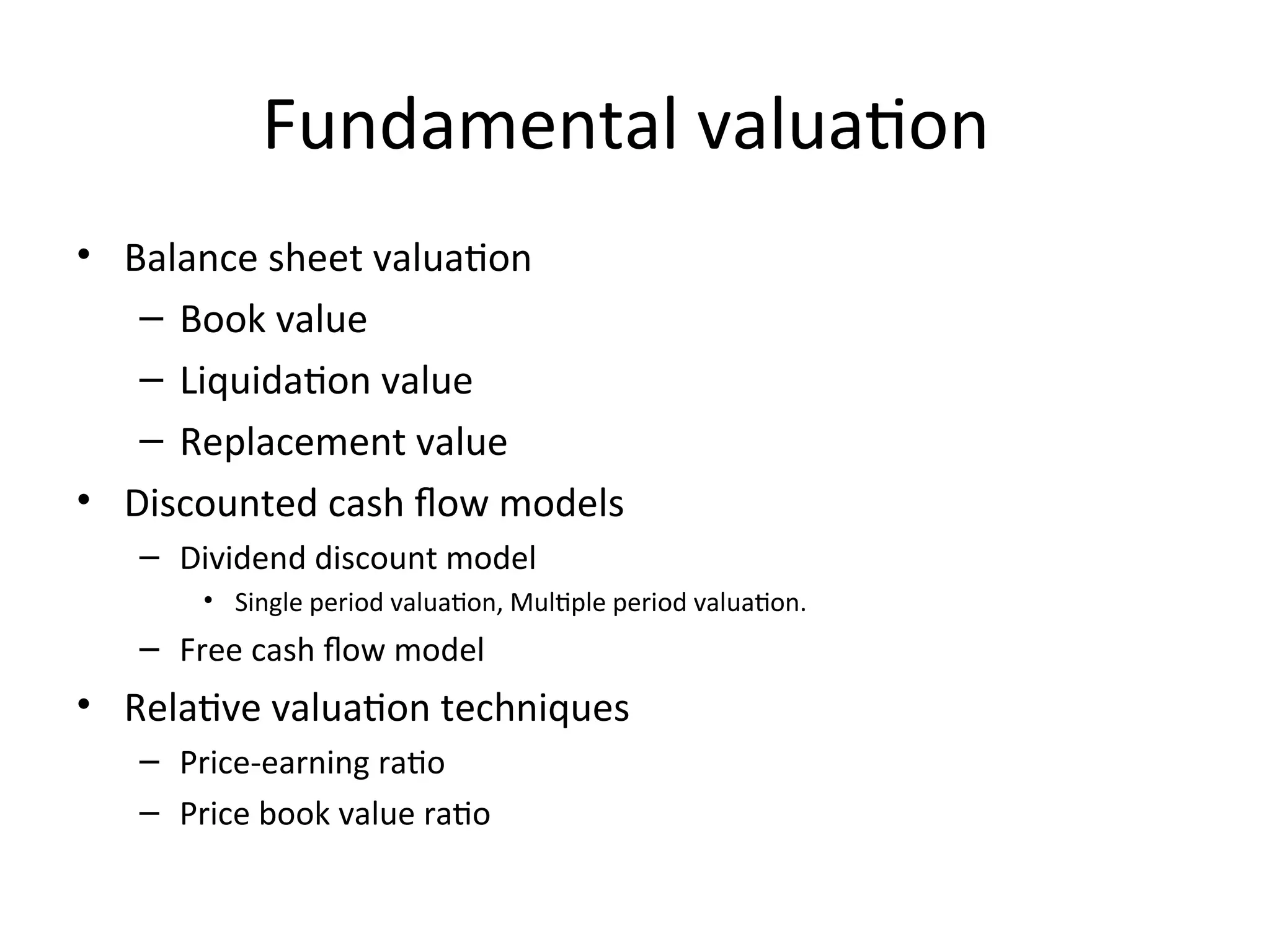

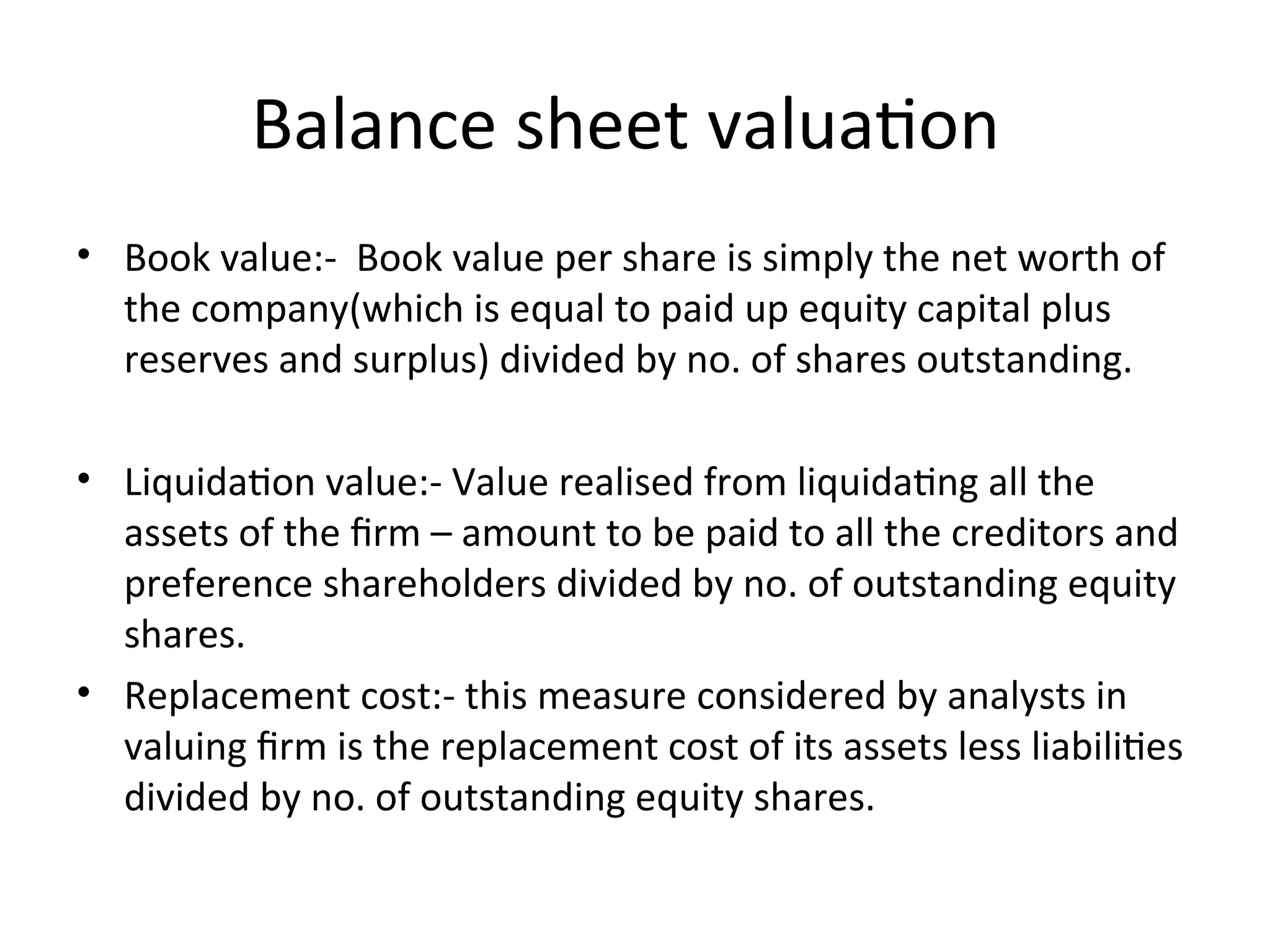

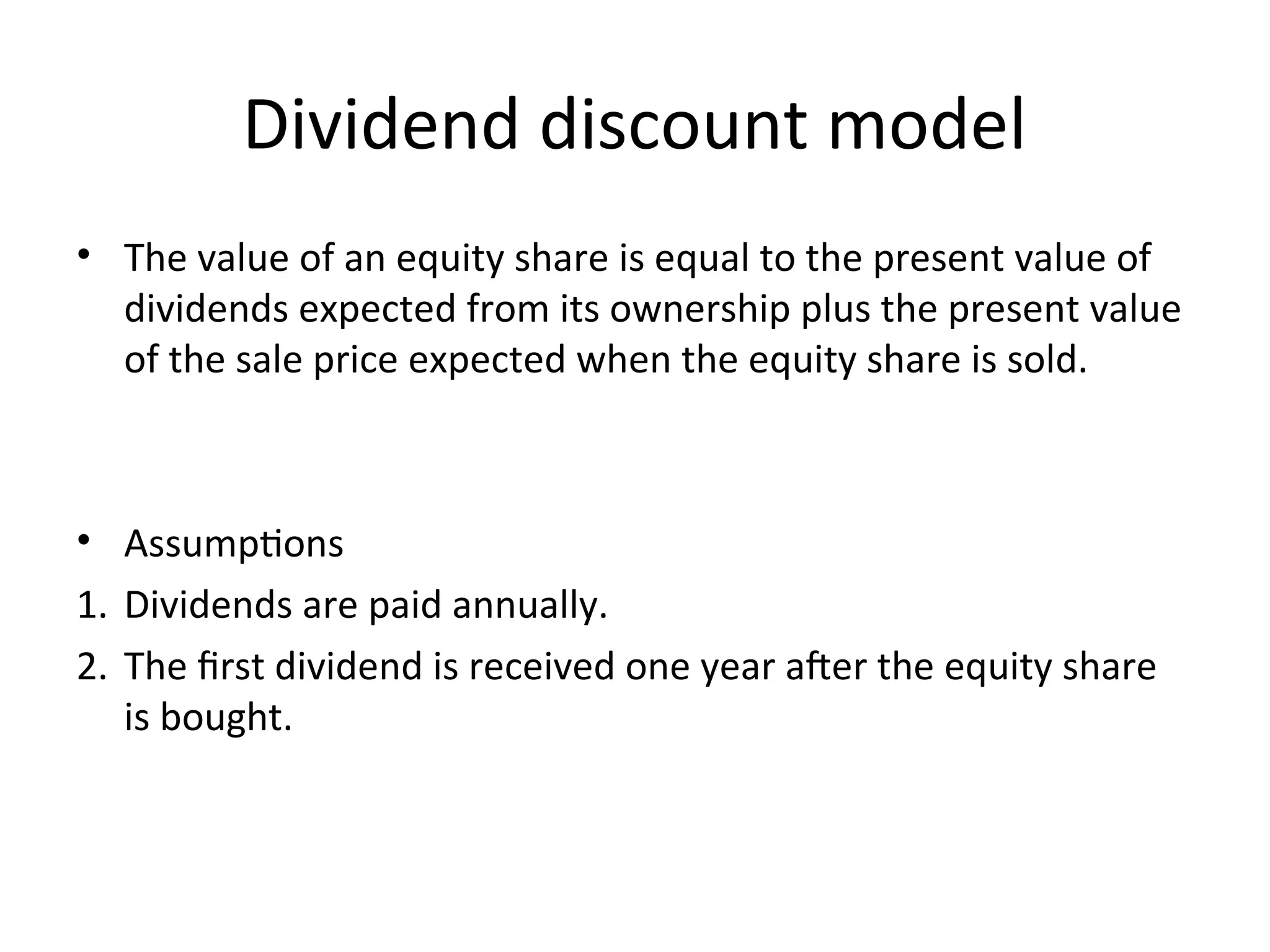

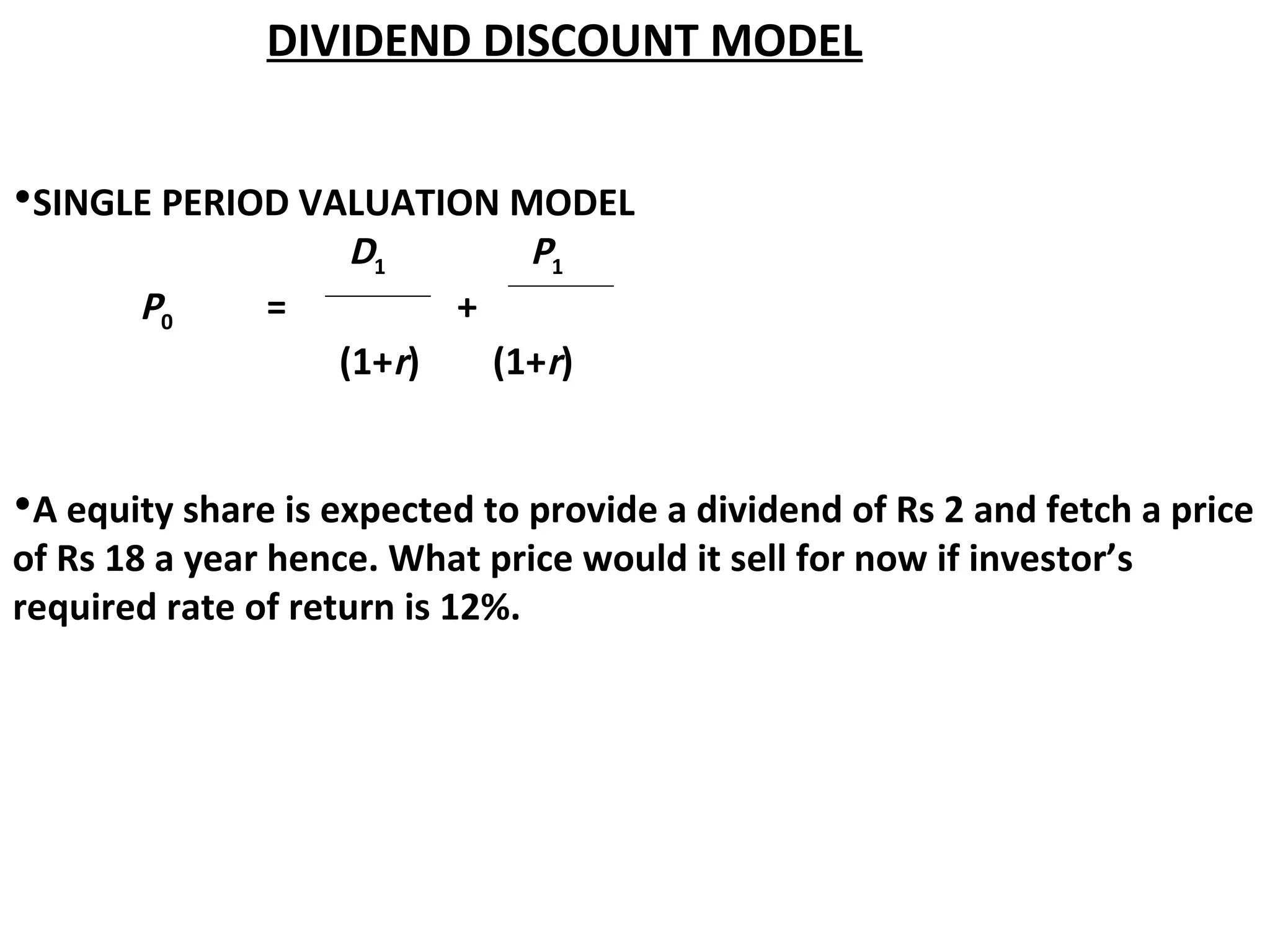

