1. Market Outlook

India Research

October 21, 2010

Dealer’s Diary

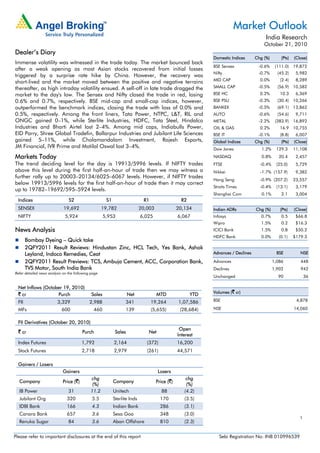

Domestic Indices Chg (%) (Pts) (Close)

Immense volatility was witnessed in the trade today. The market bounced back

BSE Sensex -0.6% (111.0) 19,872

after a weak opening as most Asian stocks recovered from initial losses

Nifty -0.7% (45.2) 5,982

triggered by a surprise rate hike by China. However, the recovery was

MID CAP 0.0% (2.4) 8,289

short-lived and the market moved between the positive and negative terrains

thereafter, as high intraday volatility ensued. A sell-off in late trade dragged the SMALL CAP -0.5% (56.9) 10,582

market to the day's low. The Sensex and Nifty closed the trade in red, losing BSE HC 0.2% 10.3 6,369

0.6% and 0.7%, respectively. BSE mid-cap and small-cap indices, however, BSE PSU -0.3% (30.4) 10,266

outperformed the benchmark indices, closing the trade with loss of 0.0% and BANKEX -0.5% (69.1) 13,862

0.5%, respectively. Among the front liners, Tata Power, NTPC, L&T, RIL and AUTO -0.6% (54.6) 9,711

ONGC gained 0–1%, while Sterlite Industries, HDFC, Tata Steel, Hindalco METAL -2.2% (383.9) 16,892

Industries and Bharti Airtel lost 2–4%. Among mid caps, Indiabulls Power, OIL & GAS 0.2% 16.9 10,755

EID Parry, Shree Global Tradefin, Ballarpur Industries and Jubilant Life Sciences BSE IT -0.1% (8.8) 6,007

gained 5–11%, while Cholamandalam Investment, Rajesh Exports, Global Indices Chg (%) (Pts) (Close)

JM Financial, IVR Prime and Motilal Oswal lost 3–4%. Dow Jones 1.2% 129.3 11,108

Markets Today NASDAQ 0.8% 20.4 2,457

The trend deciding level for the day is 19913/5996 levels. If NIFTY trades FTSE -0.4% (25.0) 5,729

above this level during the first half-an-hour of trade then we may witness a Nikkei -1.7% (157.9) 9,382

further rally up to 20003–20134/6025–6067 levels. However, if NIFTY trades

Hang Seng -0.9% (207.2) 23,557

below 19913/5996 levels for the first half-an-hour of trade then it may correct

Straits Times -0.4% (13.1) 3,179

up to 19782–19692/595–5924 levels.

Shanghai Com 0.1% 2.1 3,004

Indices S2 S1 R1 R2

SENSEX 19,692 19,782 20,003 20,134 Indian ADRs Chg (%) (Pts) (Close)

NIFTY 5,924 5,953 6,025 6,067 Infosys 0.7% 0.5 $66.8

Wipro 1.5% 0.2 $16.3

News Analysis ICICI Bank 1.5% 0.8 $50.2

HDFC Bank 0.0% (0.1) $179.3

Bombay Dyeing – Quick take

2QFY2011 Result Reviews: Hindustan Zinc, HCL Tech, Yes Bank, Ashok

Leyland, Indoco Remedies, Ceat Advances / Declines BSE NSE

2QFY2011 Result Previews: TCS, Ambuja Cement, ACC, Corporation Bank, Advances 1,086 448

TVS Motor, South India Bank Declines 1,902 942

Refer detailed news analysis on the following page

Unchanged 90 36

Net Inflows (October 19, 2010)

Volumes (` cr)

