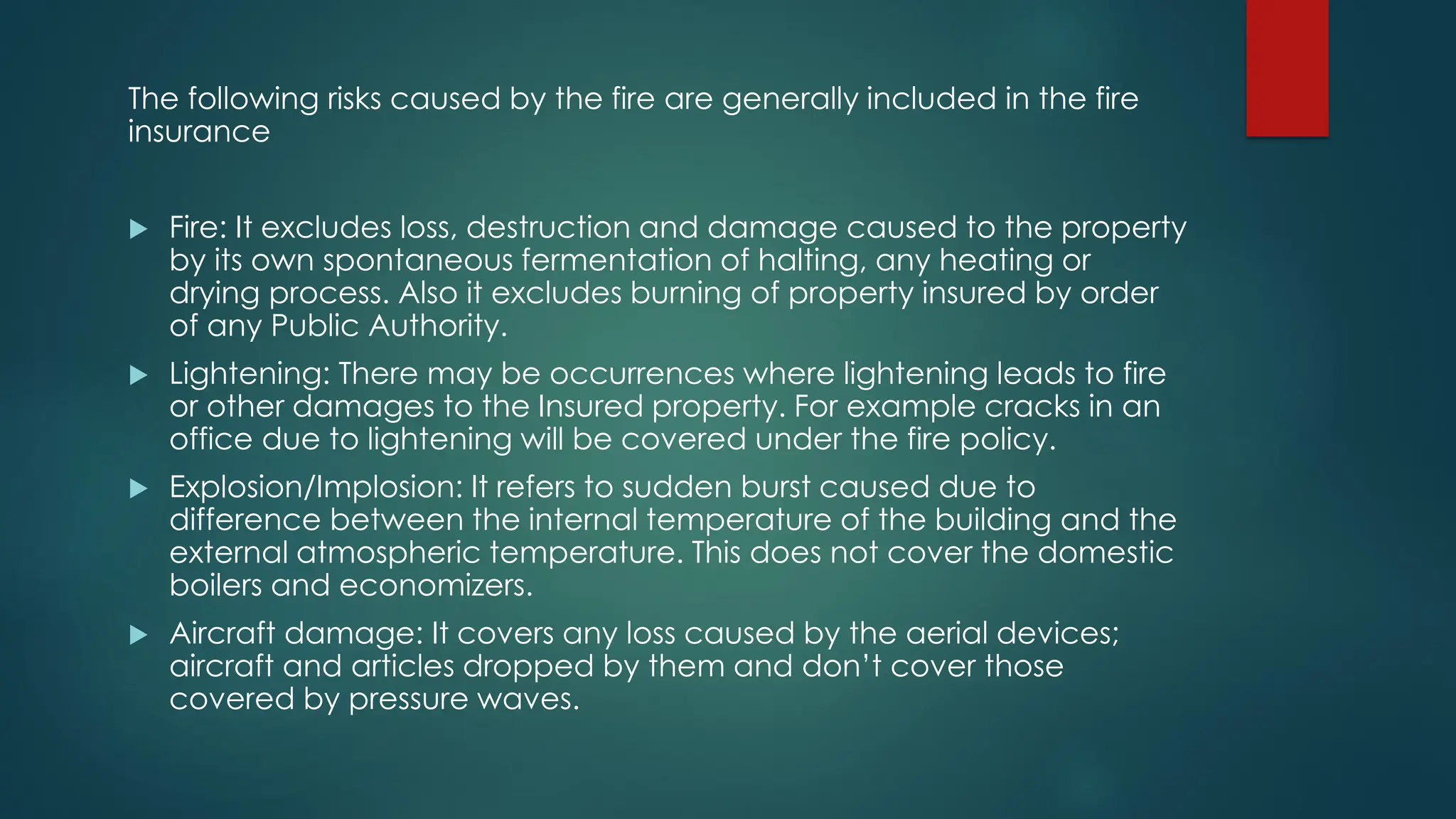

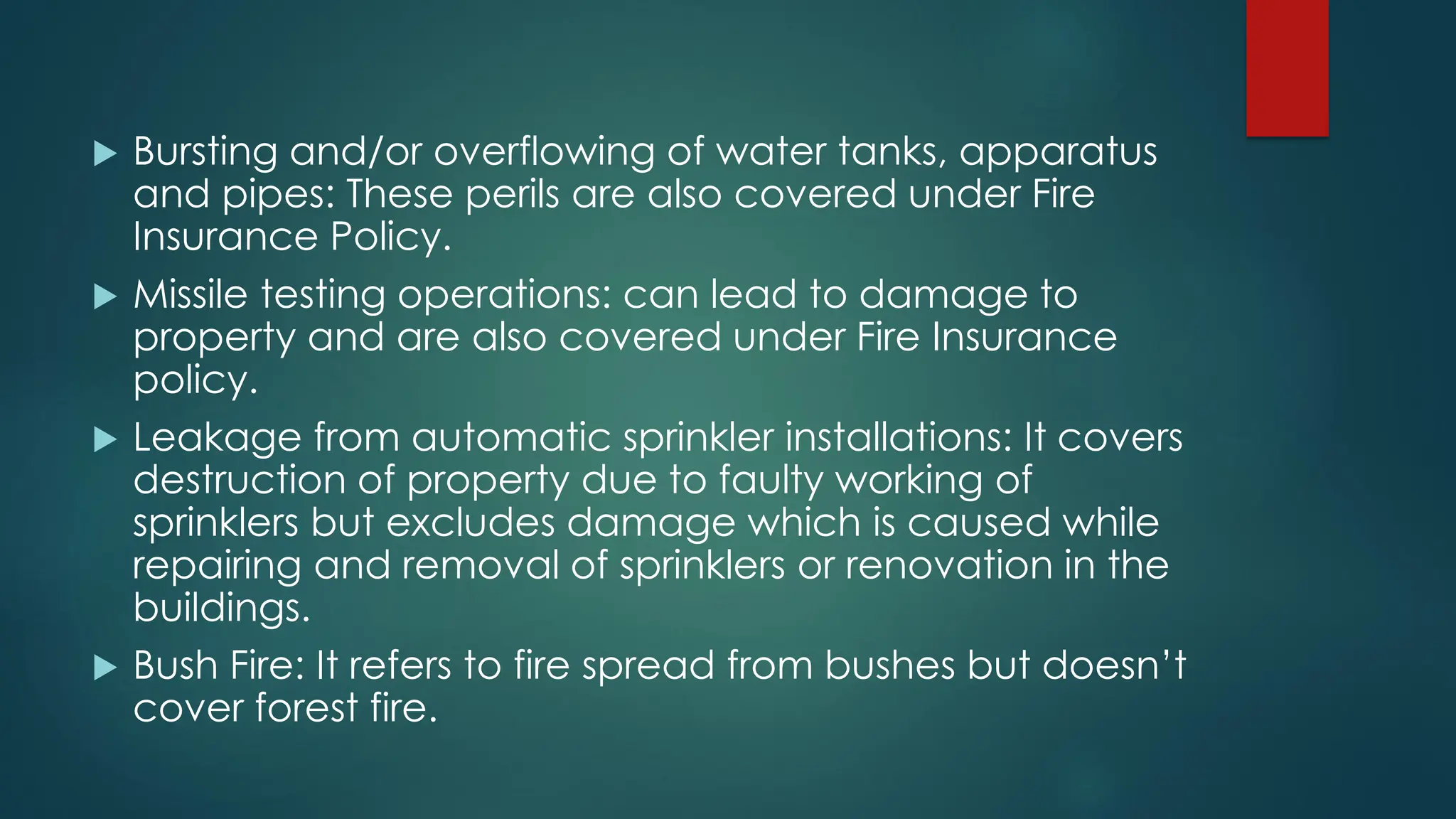

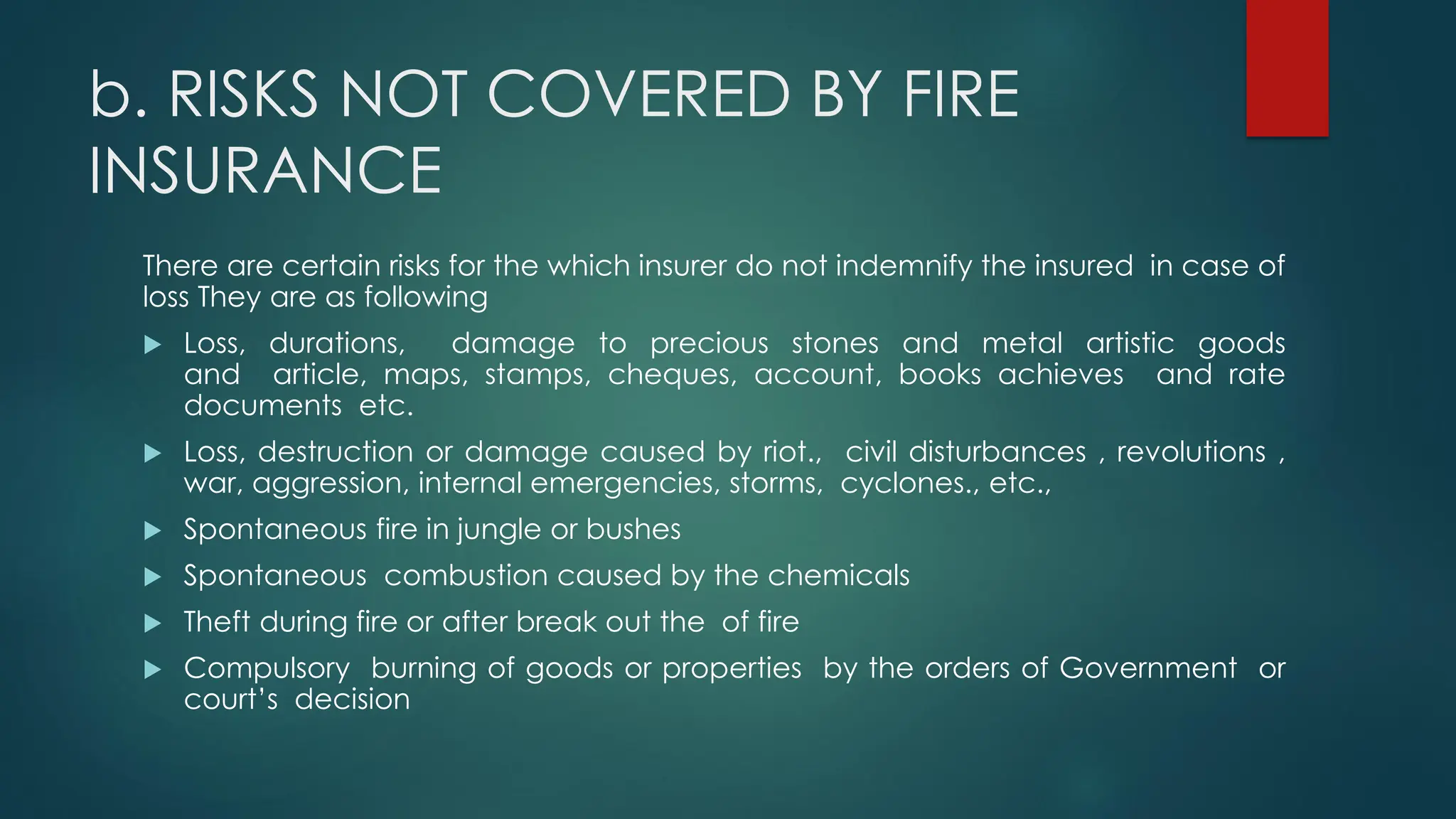

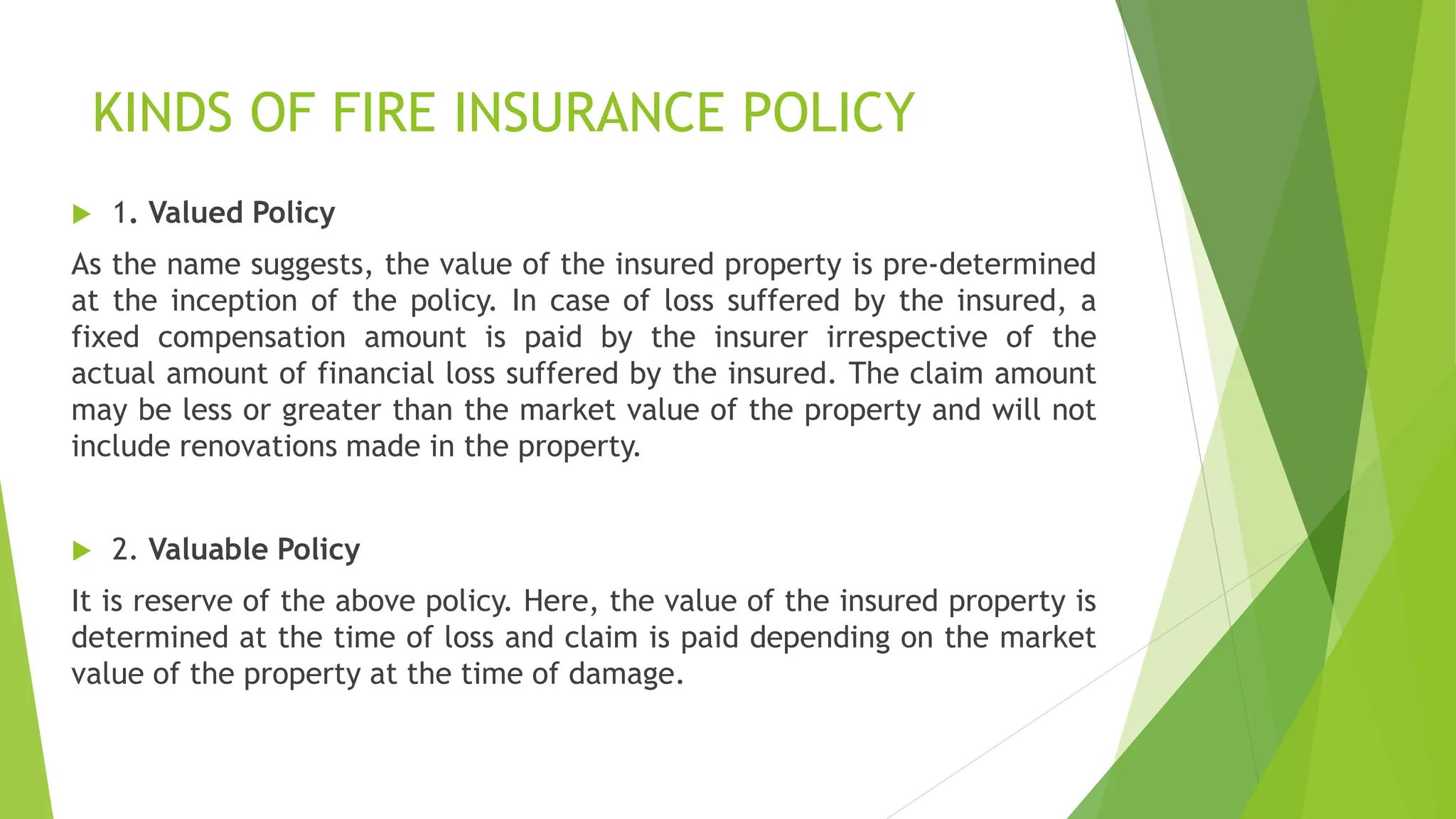

