Downloaded 66 times

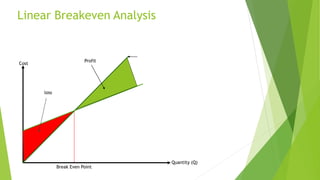

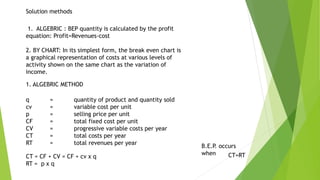

This document discusses break-even analysis, which is a method used to determine the minimum sales level required for a company to start making a profit. It examines the relationship between costs and sales volume. The break-even point is where total revenues equal total costs - there is no net profit or loss. Linear break-even analysis can graph costs and revenues at different production levels to determine the break-even point quantity. The document outlines algebraic and chart methods for calculating the break-even point quantity algebraically or graphically.