BGR Energy

•

1 like•214 views

BGR Energy Systems reported strong results for the first quarter of fiscal year 2011. Revenue grew 191% year-over-year to Rs. 905 crore, driven by execution of EPC projects. Net profit increased 205.6% to Rs. 61 crore. Margins were compressed due to higher raw material costs but execution of large EPC contracts provides good revenue visibility. The company maintains its neutral rating on BGR Energy Systems due to its order backlog, transformation into a full EPC provider through potential JV with Hitachi, and growth opportunities in the power sector.

Recommended

More Related Content

What's hot

Viewers also liked

Viewers also liked (17)

Similar to BGR Energy

More from Angel Broking

More from Angel Broking (20)

Recently uploaded

Recently uploaded (20)

BGR Energy

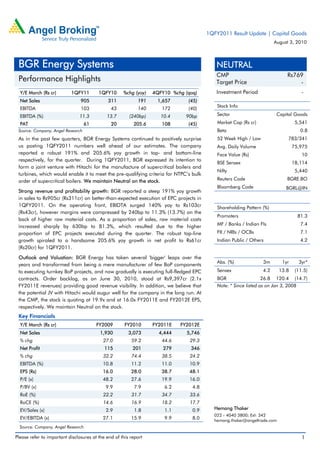

- 1. 1QFY2011 Result Update | Capital Goods August 3, 2010 BGR Energy Systems NEUTRAL CMP Rs769 Performance Highlights Target Price - Y/E March (Rs cr) 1QFY11 1QFY10 %chg (yoy) 4QFY10 %chg (qoq) Investment Period - Net Sales 905 311 191 1,657 (45) Stock Info EBITDA 103 43 140 172 (40) EBITDA (%) 11.3 13.7 (240bp) 10.4 90bp Sector Capital Goods PAT 61 20 205.6 108 (45) Market Cap (Rs cr) 5,541 Source: Company, Angel Research Beta 0.8 As in the past few quarters, BGR Energy Systems continued to positively surprise 52 Week High / Low 783/341 us posting 1QFY2011 numbers well ahead of our estimates. The company Avg. Daily Volume 75,975 reported a robust 191% and 205.6% yoy growth in top- and bottom-line Face Value (Rs) 10 respectively, for the quarter. During 1QFY2011, BGR expressed its intention to BSE Sensex 18,114 form a joint venture with Hitachi for the manufacture of supercritical boilers and Nifty 5,440 turbines, which would enable it to meet the pre-qualifying criteria for NTPC’s bulk order of supercritical boilers. We maintain Neutral on the stock. Reuters Code BGRE.BO Bloomberg Code BGRL@IN Strong revenue and profitability growth: BGR reported a steep 191% yoy growth in sales to Rs905cr (Rs311cr) on better-than-expected execution of EPC projects in 1QFY2011. On the operating front, EBIDTA surged 140% yoy to Rs103cr Shareholding Pattern (%) (Rs43cr), however margins were compressed by 240bp to 11.3% (13.7%) on the Promoters 81.3 back of higher raw material costs. As a proportion of sales, raw material costs increased sharply by 630bp to 81.3%, which resulted due to the higher MF / Banks / Indian Fls 7.4 proportion of EPC projects executed during the quarter. The robust top-line FII / NRIs / OCBs 7.1 growth spiraled to a handsome 205.6% yoy growth in net profit to Rs61cr Indian Public / Others 4.2 (Rs20cr) for 1QFY2011. Outlook and Valuation: BGR Energy has taken several 'bigger' leaps over the Abs. (%) 3m 1yr 3yr* years and transformed from being a mere manufacturer of few BoP components to executing turnkey BoP projects, and now gradually is executing full-fledged EPC Sensex 4.2 13.8 (11.5) contracts. Order backlog, as on June 30, 2010, stood at Rs9,397cr (2.1x BGR 26.8 120.4 (14.7) FY2011E revenues) providing good revenue visibility. In addition, we believe that Note: * Since listed as on Jan 3, 2008 the potential JV with Hitachi would augur well for the company in the long run. At the CMP, the stock is quoting at 19.9x and at 16.0x FY2011E and FY2012E EPS, respectively. We maintain Neutral on the stock. Key Financials Y/E March (Rs cr) FY2009 FY2010 FY2011E FY2012E Net Sales 1,930 3,073 4,444 5,746 % chg 27.0 59.2 44.6 29.3 Net Profit 115 201 279 346 % chg 32.2 74.4 38.5 24.2 EBITDA (%) 10.8 11.2 11.0 10.9 EPS (Rs) 16.0 28.0 38.7 48.1 P/E (x) 48.2 27.6 19.9 16.0 P/BV (x) 9.9 7.9 6.2 4.8 RoE (%) 22.2 31.7 34.7 33.6 RoCE (%) 14.6 16.9 18.2 17.7 EV/Sales (x) 2.9 1.8 1.1 0.9 Hemang Thaker 022 - 4040 3800; Ext: 342 EV/EBITDA (x) 27.1 15.9 9.9 8.0 hemang.thaker@angeltrade.com Source: Company, Angel Research Please refer to important disclosures at the end of this report 1