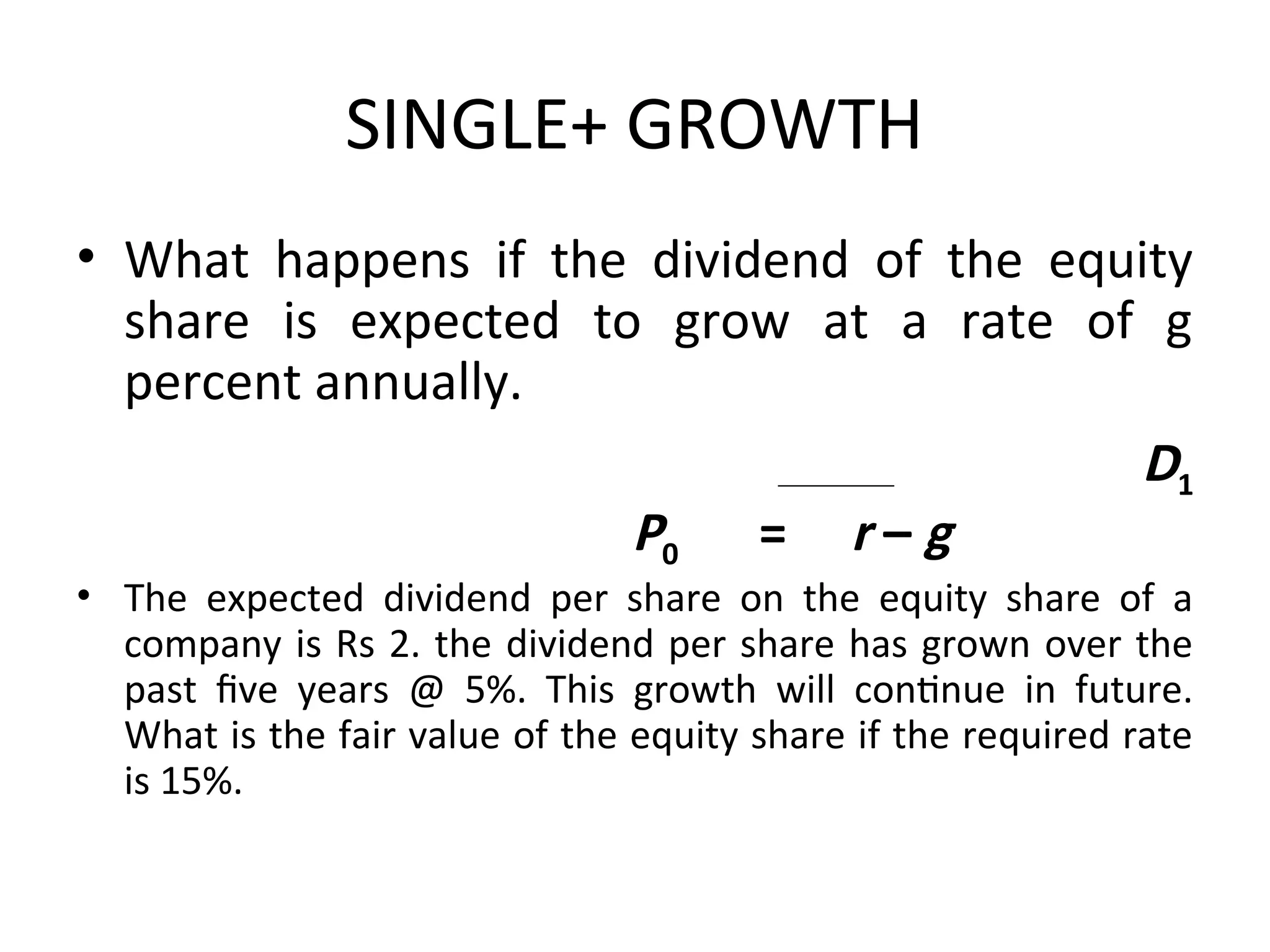

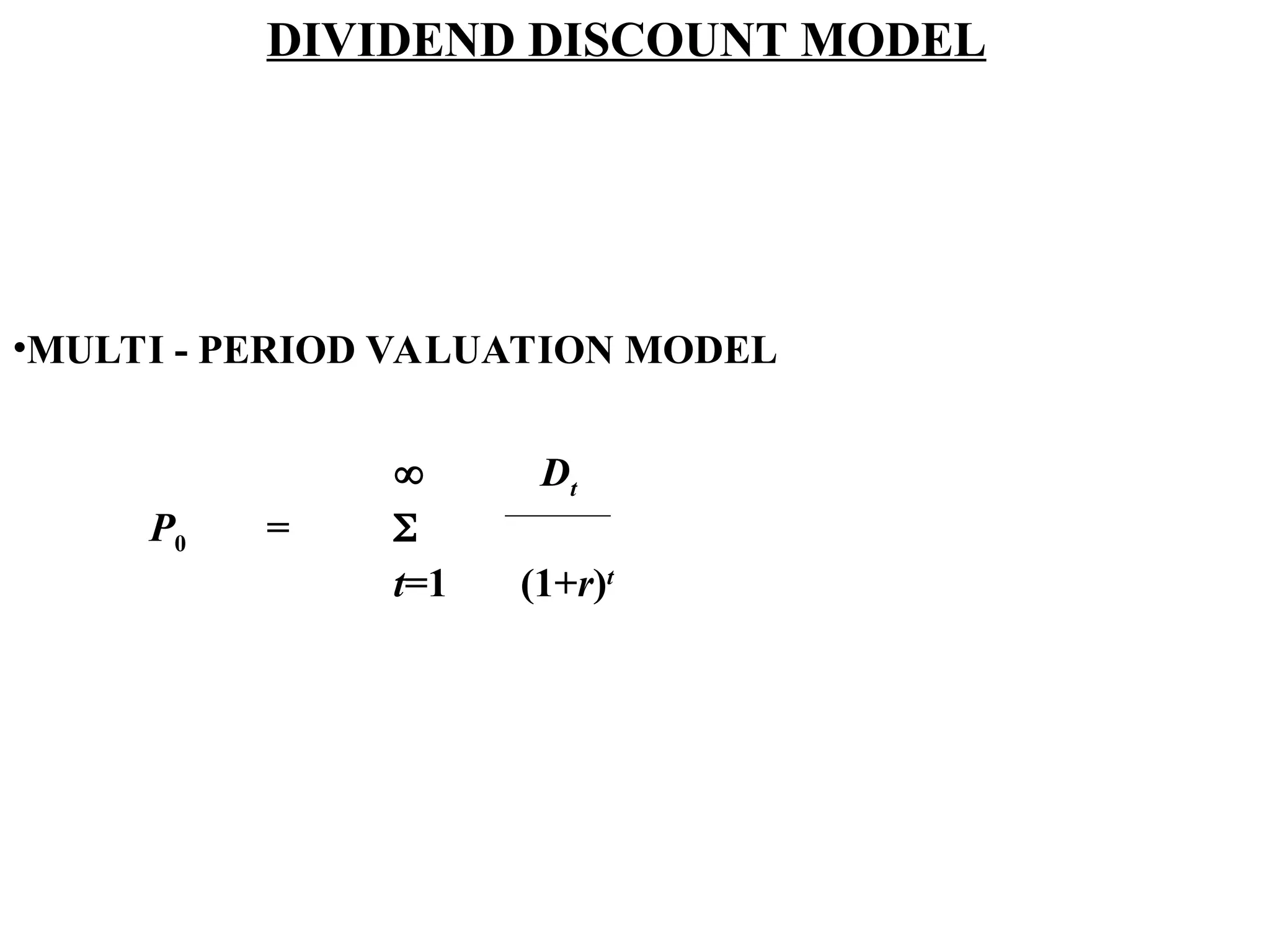

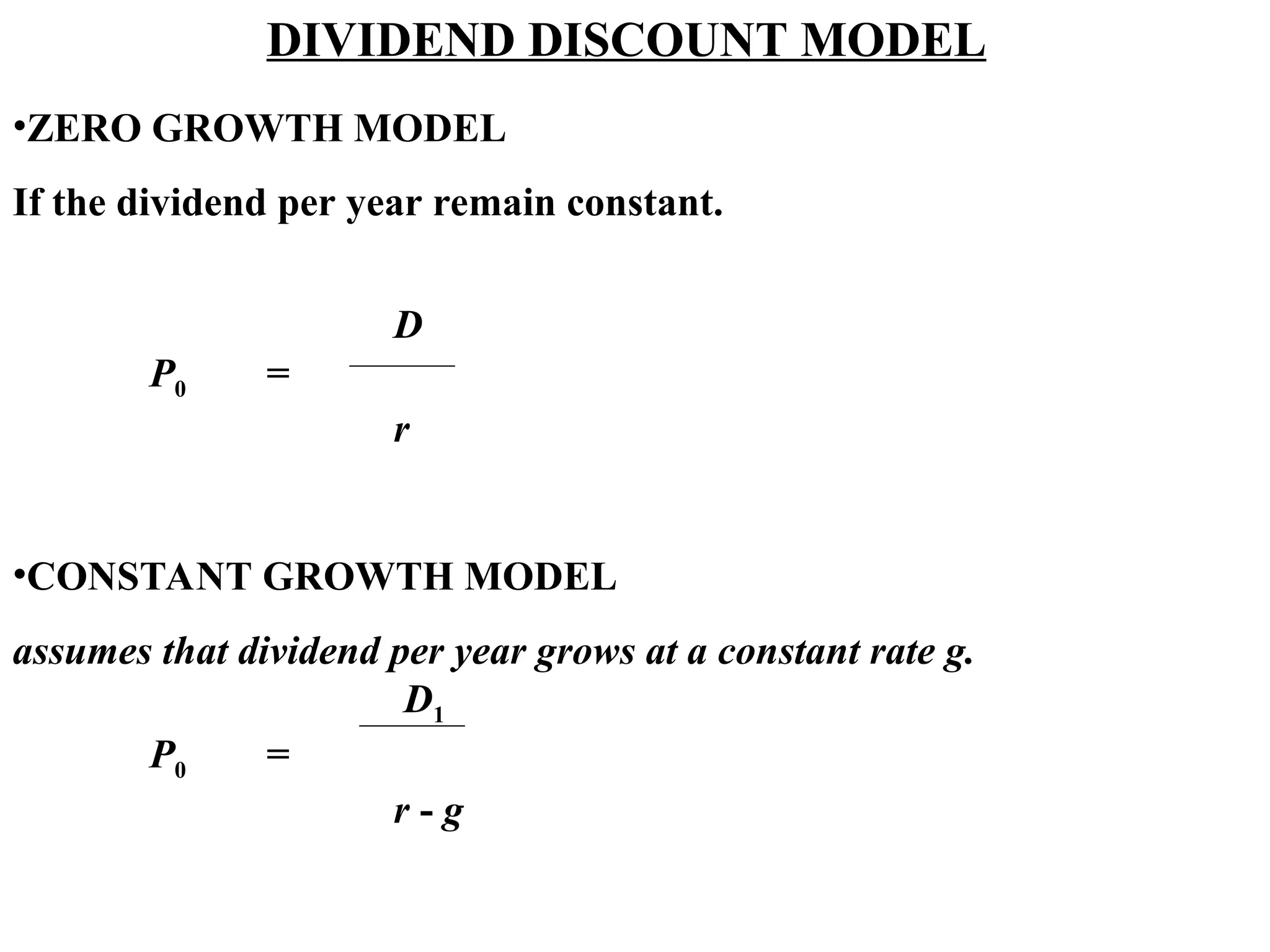

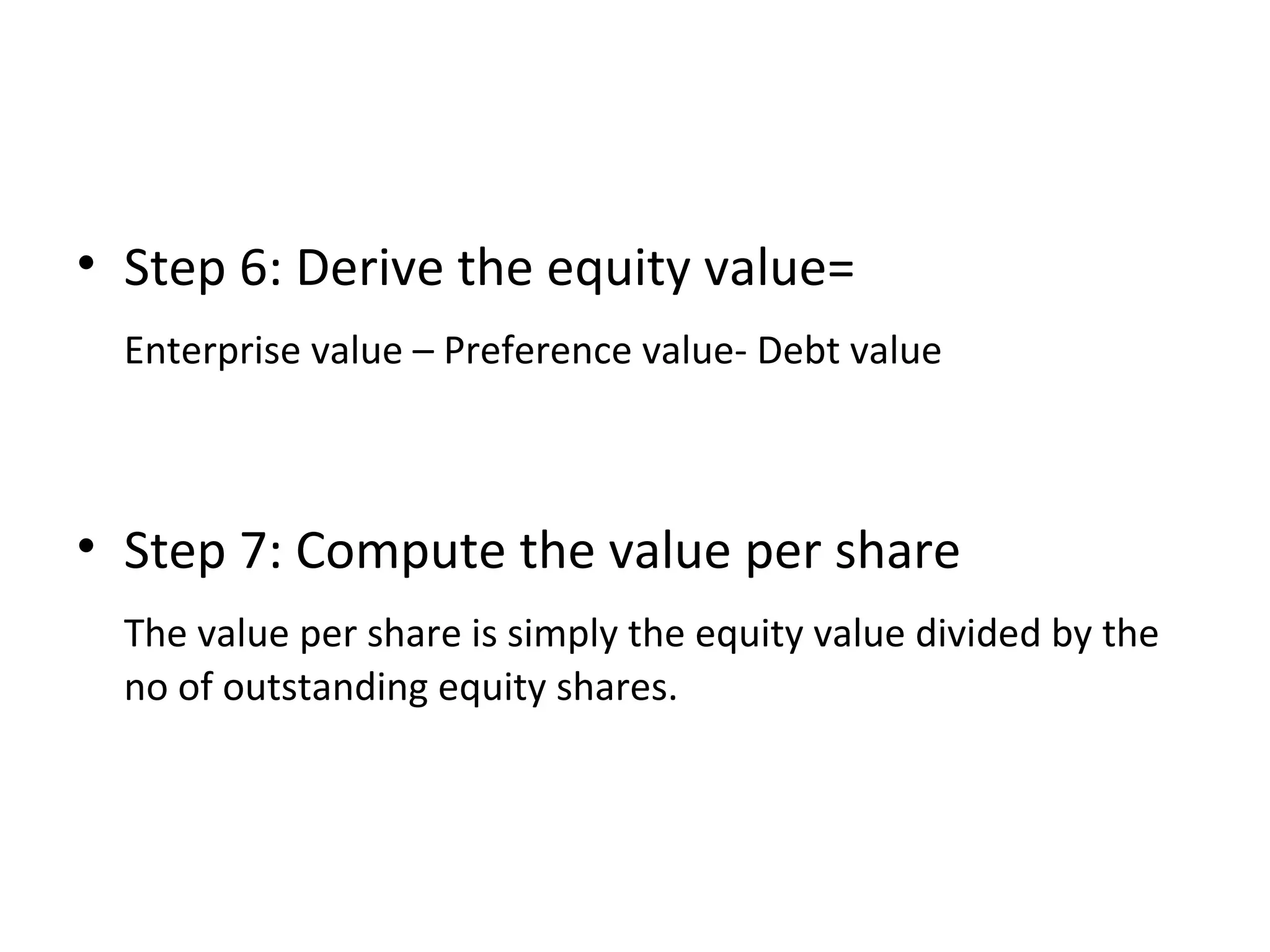

