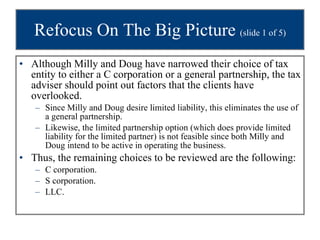

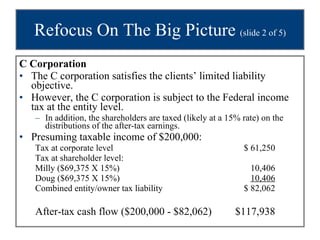

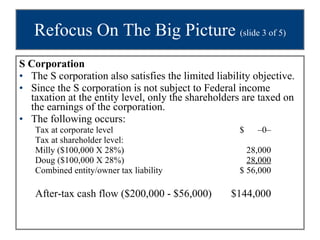

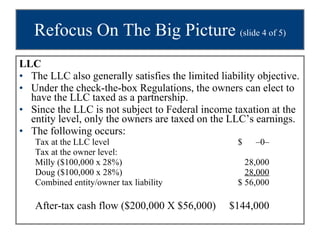

Milly and Doug are considering starting a dot-com business and need to choose between a C corporation or general partnership structure. They expect $200,000 in annual pre-tax earnings. As single filers with a 28% tax rate, an S corporation or LLC would minimize total taxes of $56,000, leaving $144,000 after-tax cash flow compared to $82,062 for a C corporation. The LLC offers additional flexibility over an S corporation.

![If you have any comments or suggestions concerning this PowerPoint Presentation for South-Western Federal Taxation, please contact: Dr. Donald R. Trippeer, CPA [email_address] SUNY Oneonta](https://image.slidesharecdn.com/chapter13presentation-110916132227-phpapp01/85/Chapter-13-presentation-70-320.jpg)