` cr Purch Sales Net MTD YTD

FII 3,329 2,988 341 19,264 1,07,586 BSE 4,878

MFs 600 460 139 (5,655) (28,684) NSE 14,060

FII Derivatives (October 20, 2010)

Open

` cr Purch Sales Net

Interest

Index Futures 1,792 2,164 (372) 16,200

Stock Futures 2,718 2,979 (261) 44,571

Gainers / Losers

Gainers Losers

chg chg

Company Price (`) Company Price (`)

(%) (%)

IB Power 31 11.2 Unitech 88 (4.2)

Jubilant Org 320 5.5 Sterlite Inds 170 (3.5)

IDBI Bank 166 4.3 Indian Bank 286 (3.1)

Canara Bank 657 3.6 Sesa Goa 348 (3.0)

1

Renuka Sugar 84 3.6 Aban Offshore 810 (2.3)

Please refer to important disclosures at the end of this report Sebi Registration No: INB 010996539

2. Market Outlook | India Research

Bombay Dyeing – Quick take

We believe that Bombay Dyeing (BD) monetising its legacy land bank in a timely manner

will be a key trigger for its stock performance. Moreover, ongoing recovery in its

manufacturing (textile and polyester units) business will act as an additional catalyst for the

stock. BD intends to develop 9.0msf of saleable area (1.0msf already developed) on its

historical mill land located in Central Mumbai over the next 8–10 years. For the

manufacturing business, the company has undertaken cost-reduction measures and

launched new products to turn profitable. Consequently, EBIT loss was lower for the textile

division at `14.4cr in 1HFY2011 v/s `22.3cr in 1HFY2010, while the polyester division

reported profit of `9.1cr in 1HFY2011 v/s loss of `39.6cr in 1HFY2010. The promoters

recently issued 4mn warrants at `527.83/share, which will increase their stake from 47.8%

to 52.7% post conversion. We have valued the real estate business at `940/share and the

manufacturing business at 0.5x of its asset value fetching `112/share. Hence,

we recommend a Buy rating on the stock with a Target Price of `894/share (implying 43%

upside from the current level), which is at 15% discount to our NAV..

Result Reviews – 2QFY2011

Hindustan Zinc

For 2QFY2011, Hindustan Zinc (HZL) reported a 20% yoy and 10.9% qoq increase in net

revenue to `2,163cr. Sales volume for zinc, lead and silver increased by 24.4%, 27.0%

and 25.8% yoy, respectively, to 175,309 tonnes, 14,458 tonnes, and 36,879 kg. Average

realisation for zinc, lead and silver increased by 12.9%, 7.5% and 36.2% yoy, respectively,

to US $2,176/tonne, US $2, 285/tonne and US $656/kg, respectively. The new 210Ktpa

zinc smelter contributed ~39,000 tonnes.

EBITDA margins declined by 807bp yoy to 52.0%, although flat on a qoq basis. The

decline was mainly due to a) higher stripping costs at mines, resulting in a 29.7% yoy

increase in mining expenses, b) 90% yoy increase in stores and spares cost and c) 46.8%

yoy increase in power costs on account of increased coal costs. Consequently, EBITDA

grew by 4.6% yoy to `1,125cr. Other income increased by 19.7% yoy to `184cr and

depreciation expense increased by `50.2% to `115.8cr. Consequently, net income grew by

only 1.5% yoy to `949cr.

HZL is expected to benefit from the expansion of zinc-lead smelting capacity and increased

silver production. In addition, HZL has a huge cash balance of `12,213cr at the end of the

quarter (`289 per share). We recommend an Accumulate rating on the stock with a revised

Target Price of `1,342 earlier (`1,227), valuing the stock at 6.0x FY12012E EV/EBITDA.

