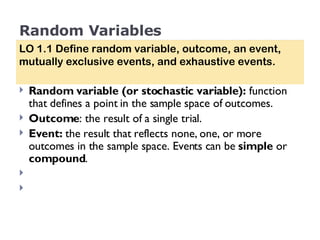

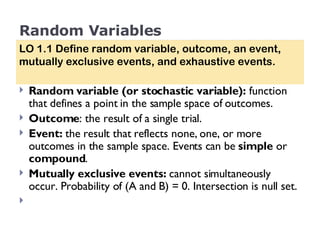

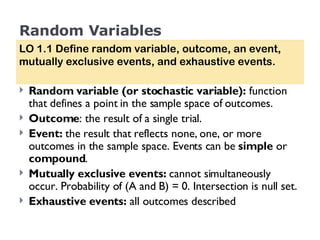

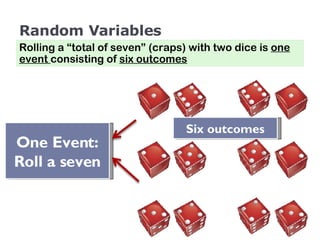

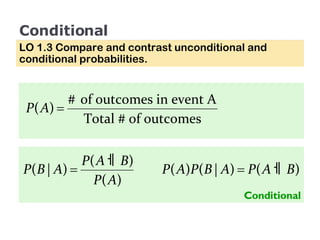

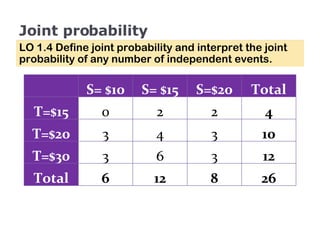

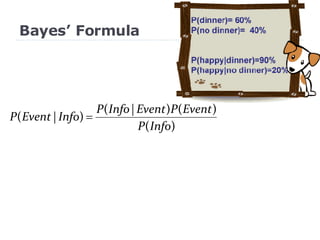

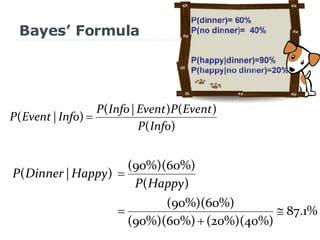

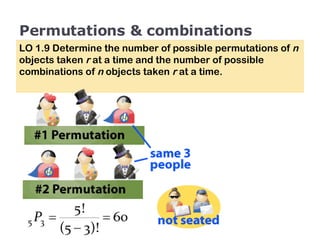

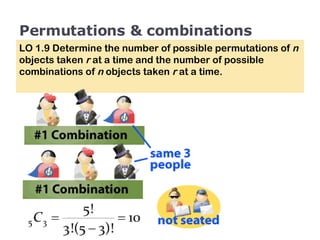

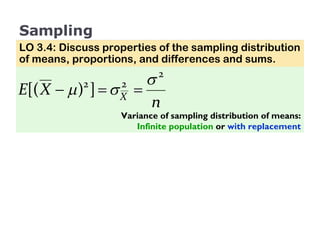

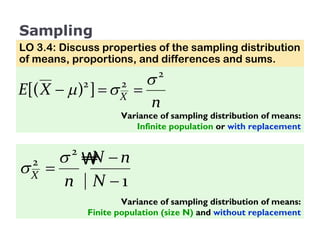

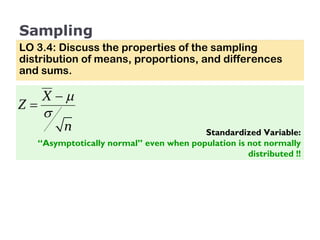

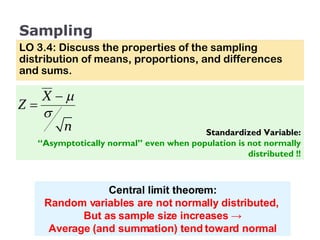

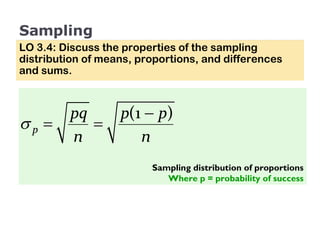

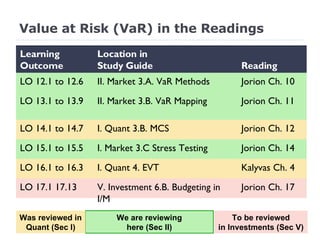

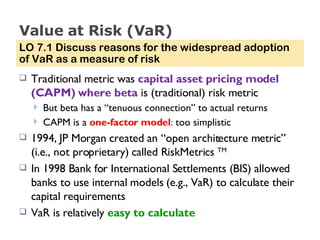

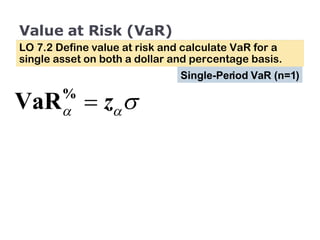

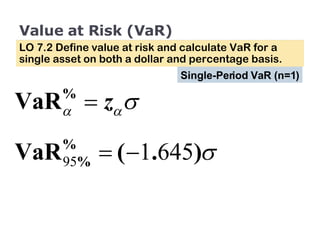

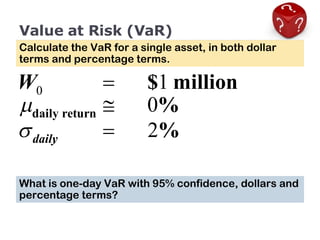

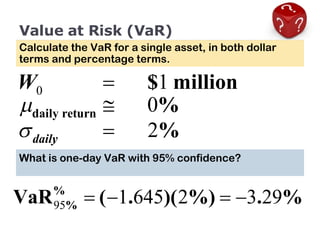

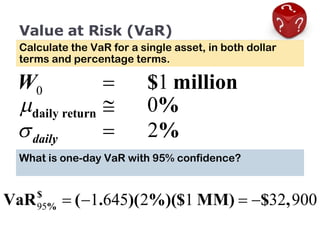

