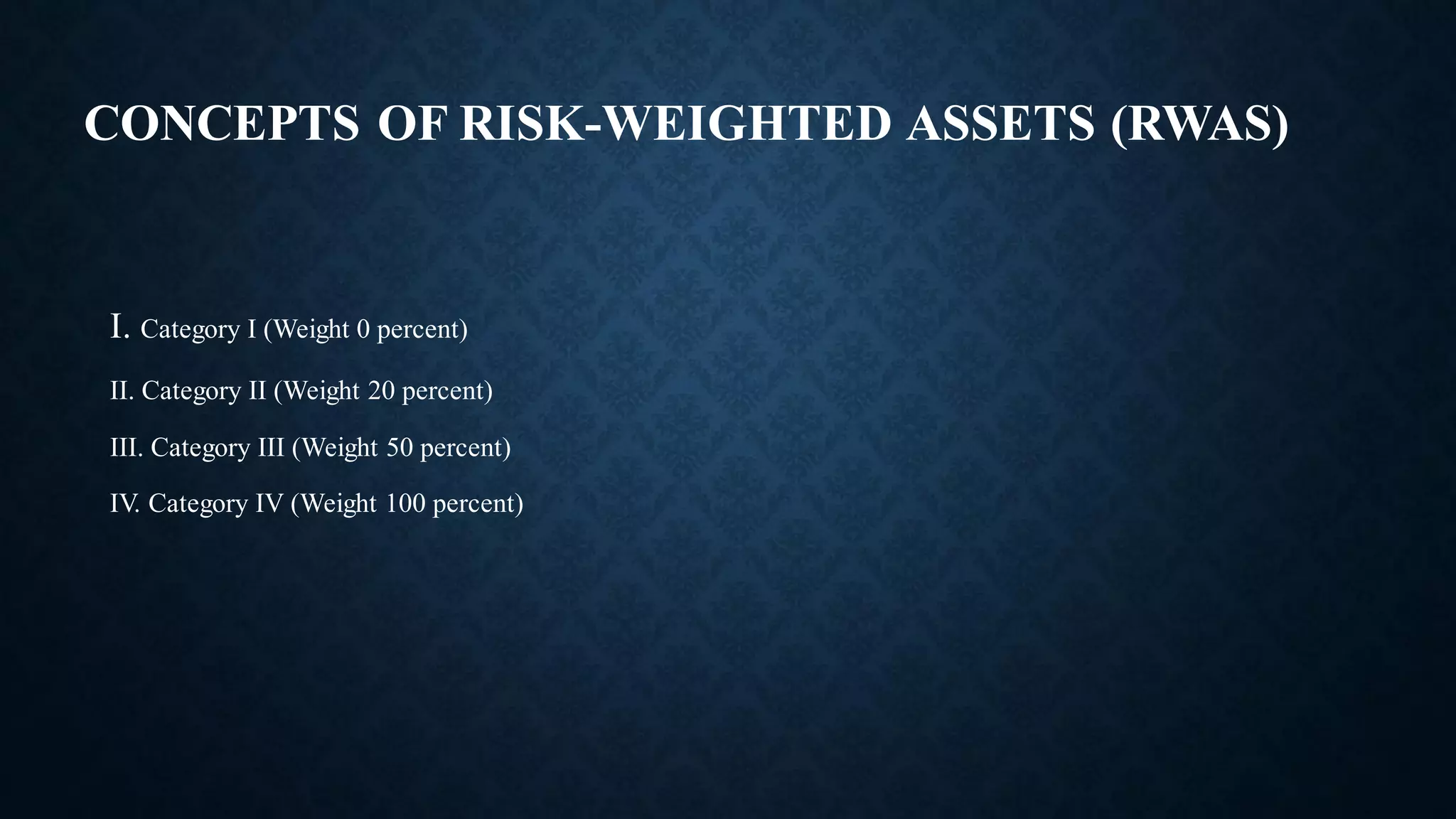

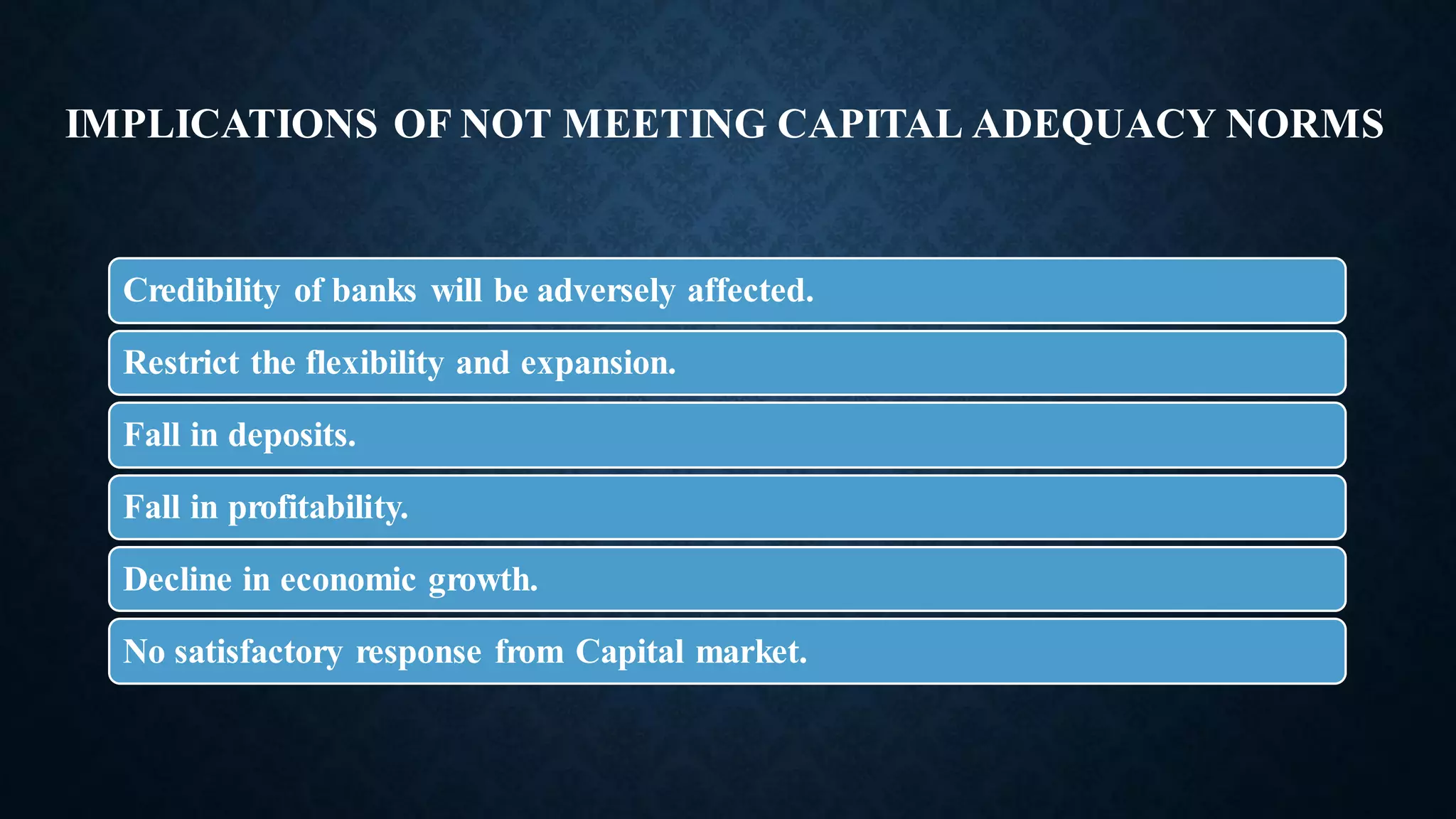

This document discusses capital adequacy ratio (CAR) and non-performing assets (NPAs). It defines CAR as a ratio of a bank's capital to its risk-weighted assets that regulators use to ensure banks can absorb losses. It discusses the types of capital (Tier I and Tier II), risk weights, and implications of not meeting CAR norms. Methods to improve CAR include mergers, better asset management, improved NPA recovery, recapitalization, and raising funds. NPAs are defined as loans overdue over 90-180 days. Factors contributing to NPAs include political interference, willful defaults, targeted lending, lack of monitoring, and hiding NPAs.