Best VIP Call Girls Noida Sector 18 Call Me: 8448380779

Federal bank ru2 qfy2011-291010

1. Please refer to important disclosures at the end of this report 1

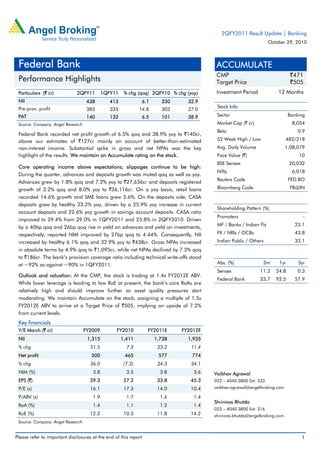

Particulars (` cr) 2QFY11 1QFY11 % chg (qoq) 2QFY10 % chg (yoy)

NII 438 413 6.1 330 32.9

Pre-prov. profit 385 335 14.8 303 27.0

PAT 140 132 6.5 101 38.9

Source: Company, Angel Research

Federal Bank recorded net profit growth of 6.5% qoq and 38.9% yoy to `140cr,

above our estimates of `127cr mainly on account of better-than-estimated

non-interest income. Substantial spike in gross and net NPAs was the key

highlight of the results. We maintain an Accumulate rating on the stock.

Core operating income above expectations; slippages continue to be high:

During the quarter, advances and deposits growth was muted qoq as well as yoy.

Advances grew by 1.8% qoq and 7.2% yoy to `27,636cr and deposits registered

growth of 3.2% qoq and 8.0% yoy to `36,116cr. On a yoy basis, retail loans

recorded 14.6% growth and SME loans grew 5.6%. On the deposits side, CASA

deposits grew by healthy 23.2% yoy, driven by a 25.9% yoy increase in current

account deposits and 22.6% yoy growth in savings account deposits. CASA ratio

improved to 29.4% from 29.0% in 1QFY2011 and 25.8% in 2QFY2010. Driven

by a 40bp qoq and 26bp qoq rise in yield on advances and yield on investments,

respectively, reported NIM improved by 27bp qoq to 4.44%. Consequently, NII

increased by healthy 6.1% qoq and 32.9% yoy to `438cr. Gross NPAs increased

in absolute terms by 4.9% qoq to `1,095cr, while net NPAs declined by 7.2% qoq

to `186cr. The bank’s provision coverage ratio including technical write-offs stood

at ~92% as against ~90% in 1QFY2011.

Outlook and valuation: At the CMP, the stock is trading at 1.4x FY2012E ABV.

While lower leverage is leading to low RoE at present, the bank’s core RoAs are

relatively high and should improve further as asset quality pressures start

moderating. We maintain Accumulate on the stock, assigning a multiple of 1.5x

FY2012E ABV to arrive at a Target Price of `505, implying an upside of 7.2%

from current levels.

Key financials

Y/E March (` cr) FY2009 FY2010 FY2011E FY2012E

NII 1,315 1,411 1,738 1,935

% chg 51.5 7.3 23.2 11.4

Net profit 500 465 577 774

% chg 36.0 (7.2) 24.3 34.1

NIM (%) 3.8 3.5 3.8 3.6

EPS (`) 29.3 27.2 33.8 45.3

P/E (x) 16.1 17.3 14.0 10.4

P/ABV (x) 1.9 1.7 1.6 1.4

RoA (%) 1.4 1.1 1.2 1.4

RoE (%) 12.2 10.3 11.8 14.2

Source: Company, Angel Research

ACCUMULATE

CMP `471

Target Price `505

Investment Period 12 Months

Stock Info

Sector Banking

Market Cap (` cr) 8,054

Beta 0.9

52 Week High / Low 482/218

Avg. Daily Volume 1,08,079

Face Value (`) 10

BSE Sensex 20,032

Nifty 6,018

Reuters Code FED.BO

Bloomberg Code FB@IN

Shareholding Pattern (%)

Promoters -

MF / Banks / Indian Fls 23.1

FII / NRIs / OCBs 43.8

Indian Public / Others 33.1

Abs. (%) 3m 1yr 3yr

Sensex 11.3 24.8 0.3

Federal Bank 33.7 92.5 57.9

Vaibhav Agrawal

022 – 4040 3800 Ext: 333

vaibhav.agrawal@angelbroking.com

Shrinivas Bhutda

022 – 4040 3800 Ext: 316

shrinivas.bhutda@angelbroking.com

2QFY2011 Result Update | Banking

October 29, 2010

Federal Bank

Performance Highlights

2. Federal Bank | 2QFY2011 Result Update

October 29, 2010 2

Exhibit 1: 2QFY2011 performance

Particulars (` cr) 2QFY11 1QFY11 % chg (qoq) 2QFY10 % chg (yoy)