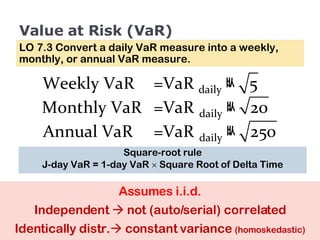

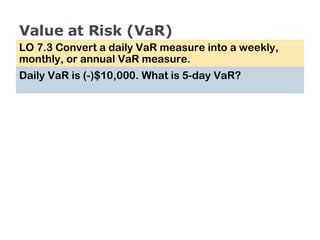

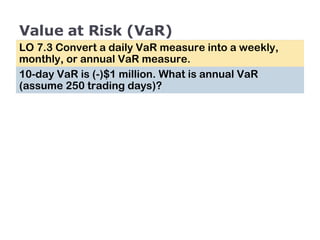

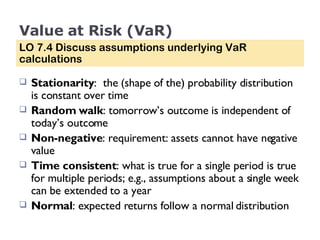

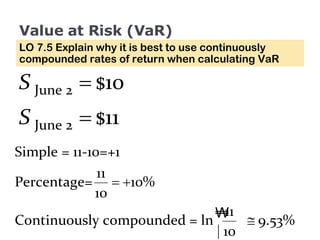

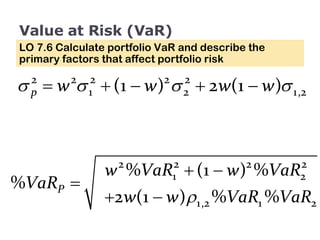

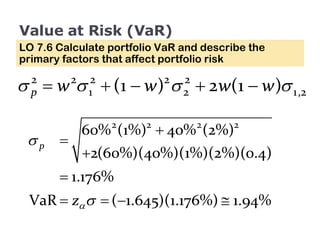

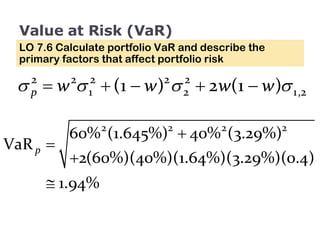

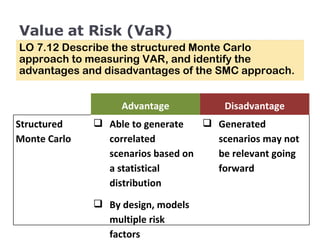

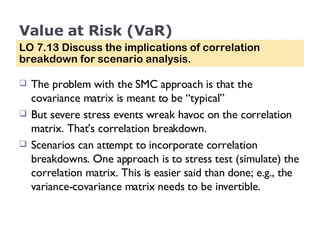

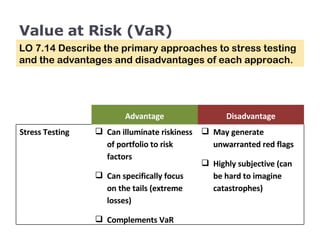

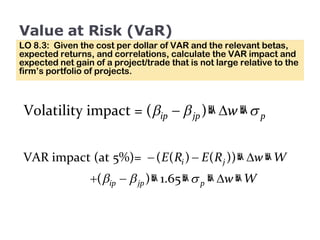

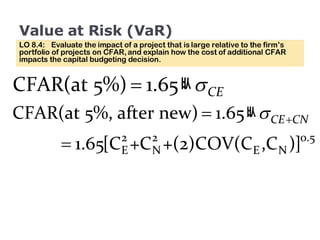

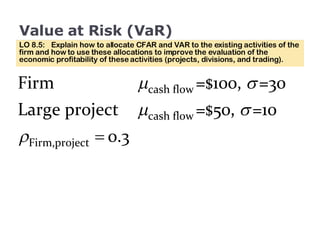

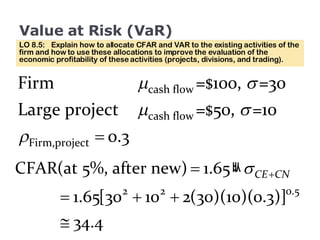

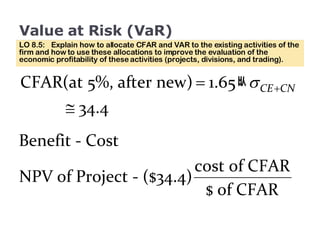

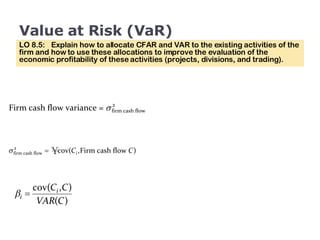

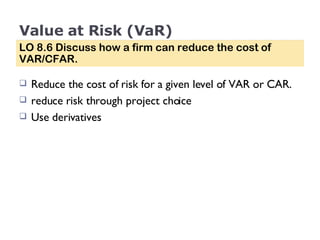

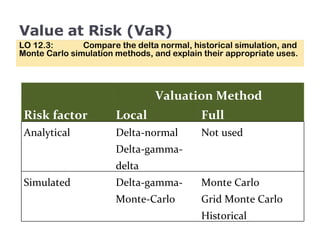

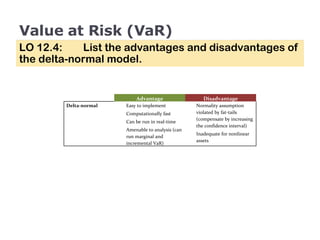

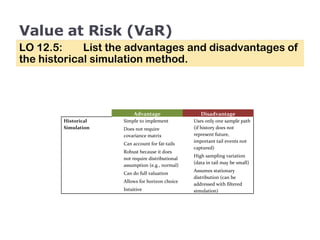

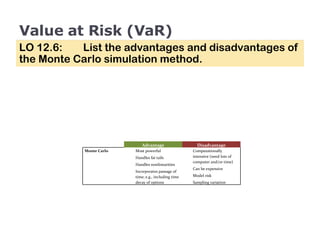