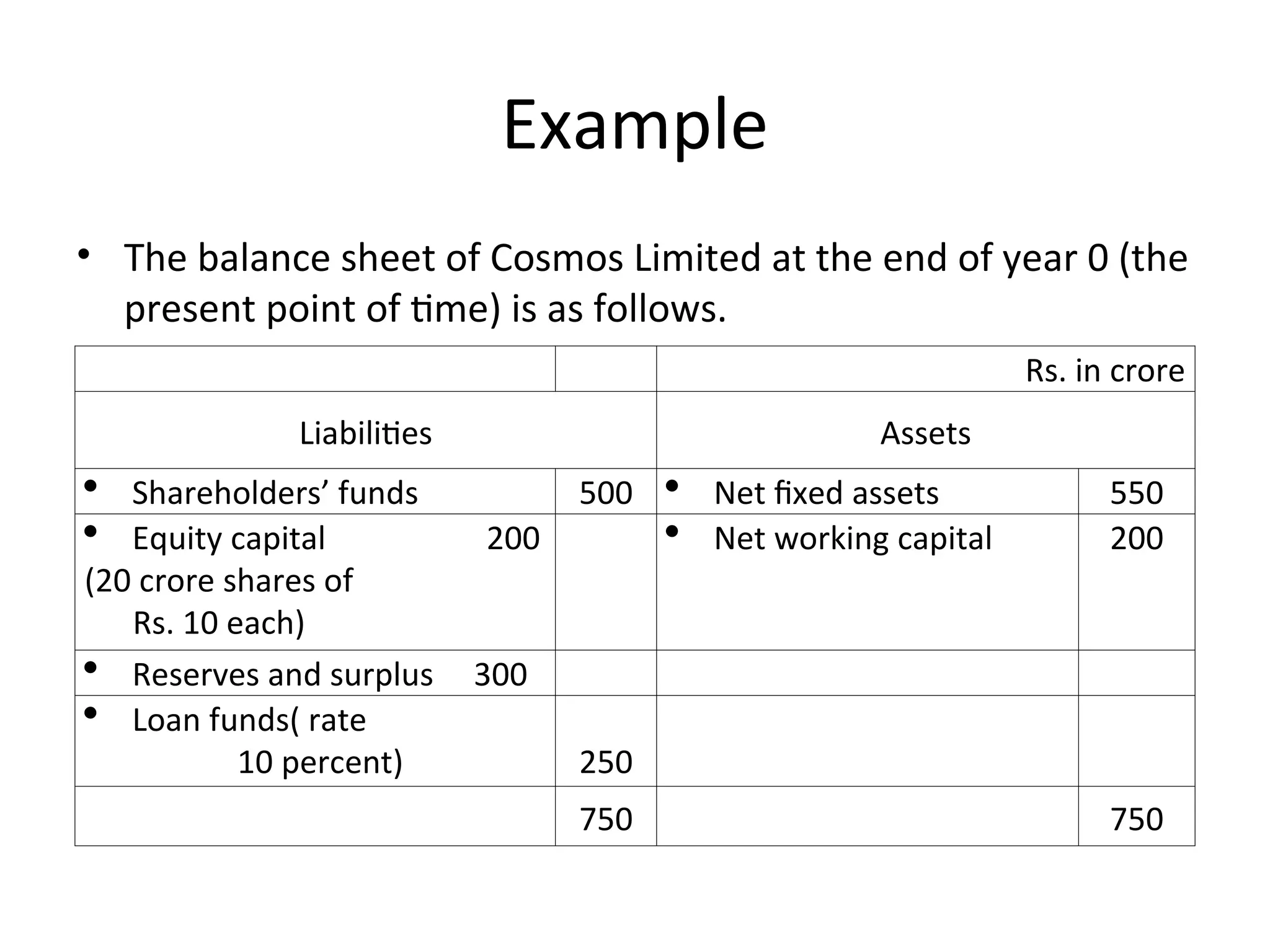

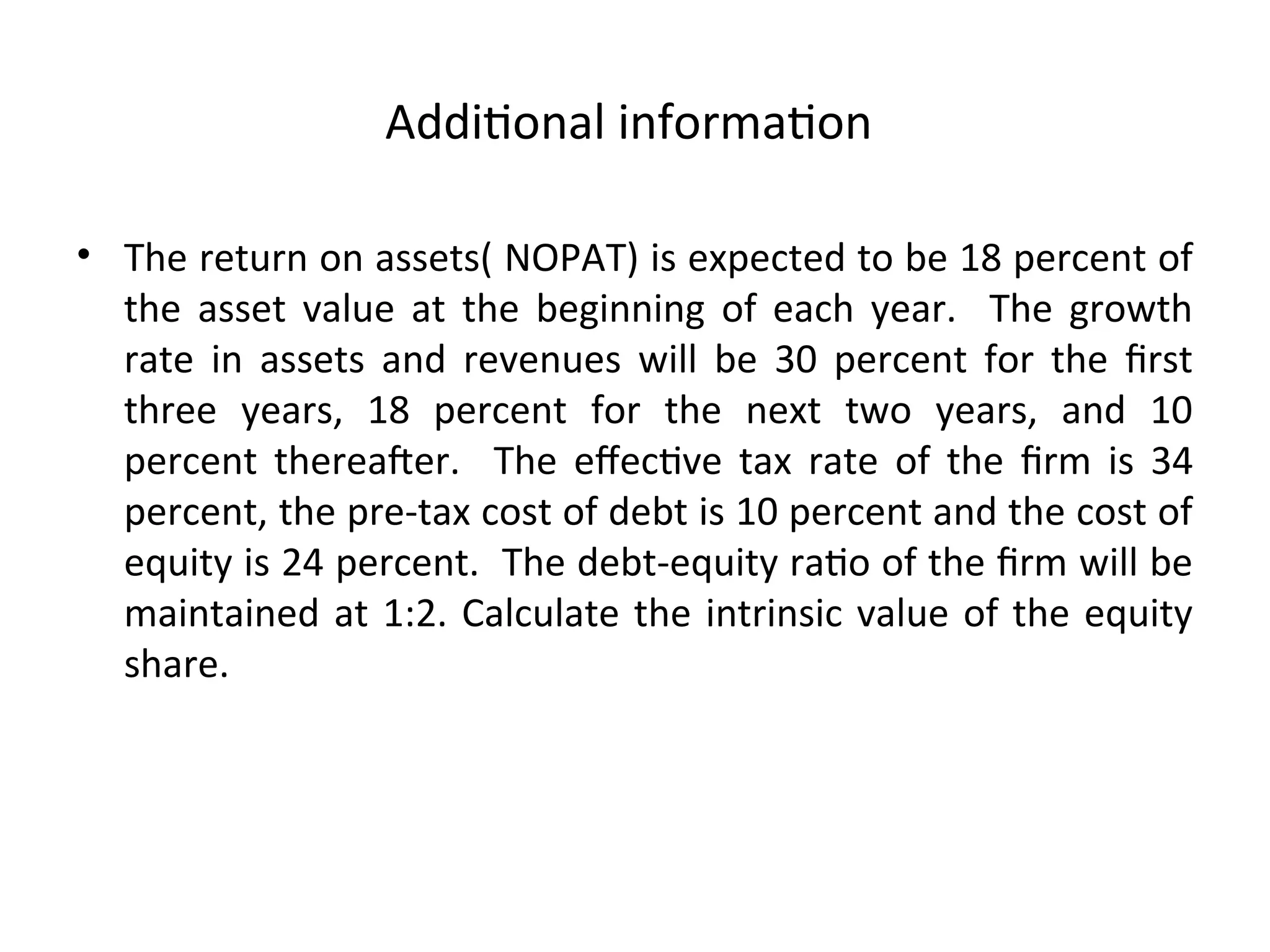

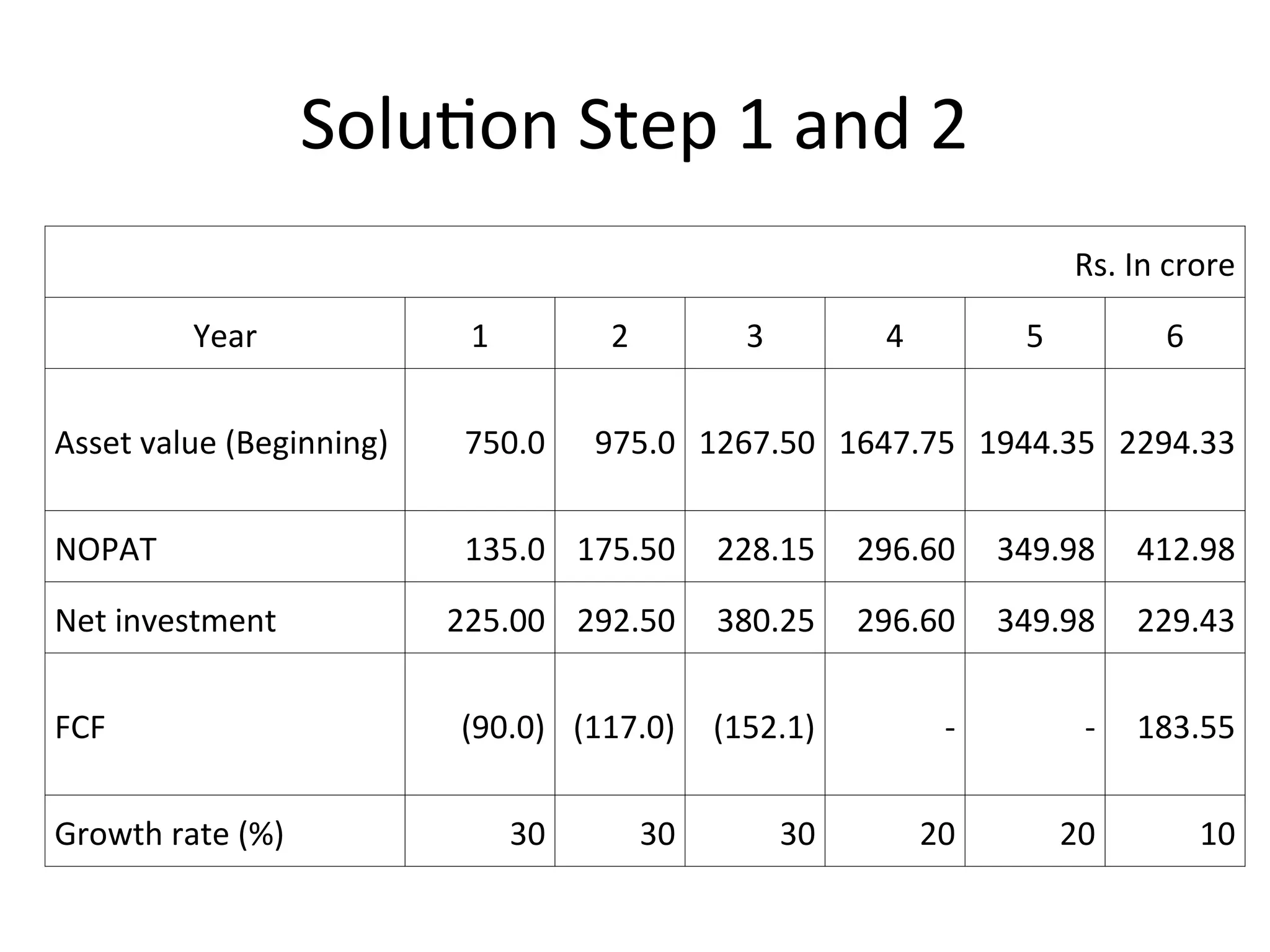

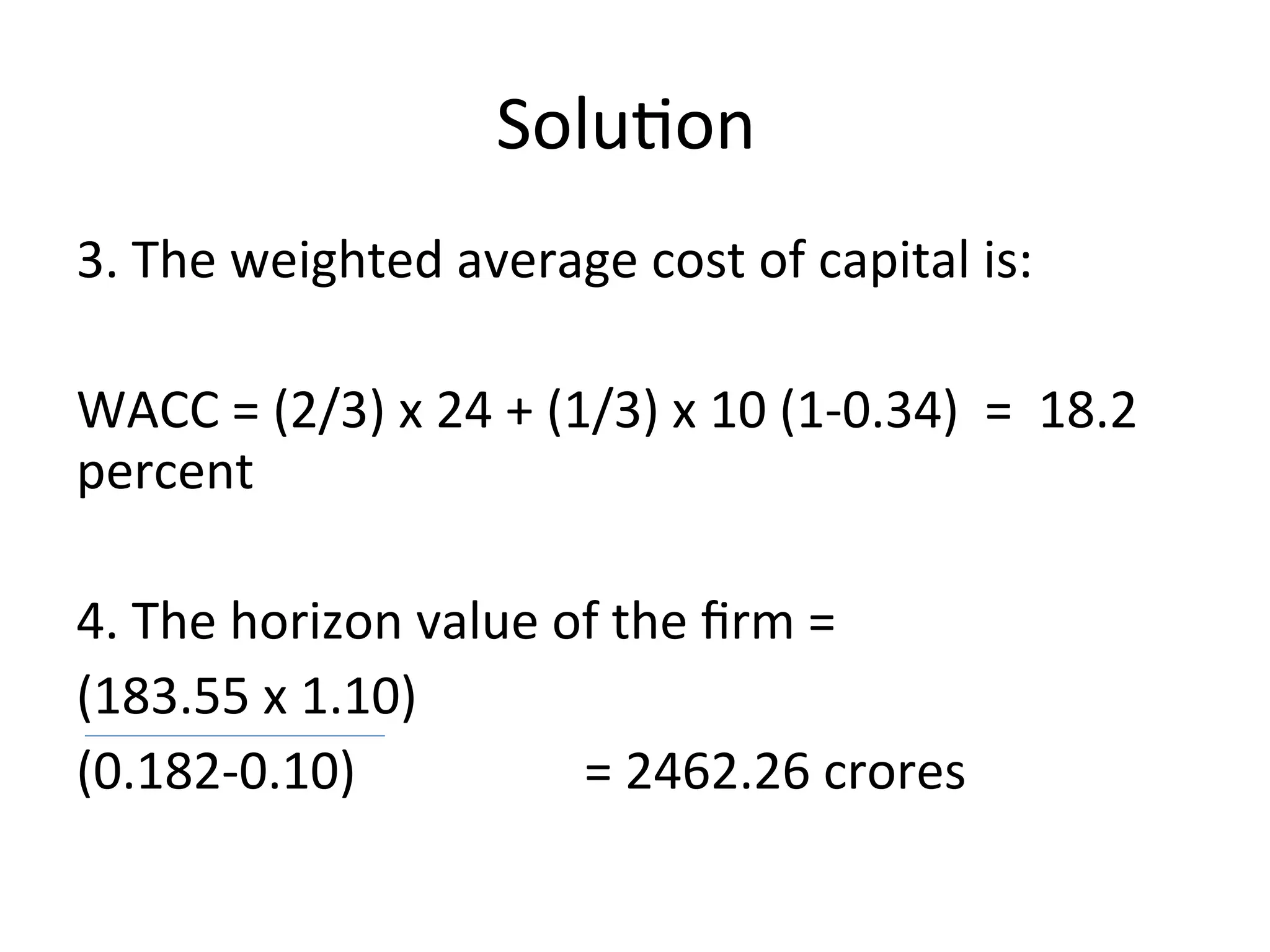

