Downloaded 458 times

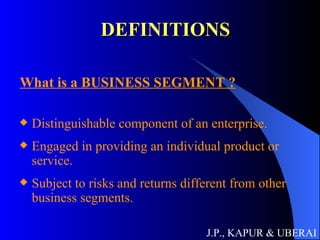

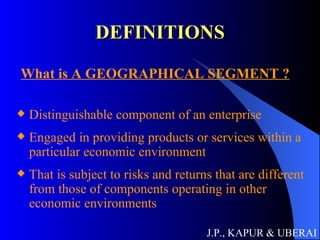

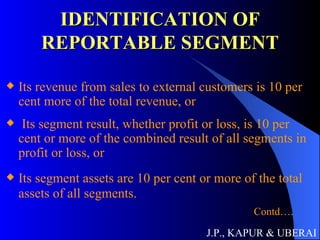

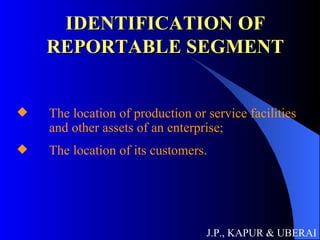

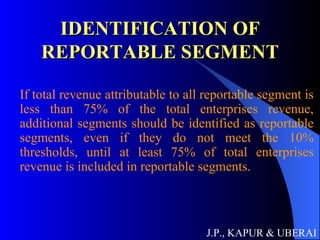

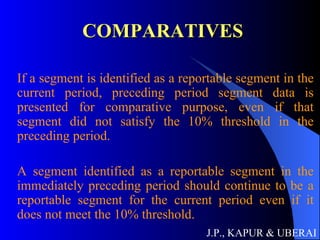

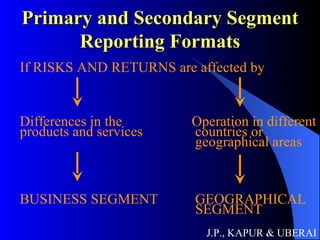

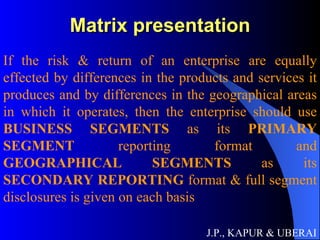

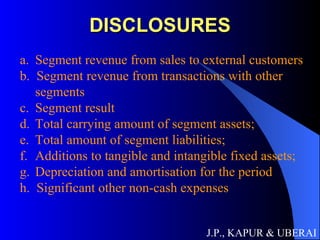

Accounting Standard 17 outlines requirements for segment reporting in financial statements. It requires companies to report financial information for different business segments and geographical segments. Applicable to listed companies and unlisted companies with annual turnover over Rs. 50 crores from April 2001. A business segment is a distinguishable component engaged in providing an individual product or service subject to different risks and returns. A geographical segment provides products/services in a particular economic environment subject to different risks and returns. Reportable segments meet certain thresholds for revenue, profit/loss, or assets. At least 75% of total revenue should be included in reportable segments. Comparative segment data is required. Primary reporting format is by business segment or geographical segment depending on how risks and returns are