- 2. BGR Energy |1QFY2011 Result Update Exhibit 1: 1QFY2011 performance (Standalone) Y/E March (Rs cr) 1QFY2011 1QFY2010 yoy (%) 4QFY2010 qoq (%) FY2010 FY2009 yoy (%) Net Sales 905 311 191.0 1,657 (45.4) 3,069 1,922 59.7 Raw Material 736 234 215 1,382 (46.8) 2,487 1,579 57.5 (% of Net Sales) 81.3 75.1 83.4 81.0 82.2 Employee Cost 33 22 50.5 48 (32.3) 125 73 71.2 (% of Net Sales) 3.6 6.9 2.9% 4.1 3.8 Other Expenses 34 13 157.9 55 (37.6) 114 62 83.9 (% of Net Sales) 3.8 4.3 3.3 3.7 3.2 Total Expenditure 803 269 199 1,485 (45.9) 2,726 1,714 59.0 EBITDA 103 43 140 172 (40.1) 343 208 64.9 EBITDA (%) 11.3 13.7 10.4 11.2 10.8 Interest 12 16 (29.0) 12 - 54 58 (6.9) Depreciation 3 2 50.0 3 3.0 10 7 42.9 Other Income 3 6 (55.2) 7 25 32 (21.9) Profit before Tax 91 30 201.4 164 (44.7) 304 175 73.7 (% of Net Sales) 10.0 9.7 9.9 9.9 9.1 Total Tax 31 10 199.0 56 (44.5) 104 60 73.3 (% of PBT) 34.3 34.6 34.1 34.2 34.3 Reported PAT 61 20 205.6 108 (44.4) 200 115 73.9 (% of Net Sales) 6.6 6.3 6.5 (45.4) 6.5 6.0 8.9 Source: Company, Angel Research EPC segment strongly aided top-line: BGR has transformed itself over the years from being a mere manufacturer of a few BoP components to executing turnkey BoP projects, and is now gradually executing full-fledged EPC contracts. The company is riding on the back of two big EPC contracts namely 1*600MW EPC of a power plant at Mettur, Tamil Nadu worth Rs3,100cr, and second the 2*600MW EPC of a power plant at Kalisind TPS, Rajasthan, worth Rs4,900cr. For both these projects, BGR would be handling the BoP package at its level, while the BTG would be sourced from Dongfang, China. Both the projects have gathered pace in execution and have single-handedly contributed Rs644cr to the company’s 1QFY2011 revenues. August 3, 2010 2