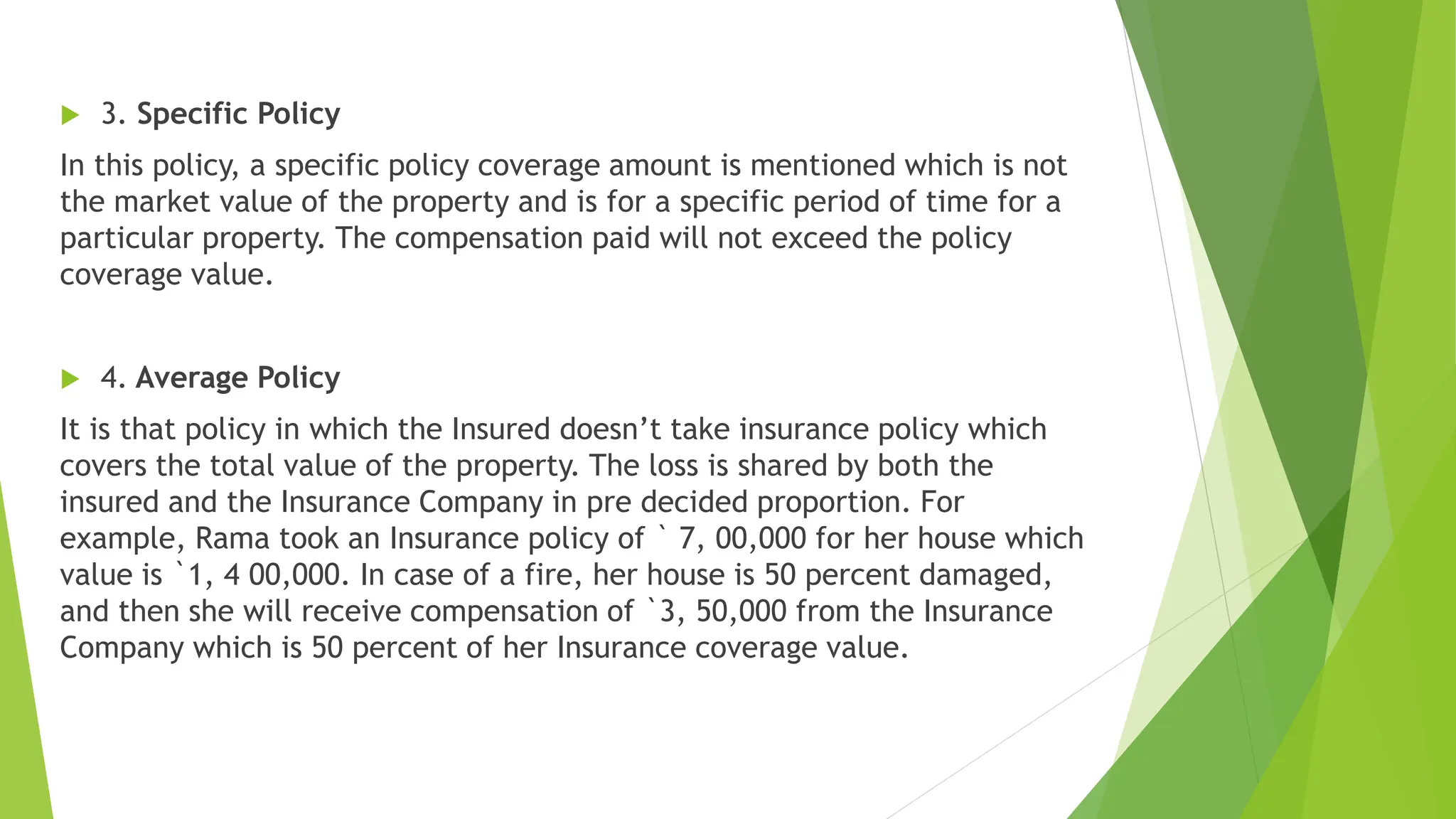

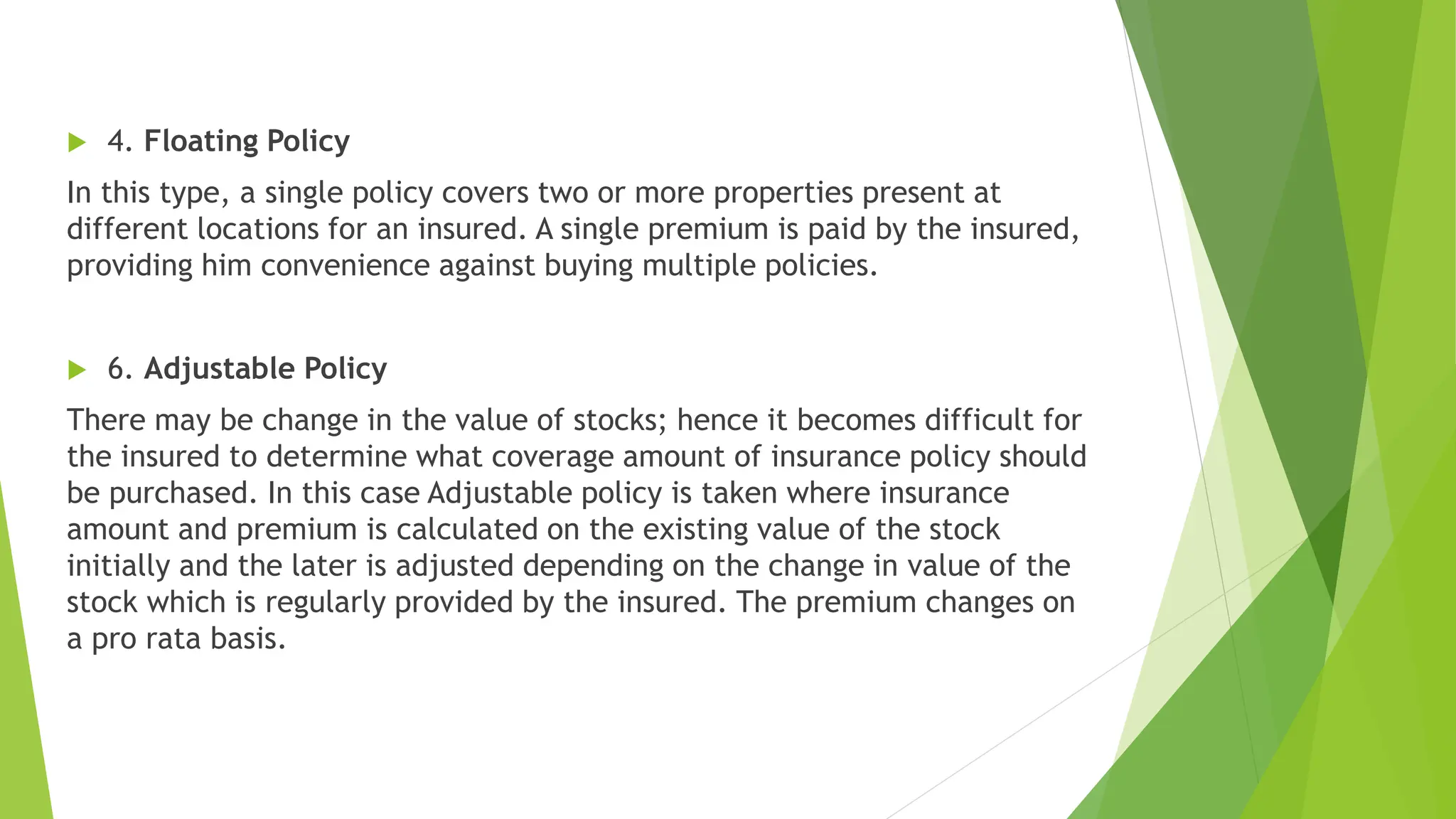

Fire insurance, defined by the Insurance Act of 1938, is a contract where the insurer compensates the insured for loss due to fire or related incidents. It covers various aspects including buildings, machinery, and specific risks such as explosions and natural disasters, while excluding certain losses like theft and damage caused by riots. There are multiple types of fire insurance policies, such as valued, floating, and comprehensive, each tailored to different coverage needs.

![87356964 introduction-to-insurance[1]](https://cdn.slidesharecdn.com/ss_thumbnails/87356964-introduction-to-insurance1-121105111440-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)