HCL Technologies – 1QFY2011

HCL Technologies reported its 1QFY2011 results. At the revenue front, in dollar terms,

numbers were ahead of the street as well as our expectations. The company’s revenue

came in at US $803.8mn, with growth of 9% qoq (v/s our expectation of US $792.5mn) on

the back of 7.87% volume growth in core software as well as 7.6% qoq constant currency

growth in infrastructure services. Cross-currency movement further aided growth by 1.6%

qoq. EBIT margins at 12.9% were in line with our expectation. PAT came in at `300.5cr v/s

our expectation of `269cr on the back of stronger growth, lower forex loss (`63.8cr v/s

expectation of `74cr) and lower effective tax rate.

The company is expected to be the outperformer in Tier-I IT pack in terms of volume

growth because of strong deal pipeline spanning across higher value-chain services. The

company is one of our preferred picks in the IT sector. At the CMP of `426, the stock is at

attractive valuations of 13.6x FY2012 EPS. We remain positive on the stock. The stock is

currently under review.

October 21, 2010 2

3. Market Outlook | India Research

Yes Bank

Yes Bank registered robust net profit growth of 57.8% yoy and 12.7% qoq to `176cr, well

above our estimates of `138cr on account of substantially higher balance sheet growth

than guided by the bank towards the beginning of the year. Advances grew strongly by

15.6% qoq and 86.3% yoy compared to marginal industry growth of ~0.6% qoq. Deposits

increased by 32.3% sequentially and by 106.6% yoy compared to ~1.6% sequential

industry growth. This led to 95.8% yoy growth in NII, despite a sequential NIM

compression of 10bp due to a higher-than-sector-average 40bp increase in cost of funds.

While we have been conservatively building in higher provisioning expenses for the bank,

keeping in view the sectoral averages, the bank continues to maintain its track record in

asset quality. Gross and net NPA ratios stood at 0.22% (0.23% in 1QFY2011) and 0.06%

(0.04% in 1QFY2011), respectively, implying a provision coverage ratio of 74.7%,

excluding write-offs (81.4% in 1QFY2011).

Corporate and institutional banking accounted for 69.8% of the portfolio, commercial

banking accounted for 19.6% and branch banking accounted for 10.6%. CASA deposits

registered strong growth of 118.9% yoy. However, CASA ratio declined to 10.1% from

10.5% in 1QFY2011. Operating costs increased by 35.9% yoy and 3.7% qoq to `163cr.

The cost-to-income ratio stood at 36.6%, lower than its eight-quarter average of 38.9%.

Restructured advances (excluding NPAs) declined by `11cr sequentially to `69cr. The

bank’s CAR continued to be healthy at 19.4% with Tier-I at 11.0%.

Considering the experience of the past several quarters, the inherent challenges of building a

retail franchise are substantial despite the management’s high pedigree. Moreover, with rising

interest rates, the cost of funds for the bank is expected to rise at a faster rate due to the bank’s

wholesale-based funding mix. That said, notwithstanding medium-term downside risks to RoAs

towards sectoral averages, the bank’s high rate of growth within the wholesale segment is likely

to drive strong earnings growth in the near term. At the CMP, the stock is trading at 2.7x

FY2012E ABV, which is below our target multiple of 2.9x FY2012E ABV for the bank.

Hence, we recommend Accumulate on the stock with a Target Price of `373.

Ashok Leyland

Ashok Leyland (ALL) reported 72% yoy top-line growth at `2,714cr, which was marginally

below our expectation of `2,788cr and largely aided by ~72% yoy jump in volumes. Net

average realisation for the quarter was flat on a yoy basis at `1,103,684 (`1,103,203 in

2QFY2010), largely due to lower growth in the non-cyclical business. EBITDA margins

came in 104bp ahead of our estimate at 11.3%, a jump of 126bp qoq and 76bp yoy.

Raw-material cost for the quarter increased by almost 460bp yoy. Higher commercial

vehicle volumes helped the company to improve its operating leverage and expand

EBITDA margins. Net profit grew by a substantial 88.5% yoy to `167cr (`89cr in

2QFY2010), as against our estimate of `157cr, largely aided by improved operating

performance.

At current levels, the stock is trading at 16x FY2011E and 13.2x FY2012E earnings.