- 3. BGR Energy |1QFY2011 Result Update Exhibit 2: Segment-wise performance (Standalone) Y/E March (Rs cr) 1QFY11 1QFY10 yoy % FY10 FY09 yoy % Revenues Capital Goods 27 17 58.6 168 191 (12.0) Construction and EPC 879 294 198.9 2,901 1,731 67.6 contracts Total Revenues 905 311 191.2 3,069 1,922 59.7 EBIT Capital Goods 0.2 1.83 (88.5) 21 16 31.3 Construction and EPC 100 39.21 156.1 318 190 67.4 contracts Total EBIT 101 41.04 145.2 339 206 64.6 Revenue Mix (%) Capital Goods 3.0 5 5.5 9.9 Construction and EPC 97.0 95 94.5 90.1 contracts EBIT Margin (%) Capital Goods 0.8 10.8 12.5 8.4 Construction and EPC 11.4 13.3 11.0 11.0 contracts Source: Company, Angel Research Segment-wise performance: During the quarter, the construction and EPC contracts division was the key driver, registering robust 198.9% yoy growth in top-line to Rs879cr (Rs279cr). Margins (EBIT) of the division however declined 190bp to 11.4% (13.3%) during 1QFY2011. On the other hand, the capital goods segment reported dismal margins of 0.8% (10.8%) despite the decent revenue growth of 58.6% yoy. Order book: The company’s order backlog for the quarter declined 13.6% yoy to Rs9,397cr. The power projects division orders constituted 93%, while the oil & gas division contributed 5% of the backlog. The company continues to see a strong bidding pipeline and expects strong growth opportunities. Exhibit 3: Quarterly order backlog 14,000 12,179 11,609 12,000 10,881 10,230 10,000 9,523 9,397 8,000 (Rs cr) 6,000 4,000 2,000 0 4QFY09 1QFY10 2QFY10 3QFY10 4QFY10 1QFY11 Source: Company, Angel Research August 3, 2010 3

- 4. BGR Energy |1QFY2011 Result Update Investment Arguments Power sector - A structural growth driver: The government has embarked on an ambitious plan of promoting "Power for all by 2012", and increasing the country’s per capita consumption of electricity to over 1,000 KWh by FY2012E. To this effect, the government has planned capacity addition of 78,700MW during the Eleventh Plan period. Assuming around 60% achievement rate, it would result in capacity addition of about 45-50GW. Pertinently, the scale gets even bigger for the Twelfth Plan, with a planned capacity addition of over 100GW. The share of thermal capacity, including both the Eleventh and Twelfth Plans, totals 134,893MW thereby necessitating BOP along with boiler turbine generator (BTG) needs. Typically, an average BoP work constitutes about 40% of the project cost. In this way, the 75,200MW of thermal capacity planned during the Twelfth Plan period alone throws up a potential BoP opportunity of Rs1,35,360cr (ie. ~Rs27,072cr of an average annual opportunity). Turnkey BoP - BGR's forte: BGR has its own set of competitive advantages to differentiate its offerings in the turnkey BoP space and hence it is one of the very few established players to offer complete turnkey BoP services. The company has a lot of in-house expertise, particularly with a strong in-house design and engineering team (~53% of the total employees), which gives control over cost, design and scheduling of projects. Besides, over the years, the company has augmented its product portfolio through a combination of in-house developments and strategic technological tie-ups with several international players. The company can currently manufacture about 50% of the BoP package requirements in-house, giving it an edge both in terms of cost and lesser sub-vendor management. Additionally, its proven track record in managing equipment and turnkey projects helps it to further strengthen its position vis-à-vis new entrants. EPC contracts - Transforming to the next level: The company has scaled up to the next level, having won two major EPC orders combined worth of Rs8,000cr. For both these orders, BGR would be handling the BoP package at its end, while the BTG would be sourced from Dongfang, China. Post operationalising of the potential JV with Hitachi, BGR would be able to fulfill the pre-qualifying criteria for NTPC’s bulk order of supercritical boilers, thereby transforming itself into a fully integrated EPC major with complete access to BTG equipment. Outlook and Valuation: BGR Energy has taken several 'bigger' leaps over the years and has transformed itself from being a mere manufacturer of few BoP components to executing turnkey BoP projects, and now executing full-fledged EPC contracts. The company’s order backlog, as on June 30, 2010, stood at Rs9,397cr (2.1x FY2011E revenues) providing good revenue visibility. In addition, we believe that the potential JV with Hitachi would augur well for the company in the long run. At the CMP of Rs769, the stock is quoting at 19.9x and at 16.0x FY2011E and FY2012E EPS, respectively. We maintain Neutral on the stock. August 3, 2010 4

