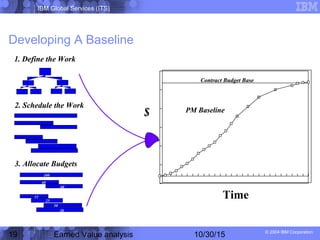

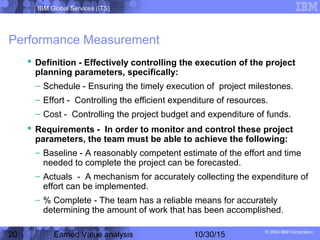

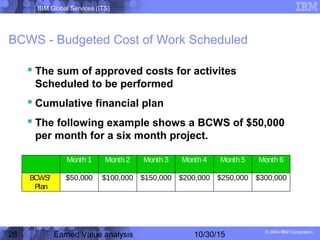

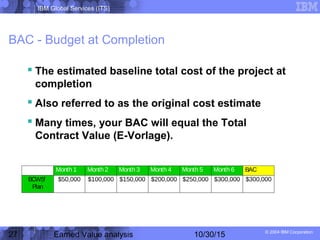

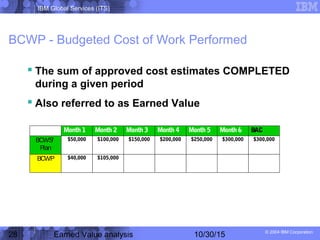

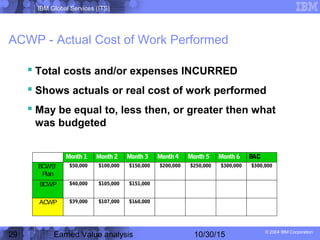

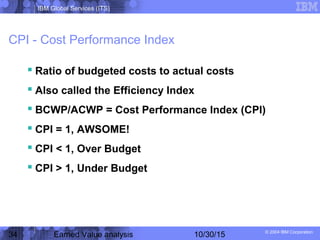

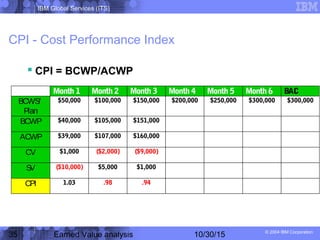

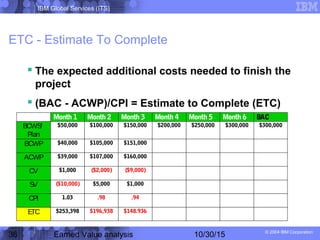

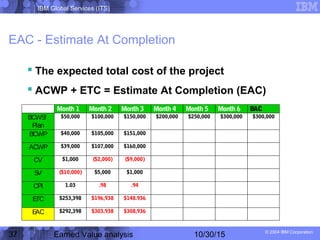

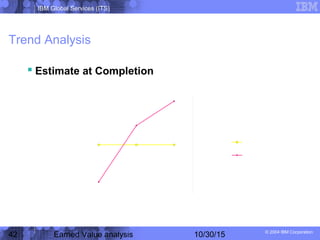

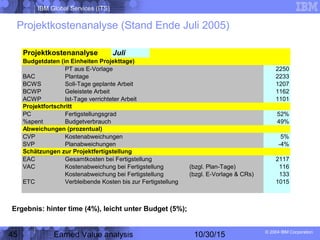

This document provides an overview of earned value analysis for project management. It defines key earned value terms and discusses how earned value can be used to enhance project performance by providing early awareness of potential issues. The document outlines an agenda for an earned value analysis training, including introducing earned value concepts and metrics, comparing forecasting methods, defining terminology, and providing a calculation example. It emphasizes that successful earned value implementation requires establishing a work breakdown structure, cost and schedule baselines, and processes for tracking progress and costs.

![IBM Global Services (ITS)

© 2004 IBM Corporation

9 Earned Value analysis 10/30/15

EV Management - Criteria for Success

Successful implementation of EV Management requires:

• Determine early if EV Management is going to be used and include

in all planning activities

• Define a WBS with clearly identifiable and measurable tasks

• [Include tasks in support of EV in the WBS and fund them]

• Schedule all work within required and achievable time frames

• Assign resources and costs/person days to each task

• Prepare baselines for budget and project plans

• Capture and monitor all project costs

• Track progress for scope, schedule, and budget

• [Adjust project management efforts as a result of EV analyses (i.e.

Recovery plans)]](https://image.slidesharecdn.com/earnedvalue-151030143606-lva1-app6892/85/Earned-value-9-320.jpg)

![IBM Global Services (ITS)

© 2004 IBM Corporation

58 Earned Value analysis 10/30/15

EVA Informationen (ungeprüft)

Bücher

Earned Value

Quentin W. Fleming & Joel M. Koppleman

Cost/Schedule Control Systems Criteria

Quentin W. Fleming

Project Performance Measurement

Robert R. Kemps

Visualizing Project Management

Kevin Forsberg, Ph.D., Hal Mooz and Howard

Cotterman

Software

Artemis Views

Artemis Management Systems

Contact: Patrick Perugini (303) 581-3102

Web: http://www.artemispm.com

Cobra

Welcom Software

Contact: Diana Melton (281) 558-0514

Web: http://www.wst.com

Software [Fortsetzung]

Dekker TRAKKER

Dekker Ltd.

Contact: Ron Barry (909) 384-9000

Web: http://www.dtrakker.com

MicroFrame Project Manager (MPM)

MicroFrame Technologies, Inc.

Contact: Carl Amacker (415) 616-4000

Web: http://www.microframe.com

Internet

Project Management Institute

http://www.pmi.org

US DoD Earned Value

http://www.acq.osd.mil/pm

Earned Value Bibliography

http://www.uwf.edu/~dchriste/ev-bib.html

Amazon.com

http://www.amazon.com](https://image.slidesharecdn.com/earnedvalue-151030143606-lva1-app6892/85/Earned-value-58-320.jpg)