Downloaded 5,005 times

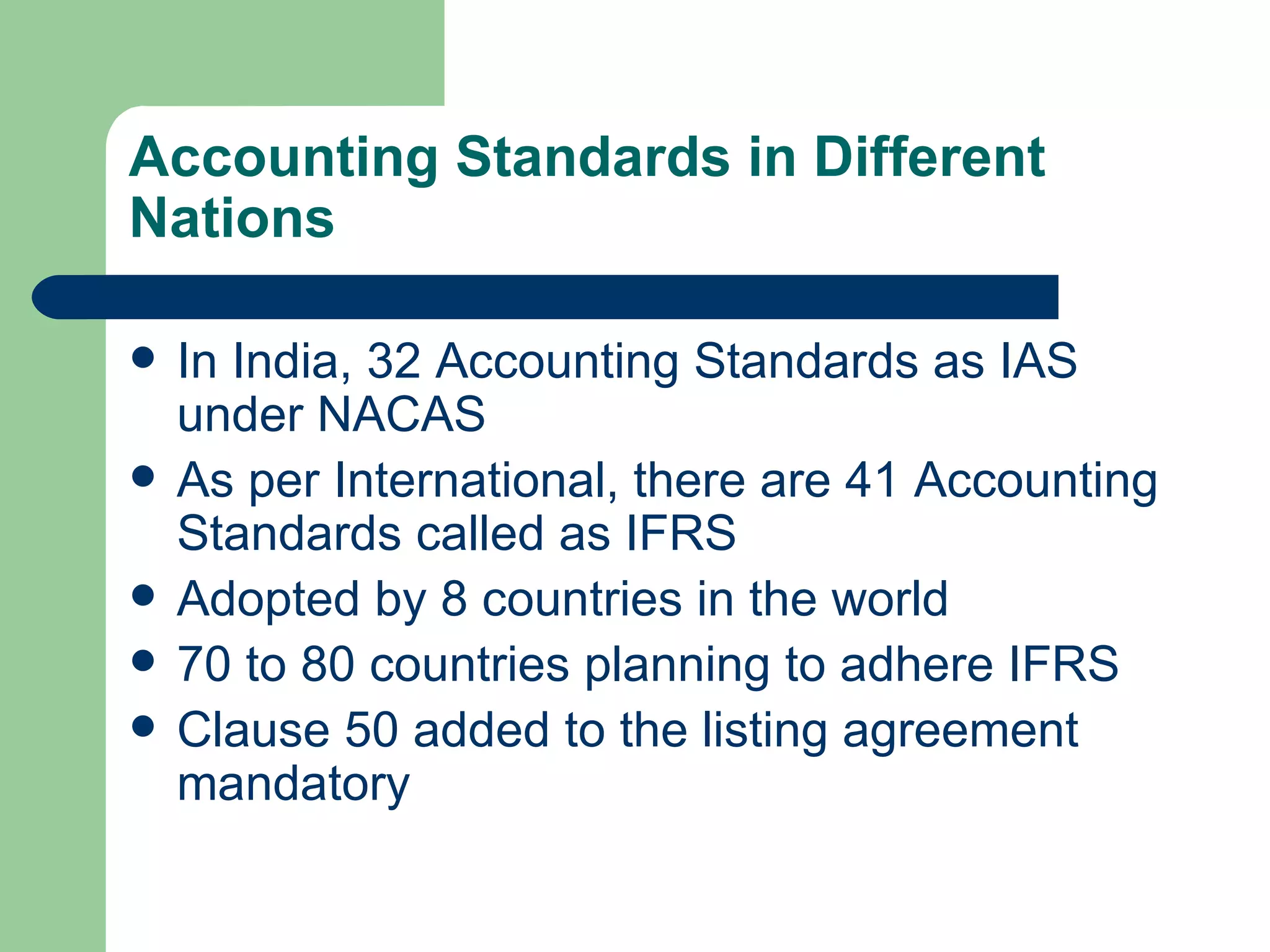

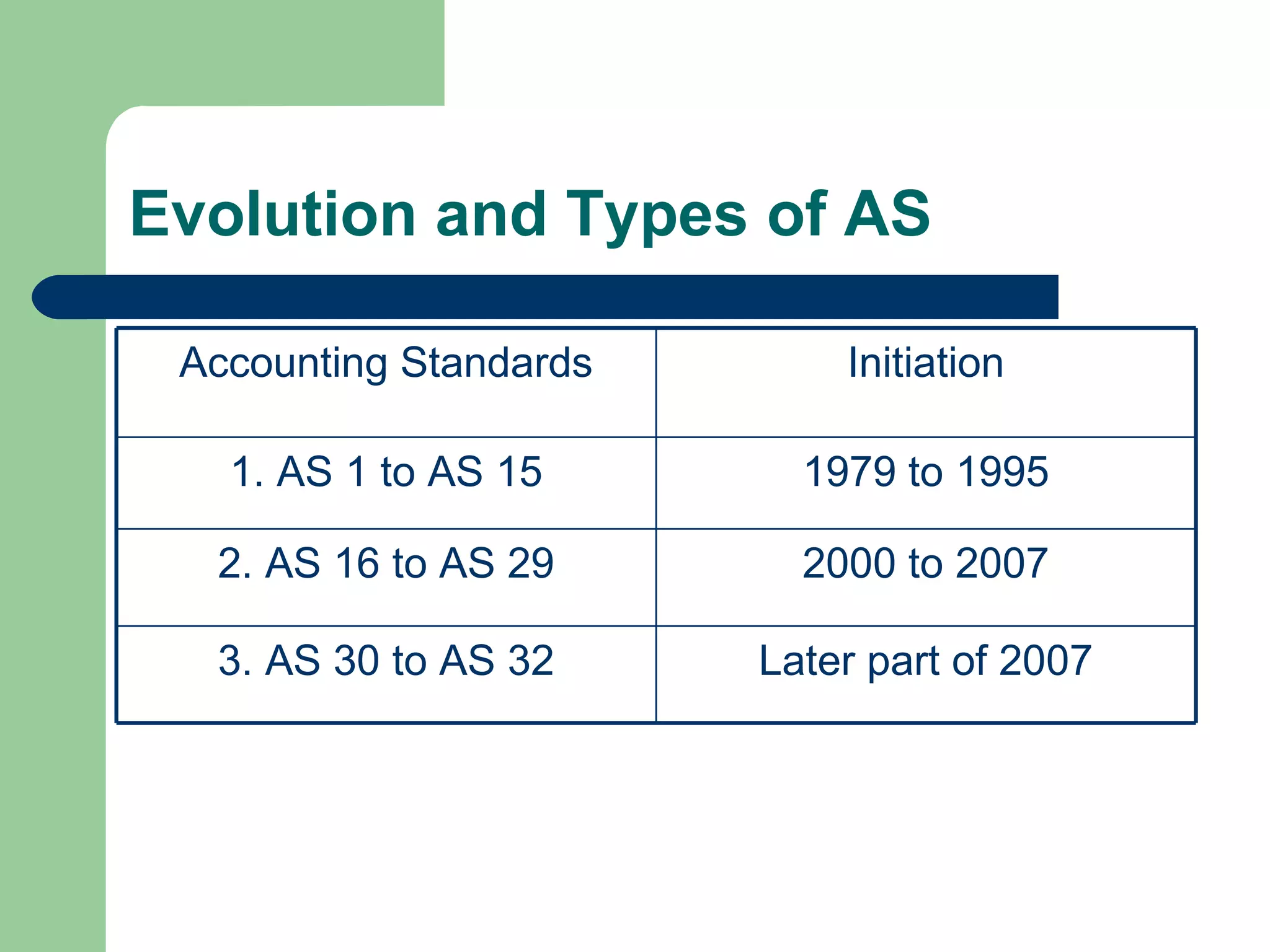

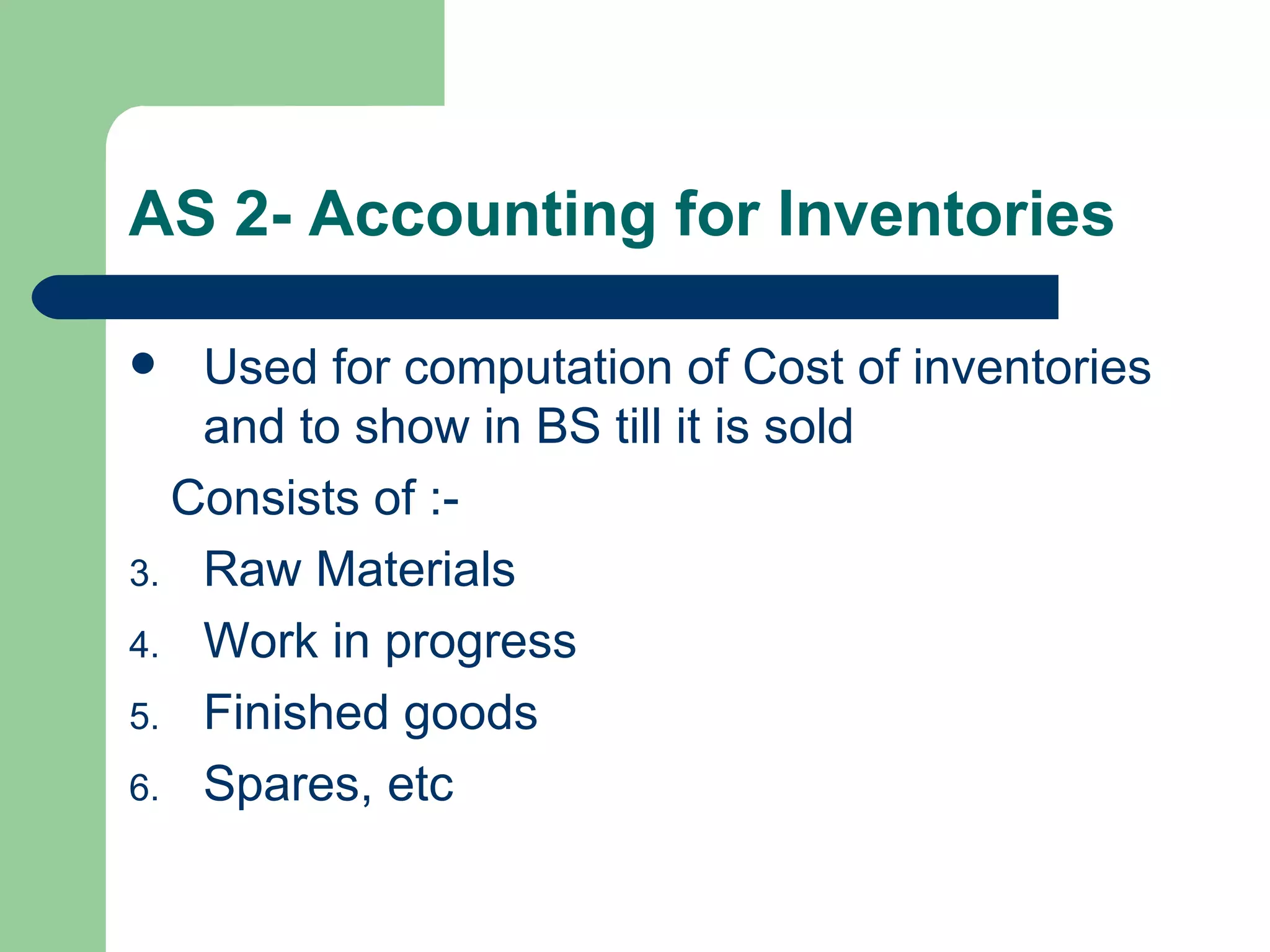