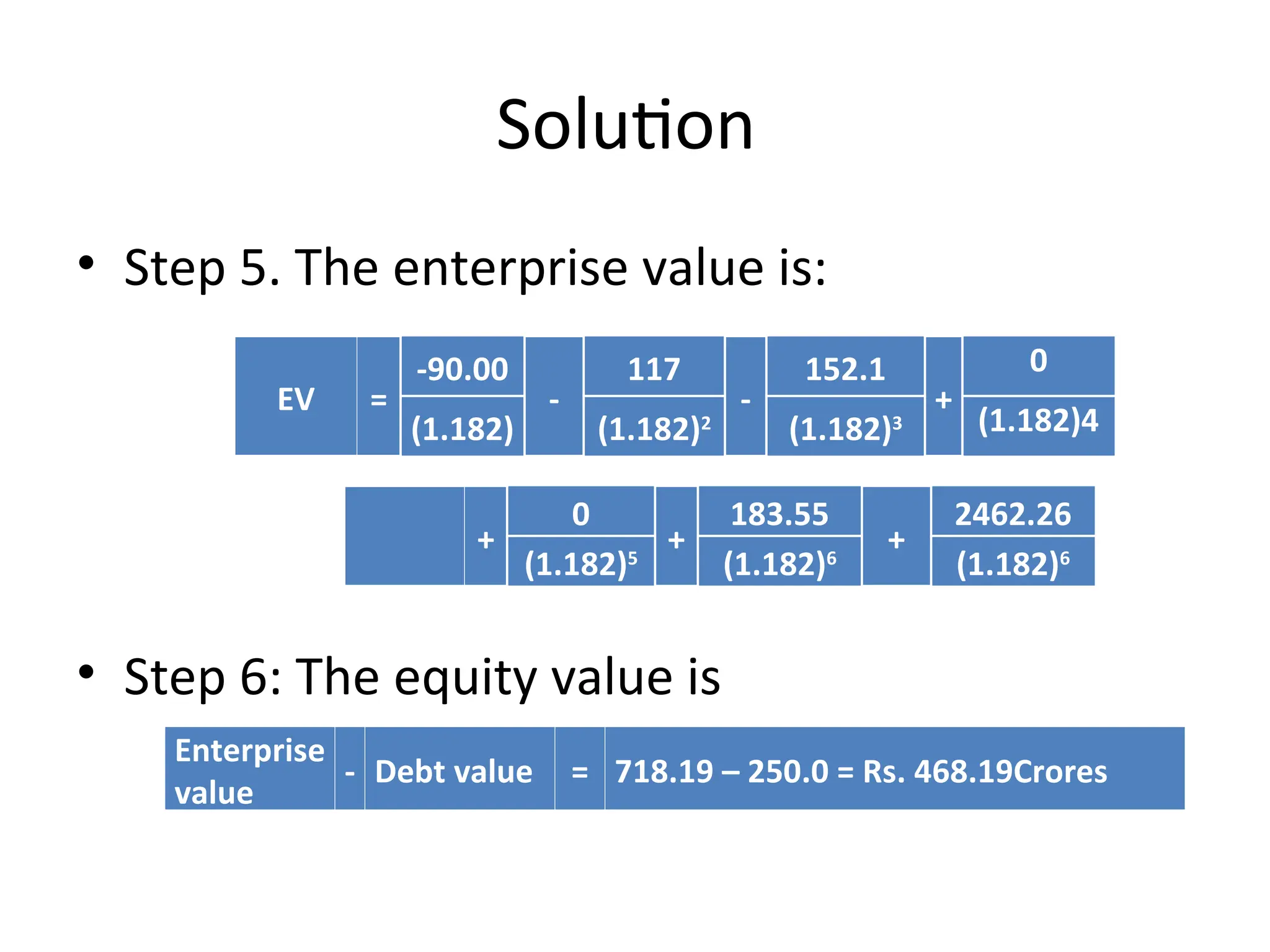

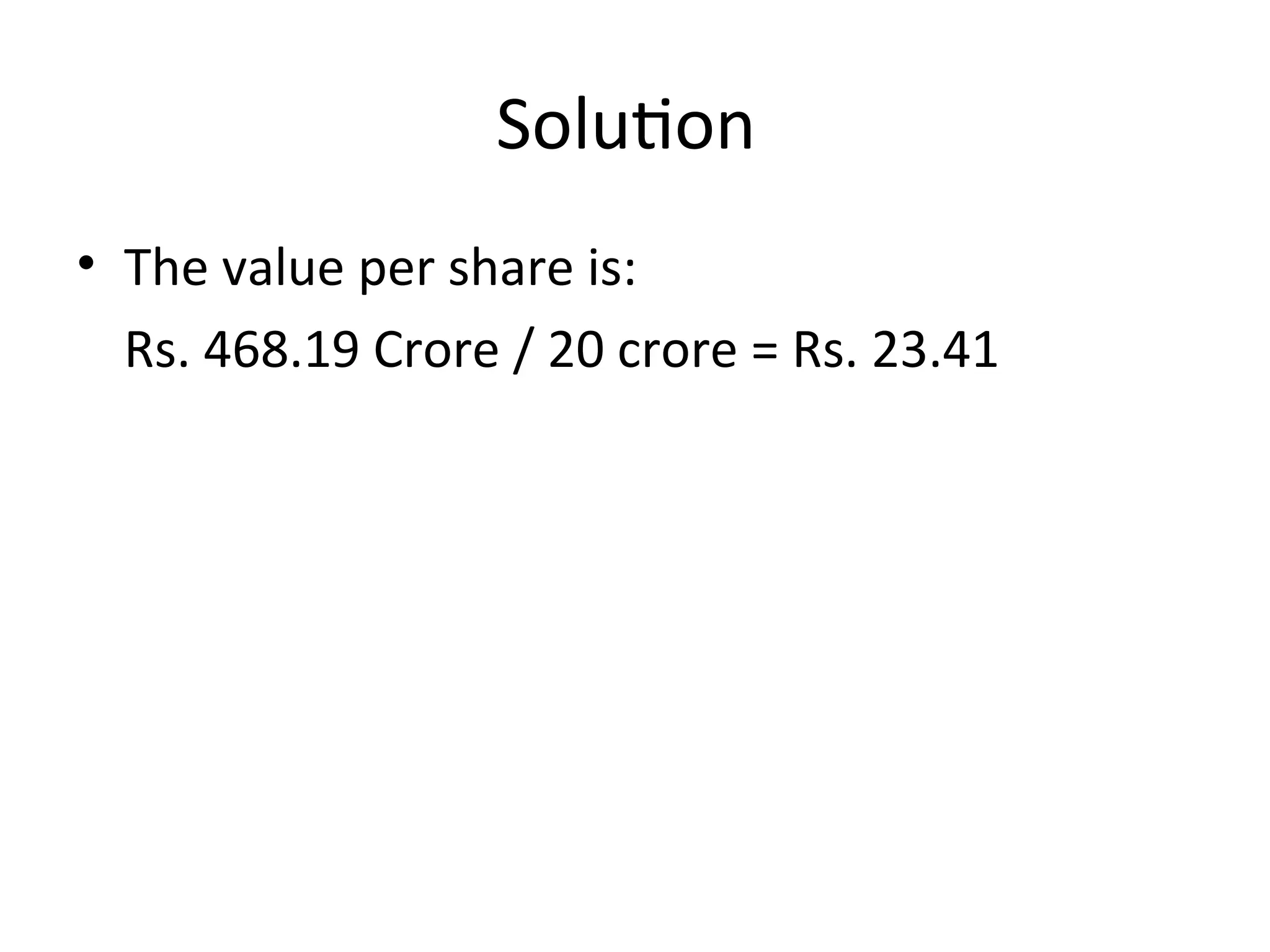

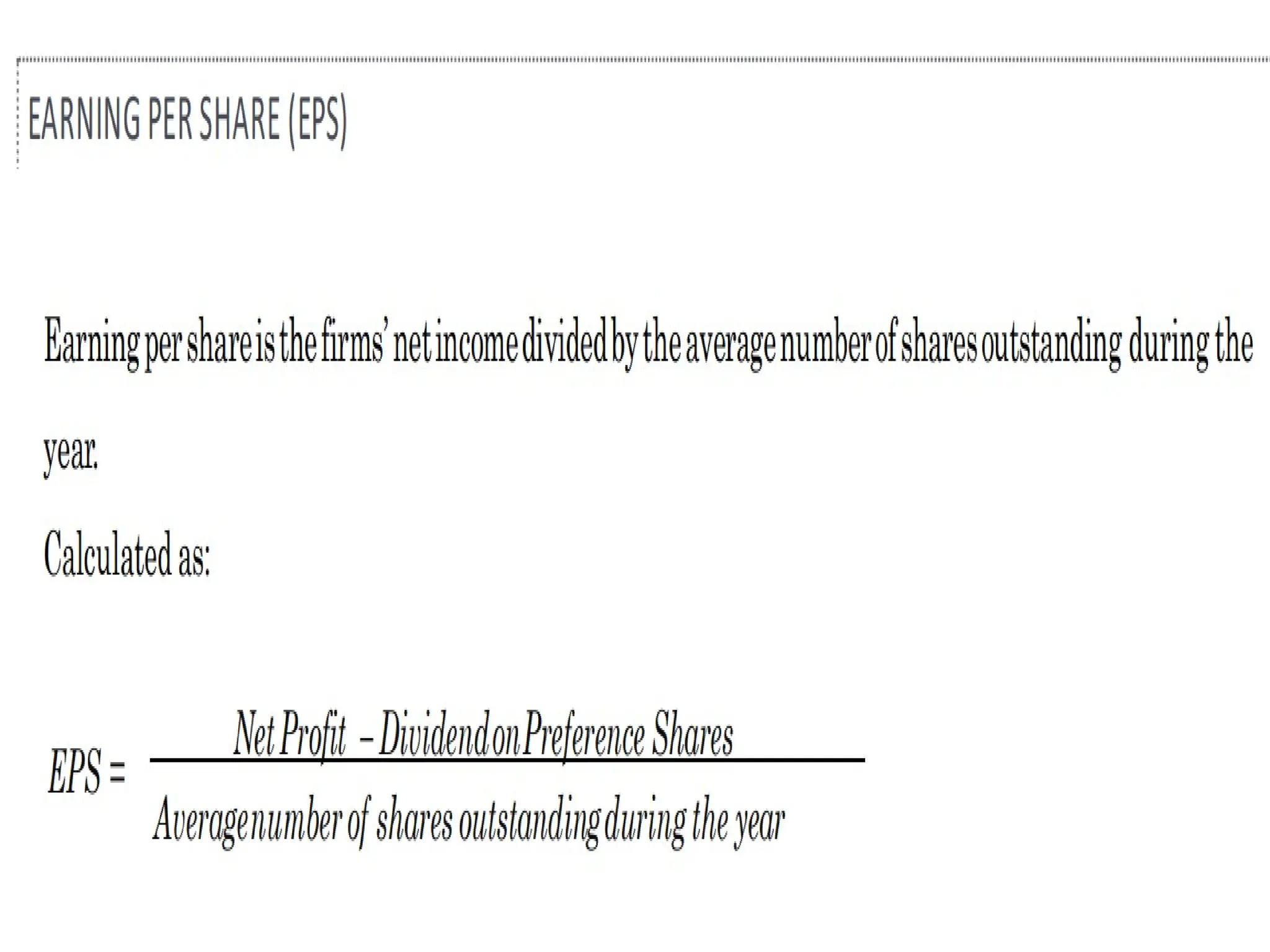

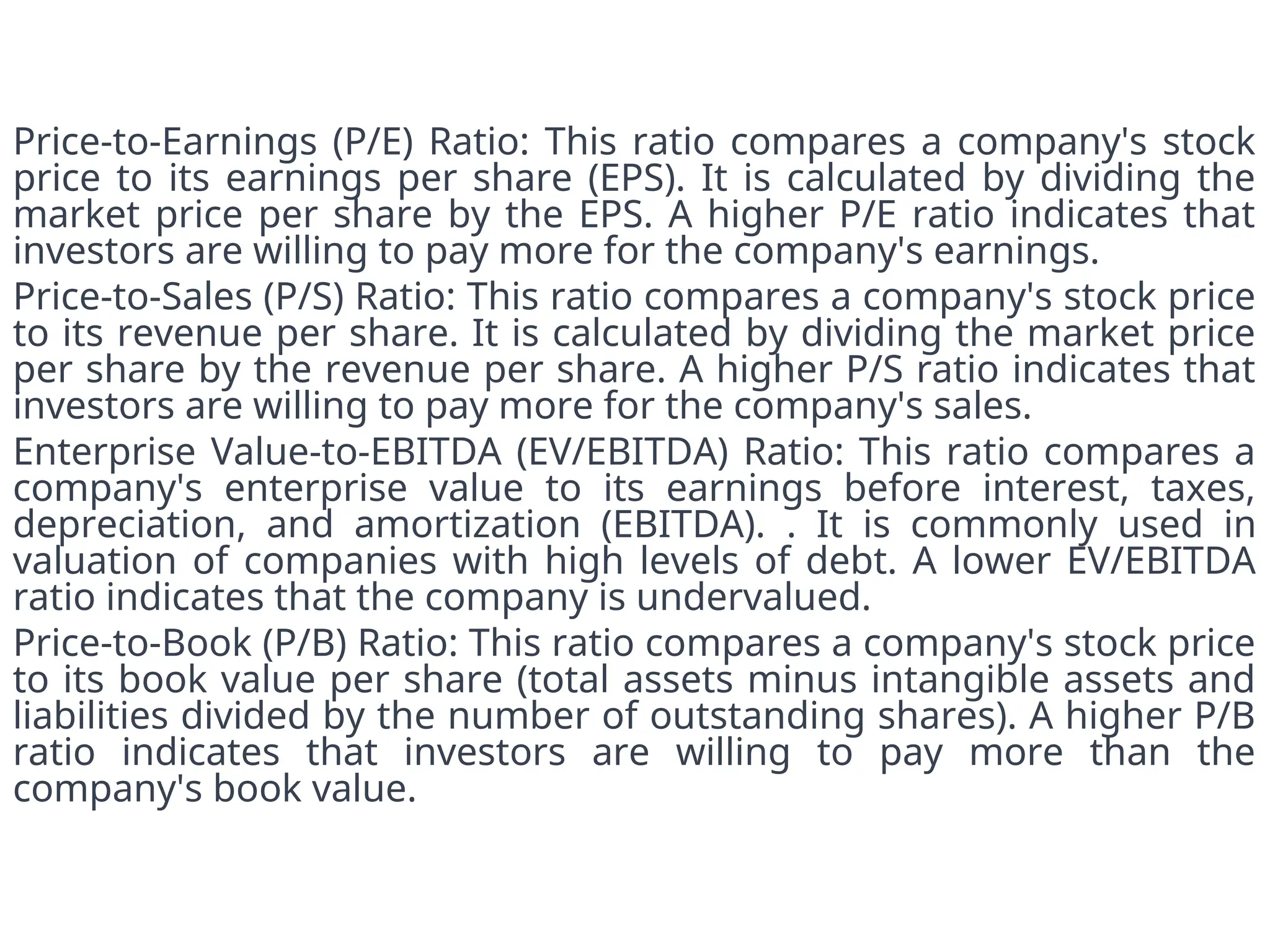

