Downloaded 29 times

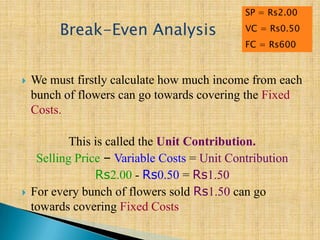

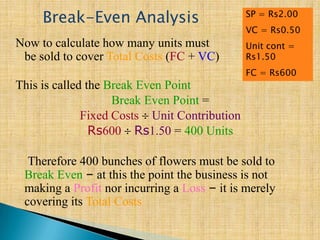

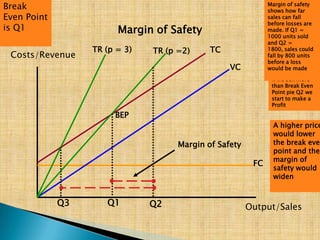

This document discusses break-even analysis, which examines the relationship between changes in volume, sales revenue, expenses, and net profit. It defines variable costs, fixed costs, total costs, contribution margin, break-even point, and margin of safety. An example is provided to illustrate how to calculate break-even point and margin of safety using fixed costs of Rs. 600, variable cost of Rs. 0.50 per unit, and selling price of Rs. 2 per unit. Limitations of break-even analysis are also outlined.

![Breakeven_Analysis_0[1].ppt](https://cdn.slidesharecdn.com/ss_thumbnails/breakevenanalysis01-220916071656-ab750b6d-thumbnail.jpg?width=640&height=640&fit=bounds)