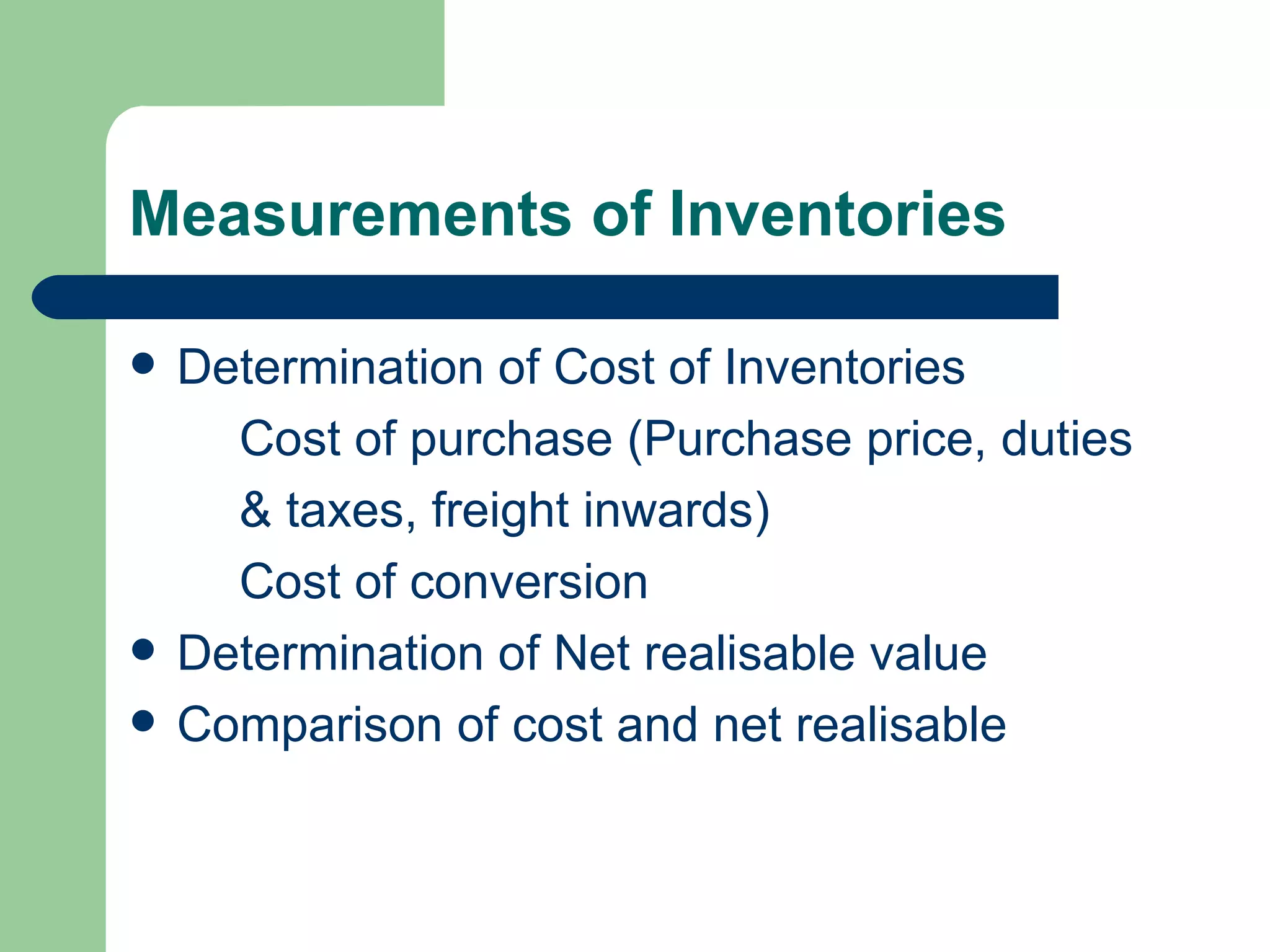

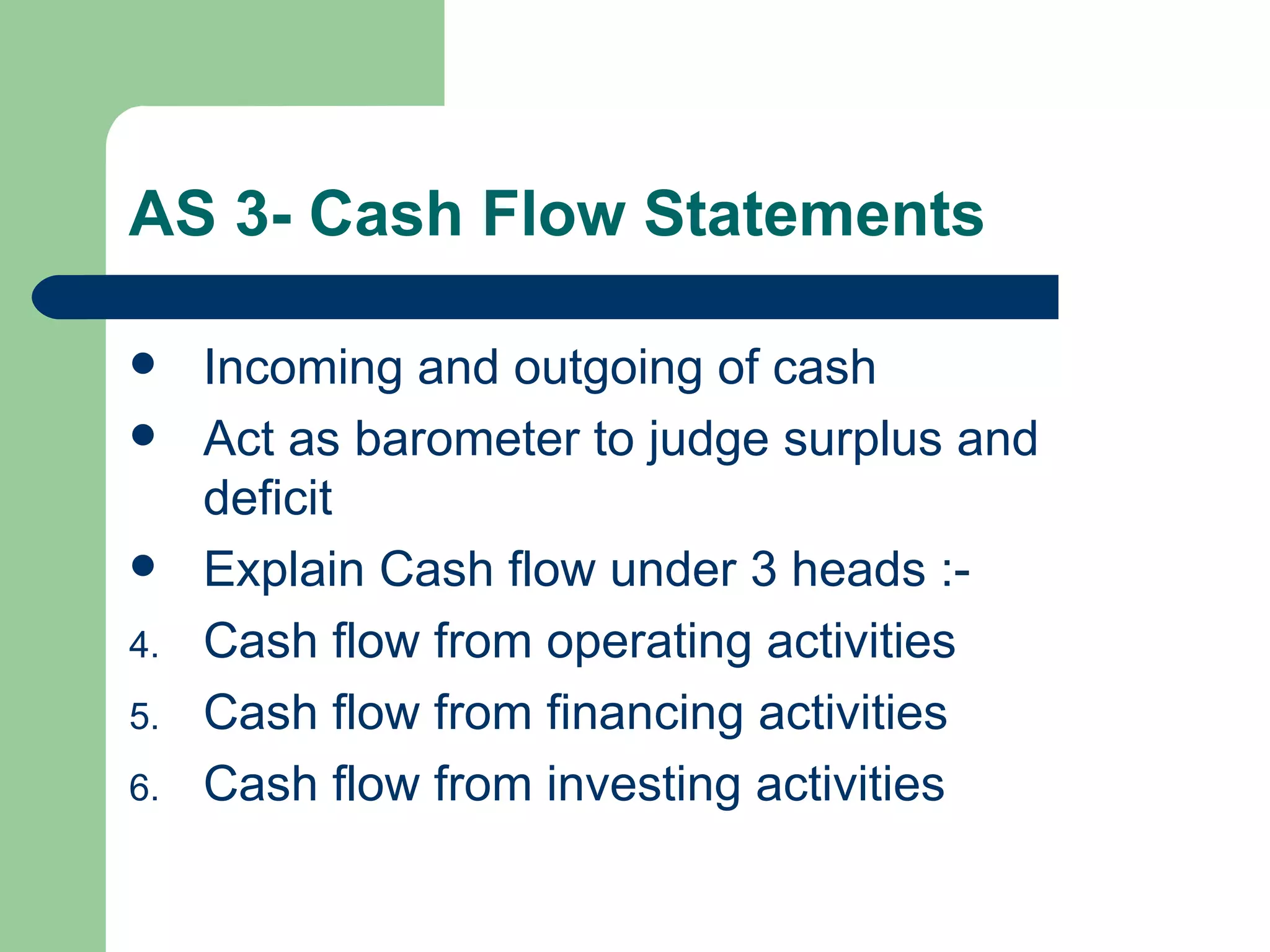

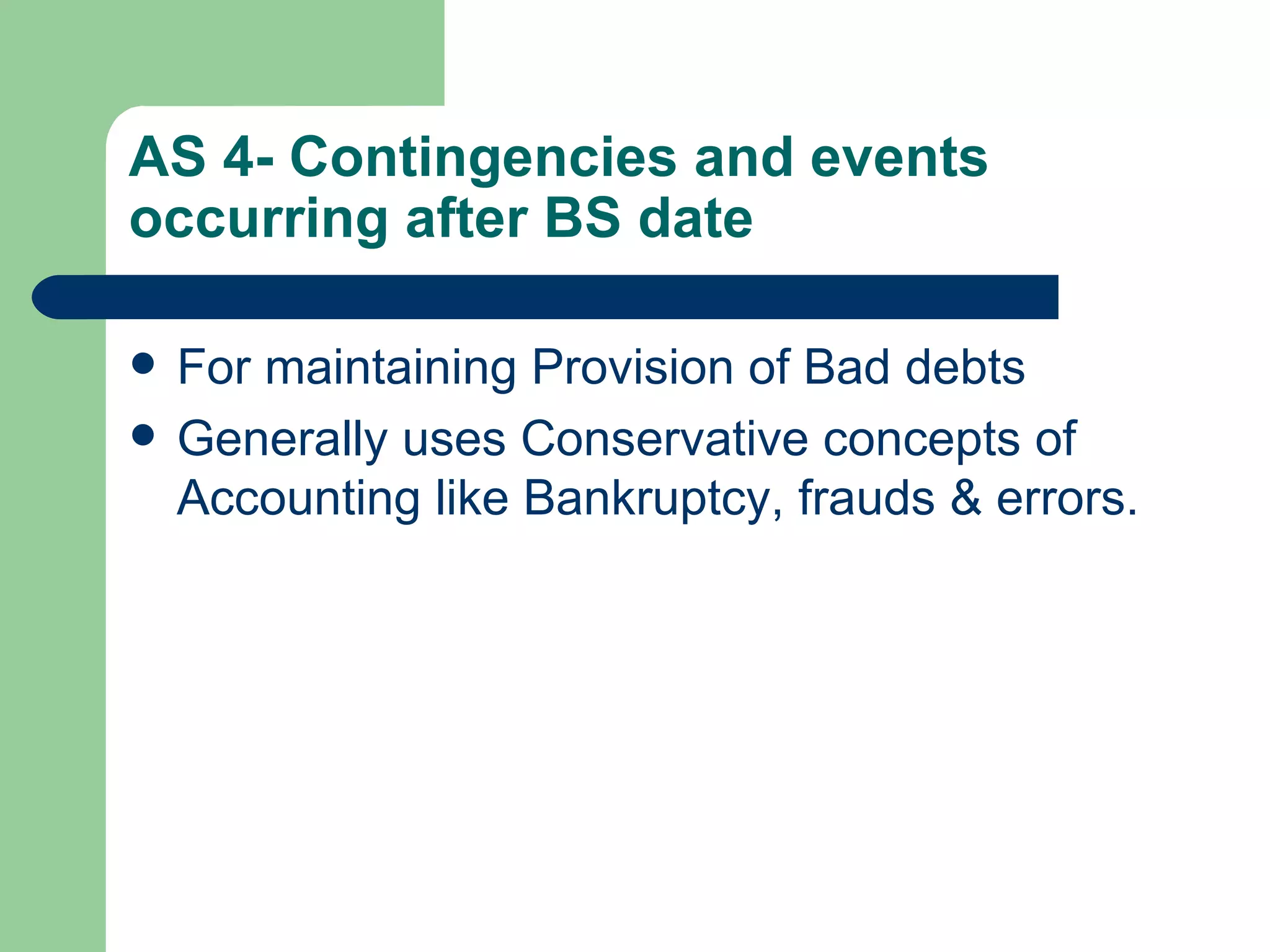

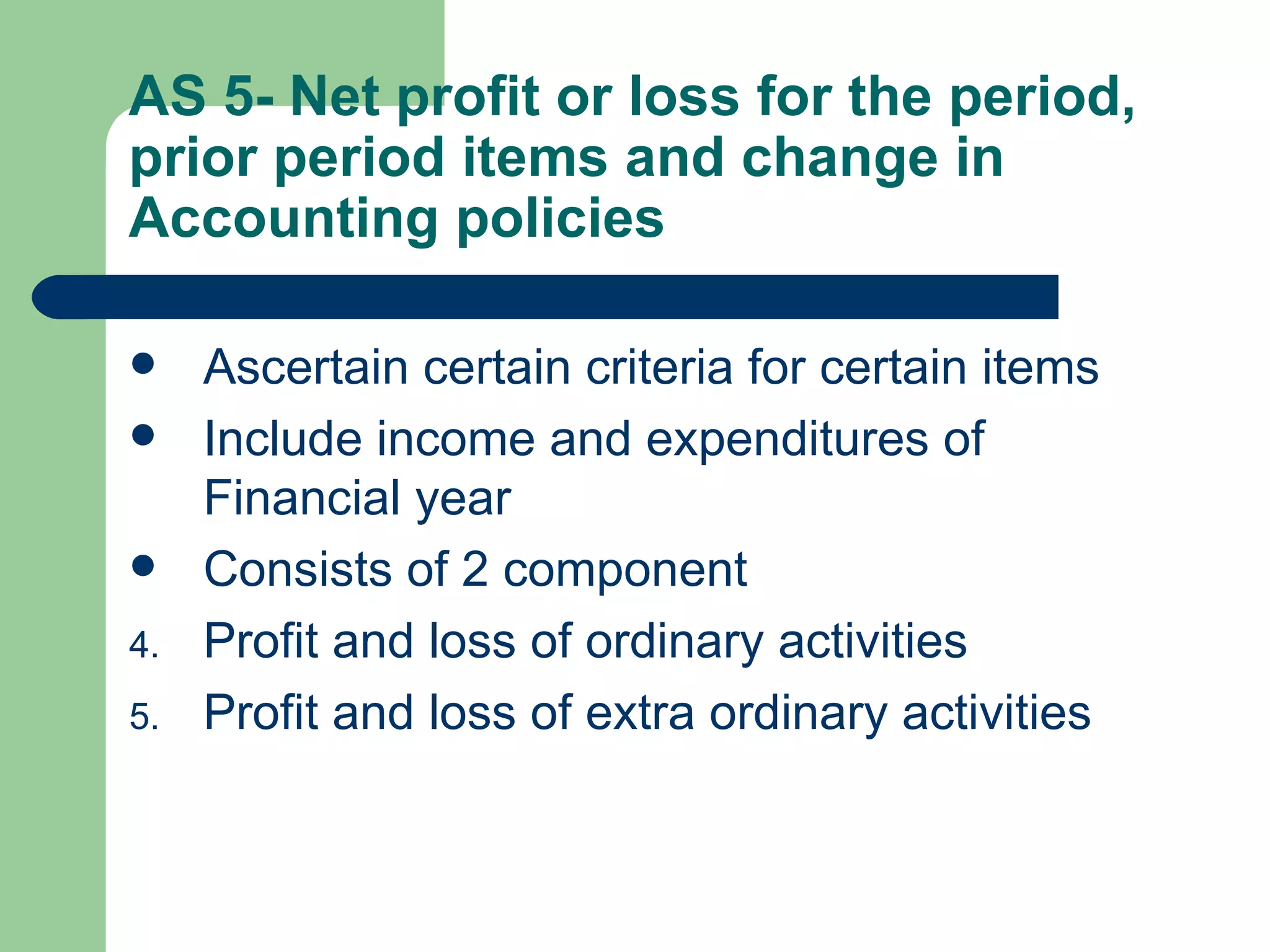