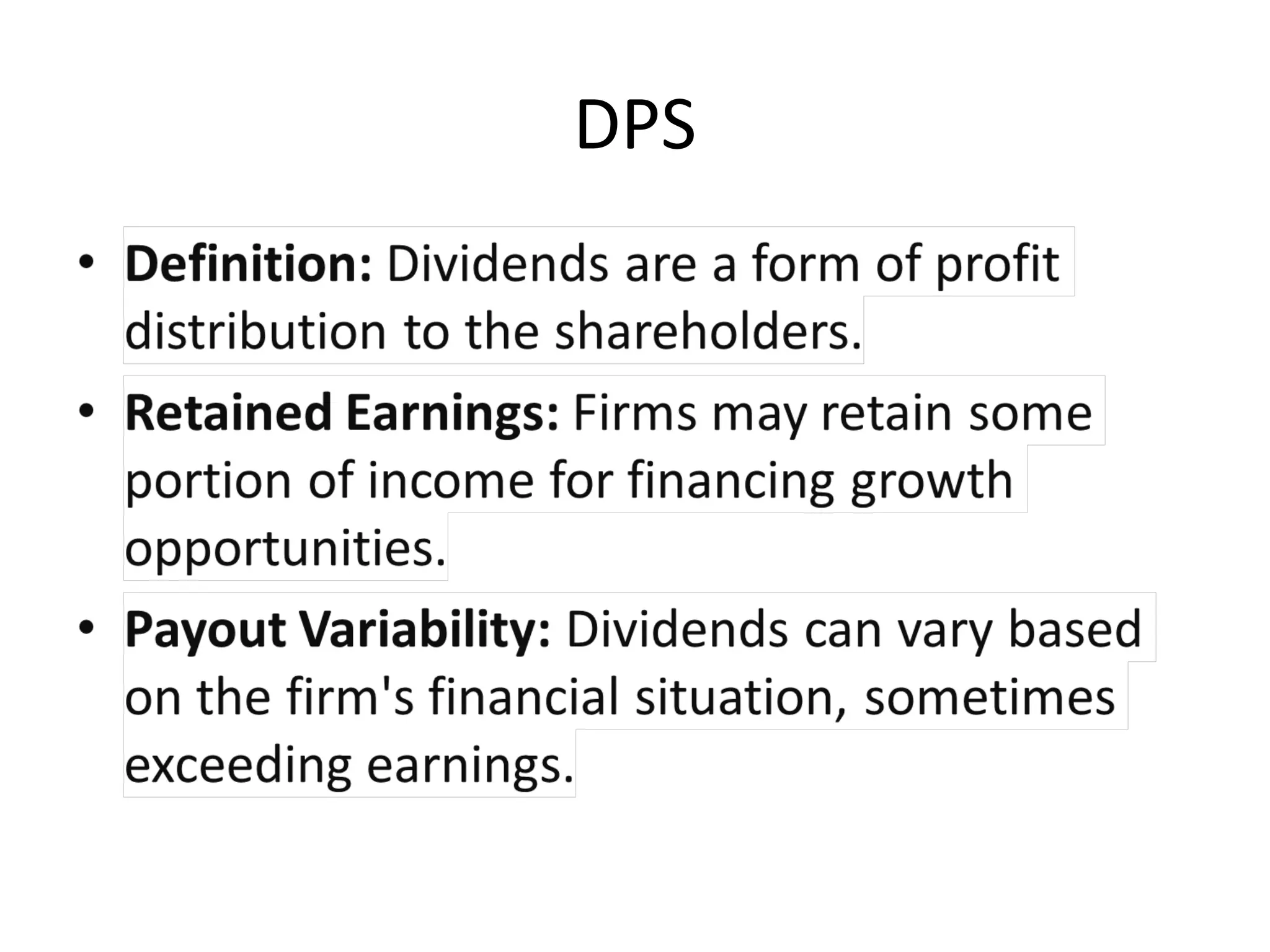

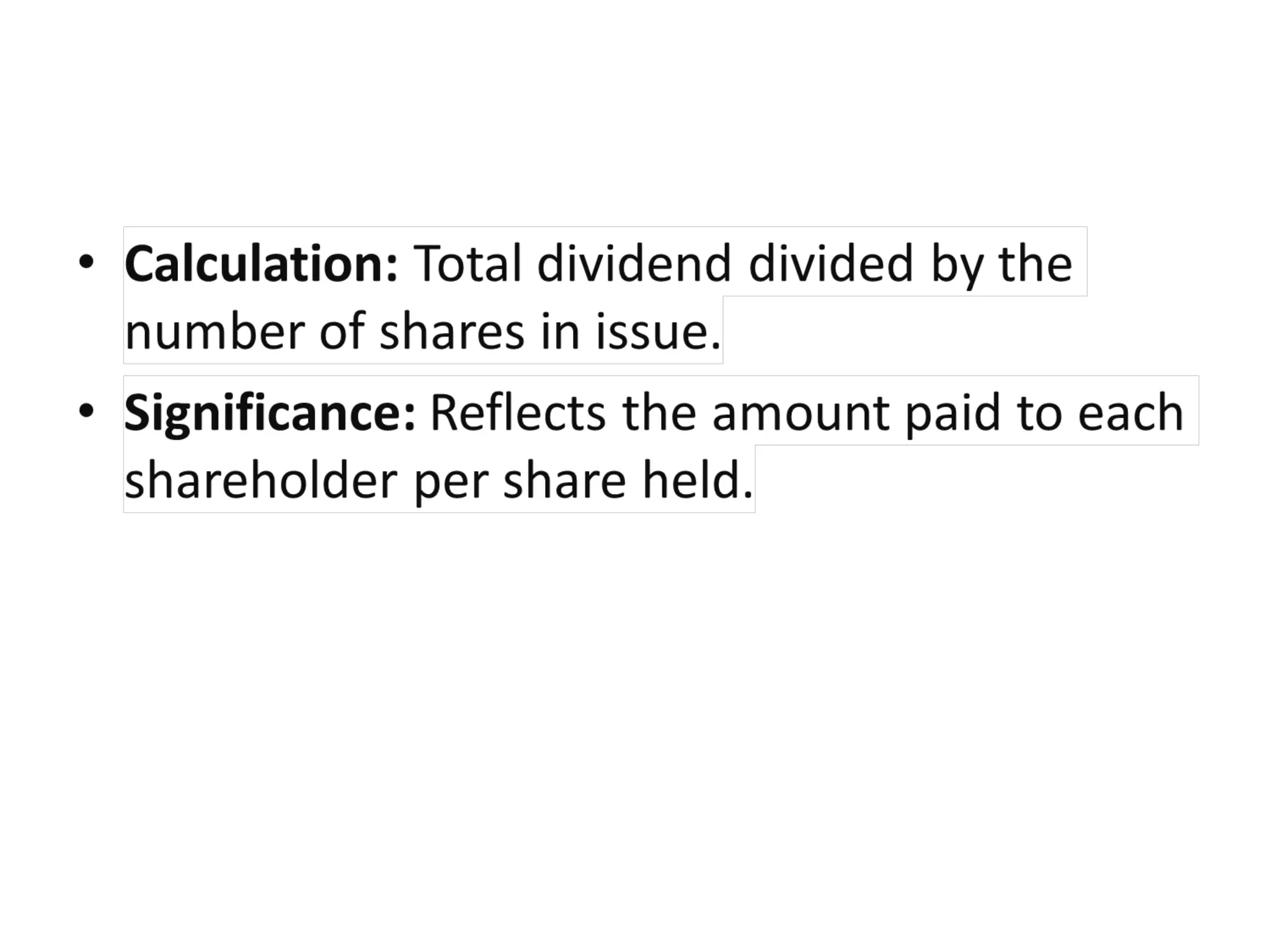

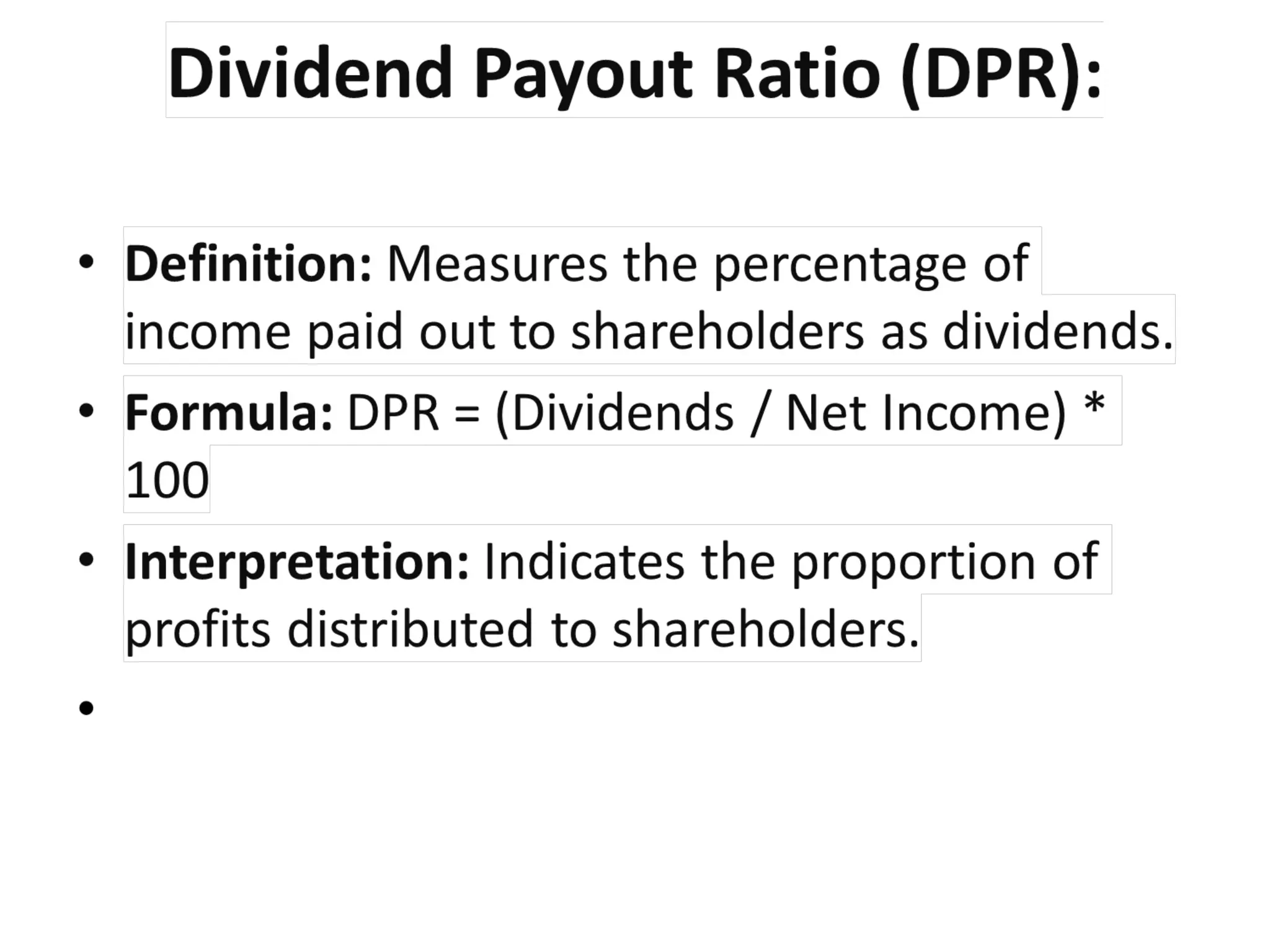

The document outlines various methods for equity valuation, including fundamental analysis, discounted cash flow models, and relative valuation techniques like price-earnings and price-to-book ratios. It emphasizes the importance of intrinsic value in investment decisions and provides detailed steps for calculating value per share using methods like the dividend discount model and free cash flow model. Additionally, it covers practical examples to illustrate intrinsic value calculations and key financial ratios used for valuation comparisons.