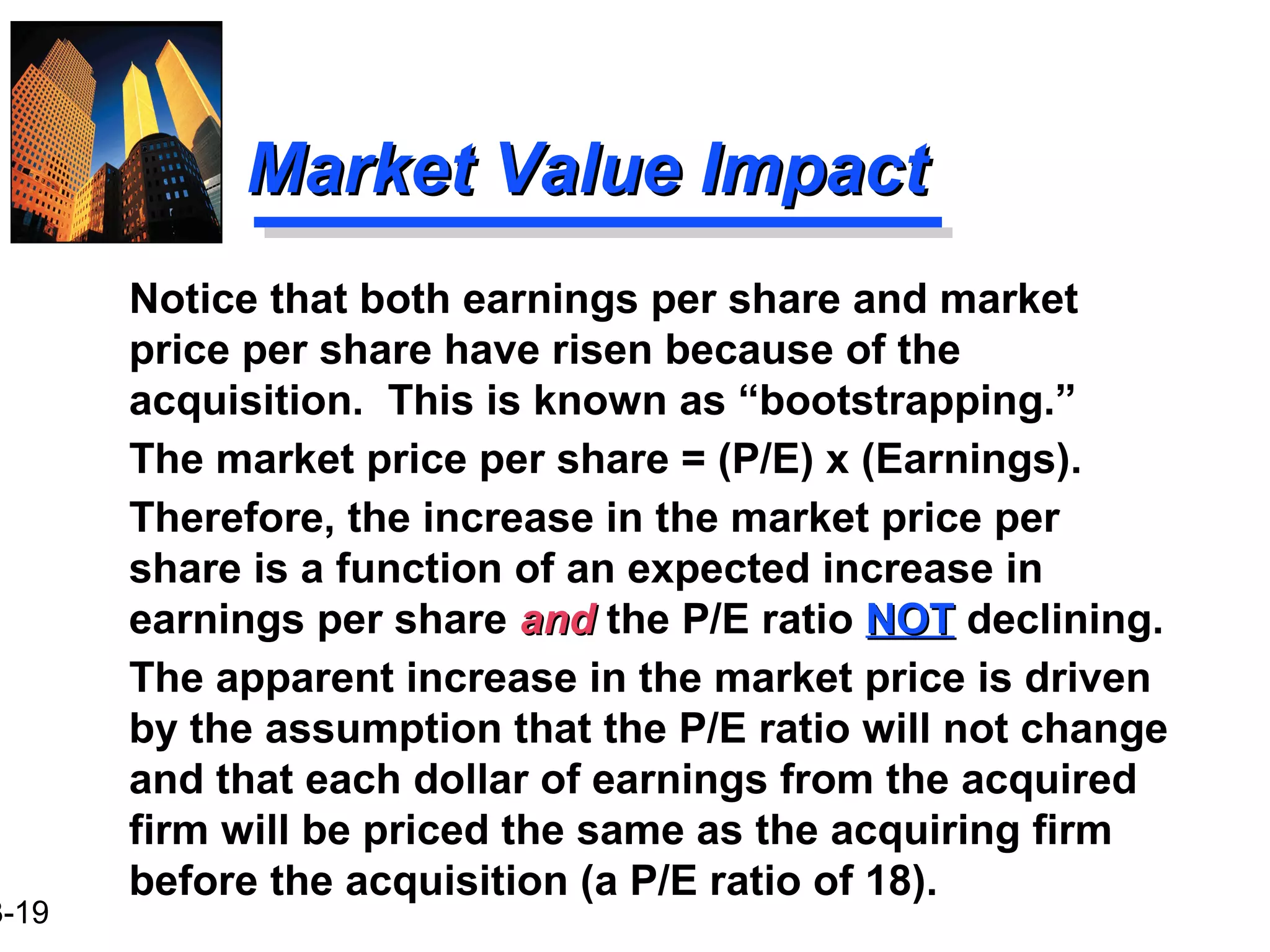

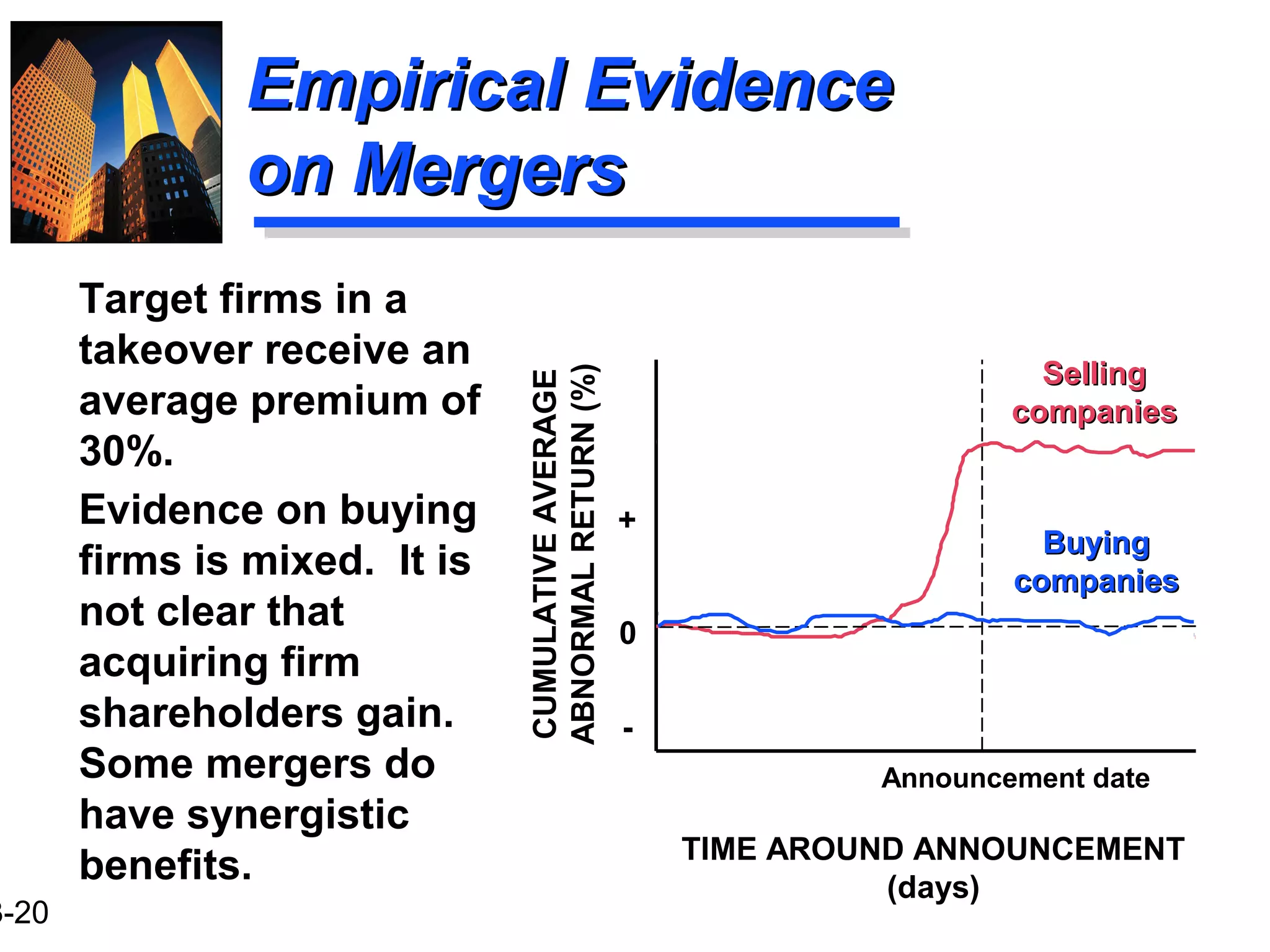

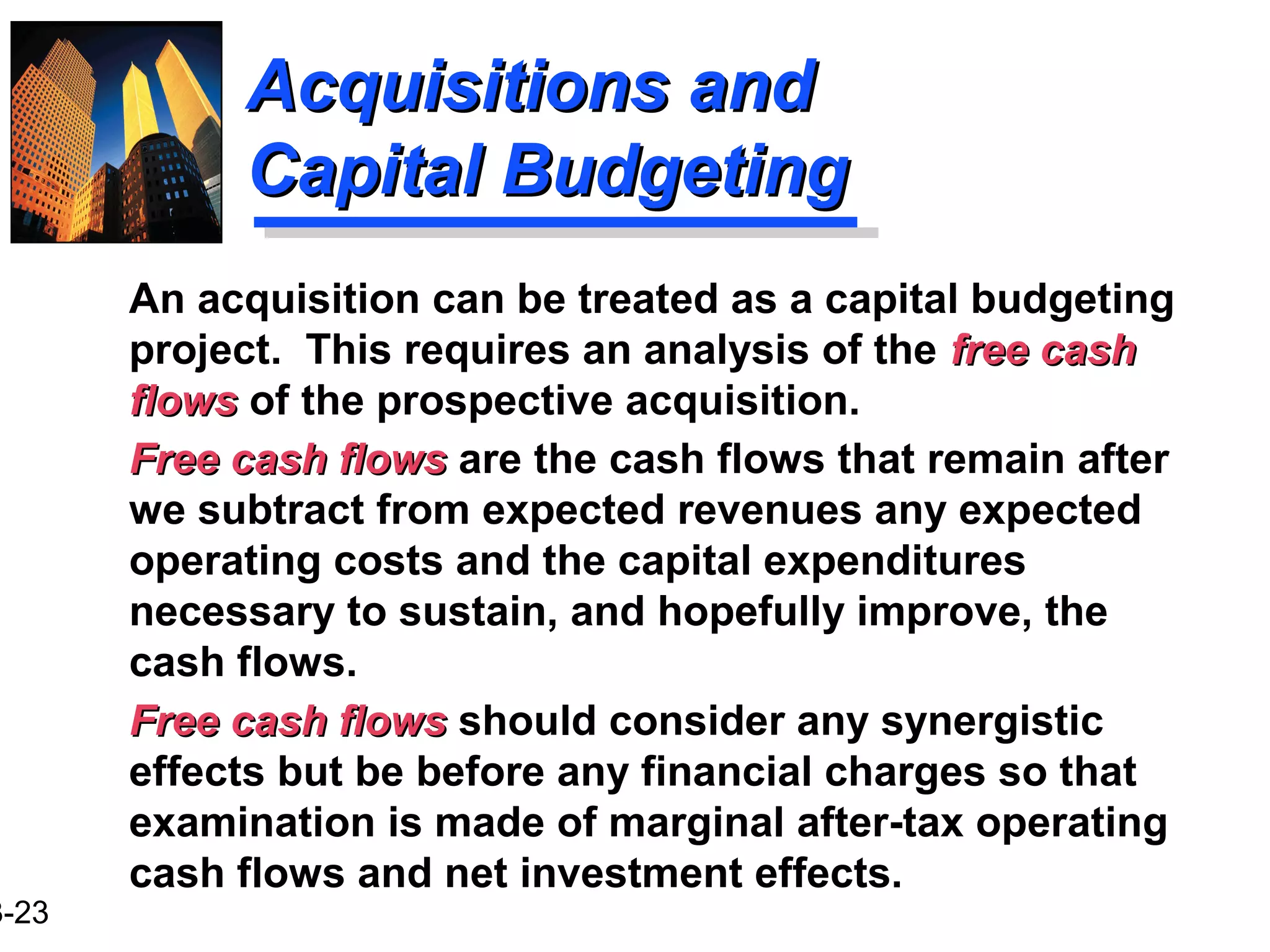

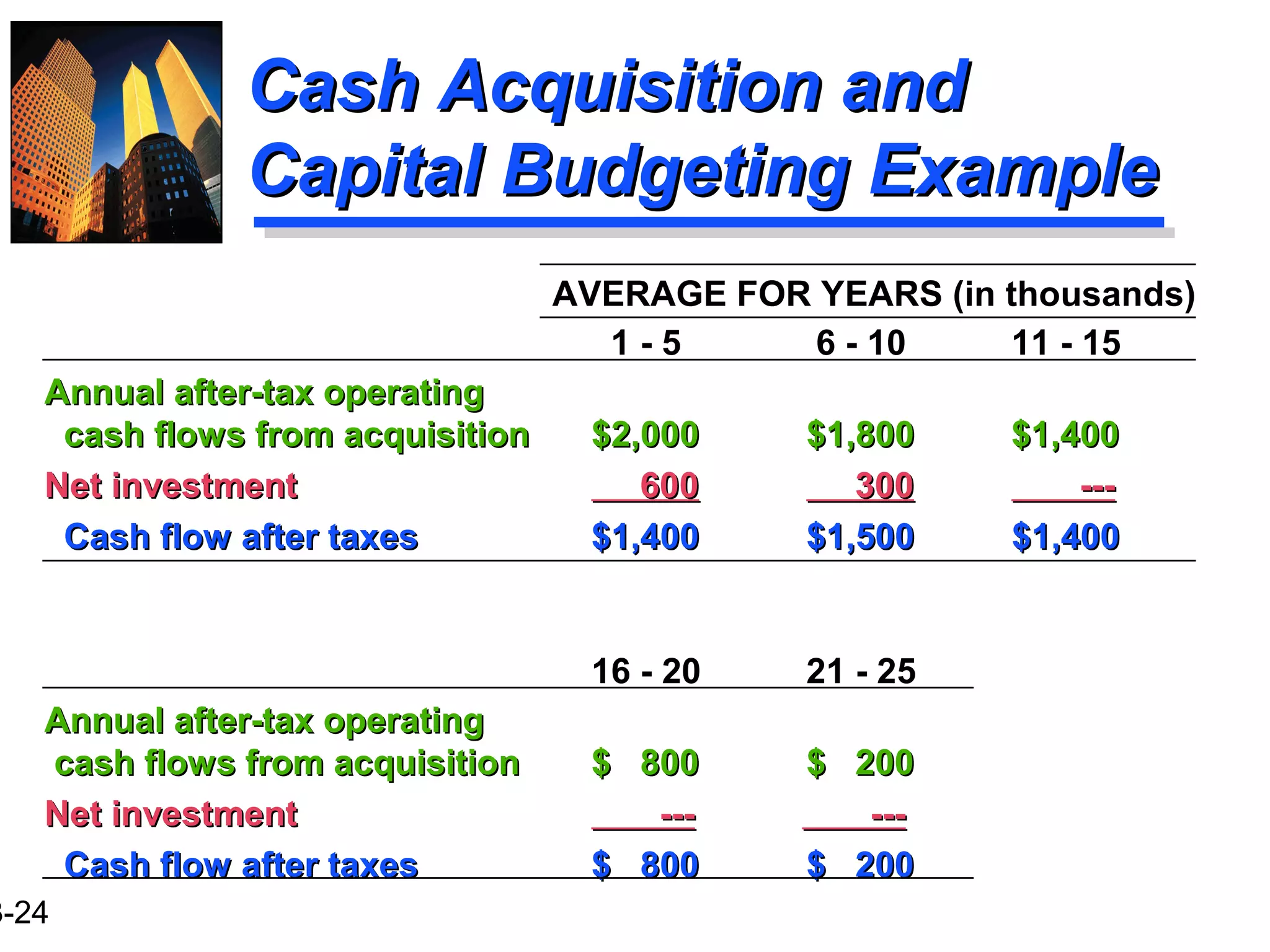

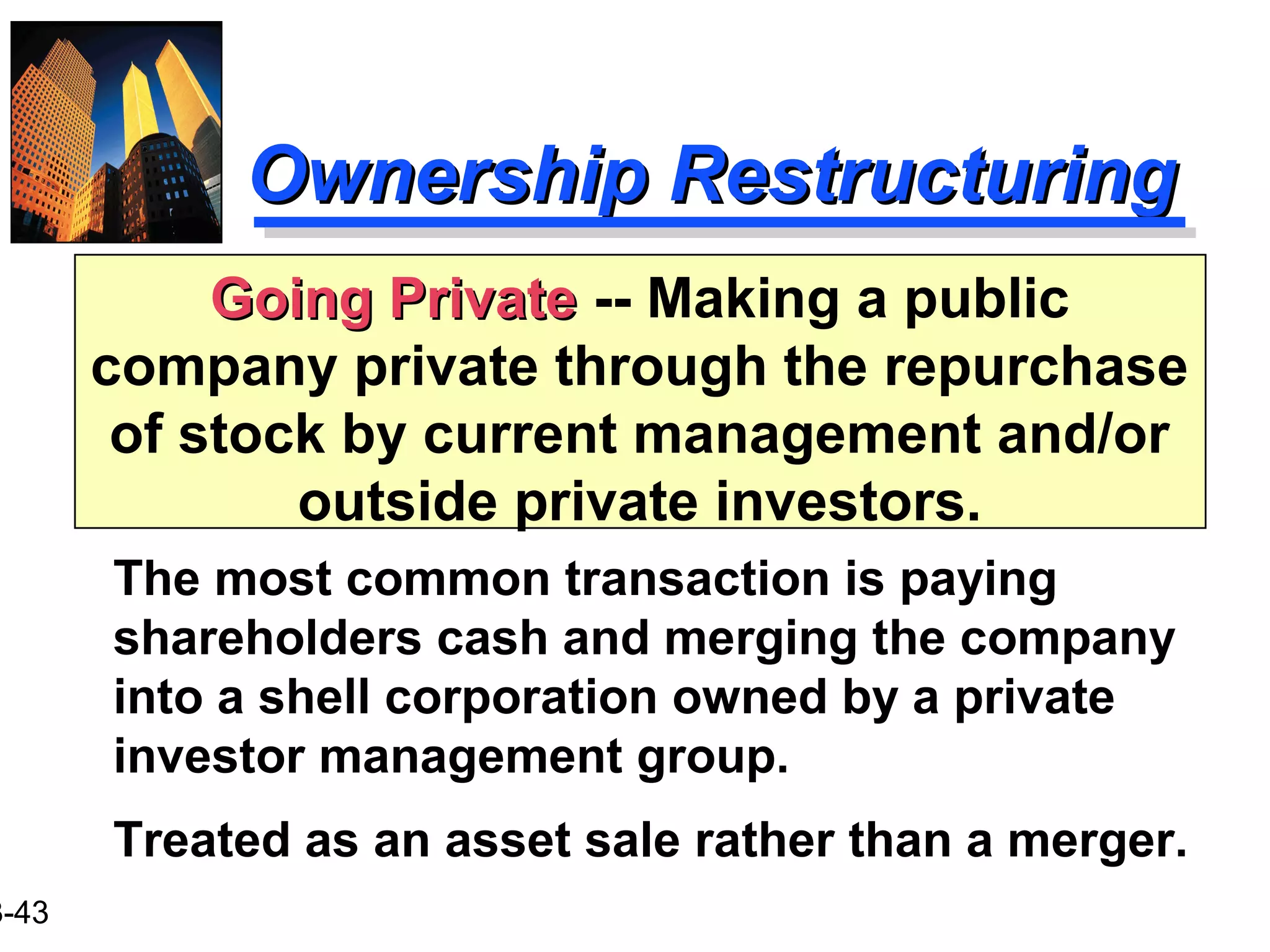

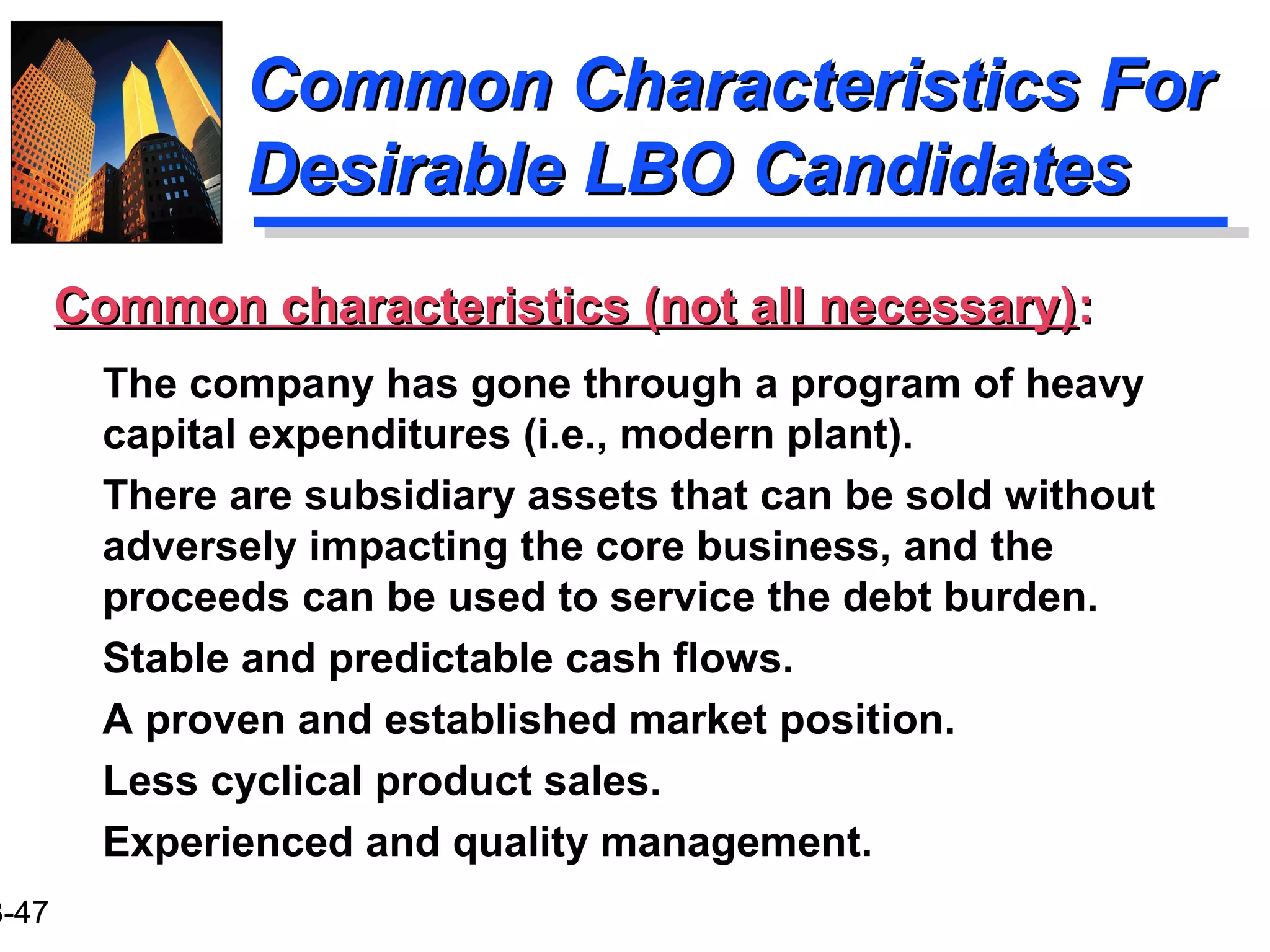

This document discusses various forms of corporate restructuring, including mergers, acquisitions, divestitures, and leveraged buyouts. It provides details on strategic acquisitions involving common