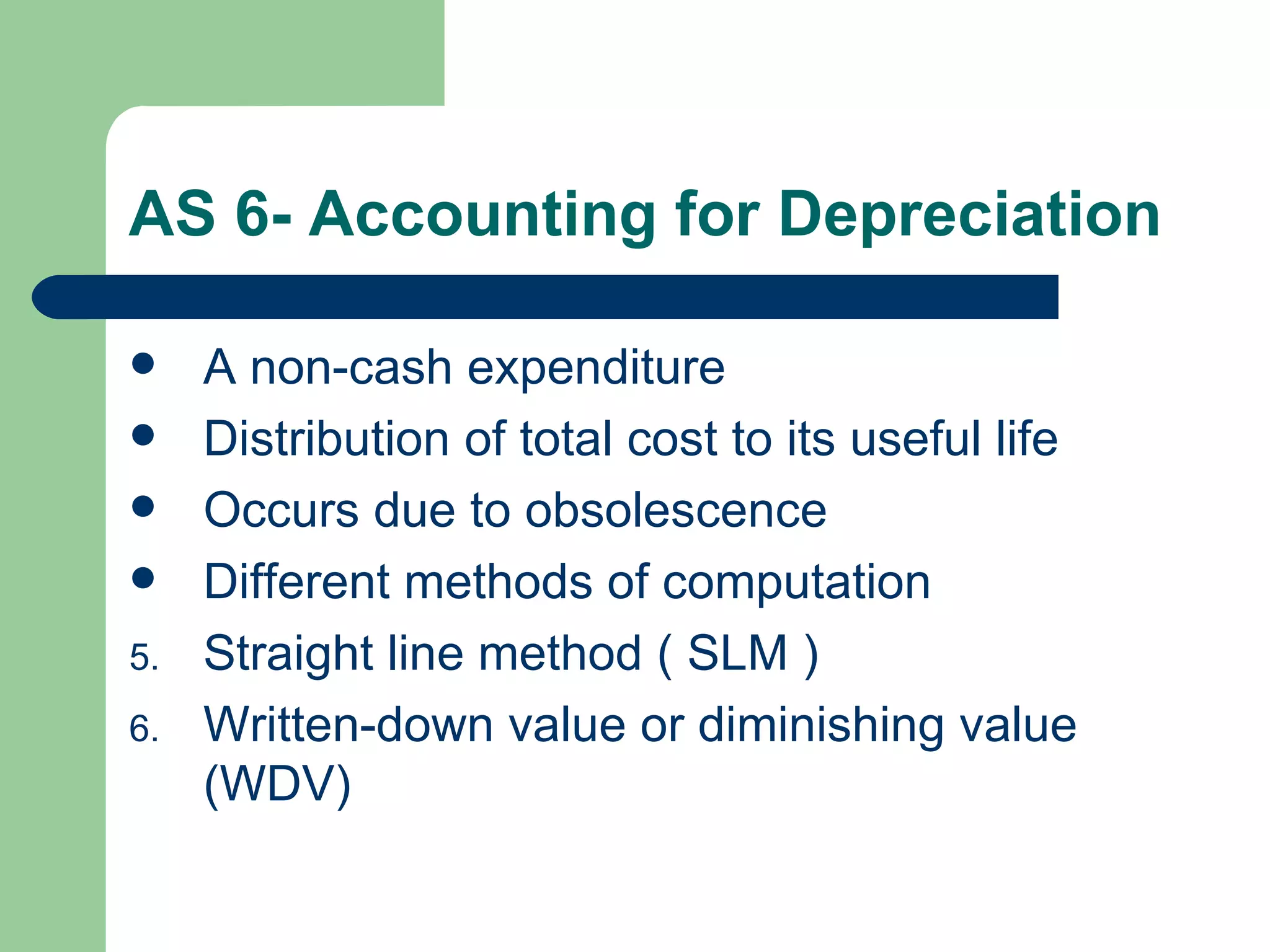

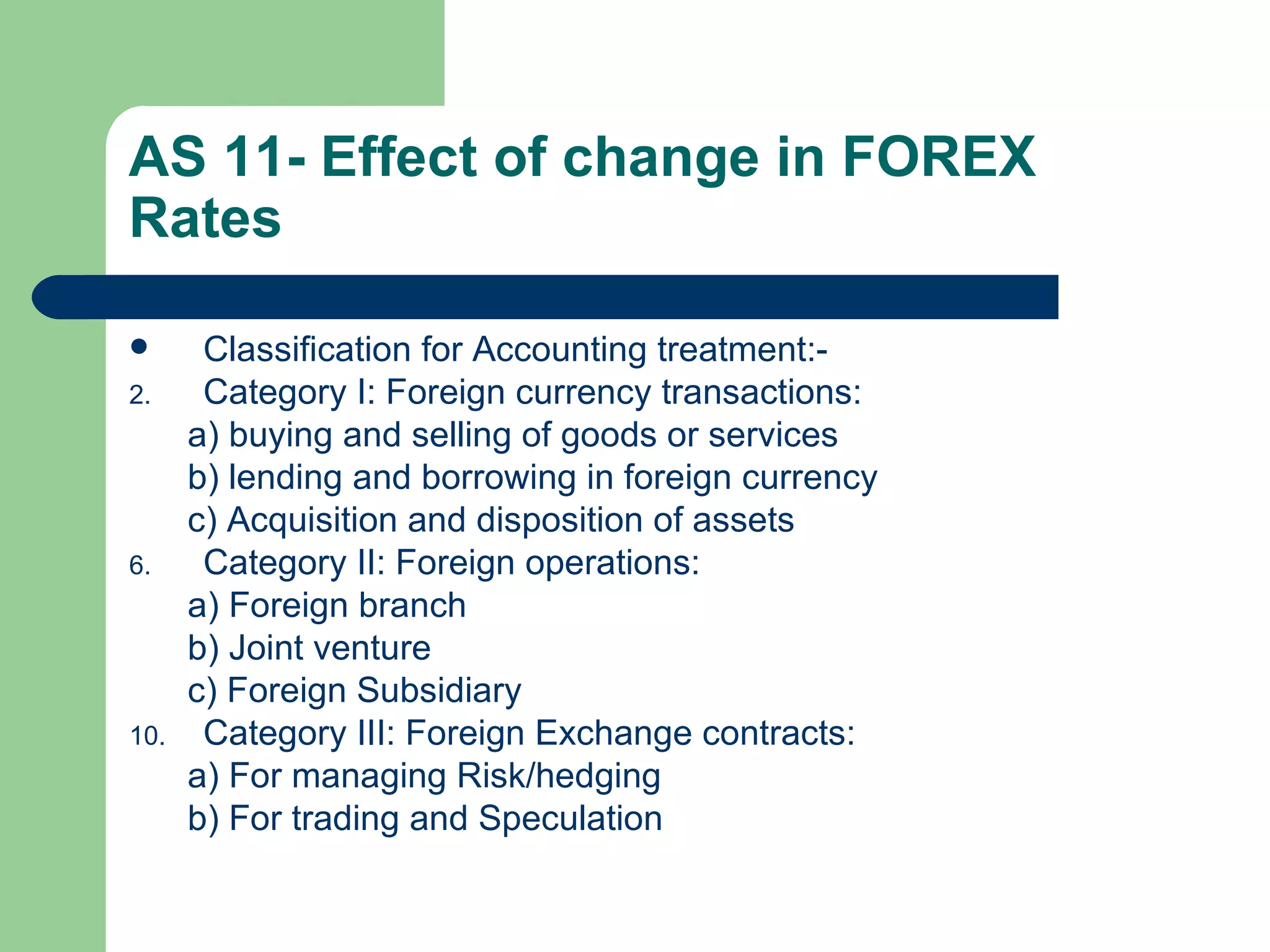

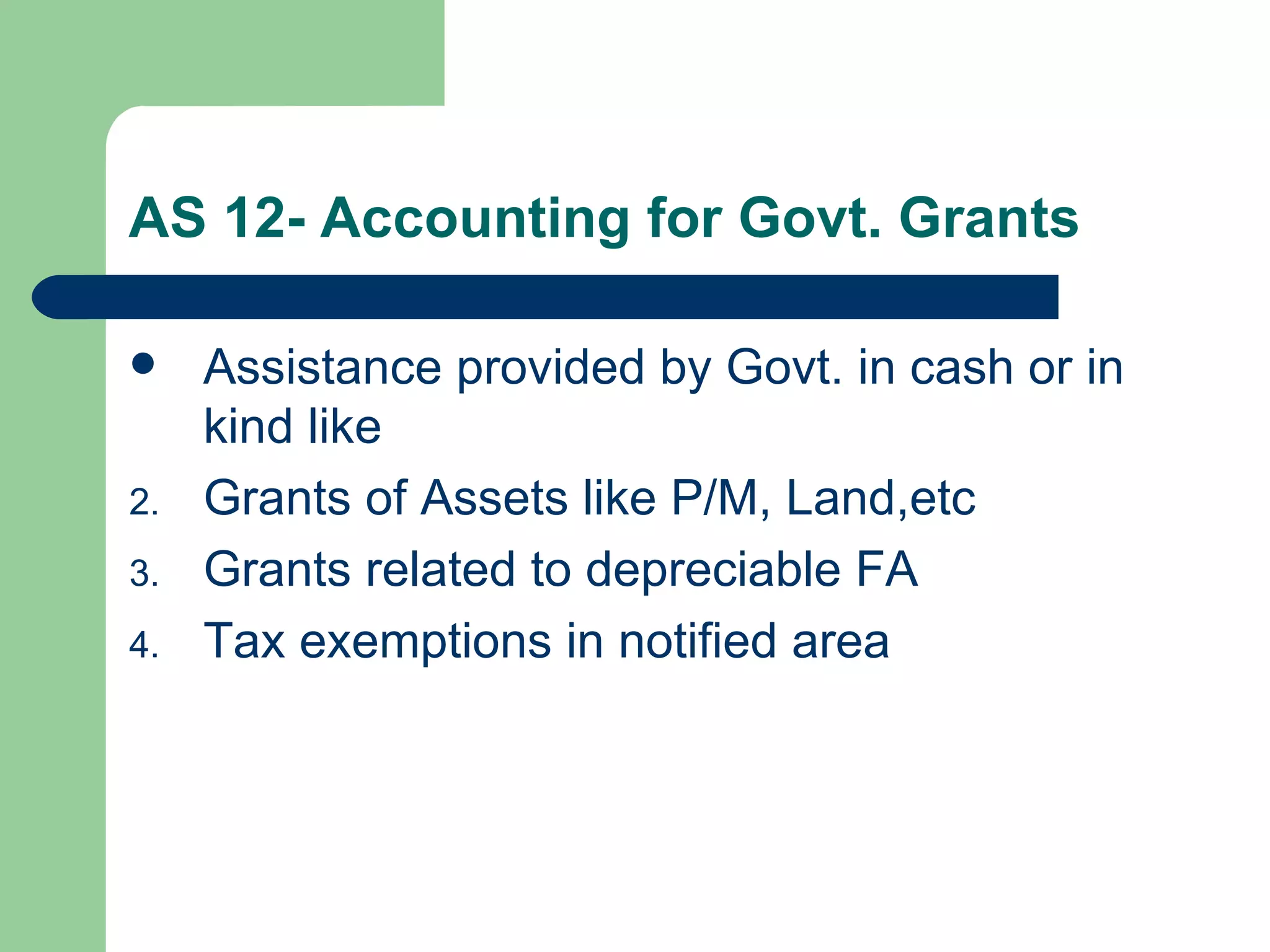

