Downloaded 20 times

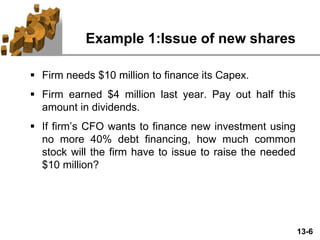

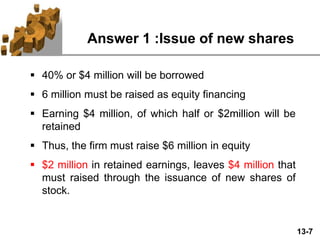

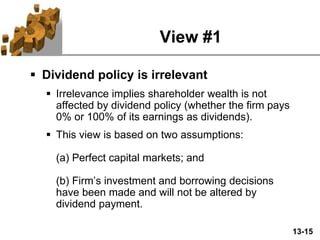

This document discusses dividend policy and internal financing. It describes the tradeoff between paying dividends and retaining profits, and how dividend policy affects stock prices. There are three views on the impact of dividends: that policy is irrelevant, that high dividends increase prices, or that low dividends increase prices. The document also outlines dividend payout ratios, procedures for paying dividends, and alternatives like stock dividends, splits, and repurchases.

![Fmch17[1]](https://cdn.slidesharecdn.com/ss_thumbnails/fmch171-211219052311-thumbnail.jpg?width=640&height=640&fit=bounds)

![Dividends and _dividend_policy_powerpoint_presentation[1]](https://cdn.slidesharecdn.com/ss_thumbnails/dividendsanddividendpolicypowerpointpresentation1-130929215028-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)