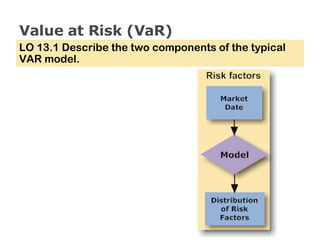

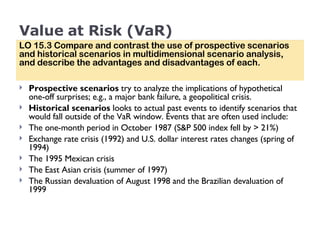

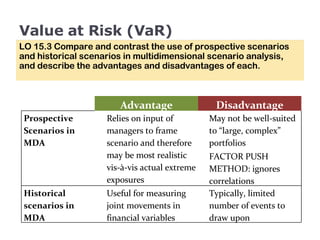

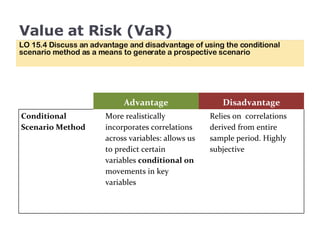

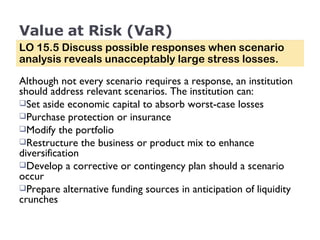

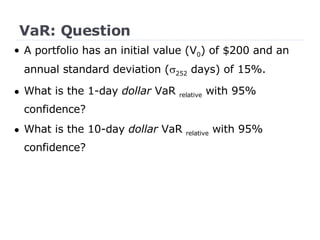

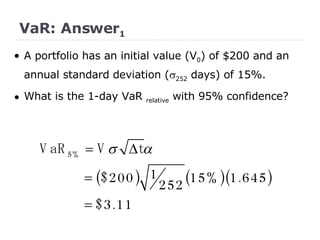

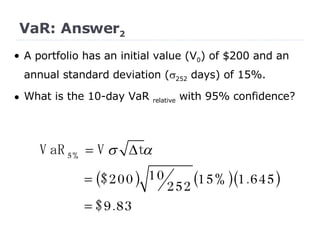

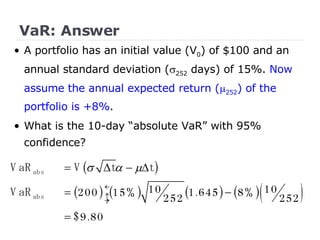

This document discusses Value at Risk (VaR) and related concepts over multiple learning outcomes (LOs). It introduces VaR and explains why it was widely adopted as a risk measure. It also defines how to calculate VaR for single and multiple assets, and how to convert between time periods. The document discusses assumptions of VaR calculations and reasons for using continuously compounded returns. It also addresses factors that affect portfolio risk and how to calculate VaR for linear and non-linear derivatives. Finally, it introduces cash flow at risk (CFaR) and how VaR and CFaR can be used to evaluate projects and allocate risk.

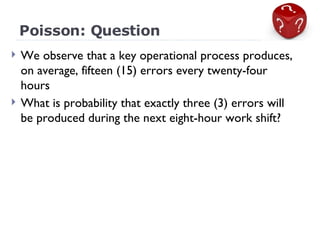

![Value at Risk (VaR) Absolute change (today’s price – yesterday’s price): violates stationarity requirement. Simple change ([today price – yesterday’s price] [yesterday’s price]): satisfies stationarity requirement, but violates time consistency requirement. Continuous compounded return is best because it satisfies the time consistency requirement: the 2-period return = sum of 1-period returns. The sum of two random variables that are jointly distributed is itself (i.e., the sum) normally distributed. LO 7.5 Explain why it is best to use continuously compounded rates of return when calculating VaR Except for interest rate variables: absolute ](https://image.slidesharecdn.com/value-at-risk-var-intro-1198113943735432-2/85/Value-at-Risk-VaR-Intro-28-320.jpg)

