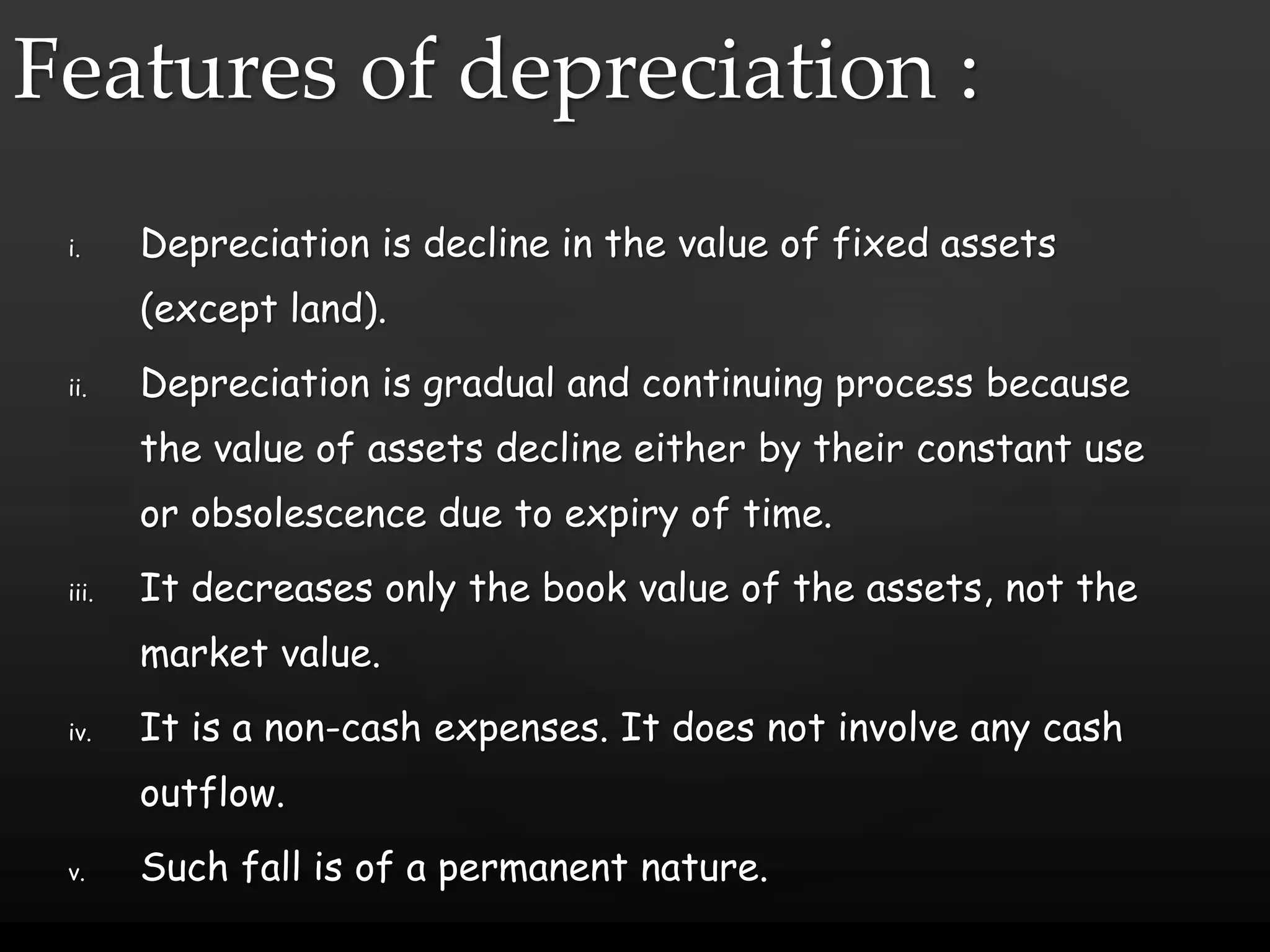

The document is a comprehensive guide on depreciation, outlining its meaning, causes, importance, and methods of allocation. It details both the straight line and written down value methods, illustrating calculations and accounting treatments with various examples. Acknowledgments are made to the teacher and parents, emphasizing the project's educational value.