Downloaded 211 times

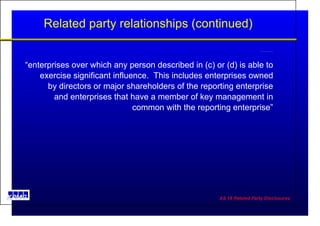

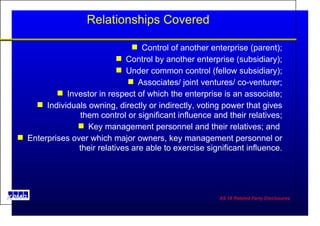

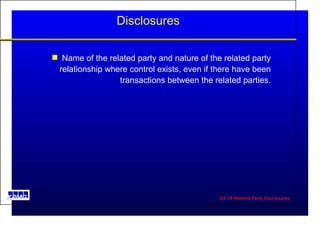

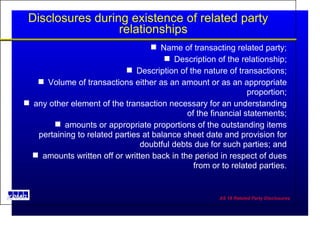

The document discusses the disclosure requirements for related party transactions under the Indian accounting standard AS-18. It defines related parties as individuals or entities that have the ability to control or exercise significant influence over the reporting entity. It requires disclosure of the nature and volume of transactions between the reporting entity and its related parties, as well as outstanding balances and any provisions for doubtful debts involving such parties. The disclosures are necessary because related party transactions may not be conducted under normal commercial terms.

![Presentation on AS 18_Chaitanya_06.06.2015.pptx [Autosaved] (1)](https://cdn.slidesharecdn.com/ss_thumbnails/81ed098d-2d4d-4dba-b4a8-e2bd4d4d2f36-150717065205-lva1-app6891-thumbnail.jpg?width=640&height=640&fit=bounds)