- 5. BGR Energy |1QFY2011 Result Update Exhibit 4: Strong revenue growth 7,000 165.8 180 6,000 160 140 5,000 120 93.3 4,000 100 (Rs cr) (%) 3,000 80 59.2 44.6 60 2,000 27.0 29.3 40 1,000 20 - 0 FY2007* FY2008 FY2009 FY2010 FY2011E FY2012E Revenues (LHS) Growth (RHS) Source: Company, Angel Research; Note: *For 18 months Exhibit 5: Profitability trend 700 11.2 10.8 11.2 11.0 10.9 12.0 10.2 600 10.0 500 6.6 6.3 8.0 5.7 6.0 6.0 400 5.3 (Rs cr) 6.0 (%) 300 4.0 200 100 2.0 0 0.0 FY2007* FY2008 FY2009 FY2010 FY2011E FY2012E EBITDA (LHS) PAT (LHS) EBITDA% (RHS) PAT% (RHS) Source: Company, Angel Research; Note: *For 18 months Exhibit 6: One year forward P/E band 1,600 1,400 1,200 1,000 800 600 400 200 0 Dec-08 Dec-09 Apr-08 Aug-08 Apr-09 Aug-09 Apr-10 Aug-10 Oct-08 Oct-09 Feb-09 Feb-10 Jun-08 Jun-09 Jun-10 Share Price (Rs) 8x 16x 24x 32x Source: Company, Angel Research Exhibit 7: Angel EPS Forecast v/s consensus Year (%) Angel forecast Bloomberg consensus var. (%) FY2011E 38.7 38.1 1.6 FY2012E 48.1 48.9 (1.6) Source: Company, Bloomberg, Angel Research August 3, 2010 5

- 6. BGR Energy |1QFY2011 Result Update Exhibit 8: Peer valuation CMP Tgt Price Upside FY2012E FY2012E FY2010-12E FY2012E FY2012E Company Reco EPS CAGR (Rs) (Rs) (%) P/BV (x) P/E(x) RoCE (%) RoE (%) (%) ABB* Neutral 799 - - 5.0 23.8 35.3 22.3 20.8 Areva T&D* Sell 288 - - 5.9 20.3 11.3 17.6 22.2 BHEL Neutral 2,464 - - 4.9 19.0 21.5 30.4 28.6 BGR Energy Neutral 769 4.8 16.0 31 17.7 33.6 Accumulat Crompton Greaves 275 307 11.6 4.4 17.9 7.2 27.1 27.3 e Jyoti Structures Buy 154 215 39.6 1.8 9.3 21.4 19.3 20.6 KEC International Buy 490 648 32.2 2.3 9.8 22.3 18.9 26.2 Thermax Neutral 746 - - 5.3 19.9 30.9 31 29.5 Source: Company, Angel Research; Note: * December year ending August 3, 2010 6