We maintain our Neutral view on the stock. At present, our fair value for the stock works

out to be `78. We would be releasing a detailed result update post the earnings

conference call with management.

October 21, 2010 3

4. Market Outlook | India Research

Indoco Remedies

Indoco Remedies (Indoco) reported its 2QFY2011 results, which were ahead of our

estimates. Net sales came in at healthy `132cr (`95cr), up 38.7% yoy, as against our

estimates of `113cr. Growth was driven by the domestic formulation (up 37.2%, `88cr)

and export (up 39.0%, `40cr) segments. On the domestic front, growth was driven by the

respiratory, anti-infective and gastro segments. While on the export segment front, the

semi-regulated market grew by 140% to `8cr. The company reported gross margins of

54.2% (57.3%). Employee expenses increased by 28.2% yoy to `19cr (`15cr). The

company reported OPM of 13.4%, which was flat yoy. Indoco reported other income of

`3.1cr (`0.7cr), driven by exchange gain. While depreciation cost came in at `3cr. The

company reported net profit of `15cr (`9cr), up 65.9% yoy, driven by top-line growth.

Further, the company expanded its existing contract with Aspen and Watson, which would

commence meaningful contribution from FY2013. The stock is currently trading at 11.7x

FY2011E and 8.7x FY2012E earnings. The stock is under review.

Ceat

Ceat reported turnover of `843cr (`719cr) for 2QFY2011, up 17.1% yoy. The company’s

top line has been recovering following the uptick in OE volumes; however, during

1HFY2011 and 2QFY2011, capacity constraints restricted top-line growth. The company

posted operating profit of `43.9cr (`106.6cr) for 2QFY2011, a decline on both yoy and

qoq basis primarily due to the spurt in rubber prices, which resulted in a substantial

1,677bp yoy increase in raw-material cost at 69.2% (52.4%) of sales in 2QFY2011. OPM

for the quarter stood at 5.2% (14.8%). Net profit came in at `15.3cr (`61.5cr) for the

quarter. Higher input costs and increased interest and depreciation impacted the bottom

line, which fell by 75% yoy while increasing 10% qoq. In view of the apparent structural

shift that the tyre industry is going through, the stock is available at attractive valuations.

We retain our Buy rating on the stock with a Target Price of `205.

Result Previews – 2QFY2011

TCS

TCS is set to announce its 2QFY2011 results. We expect the company to post revenue of

US $1,927mn with 7.4% qoq growth on the back of volume growth of 8.1%, cross-

currency benefit of 0.55% and higher offshore effort. EBITDA margins are expected to be

flat at 29.3% as promotion cycles will take away the gains due to absorption of wage hike

in 1QFY2011, favourable currency and higher offshore effort. PAT is expected to be at

`1,990cr, with 7.9% qoq growth, on the back of strong revenue growth, maintained

profitability and lower forex losses. TCS remains to be our preferred pick amongst Tier-I IT

companies due to its strong capabilities in the financial services verticals with a broad

service portfolio and diversified geographical presence. At the CMP of `964, the stock is

trading at 20.5x FY2012E EPS of `47 with 7% upside to our Target Price of `1,032.

Ambuja Cements – 3QCY2010

We expect Ambuja Cements to report a 3.5% yoy decline in top line to `1,585cr on

account of a drop in realizations; however, the company’s despatches remained flat at

4.28mn tonnes. The OPM is expected to decline by 217bp yoy to 26.0%. Net profit is

expected to decline by 17.6% yoy to `263cr. We remain Neutral on the stock.

October 21, 2010 4

5. Market Outlook | India Research

ACC – 3QCY2010

We expect ACC to report a 16.7% yoy decline in top line to `1,671cr on account of a

decline in volumes and realisations. The company’s despatches were down by ~7% yoy

during the quarter. We expect the company’s OPM to decline by 1,565bp yoy to 19.4%.

Net profit is expected to decline by 56.6% yoy to `189cr. We remain Neutral on the stock.