Interest earned 978 952 2.8 901 8.6

Interest expenses 540 538 0.3 571 (5.5)

NII 438 413 6.1 330 32.9

Non-interest income 144 110 31.1 136 5.6

Operating income 582 523 11.3 466 24.9

Operating expenses 197 188 5.1 163 21.0

Pre-prov. profit 385 335 14.8 303 27.0

Provisions & cont. 170 133 27.7 150 13.4

PBT 215 202 6.3 153 40.2

Prov. for taxes 74 70 6.0 52 42.8

PAT 140 132 6.5 101 38.9

EPS (`) 8.2 7.7 6.5 5.9 38.9

Cost-to-income ratio (%) 33.9 35.9 35.0

Effective tax rate (%) 34.6 34.7 34.0

Net NPA (%) 0.7 0.7 0.5

Source: Company, Angel Research

Exhibit 2: 2QFY2011 Actual v/s Angel estimates

Particulars (` cr) Actual Estimates Var. (%)

Net interest income 438 413 6.0

Non-interest income 144 103 40.0

Operating income 582 516 12.8

Operating expenses 197 196 0.5

Pre-prov. profit 385 320 20.3

Provisions & cont. 170 127 33.9

PBT 215 193 11.4

Prov. for taxes 74 66 13.4

PAT 140 127 10.4

Source: Company, Angel Research

3. Federal Bank | 2QFY2011 Result Update

October 29, 2010 3

Advances and deposits growth below industry

For 2QFY2011, advances and deposits growth was muted on a qoq as well as yoy

basis. Advances grew by 1.8% qoq and 7.2% yoy to `27,636cr and deposits

registered growth of 3.2% qoq and 8.0% yoy to `36,116cr. On a yoy basis, retail

loans recorded 14.6% growth, SME loans grew 5.6% and corporate loans grew

marginally by 0.9%. While on a sequential basis, corporate loans registered a

3.0% decline, while SME and retail loans grew by 7.6% and 3.0%, respectively.

On the deposits side, CASA deposits grew by healthy 23.2% yoy, driven by a

25.9% yoy increase in current account deposits and 22.6% yoy growth in savings

account deposits. On a sequential basis, CASA deposits grew by 4.7% qoq on the

back of a 7.0% increase in current account deposits and 4.1% growth in savings

account deposits. CASA ratio improved to 29.4% from 29.0% in 1QFY2011 and

25.8% in 2QFY2010.

Driven by a 40bp qoq and 26bp qoq rise in yield on advances and yield on

investments, respectively, the reported NIM improved by 27bp qoq to 4.44%.

Consequently, NII increased by healthy 6.1% qoq and 32.9% yoy to `438cr. For

FY2011, management expects NIM to moderate to 3.7–3.8% from current levels.

Exhibit 3: Trend in advances and deposits

Source: Company, Angel Research

Exhibit 4: Trend in deposit-mix

Source: Company, Angel Research

Exhibit 5: Break-up of gross advances

Source: Company, Angel Research

69.5

73.3

77.1

75.3 74.7

77.6 76.5

60.0

66.0

72.0

78.0

84.0

-

10,000

20,000

30,000

40,000

4QFY09

1QFY10

2QFY10

3QFY10

4QFY10

1QFY11

2QFY11

Advances (` cr) Deposits (` cr) CD ratio (%, RHS)

4.5 4.8 4.8 4.9 5.1 5.4 5.6

20.0 21.3 21.0 21.0 21.1 23.6 23.8

75.5 73.9 74.2 74.1 73.8 71.0 70.6

0%

20%

40%

60%

80%

100%

4QFY09

1QFY10

2QFY10

3QFY10

4QFY10

1QFY11

2QFY11

CA SA Term Deposits

Large corporates

38%

SME

31%

Housing

18%

Gold loans

3%

Adv. against

sec./dep.

2%

Mortgage

1%

Home OD

2%

Vehicle

2%

Education

1%

Others

2%

Retail

31%

4. Federal Bank | 2QFY2011 Result Update

October 29, 2010 4

Strong recoveries drive non-interest income

Non-interest income registered growth of 31.1% qoq and 5.6% yoy to `144cr, in

spite of a 14.7% qoq and 51.8% yoy decline in treasury income. Growth in

non-interest income excluding treasury was healthy at 39.2% qoq and 21.3% yoy.

