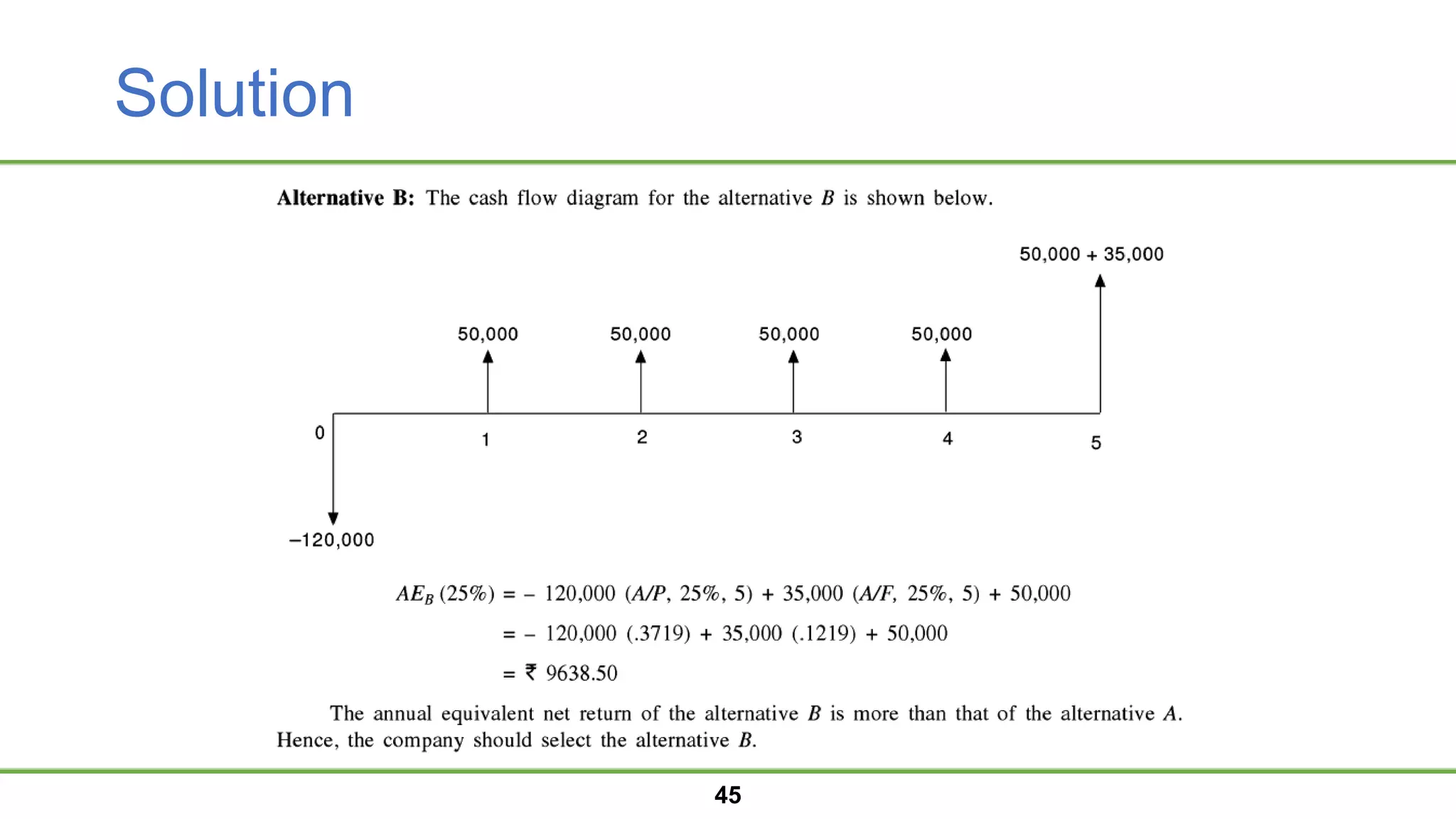

The document discusses capital budgeting, which is the process of planning and evaluating long-term investments. It covers key concepts like net present value (NPV), internal rate of return (IRR), payback period, and profitability index. The steps to capital budgeting are outlined as estimating cash flows, assessing risk, determining the cost of capital, and using methods like NPV and IRR to evaluate whether projects should be accepted. Examples are provided to illustrate how to calculate these metrics and address issues that can arise like mutually exclusive projects.

![5) capital_budgeting_(1)_-(2)[1].ppt.pdf](https://cdn.slidesharecdn.com/ss_thumbnails/5capitalbudgeting121-250323135834-146732f6-thumbnail.jpg?width=640&height=640&fit=bounds)