Downloaded 36 times

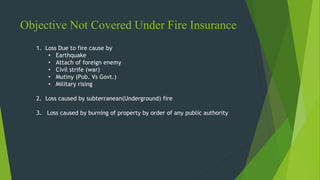

Fire insurance is a policy where an insurer agrees to compensate for fire-related losses to specified property types, such as buildings and machinery, while excluding losses from specific causes like earthquakes or civil strife. Various policy types exist, including valued policies for hard-to-value items and floating policies for goods in multiple locations. Fire insurance benefits both enterprises and homeowners by offering security for property and recovery of damages.

![87356964 introduction-to-insurance[1]](https://cdn.slidesharecdn.com/ss_thumbnails/87356964-introduction-to-insurance1-121105111440-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)