stock, including examples of calculating earnings per share and exchange ratios for mergers. The document also covers tender offers, defensive tactics by target companies, and the accounting treatment of goodwill in mergers and acquisitions.

![3-10

Strategic AcquisitionsStrategic Acquisitions

Involving Common StockInvolving Common Stock

The shareholders of Company A will

experience an increase in earnings per

share because of the acquisition [$4.10 post-

merger EPS versus $4.00 pre-merger EPS].

The shareholders of Company B will

experience a decrease in earnings per share

because of the acquisition [.546875 x $4.10 =

$2.24 post-merger EPS versus $2.50 pre-

merger EPS].](https://image.slidesharecdn.com/ch23-180315073238/75/Financial-Management-Slides-Ch-23-10-2048.jpg)

![3-11

Strategic AcquisitionsStrategic Acquisitions

Involving Common StockInvolving Common Stock

Surviving firm EPS will increase any time the

P/E ratio “paid” for a firm is less than the

pre-merger P/E ratio of the firm doing the

acquiring. [Note: P/E ratio “paid” for

Company B is $35/$2.50 = 14 versus pre-

merger P/E ratio of 16 for Company A.]](https://image.slidesharecdn.com/ch23-180315073238/75/Financial-Management-Slides-Ch-23-11-2048.jpg)

![3-13

Strategic AcquisitionsStrategic Acquisitions

Involving Common StockInvolving Common Stock

The shareholders of Company A will

experience a decrease in earnings per share

because of the acquisition [$3.90 post-

merger EPS versus $4.00 pre-merger EPS].

The shareholders of Company B will

experience an increase in earnings per

share because of the acquisition [.703125 x

$4.10 = $2.88 post-merger EPS versus $2.50

pre-merger EPS].](https://image.slidesharecdn.com/ch23-180315073238/75/Financial-Management-Slides-Ch-23-13-2048.jpg)

![3-14

Strategic AcquisitionsStrategic Acquisitions

Involving Common StockInvolving Common Stock

Surviving firm EPS will decrease any time

the P/E ratio “paid” for a firm is greater than

the pre-merger P/E ratio of the firm doing the

acquiring. [Note: P/E ratio “paid” for

Company B is $45/$2.50 = 18 versus pre-

merger P/E ratio of 16 for Company A.]](https://image.slidesharecdn.com/ch23-180315073238/75/Financial-Management-Slides-Ch-23-14-2048.jpg)