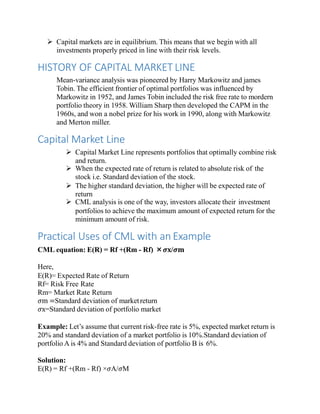

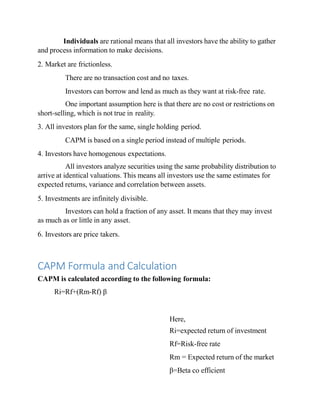

This document provides an overview of an upcoming presentation on asset pricing models. The presentation will cover capital market theory, the capital market line, security market line, capital asset pricing model, and diversification. It will discuss the assumptions and formulas for the capital market line and security market line. The capital market line shows expected returns based on portfolio risk, while the security market line shows expected individual asset returns based on systematic risk. The capital asset pricing model uses the concept of beta to calculate the expected return of an asset based on its risk relative to the market.