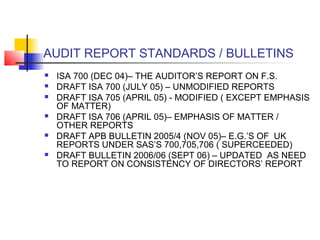

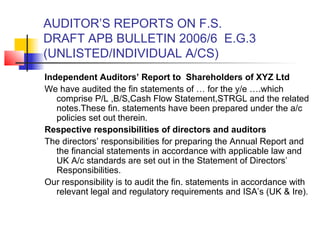

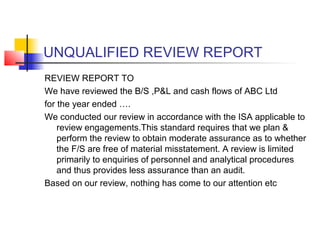

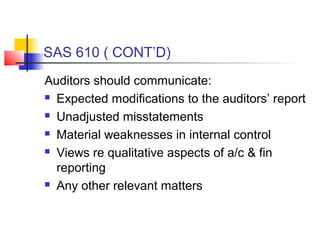

This document summarizes various audit reporting standards and bulletins. It includes examples of unmodified audit reports, modified reports that include disagreements, uncertainties and scope limitations, as well as emphasis of matter and other matter paragraphs. It also discusses auditor responsibilities in relation to listed company reporting and reviews of financial statements.