- 7. BGR Energy |1QFY2011 Result Update Profit & Loss Statement Y/E March (Rs cr) FY2007 FY2008 FY2009 FY2010 FY2011E FY2012E Net Sales 787 1,521 1,930 3,073 4,444 5,746 Other operating - - - - - - income Total operating income 787 1,521 1,930 3,073 4,444 5,746 % chg 172.3 93.3 27.0 59.2 44.6 29.3 Total Expenditure 698 1,365 1,721 2,729 3,953 5,121 Net Raw Materials 628 1,279 1,584 2,489 3,610 4,682 Other Mfg costs 37 41 63 114 166 210 Personnel 33 45 74 126 178 230 Other - - - - - - EBITDA 88 155 209 344 491 625 % chg 227.9 75.7 34.5 64.8 42.6 27.3 (% of Net Sales) 11.2 10.2 10.8 11.2 11.0 10.9 Depreciation& 9 6 8 10 15 21 Amortisation EBIT 80 150 201 334 476 604 % chg 228.6 88.3 34.4 65.8 42.5 26.9 (% of Net Sales) 10.1 9.9 10.4 10.9 10.7 10.5 Interest & other 18 27 58 54 91 126 Charges Other Income 0 7 32 25 38 47 (% of PBT) 0.5 5.1 18.1 8.2 8.9 9.0 Others - - - - - - Recurring PBT 62 130 175 305 423 525 % chg 231.0 109.4 35.2 74.2 38.6 24.2 Extraordinary - - - - - - Expense/(Inc.) PBT (reported) 62 130 175 305 423 525 Tax 21 41 60 104 144 179 (% of PBT) 34.0 31.7 34.0 34.0 34.0 34.0 PAT (reported) 41 88 116 201 279 347 Add: Share of earnings - - - - - - of associate Less: Minority interest (1) 1 0 0 0 0 (MI) Prior period items - - - - - - PAT after MI (reported) 41 87 115 201 279 346 ADJ. PAT 41 87 115 201 279 346 % chg 212.5 110.8 32.2 74.4 38.5 24.2 (% of Net Sales) 5.3 5.7 6.0 6.6 6.3 6.0 Basic EPS (Rs) 38 12 16 28 39 48 Fully Diluted EPS (Rs) 6 12 16 28 39 48 % chg 212.5 110.8 32.2 74.4 38.5 24.2 August 3, 2010 7

- 8. BGR Energy |1QFY2011 Result Update Balance Sheet Y/E March (Rs cr) FY2007 FY2008 FY2009 FY2010 FY2011E FY2012E SOURCES OF FUNDS Equity Share Capital 11 72 72 72 72 72 Preference Capital - - - - - - Reserves& Surplus 72 402 492 634 829 1,091 Shareholders Funds 83 474 564 706 901 1,163 Minority Interest 2 3 3 3 3 3 Total Loans 246 503 709 934 1,334 1,634 Deferred Tax Liability - 36 75 155 155 155 Total Liabilities 331 1,015 1,350 1,798 2,393 2,955 APPLICATION OF FUNDS Gross Block 63 73 125 190 269 368 Less: Acc. Depreciation 25 21 27 37 52 73 Net Block 38 53 98 153 217 295 Capital Work-in-Progress 3 1 5 3 4 5 Goodwill 0 1 1 1 1 1 Investments 0 151 1 1 1 1 Current Assets 583 1,333 2,569 3,770 4,534 5,695 Cash 93 307 615 1,028 1,061 1,212 Loans & Advances 88 266 643 727 889 1,149 Other 4 9 18 18 27 34 Current liabilities 295 524 1,323 2,129 2,363 3,041 Net Current Assets 289 809 1,246 1,641 2,171 2,654 Mis. Exp. not written off - - - - - - Total Assets 331 1,015 1,350 1,798 2,393 2,955 August 3, 2010 8

- 9. BGR Energy |1QFY2011 Result Update Cash Flow Statement Y/E March FY2007 FY2008 FY2009 FY2010 FY2011E FY2012E Profit before tax 62 130 175 305 423 525 Depreciation 9 6 8 10 15 21 (Inc)/Dec in Working Capital (107) (306) (129) 18 (497) (332) Less: Other income 0 7 32 25 38 47 Direct taxes paid 22 15 20 104 144 179 Cash Flow from Operations (59) (192) 1 205 (241) (12) (Inc.)/Dec.in Fixed Assets (28) (8) (55) (63) (80) (100) (Inc.)/Dec. in Investments 5 (151) 151 - - - Other income 0 7 32 25 38 47 Cash Flow from Investing (23) (153) 127 (38) (42) (53) Issue of Equity - 320 - - - - Inc./(Dec.) in loans 160 256 206 225 400 300 Dividend Paid (Incl. Tax) 4 17 25 59 84 84 Others 1 (0) (1) 80 - - Cash Flow from Financing 156 559 181 166 316 216 Inc./(Dec.) in Cash 75 214 308 413 33 151 Opening Cash balances 18 93 307 615 1,028 1,061 Closing Cash balances 93 307 615 1,028 1,061 1,212 August 3, 2010 9

