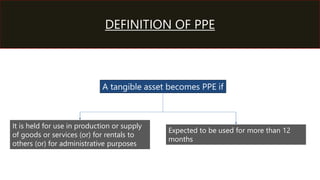

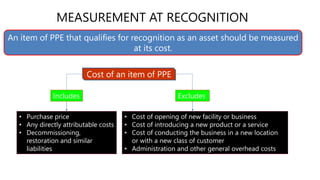

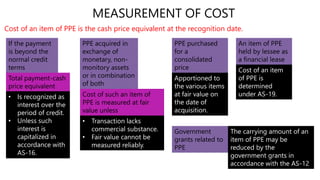

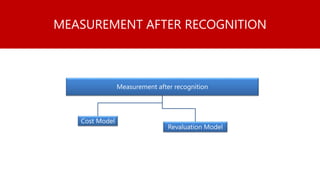

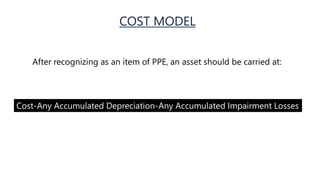

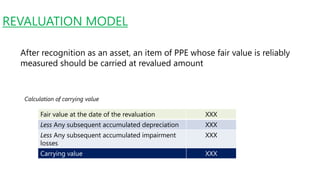

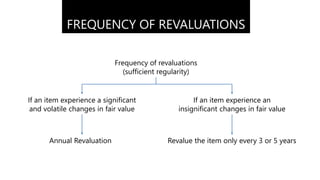

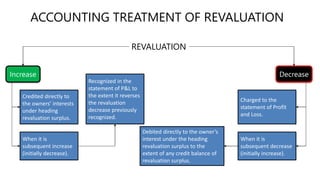

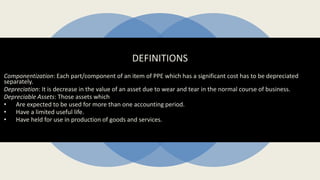

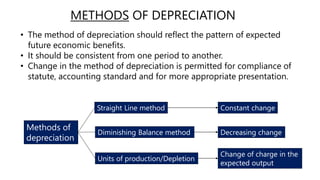

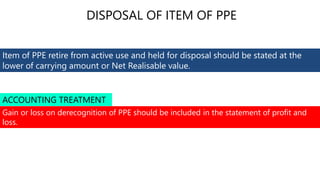

This document summarizes Accounting Standard 10 on Property, Plant and Equipment. It describes the objectives, scope, definitions and accounting treatment for PPE. Key points include: the standard establishes principles for recognition, measurement, presentation and disclosure of PPE; assets qualifying as PPE must be held for use in production or supply of goods/services and have a useful life of more than one year; PPE is initially measured at cost and subsequently using either the cost or revaluation model; depreciation is charged over the useful life of an asset using methods like straight line or diminishing balance; and gains or losses on disposal of PPE are included in profit or loss.

![02;_FR_TOPIC_2-_IAS_16[1].ppt fffhddgffdfd](https://cdn.slidesharecdn.com/ss_thumbnails/02frtopic2-ias161-250711045807-5a4e170c-thumbnail.jpg?width=640&height=640&fit=bounds)