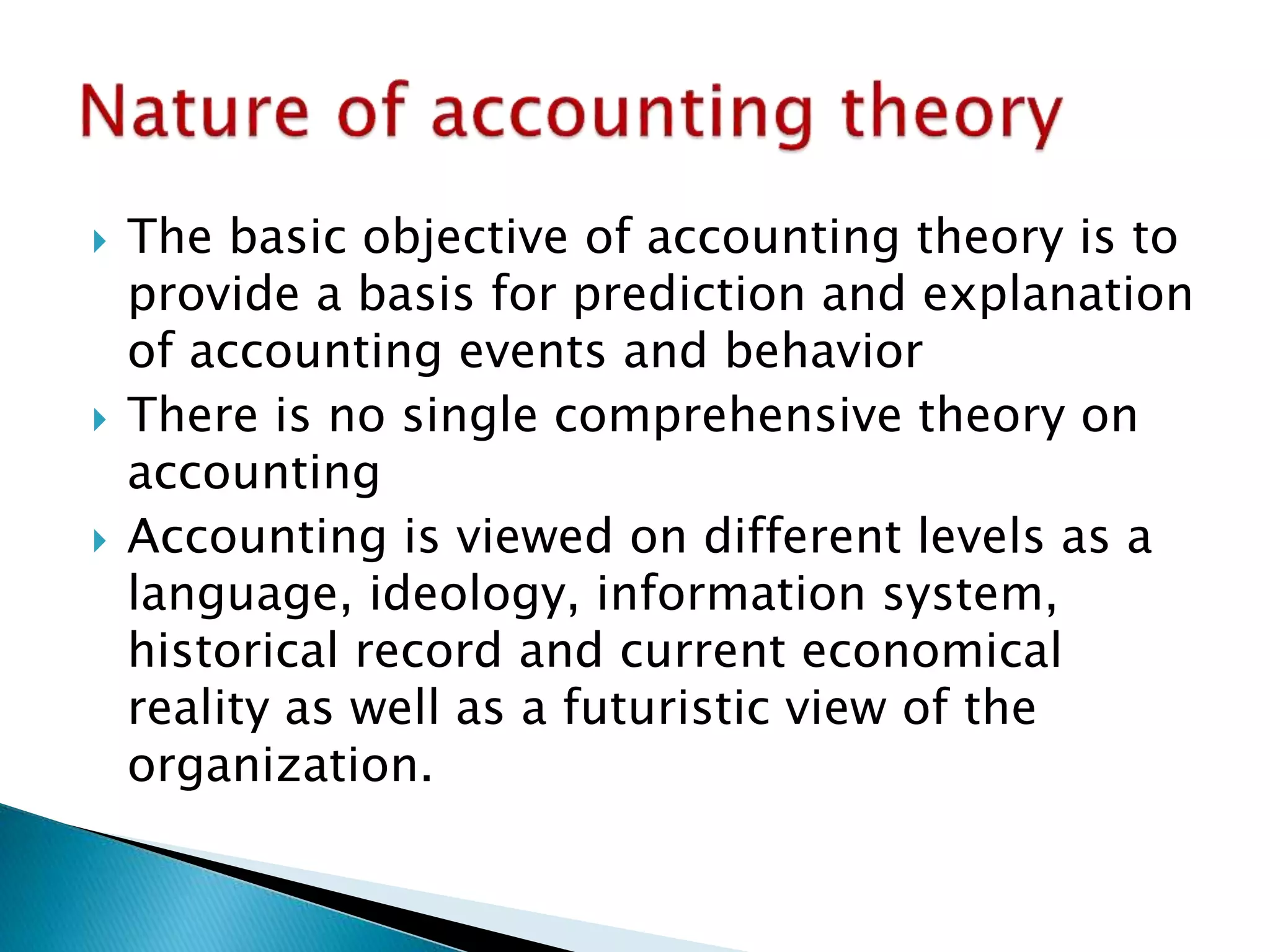

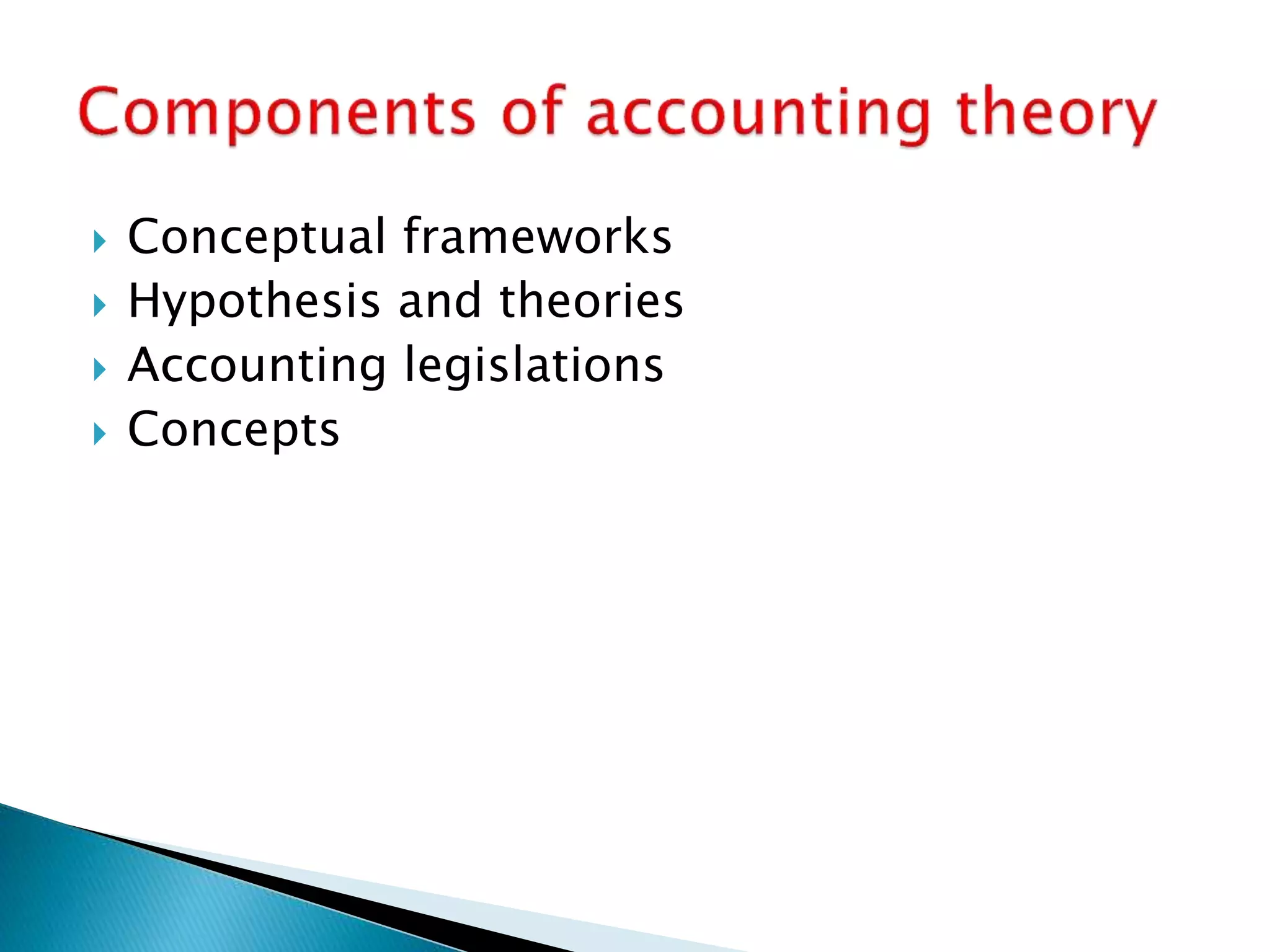

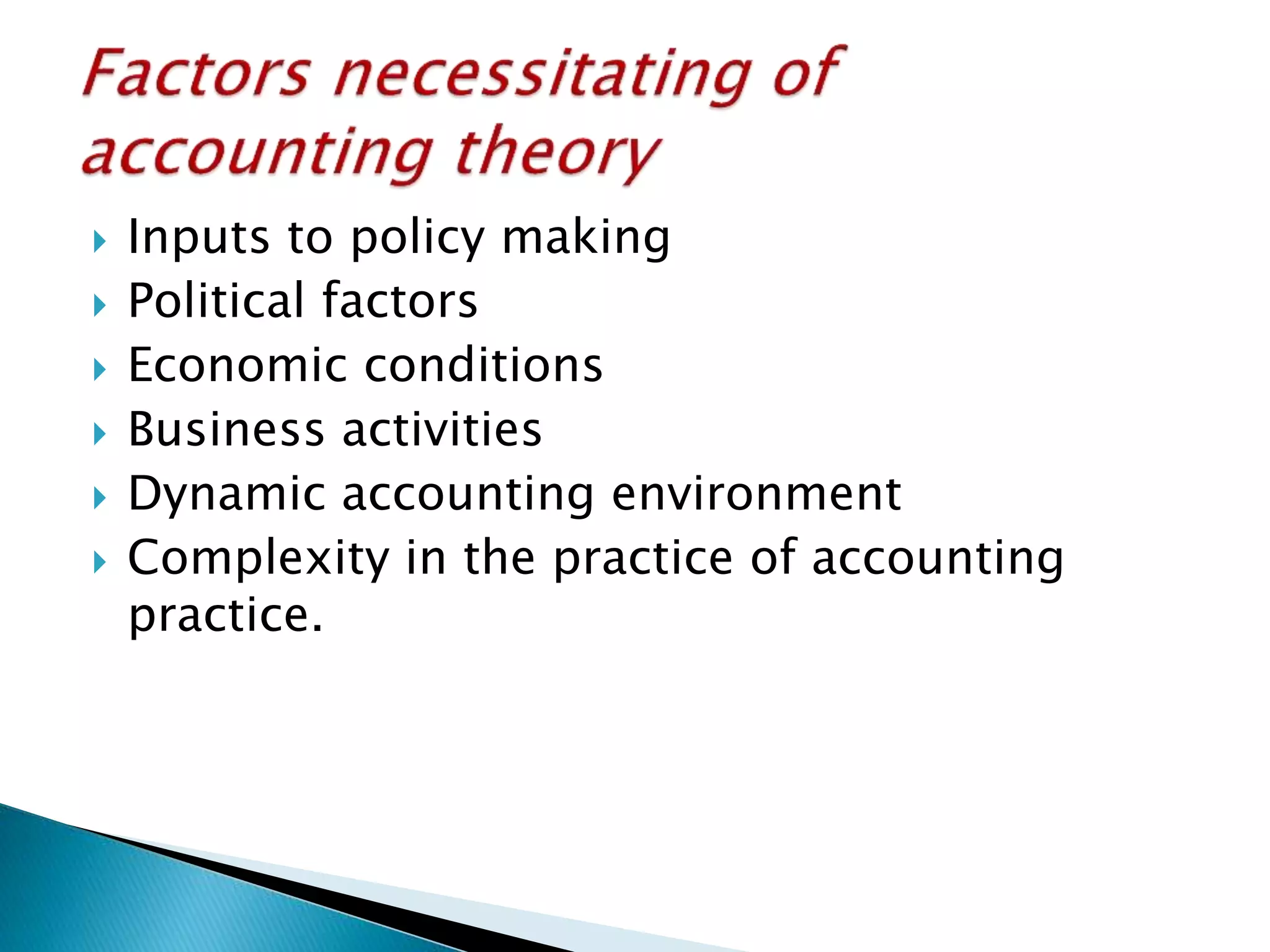

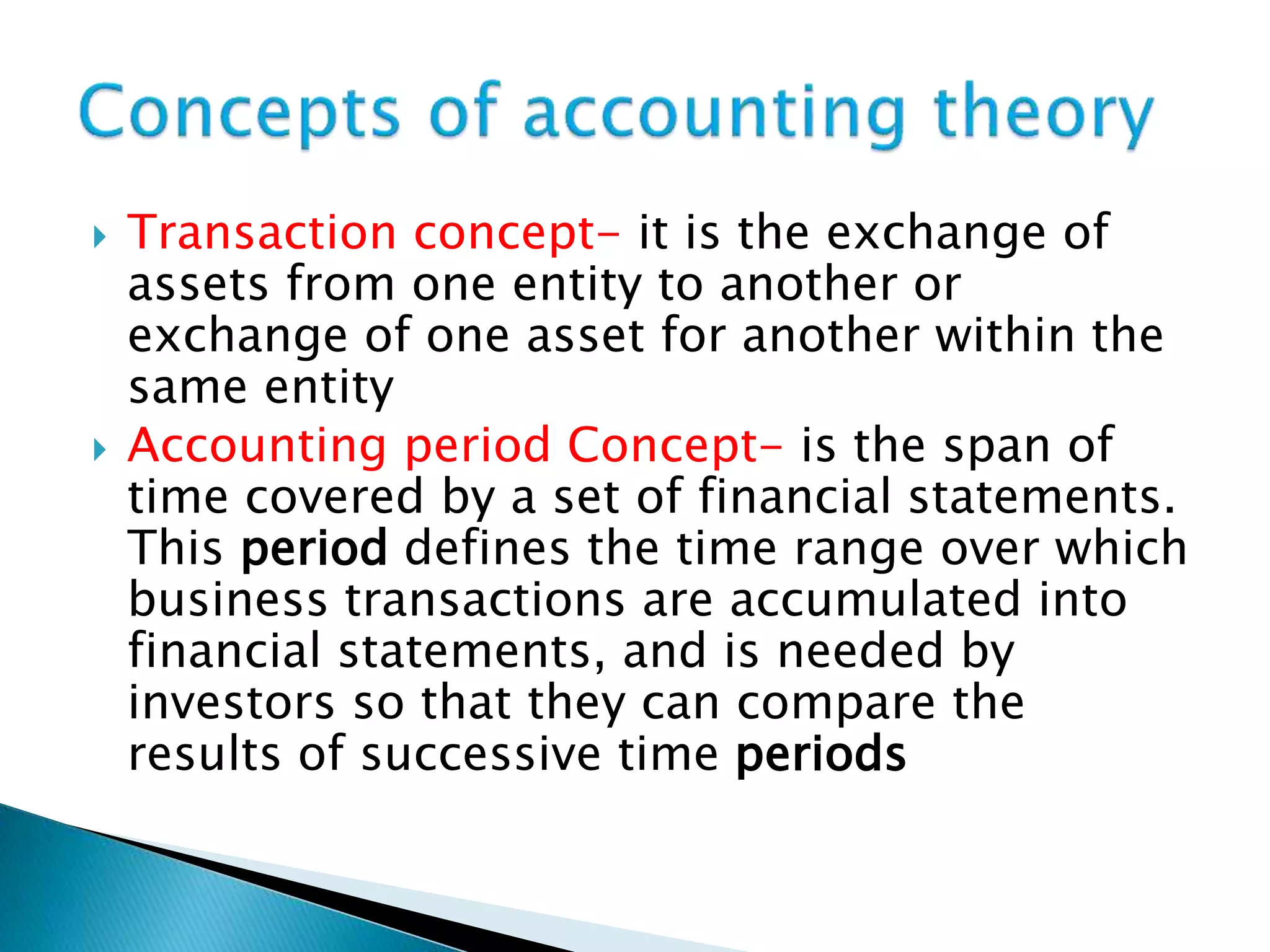

This document discusses accounting theory, which provides a logical framework for accounting practice and explains existing financial reporting rules and procedures. It outlines key concepts in accounting theory like the transaction concept and materiality concept. The document also discusses the objectives of accounting theory in providing a basis for predicting accounting behaviors and events. It notes that accounting theory has evolved from a focus on stewardship to incorporating financial reporting and management accounting. Various accounting standards bodies and their roles are also outlined.