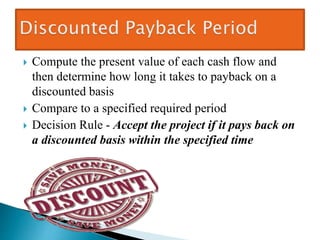

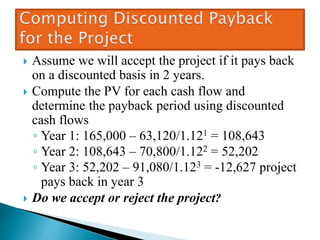

The document discusses various capital budgeting techniques including discounted payback period and net present value (NPV). It provides an example calculation of discounted payback period for a project that pays back in 3 years. While discounted payback includes the time value of money, it does not consider cash flows after the payback date or whether NPV is positive. NPV is described as the best measure as it directly shows whether a project will increase owner wealth by accounting for the time value of money and all cash flows. The internal rate of return (IRR) is also discussed as an alternative to NPV for evaluating projects.

![5) capital_budgeting_(1)_-(2)[1].ppt.pdf](https://cdn.slidesharecdn.com/ss_thumbnails/5capitalbudgeting121-250323135834-146732f6-thumbnail.jpg?width=640&height=640&fit=bounds)