- 10. BGR Energy |1QFY2011 Result Update Key Ratios Y/E March FY2007 FY2008 FY2009 FY2010 FY2011E FY2012E Valuation Ratio (x) P/E (on FDEPS) 134.2 63.7 48.2 27.6 19.9 16.0 P/CEPS 110.5 59.9 45.2 26.3 18.9 15.1 P/BV 67.1 11.7 9.9 7.9 6.2 4.8 Dividend yield (%) 0.4 0.3 0.4 0.9 1.3 1.3 EV/Sales 7.3 3.7 2.9 1.8 1.1 0.9 EV/EBITDA 64.6 36.1 27.1 15.9 9.9 8.0 EV/Total Assets 17.3 5.5 4.2 3.0 2.0 1.7 Per Share Data (Rs) EPS (Basic) 38.4 12.1 16.0 28.0 38.7 48.1 EPS (fully diluted) 5.8 12.1 16.0 28.0 38.7 48.1 Cash EPS 7.0 12.9 17.1 29.4 40.8 51.0 DPS 3.0 2.0 3.0 7.0 10.0 10.0 Book Value 11.5 65.8 78.3 98.1 125.1 161.5 Dupont Analysis EBIT margin (%) 10.1 9.9 10.4 10.9 10.7 10.5 Tax retention ratio 0.7 0.7 0.7 0.7 0.7 0.7 Asset turnover (x) 4.5 3.8 3.0 4.1 4.2 3.7 ROIC (Post-tax) (%) 29.8 25.8 20.6 29.3 29.9 25.9 Cost of Debt (Post 7.1 4.9 6.3 4.3 5.3 5.6 Tax) (%) Leverage (x) 1.8 0.1 0.2 (0.1) 0.3 0.4 Operating RoE (%) 71.7 27.7 22.9 26.0 37.3 33.3 Returns (%) RoCE (Pre-tax) 34.0 22.3 17.0 21.2 22.7 22.6 Angel RoIC (Pre-tax) 45.7 38.0 31.4 44.7 45.5 39.4 RoE 63.1 31.4 22.2 31.7 34.7 33.6 Turnover ratios (x) Asset Turnover (Gross 15.6 22.2 19.5 19.6 19.4 18.1 Block) Inventory / Sales 11 5 3 2 2 2 (days) Receivables (days) 113 133 190 194 185 184 Payables (days) 29 46 71 92 90 88 Working capital cycle 91 120 119 73 91 92 (ex-cash) (days) Solvency ratios (x) Net debt to equity 1.8 0.1 0.2 (0.1) 0.3 0.4 Net debt to EBITDA 1.7 0.3 0.4 (0.3) 0.6 0.7 Interest Coverage 4.4 5.6 3.5 6.2 5.2 4.8 (EBIT / Interest) August 3, 2010 10

- 11. BGR Energy |1QFY2011 Result Update Research Team Tel: 022 - 4040 3800 E-mail: research@angeltrade.com Website: www.angeltrade.com DISCLAIMER This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and risks of such an investment. Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this document are those of the analyst, and the company may or may not subscribe to all the views expressed within. Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's fundamentals. The information in this document has been printed on the basis of publicly available information, internal data and other reliable sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this document is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report. Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While Angel Broking Limited endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory, compliance, or other reasons that prevent us from doing so. This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced, redistributed or passed on, directly or indirectly. Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in the past. Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in connection with the use of this information. Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and its affiliates may have investment positions in the stocks recommended in this report. Disclosure of Interest Statement BGR Energy 1. Analyst ownership of the stock No 2. Angel and its Group companies ownership of the stock No 3. Angel and its Group companies' Directors ownership of the stock No 4. Broking relationship with company covered No Note: We have not considered any Exposure below Rs 1 lakh for Angel, its Group companies and Directors. Ratings (Returns) : Buy (> 15%) Accumulate (5% to 15%) Neutral (-5 to 5%) Reduce (-5% to 15%) Sell (< -15%) August 3, 2010 11