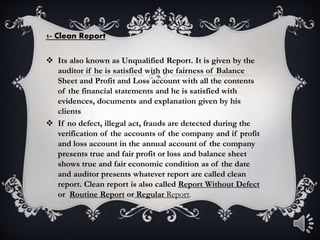

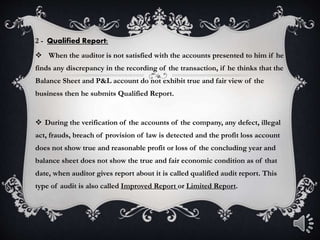

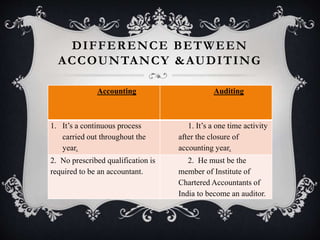

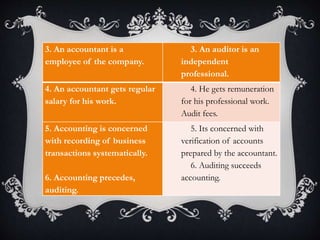

The document presents an audit report on the true and fair concept in accounting. It defines an audit report as a statement of collected facts that provides clear information to those without full knowledge. An auditor must verify accounts carefully and report whether they accurately present a company's true financial condition according to accounting principles. A true and fair report means accounts follow standards, transactions are properly classified, information is complete, and assets/liabilities are properly valued and reported. The document also distinguishes accounting from auditing and describes types of audit reports.

![AUDIT REPORT [ AUDITING ]](https://cdn.slidesharecdn.com/ss_thumbnails/auditingtypesofauditreport-210303052610-thumbnail.jpg?width=640&height=640&fit=bounds)