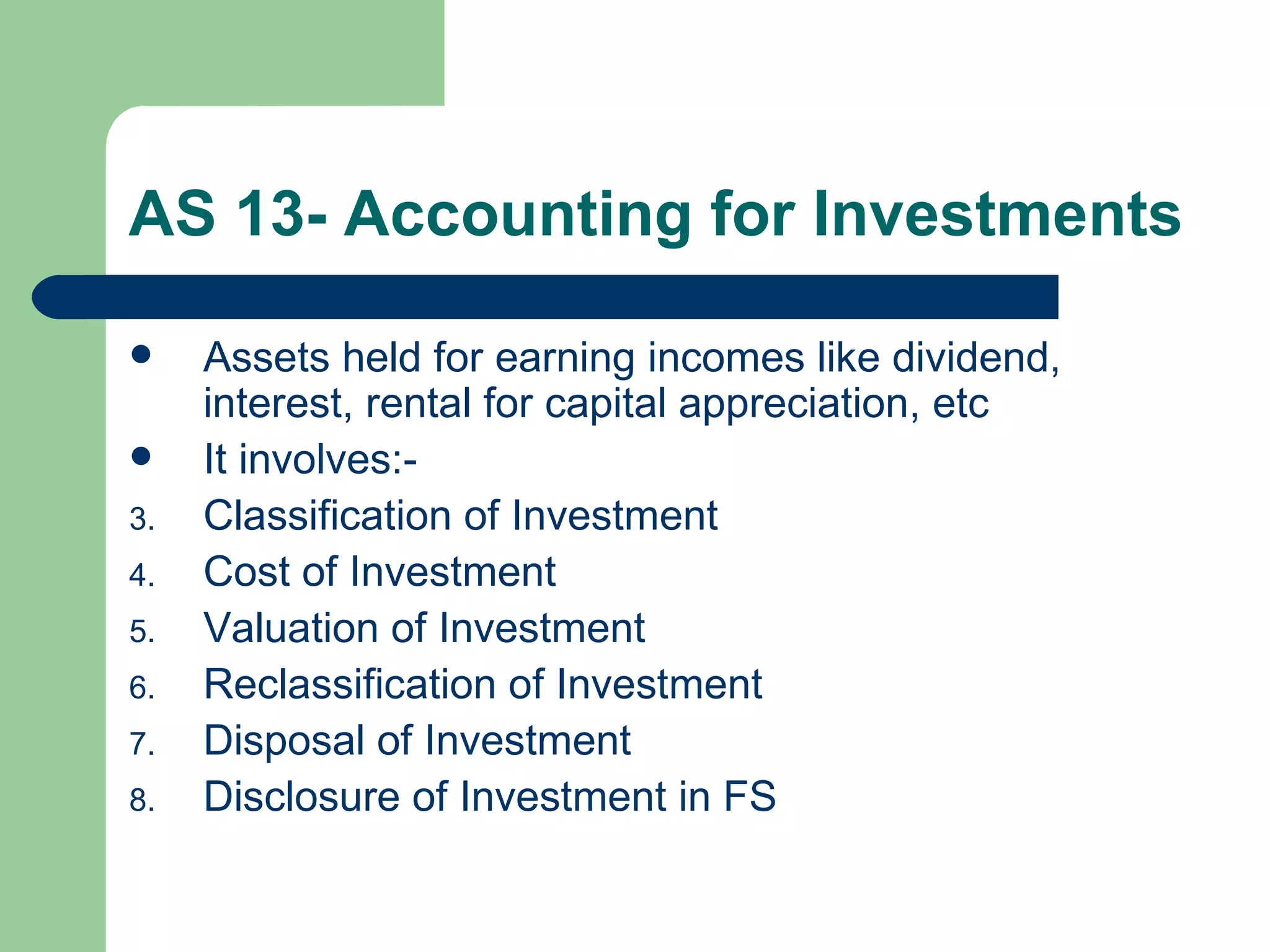

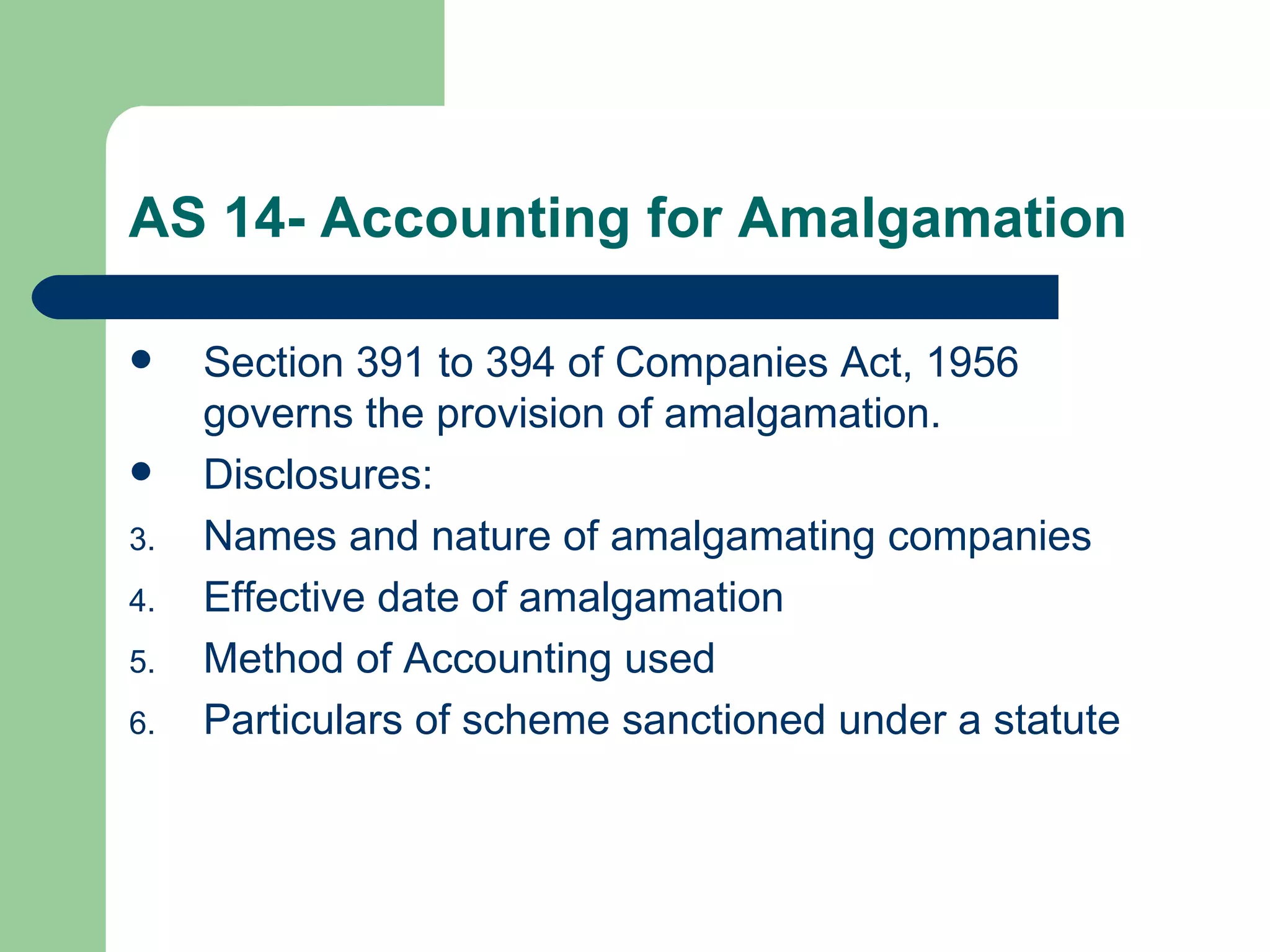

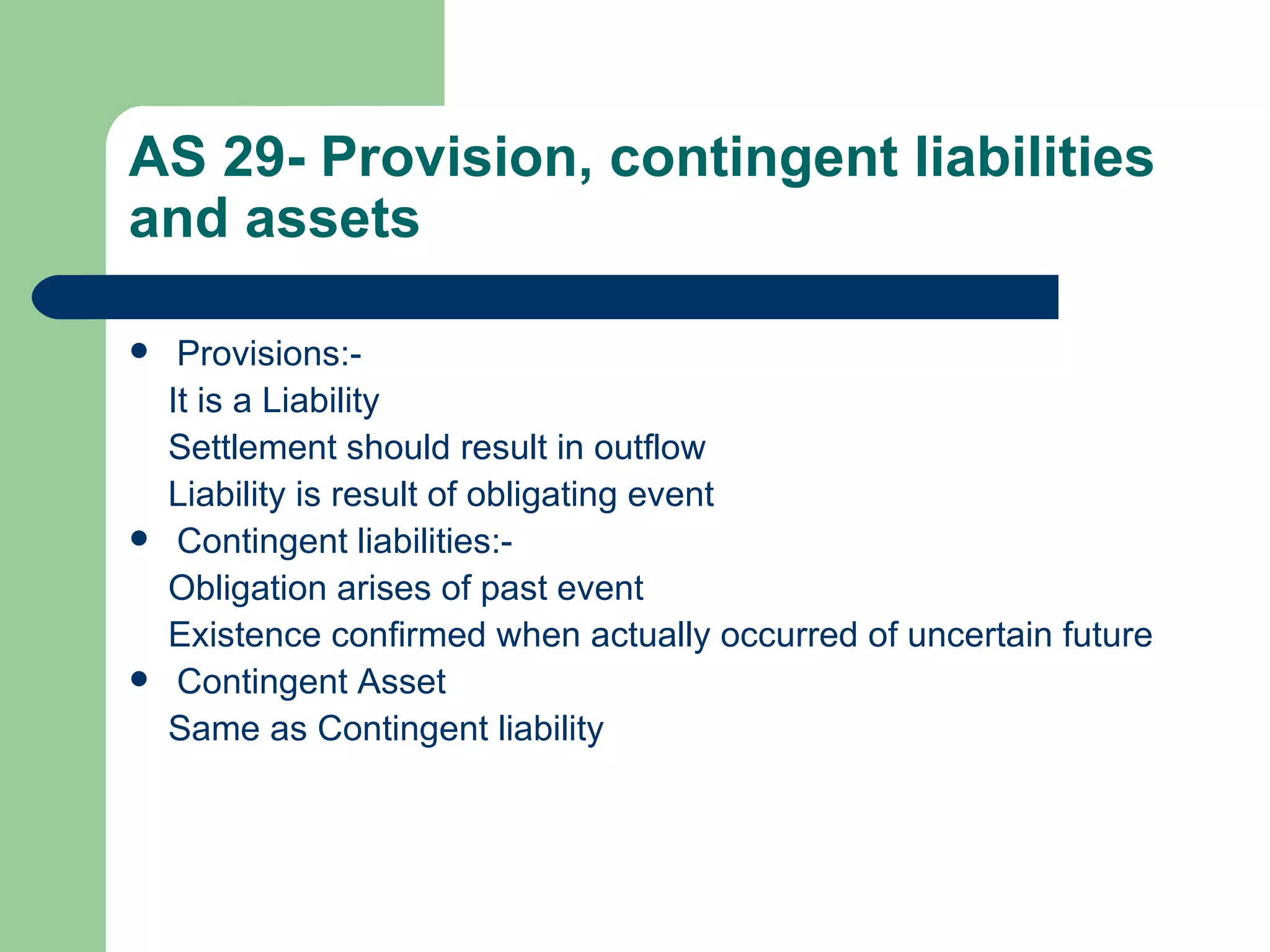

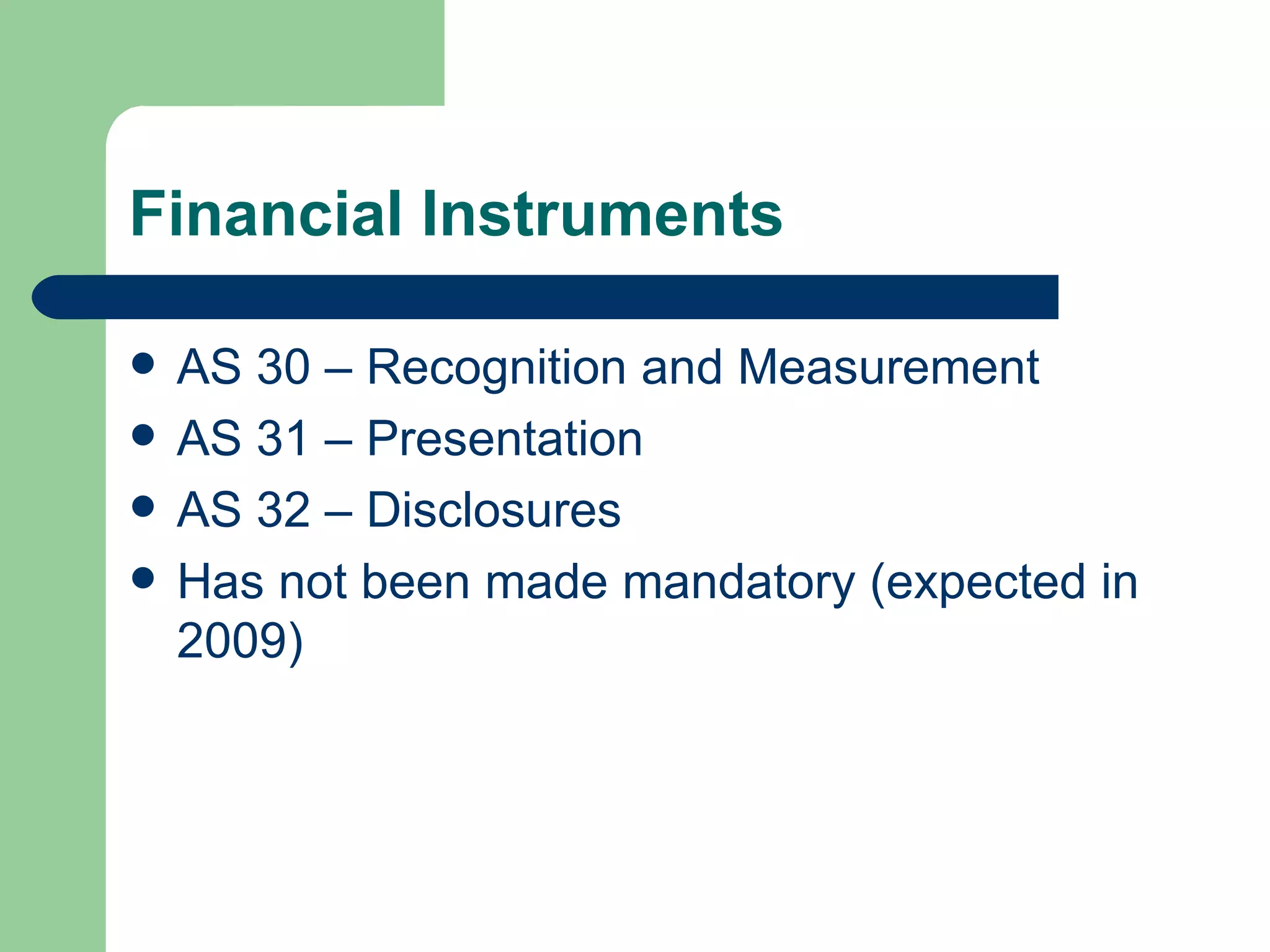

The document provides an overview of accounting standards in India and other countries. It discusses 32 accounting standards issued by the Institute of Chartered Accountants of India that are based on the 41 International Financial Reporting Standards. The standards cover various topics such as disclosure of accounting policies, treatment of inventories, cash flow statements, revenue recognition, accounting for fixed assets, foreign exchange rates, and financial instruments. The objectives, evolution, and key aspects of many individual accounting standards are summarized.