Downloaded 268 times

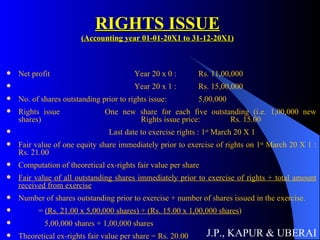

![RIGHTS ISSUE (CONTD.) Computation of adjustment factor = Fair value per share prior to exercise of rights = Rs. 21.00 = 1.05 Theoretical ex-rights value per share Rs. 20.00 Computation of earnings per share Year 20 X 0 Year 20 x 1 EPS for the year 20 x 0 as originally reported : Rs. 2.20 [Rs. 11,00,000 / 5,00,000 shares] EPS for the year 20 x 0 restated for rights Rs. 2.10 [Issue : Rs. 11,00,000 / (5,00,000 shares x 1.05)] EPS for the year 20 x 1 including effects of rights issue Rs. 2.55 Rs. 15,00,000 (5,00,000 x 1.05 x 2/12) + (6,00,000 x 10/12) J.P., KAPUR & UBERAI](https://image.slidesharecdn.com/as-20-100306060522-phpapp02/85/As-20-13-320.jpg)

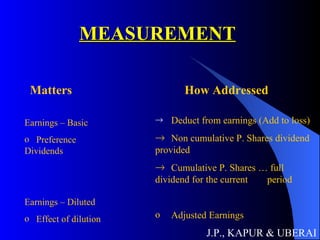

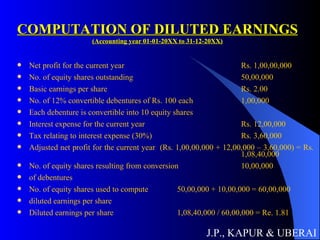

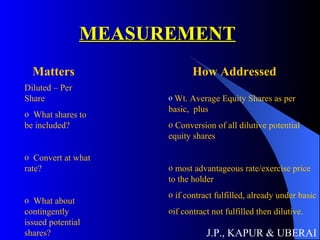

This document discusses Accounting Standard 20 on Earnings Per Share. It outlines how to calculate basic and diluted EPS, including determining the weighted average number of shares, adjusting for rights issues, and the treatment of convertible instruments. Basic EPS is calculated by dividing earnings by the weighted average number of equity shares outstanding. Diluted EPS considers all dilutive potential equity shares. Disclosures required include reconciliations of EPS numerators and denominators.