Growth in other income was driven by strong recoveries, which increased by

160.1% qoq and 66.8% yoy to `47cr compared to `18cr in 1QFY2011 and `28cr

in 2QFY2010. Commission, exchange and brokerage (CEB) income growth was

muted, in line with advances growth.

Exhibit 6: Recoveries drive growth in other income

Particulars (` cr) 2QFY11 1QFY11 % chg (qoq) 2QFY10 % chg (yoy)

CEB 29 28 5.4 29 1.5

Treasury 14 17 (14.7) 29 (51.8)

Forex 14 14 (1.4) 13 9.2

Recoveries 47 18 160.1 28 66.8

Others 40 34 19.1 38 6.4

Total 144 110 31.1 136 5.6

Source: Company, Angel Research

Operating costs under control

During the quarter, the bank’s operating expenses increased by 21.0% yoy, driven

by a 34.6% increase in employee costs and 4.4% increase in other operating

expenses. Cost-to-income ratio improved on the back of healthy operating

performance to 33.9% (from 35.9% in 1QFY2011 and 35.0% in 2QFY2010).

Exhibit 7: Trend in productivity

Source: Company, Angel Research

66

72

103

77

92

90

87

96

105

121

55

62

62

76

67

73

79

92

83

77

32.3

30.5 30.0

32.4

36.4 35.0

33.4 34.9 35.9

33.9

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

-

50

100

150

200

250

1QFY09

2QFY09

3QFY09

4QFY09

1QFY10

2QFY10

3QFY10

4QFY10

1QFY11

2QFY11

Staff exps (` cr) Other opex (` cr) Cost-to-income ratio (%, RHS)

5. Federal Bank | 2QFY2011 Result Update

October 29, 2010 5

Slippages still high

Gross NPAs increased in absolute terms by 4.9% qoq to `1,095cr, while net NPAs

declined by 7.2% qoq to `186cr. Gross NPA ratio deteriorated to 3.84% as against

3.73% in 1QFY2011, while net NPA ratio improved from 0.74% in 1QFY2011 to

0.68% in 2QFY2011. Gross slippages stood at `257cr (as against `327cr in

1QFY2011), indicating an annualised slippage ratio of 3.8% (4.8% in 1QFY2011).

Majority of the slippages were from the SME segment (`121cr), while the retail

loans segment witnessed slippages of `75cr, of which slippages of ~`60cr were

from the housing segment. Out of the outstanding gross NPAs, the SME loans

segment accounts for 45.2% and the retail and corporate loans segments account

for 33.1% and 21.7%, respectively. Management has indicated that it will take

about 4–6 quarters for the slippage rate to come down by 150–200bp.

Accordingly, we have conservatively increased our estimates for provision expenses

for FY2011 by 25.1% and for FY2012 by 9.9%. There could be an upside to our

earnings estimates from stronger-than-expected recoveries and upgrades (already

`126cr or 1.9% of advances in 2QFY2011) along with strong recoveries from fully

written-off accounts (already `47cr in 2QFY2011).

On the positive side, the bank’s provision coverage ratio including technical

write-offs remained strong at ~92% as against ~90% in 1QFY2011. The bank

restructured `103cr of its loans during the quarter, taking its cumulative

restructured loans to `1,243cr (4.5% of loans, 25.1% of net worth).

Exhibit 8: Trend in asset quality

Source: Company, Angel Research; Note: NPA coverage % excluding technical write-offs

The bank made provisions of `143cr towards NPAs in 2QFY2011, up 5.3% from

`136cr made in 1QFY2011. The bank had to provide for depreciation of `8cr on

investments compared to a write-back of `4cr in 1QFY2011 and `27cr in

2QFY2010. The bank also made provisions of ~`16cr on account of the second

pension option, of which total liability is estimated to be ~`145cr.

572

626

590

631

789

791

821

1,044

1,095

85

71

68

67

138

147

129

201

186

85.1

88.7 88.4 89.3

82.5 81.4

83.4

88.4

82.2

60.0

65.0

70.0

75.0

80.0

85.0

90.0

-

300

600

900

1,200

2QFY09

3QFY09

4QFY09

1QFY10

2QFY10

3QFY10

4QFY10

1QFY11

2QFY11

Gross NPAs (` cr) Net NPAs (` cr) Coverage ratio (%, RHS)

6. Federal Bank | 2QFY2011 Result Update

October 29, 2010 6

Exhibit 9: Break-up of provisions

Particulars (` cr) 2QFY11 1QFY11 % chg (qoq) 2QFY10 % chg (yoy)

NPA 143 136 5.3 159 (9.9)

Investment-related 8 (4) - (27) -

Others 20 2 1,071.9 18 8.7

Total 170 133 27.7 150 13.4

Source: Company, Angel Research

Comfortable capital adequacy (CAR)

The bank’s CAR was strong at 17.3% as compared to 17.9% in 1QFY2011.