Corporation Bank

Corporation Bank is slated to announce its 2QFY2011 results. The bank is expected to

post healthy yoy growth of 40.4% in net interest income (NII) to `707cr. Non-interest

income is expected to decline by 18.1% yoy. Provisioning expenses are expected to

increase by 51.7% yoy. Net profit is expected to be subdued at `303cr. We will be closely

watching slippages from the restructured loans of the bank, which stand at `2,811cr,

forming 46.0% of the net worth. At the CMP, the stock is trading at 1.3x FY2012E ABV of

`555. Currently, we have a Neutral rating on the stock.

TVS Motor 3472

TVS Motor is slated to announce its 2QFY2011 results. We expect the company’s top line

to grow by 41% yoy to `1,573cr on account of 33.4% yoy growth in volumes and higher

realisations. On the operating front, EBITDA margin is expected to expand by 134bp yoy

to 6.9%. Hence, the bottom line is expected to grow by 113.7% yoy to `52.5cr. The stock

rating is under review.

South Indian Bank

South Indian Bank is scheduled to announce its 2QFY2011 results today. The bank is

expected to post a muted Net Interest Income (NII) growth of 4.2% yoy and 2.8% qoq to

`172cr. Non-interest income is expected to decline by 45.4% yoy to `36cr. Provisions are

expected to be lower by 47.4% yoy. The net profit is expected to decline by 13.1% yoy but

it is expected to go up by 8.0% qoq to `63cr. At the CMP, the stock is trading at 1.5x

FY2012E ABV of `17. We have a Neutral rating on the stock.

October 21, 2010 5

6. Market Outlook | India Research

Economic and Political News

Govt. may invest `2,000cr more in Air India

Oil rebounds but stays below US $80 in Asian trade

SBI raises base rate by 10bp to 7.6%

Corporate News

BHEL bags solar power plant contract in Lakshadweep

SAIL seeks to rope in firms for power audit

Wockhardt Hospitals to invest `700cr to double capacity

Source: Economic Times, Business Standard, Business Line, Financial Express, Mint

Events for the day

ACC Results

Allahabad Bank Results

Alstom Projects Results

Ambuja Cements Results

Bajaj Corp Results

Ceat Results

Corporation Bank Results

Fresenius Kabi Results

Indiabulls Financial Services Results

JM Financial Results

Mahindra Forgings Results

Novartis India Results

Sasken Communication Technologies Results

SKF India Results

South Indian Bank Results

Sterlite Tech Results

TCS Results

TVS Motor Results

Wipro Results

Zensar Tech Results

October 21, 2010 6

7. Market Outlook | India Research

Research Team Tel: 022-4040 3800 E-mail: research@angeltrade.com Website: www.angeltrade.com

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make investment

decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this document are

those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable sources

believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this document is for

general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way responsible for any loss or

damage that may arise to any person from any inadvertent error in the information contained in this report. Angel Broking Limited has

not independently verified all the information contained within this document. Accordingly, we cannot testify, nor make any representation

or warranty, express or implied, to the accuracy, contents or data contained within this document. While Angel Broking Limited

endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory, compliance, or other

reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or other

advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and its affiliates may have

investment positions in the stocks recommended in this report.

Address: Acme Plaza, ‘A’ Wing, 3rd Floor, M.V. Road, Opp. Sangam Cinema, Andheri (E), Mumbai - 400 059.

Tel : (022) 3952 4568 / 4040 3800

Angel Broking Ltd: BSE Sebi Regn No : INB 010996539 / CDSL Regn No: IN - DP - CDSL - 234 - 2004 / PMS Regn Code: PM/INP000001546

Angel Capital & Debt Market Ltd: INB 231279838 / NSE FNO: INF 231279838 / NSE Member code -12798 Angel Commodities Broking (P) Ltd: MCX Member ID: 12685 / FMC Regn No: MCX / TCM /

CORP / 0037 NCDEX : Member ID 00220 / FMC Regn No: NCDEX / TCM / CORP / 0302

October 21, 2010 7