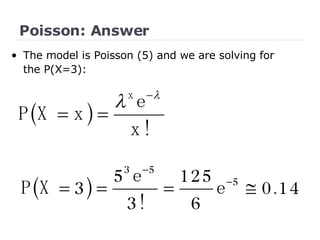

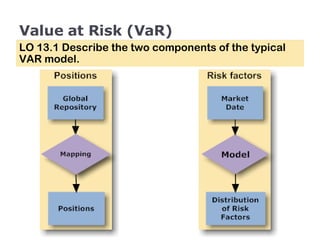

![Value at Risk (VaR) CFAR at p percent ( p %) is the cash flow shortfall (defined as expected cash flow minus [-] realized cash flow) such that there is a probability (%, percent) that the firm will have a larger cash flow shortfall. If realized, cash flow is C and expected cash flow is E ( C ), we have: LO 8.1 Calculate cash flow at risk for a firm with normally distributed cash flows for any period, given the expected return and volatility of firm value, and interpret the CFAR measure.](https://image.slidesharecdn.com/value-at-risk-var-intro-1198113943735432-2/85/Value-at-Risk-VaR-Intro-46-320.jpg)

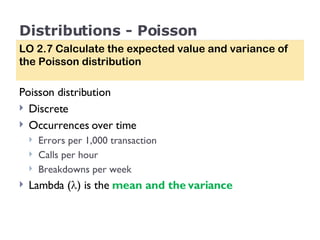

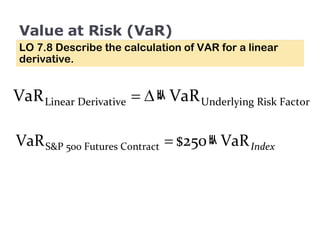

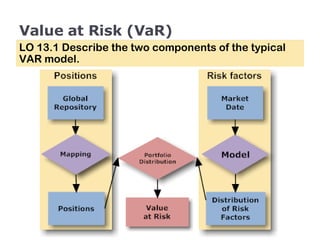

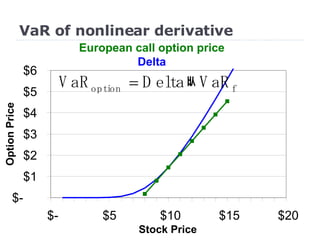

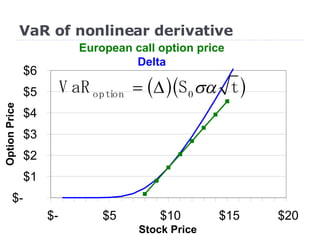

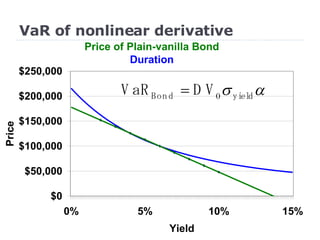

![VaR of nonlinear derivative • In the case of a linear derivative, the relationship between the derivative and the underlying asset is linear (delta, the “transmission parameter,” is constant) - Example: Futures contract on the S&P 500 Given that a futures contract is [$250 x Index], the VaR of the futures contract is: F t =250 VaR(S S&P 500 Index )](https://image.slidesharecdn.com/value-at-risk-var-intro-1198113943735432-2/85/Value-at-Risk-VaR-Intro-94-320.jpg)

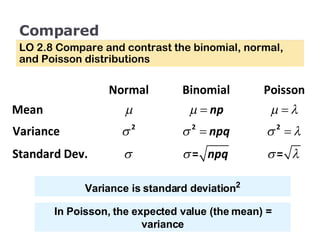

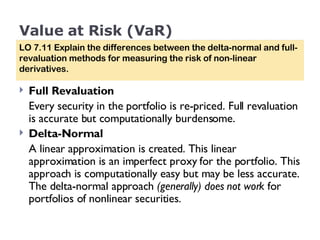

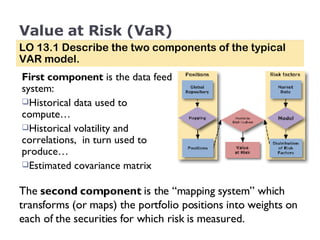

![Versus Full Re-value AIM: Explain the differences between the delta-normal and full-revaluation methods for measuring the risk of non-linear derivatives Delta-normal: linear approximation that assumes normality Option = F [Delta] Bond = F [Duration] Full-revaluation: linear approximation that assumes normality Computationally fast but… approximate Accurate but… computationally burdensome Re-price (simulate) the portfolio at several price levels](https://image.slidesharecdn.com/value-at-risk-var-intro-1198113943735432-2/85/Value-at-Risk-VaR-Intro-101-320.jpg)