Tier-I capital component was at 16.0%, constituting 92.6% of the total CAR.

Exhibit 10: Comfortable capital adequacy

Source: Company, Angel Research

Investment arguments

Healthy deposit mix

Federal Bank’s CASA deposits grew at a 20.4% CAGR during FY2005–10, leading

to a stable 25%+ CASA ratio. Further, a key differentiator for the bank is the

low-cost NRI deposits base, which constitutes 15.6% of total deposits. Thus,

effectively, low-cost deposits as a proportion of total deposits stand at around

45.0%, which are expected to underpin calculated NIM of about 3.6% in FY2012E,

even as the bank grows its advances faster than the industry to leverage its large

net worth.

Impact of Dubai crisis within manageable limits

The stock has been an underperformer due to concerns over the impact of the

Dubai crisis on the bank’s business model, which benefits meaningfully from

Middle East NRI clients. However, as indicated by the management, the bank has

a very low direct loan exposure of about `350cr (1.3% of loan book) to these

clients. Hence, the impact of the crisis on asset quality is expected to be within

manageable limits.

18.4 17.5 17.0 17.1

16.0 16.6 16.0

1.8

1.6

1.5 1.5

1.3

1.3

1.3

9.0

12.0

15.0

18.0

21.0

4QFY09

1QFY10

2QFY10

3QFY10

4QFY10

1QFY11

2QFY11

Tier-I CAR Tier-II CAR(%)

7. Federal Bank | 2QFY2011 Result Update

October 29, 2010 7

Reasonable valuations

At the CMP, the stock is trading at 1.4x FY2012E ABV. While lower leverage is

leading to low RoE at present, the bank’s core RoAs are relatively high and should

improve further as asset quality pressures start moderating. We maintain

Accumulate on the stock, assigning a multiple of 1.5x FY2012E ABV to arrive at a

Target Price of `505, implying an upside of 7.2% from current levels.

Exhibit 11: Key assumptions

Particulars (%)

Earlier estimates Revised estimates

FY2011E FY2012E FY2011E FY2012E

Credit growth 23.0 24.0 15.0 24.0

Deposit growth 23.0 24.0 15.0 24.0

CASA ratio 24.5 22.5 26.2 24.0

NIM 3.7 3.4 3.8 3.6

Other income growth 27.6 21.0 0.8 18.1

Growth in staff expenses 18.4 19.2 30.0 18.0

Growth in other expenses 18.4 19.2 5.0 18.0

Slippages 3.5 2.7 3.5 2.7

Coverage ratio 82.5 79.9 83.5 88.2

Treasury gain/(loss) (% of investments) 0.3 0.3 0.3 0.2

Source: Company, Angel Research

Exhibit 12: Change in estimates

Particulars (` cr)

FY2011E FY2012E

Earlier

estimates

Revised

estimates

% chg

Earlier

estimates

Revised

estimates

% chg

NII 1,727 1,738 0.7 1,984 1,935 (2.4)

Non-interest income 515 535 4.0 622 632 1.5

Operating income 2,241 2,273 1.4 2,606 2,567 (1.5)

Operating expenses 801 802 0.1 955 947 (0.9)

Pre-prov. profit 1,440 1,471 2.1 1,651 1,621 (1.8)

Provisions & cont. 480 600 25.1 412 453 9.9

PBT 960 871 (9.3) 1,239 1,168 (5.7)

Prov. for taxes 326 293 (10.1) 421 393 (6.6)

PAT 634 577 (8.9) 818 774 (5.3)

Source: Company, Angel Research

11. Federal Bank | 2QFY2011 Result Update

October 29, 2010 11

Research Team Tel: 022 - 4040 3800 E-mail: research@angeltrade.com Website: www.angeltrade.com

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make

investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this

document are those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify,

nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While

Angel Broking Limited endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory,

compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or

other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in

the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please

refer to the latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and

its affiliates may have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement Federal Bank

1. Analyst ownership of the stock No

2. Angel and its Group companies ownership of the stock No

3. Angel and its Group companies' Directors ownership of the stock No

4. Broking relationship with company covered No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors.

Ratings (Returns): Buy (> 15%) Accumulate (5% to 15%) Neutral (-5 to 5%)

Reduce (-5% to 15%) Sell (< -15%)